|

시장보고서

상품코드

1850393

어카운터블 케어 솔루션 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Accountable Care Solutions - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

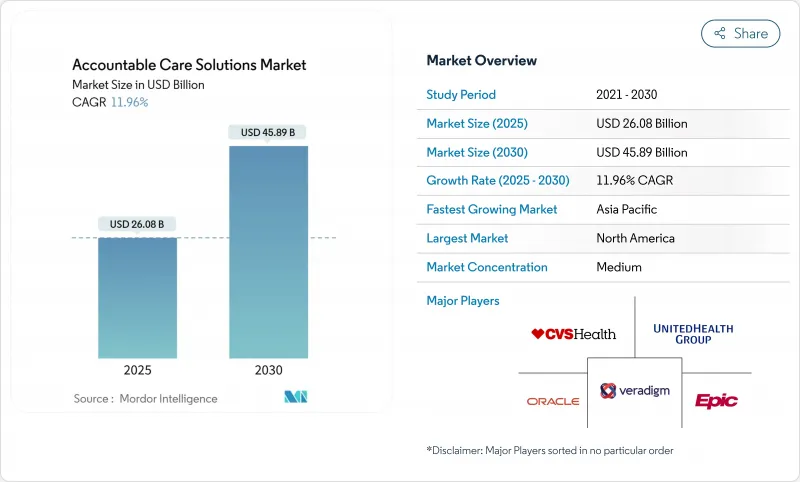

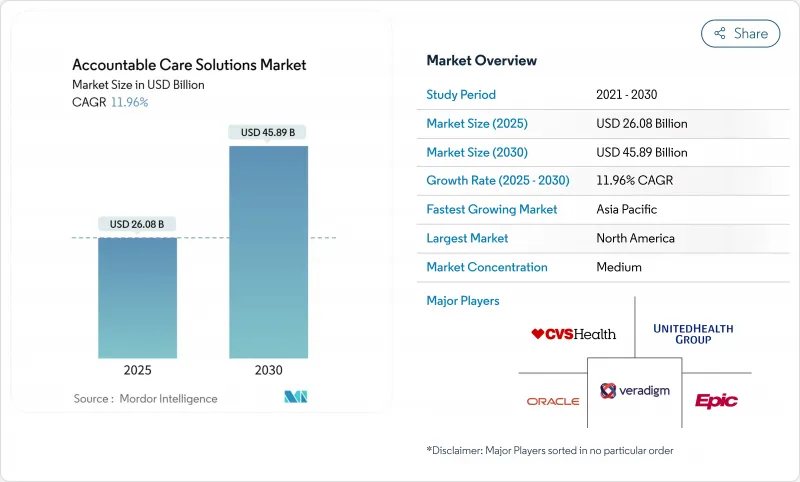

어카운터블 케어 솔루션 시장 규모는 2025년에 260억 8,000만 달러, 2030년에는 458억 9,000만 달러에 달할 것으로 예측되며, CAGR은 11.96%를 나타낼 전망입니다.

메디케어 & 메디케이드 서비스 센터(CMS)는 2030년까지 기존의 메디케어 수혜자 모두를 어카운터블 케어 관계에 두도록 규제 압력을 가하고 있으며, 이것이 수요를 지지하고 있습니다. 클라우드 퍼스트 전략은 현재 의료 시스템 1개당 연간 평균 지출액이 3,800만 달러로 AI 중심의 애널리틱스에 필요한 확장성이 높은 인프라를 제공합니다. 헬스케어 빅데이터 플랫폼의 광범위한 도입으로 의료 제공 조직의 89%가 이미 인공지능을 사용하여 임상 및 관리 업무를 간소화하고 투자가 더욱 가속화되고 있습니다. 공급자가 피 포 서비스에서 가치 기반 상환으로 전환함에 따라 임상, 재무 및 집단 건강 워크 플로우를 조정하는 통합 플랫폼이 격리 된 포인트 솔루션을 대체합니다. 선도적인 벤더들이 클라우드 네이티브 플랫폼을 통해 점유율을 통합하고 있기 때문에 경쟁력은 완만하지만, 소규모 진출기업은 전문적인 분석과 지역별 컴플라이언스에 강점을 가지고 차별화를 도모할 여지가 있습니다.

세계의 어카운터블 케어 솔루션 시장 동향과 통찰

밸류 베이스 케어와 진료 보상 개혁의 의무화

CMS는 현재 1,120만 명이 넘는 기존의 메디케어 수혜자의 케어를 관리하는 476개의 어카운터블 케어 조직(ACO)을 세고, 결과에 연계된 결제로의 명확한 시프트를 보여주고 있습니다. ACO 1차 케어 플렉스 모델과 같은 새로운 프로그램은 충분한 서비스를 받지 못한 지역에서 1차 케어의 현대화를 위한 선행 투자가 됩니다. 민간 보험 회사와 메디케이드 프로그램이 이러한 모델을 복제하고 메디케어 이외의 어카운터블 케어 솔루션 시장을 확대하고 있습니다. ACO REACH의 프레임 워크는 비용 관리와 함께 공정성 의무화를 추가하여 가치 기반 관리의 성숙 단계를 보여줍니다. 서비스 수수료에 집착하는 제공업체는 환급금이 공유 저축과 한도 결제로 전환됨에 따라 마진이 줄어드는 것을 볼 수 있습니다.

증가하는 건강 관리 및 빅 데이터 분석

이미 병원의 대부분은 임상 판단에 정보를 제공하기 위해 예측 모델에 의존하고 있으며, 의료 AI의 자금 조달액은 2024년에 110억 달러로 증가했으며 대부분의 자본은 관리 자동화를 목표로 하고 있습니다. 최신 애널리틱스 플랫폼은 청구 데이터, 임상 데이터 및 사회적 결정 데이터를 캡처하고 거의 실시간으로 위험을 예측하고 관리 갭을 채웁니다. 어카운터블 엔티티의 경우, 고위험 환자의 조기 식별은 회피 가능한 입원을 줄이고 품질 점수와 공유 저축 가능성을 향상시킵니다. 데이터 세트가 풍부해짐에 따라 실시간 대시보드는 임상의가 아웃리치 우선순위를 결정하는 데 도움을 주며, 어카운터블 케어 솔루션 시장에서 통합 플랫폼의 가치 제안을 강화하고 있습니다.

데이터 프라이버시 및 사이버 보안 취약점

헬스케어에서는 2024년에 677건의 대규모 정보 유출이 발생하여 1억 8,240만 명의 기록이 유출되었습니다. 체인지 헬스케어의 랜섬웨어 사건만으로도 1억명 이상의 환자가 영향을 받고 상호 연결된 플랫폼 전체의 체계적 리스크가 부각되었습니다. 정보 유출의 평균 비용은 488만 달러에 달하여 법적 책임에 대한 우려가 높아졌습니다. 규제 당국은 보안의 단맛에 벌칙을 부과하는 새로운 상호 운용성과 사이버 보안의 기준을 최종 결정함으로써 이에 대응하고, 벤더는 방어 강화를 강요했습니다.

부문 분석

2024년 매출액의 62.34%를 솔루션이 차지하고 임상, 재무, 집단 건강 기능을 연결하는 통합 플랫폼이 지지되고 있는 것을 알 수 있습니다. 전문가 교육, 워크플로 재설계, 지속적인 최적화가 플랫폼 가동 후에 필수적이기 때문에 서비스가 CAGR 13.15%로 소프트웨어를 능가합니다. ACO가 리스크 조정 알고리즘 및 규제 당국에 대한 보고서의 미세 조정을 위해 외부 지원을 요청함에 따라 서비스의 조정, 관리 및 솔루션 시장 규모가 확대될 것으로 예측됩니다. Epic Systems사가 2024년에 176개 시설을 추가한 것은 종합적 플랫폼으로의 통합 파도를 보여줍니다.

서비스 성장은 지속적인 변경 관리가 없으면 소프트웨어만으로는 성과를 올릴 수 없다는 인식을 반영합니다. 의료 시스템은 애널리틱스 애즈 서비스, 가상 커맨드 센터, 매니지드 포퓰레이션 헬스 오퍼레이션을 계약하고 있습니다. 이러한 계약은 자본 예산을 슬림화하고 성과 지표에 대한 어카운빌리티를 솔루션 파트너로 전환하고, 어카운터블 케어 솔루션 시장의 궤도를 강화합니다.

전자 차트는 2024년 매출의 29.51%를 차지했으며, 모든 다운스트림 워크플로우의 데이터 수집을 지원합니다. 그러나 인구 관리 및 관리 관리는 2030년까지 13.48%의 연평균 복합 성장률(CAGR)로 성장하여 어카운터블 케어 솔루션 시장의 주요 엔진이 됩니다. 카이저 퍼머넌트가 Innovaccer의 포퓰레이션 헬스 플랫폼을 캘리포니아 전역에 배포하기로 결정한 것은 이 사전 활동적인 조정에 대한 축족을 강조하는 것입니다.

분석, 수익주기 자동화 및 환자 참여 모듈도 조직이 위험 및 리소스 사용에 대한 종단 간 가시성을 우선시함에 따라 기세가 증가하고 있습니다. AI 기반 수익주기 도구는 이미 많은 병원에서 운영되고 있으며 사전 승인을 간소화하고 거부를 줄였습니다. 이러한 상호연결된 용도는 EHR을 기반으로 견고하게 하고 있지만, 어카운터블 케어 솔루션 시장에서 가치 기반의 상환을 성공으로 이끄는 임팩트가 큰 집단 건강 워크플로우를 향해 새로운 지출을 뒷받침하고 있습니다.

지역 분석

북미는 2024년 세계 매출의 42.57%를 창출했습니다. CMS 규정에 따라 기존 메디케어 가입자의 53.4%가 이미 어카운터블 케어 계약 하에 있습니다. 2030년까지 연평균 복합 성장률(CAGR) 11.04%의 지역 성장은 초기 구축에서 최적화로의 전환을 나타냅니다. 클라우드로의 마이그레이션, AI를 통합한 포퓰레이션 헬스, ACO REACH와 같은 공정성을 중시한 모델이 기존 플랫폼의 업데이트 사이클을 촉진합니다. Highmark Health와 같은 대규모 시스템은 현재 관리 및 임상 분석을 위해 Epic과 Google Cloud를 연결하여 생태계 수준의 협업을 시연하고 있습니다.

아시아태평양은 CAGR 12.72%에서 가장 급성장하고 있는 지역으로, 각국의 디지털 헬스 청사진과 신흥 기업의 자금 조달이 추진하고 있습니다. 동남아시아만으로도 인도네시아의 Halodoc사가 1억 달러의 라운드를 완료함으로써 2024년에 61억 달러의 디지털 헬스 수익을 전망하고 있습니다. 태국, 호주, 싱가포르 정부는 인공지능, 원격 의료 및 IoT 모니터링에 자본을 주입하고 다양한 규제 환경에 솔루션을 현지화하는 공급업체에게 비옥 한 토양을 만들고 있습니다. 데이터 주권에 관한 규칙은 지역에 따라 크게 다르므로 클라우드 유연성은 매우 중요합니다.

유럽에서는 통합 의료 의무화와 GDPR(EU 개인정보보호규정) 준수가 조달 기준을 형성하고 CAGR 11.56%로 성장하고 있습니다. 독일의 건강 관리를 위한 국가 클라우드 전략은 데이터 주권에 대한 엄격한 기준을 설정하면서도 공공 기관의 지도에 따라 도입이 가속화되는 방법을 보여줍니다. 한편 중동 및 아프리카는 CAGR 12.19%로 성장하여 병원의 디지털화와 국가의 의료 정보 교환에 대한 투자를 반영하고 있습니다. 남미는 CAGR 11.83%로 성장해 각국이 보험제도를 근대화하고, 원격의료에 보조금을 내고, 어카운터블 케어의 원칙을 이용하여 만성질환의 부담을 관리하고 있습니다. 이 지리적 확산은 규제 프레임워크이 다르다는 것, 어카운터블 케어 솔루션 시장이 '더 나은 성과를 보다 저비용으로' 하는 공통의 목표에 합치하고 있음을 증명하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 가치에 기초한 케어와 진료 보수의 강제 개혁

- 헬스케어 빅데이터 분석 증가

- 헬스케어비의 상승을 억제할 필요성

- 확장 가능한 클라우드 퍼스트 IT 스택으로 빠르게 전환

- AI를 활용한 사회적 결정 요인에 의한 리스크층별화의 이용 사례

- 기술과 MSO 서비스를 통합한 공급자 지원 벤처 플랫폼

- 시장 성장 억제요인

- 데이터 프라이버시 및 사이버 보안 취약점

- 레거시에서 디지털로의 변혁을 위한 고액의 CAPEX/OPEX

- 서로 다른 시스템 간의 단편화된 상호 운용성

- EHR 작업량 및 경고 피로로 인한 임상의 소진

- 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 컴포넌트별

- 솔루션

- 서비스

- 용도별

- 전자건강기록

- 헬스케어 분석

- 인구·케어 관리

- 수익주기 및 클레임 관리

- 지불 및 리스크 조정

- 의료 정보 교환(HIE)

- 환자 참여 및 포털

- 기타 용도

- 전개 모드별

- 클라우드 기반

- On-Premise

- 하이브리드

- 조직 규모별

- 대기업

- 중소기업

- 최종 사용자별

- 의료 제공자

- 헬스케어 지불자

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- Competitive Benchmarking

- 시장 점유율 분석

- 기업 프로파일

- Aledade, Inc.

- Arcadia Solutions, LLC

- athenahealth, Inc.

- Conifer Health Solutions, LLC

- CVS Health Corporation

- eClinicalWorks, LLC

- Epic Systems Corporation

- Evolent Health LLC

- Exlservice Holdings, Inc.

- Health Catalyst, Inc.

- Lumeris, Inc.

- McKesson Corporation

- Medecision, Inc.

- Merative LP

- Oracle Corporation

- Persivia, Inc.

- Signify Health, Inc.

- UnitedHealth Group

- Veradigm, Inc.

- ZeOmega, Inc.

제7장 시장 기회와 장래의 전망

SHW 25.11.11The accountable care solutions market size is valued at USD 26.08 billion in 2025 and is forecast to reach USD 45.89 billion by 2030, translating into an 11.96% CAGR.

Regulatory pressure from the Centers for Medicare & Medicaid Services (CMS) to place every Traditional Medicare beneficiary in an accountable care relationship by 2030 anchors demand. Cloud-first strategies, now averaging USD 38 million in annual spending per health system, supply the scalable infrastructure needed for AI-driven analytics. Widespread deployment of healthcare big-data platforms-in which 89% of provider organizations already use artificial intelligence to simplify clinical and administrative work-further accelerates investment. As providers move from fee-for-service to value-based reimbursement, integrated platforms that coordinate clinical, financial, and population-health workflows replace isolated point solutions. Competitive momentum remains moderate because large vendors consolidate share through cloud-native platforms, yet smaller entrants still find room to differentiate on specialized analytics or regional compliance strengths.

Global Accountable Care Solutions Market Trends and Insights

Mandatory value-based-care and reimbursement reforms

CMS now counts 476 accountable care organizations (ACOs) that collectively manage care for over 11.2 million Traditional Medicare beneficiaries, underscoring a clear shift to outcome-linked payment. New programs such as the ACO Primary Care Flex Model provide upfront investment for primary-care modernization in underserved communities. Commercial insurers and Medicaid programs replicate these models, broadening the accountable care solutions market beyond Medicare. The ACO REACH framework adds equity mandates alongside cost controls, signaling a mature stage for value-based care. Providers that cling to fee-for-service see shrinking margins as reimbursement pivots toward shared savings and capitated payments.

Growing volumes of healthcare big-data analytics

A large percent of hospitals already rely on predictive models to inform clinical decisions, and healthcare AI funding climbed to USD 11 billion in 2024 with most capital aimed at administrative automation. Modern analytics platforms ingest claims, clinical, and social-determinant data to forecast risk and close care gaps in near real time. For accountable entities, earlier identification of high-risk patients trims avoidable admissions, improving both quality scores and shared-savings potential. As datasets grow richer, real-time dashboards help clinicians prioritize outreach, reinforcing the value proposition of integrated platforms within the accountable care solutions market.

Data-privacy & cyber-security vulnerabilities

Healthcare experienced 677 large-scale breaches in 2024, exposing records of 182.4 million people and raising hesitation around expansive cloud deployments. The Change Healthcare ransomware incident alone affected more than 100 million patients and highlighted systemic risk across interconnected platforms. Average breach costs reached USD 4.88 million, amplifying liability concerns. Regulators responded by finalizing new interoperability and cybersecurity standards that impose penalties for lax security, forcing vendors to fortify defenses.

Other drivers and restraints analyzed in the detailed report include:

- Need to curb escalating healthcare expenditures

- Rapid migration toward scalable cloud-first IT stacks

- High CAPEX/OPEX for legacy-to-digital transformation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions generated 62.34% of 2024 revenue, showing that organizations favor unified platforms linking clinical, financial, and population-health functions. Services will outpace software with a 13.15% CAGR because expert training, workflow redesign, and ongoing optimization are indispensable once platforms go live. The accountable care solutions market size for services is projected to widen as ACOs seek external help to fine-tune risk-adjustment algorithms and regulatory reporting. Epic Systems' addition of 176 facilities in 2024 illustrates a consolidation wave toward comprehensive platforms.

Services growth reflects recognition that software alone cannot deliver outcomes without sustained change management. Health systems contract for analytics-as-a-service, virtual command centers, and managed population-health operations. These arrangements keep capital budgets lean and shift accountability for performance metrics to solution partners, reinforcing the trajectory of the accountable care solutions market

Electronic health records hold 29.51% of 2024 revenue, anchoring data capture for every downstream workflow. Yet population & care management will rise at a 13.48% CAGR to 2030, becoming the primary engine of the accountable care solutions market. Kaiser Permanente's decision to deploy Innovaccer's population-health platform across California underscores this pivot toward proactive coordination.

Analytics, revenue-cycle automation, and patient-engagement modules also gain momentum as organizations prioritize end-to-end visibility into risk and resource use. AI-based revenue-cycle tools are already live in a large number of hospitals, streamlining pre-authorization and reducing denials. These interconnected applications cement EHRs as a foundation but push new spending toward high-impact population-health workflows that drive value-based reimbursement success within the accountable care solutions market.

The Accountable Care Solutions Market Report is Segmented by Component (Solutions and Services), Application (Electronic Health Records, Healthcare Analytics, and More), Deployment (On-Premise and More), Organization Size (Large Enterprises and SMEs), End User (Healthcare Providers and Healthcare Payers), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 42.57% of global revenue in 2024, supported by CMS rules that already place 53.4% of Traditional Medicare members under accountable care contracts. Regional growth of 11.04% CAGR through 2030 represents a shift from initial build-out to optimization. Cloud migration, AI-embedded population health, and equity-focused models such as ACO REACH drive refresh cycles of existing platforms. Large systems like Highmark Health now link Epic and Google Cloud for administrative and clinical analytics, demonstrating ecosystem-level collaboration.

Asia-Pacific is the fastest-growing territory at 12.72% CAGR, propelled by national digital-health blueprints and startup funding. Southeast Asia alone projects USD 6.1 billion in digital-health revenue for 2024, aided by Indonesia's Halodoc closing a USD 100 million round. Governments in Thailand, Australia, and Singapore inject capital into AI, telemedicine, and IoT monitoring, creating fertile ground for vendors that localize solutions to diverse regulatory settings. Cloud flexibility is critical because data sovereignty rules vary widely across the region.

Europe expands at 11.56% CAGR as integrated-care mandates and GDPR compliance shape procurement criteria. Germany's national cloud strategy for healthcare shows how public-sector guidance accelerates adoption while setting strict data-sovereignty bars. Meanwhile, the Middle East & Africa advance at 12.19% CAGR, reflecting sovereign investments in hospital digitization and national health-information exchanges. South America grows at 11.83% CAGR as countries modernize insurance schemes and subsidize telehealth, using accountable care principles to manage chronic-disease burdens. The geographic spread proves that, while regulatory frameworks differ, the accountable care solutions market meets a common goal: better outcomes at lower cost.

- Aledade, Inc.

- Arcadia Solutions, LLC

- Athenahealth

- Conifer Health Solutions

- CVS Health

- eClinicalWorks

- Epic Systems

- Evolent Health LLC

- Exlservice Holdings, Inc.

- Health Catalyst, Inc.

- Lumeris, Inc.

- Mckesson

- Medecision, Inc.

- Merative L.P.

- Oracle

- Persivia, Inc.

- Signify Health, Inc.

- United Health Group

- Veradigm, Inc.

- ZeOmega, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mandatory value-based-care and reimbursement reforms

- 4.2.2 Growing volumes of healthcare big-data analytics

- 4.2.3 Need to curb escalating healthcare expenditures

- 4.2.4 Rapid migration toward scalable cloud-first IT stacks

- 4.2.5 AI-powered social-determinants risk-stratification use cases

- 4.2.6 Provider-enablement venture platforms integrating tech + MSO services

- 4.3 Market Restraints

- 4.3.1 Data-privacy & cyber-security vulnerabilities

- 4.3.2 High CAPEX/OPEX for legacy-to-digital transformation

- 4.3.3 Fragmented interoperability across disparate systems

- 4.3.4 Clinician burnout due to EHR workload & alert-fatigue

- 4.4 Technological Outlook

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.2 Services

- 5.2 By Application

- 5.2.1 Electronic Health Records

- 5.2.2 Healthcare Analytics

- 5.2.3 Population & Care Management

- 5.2.4 Revenue Cycle & Claims Management

- 5.2.5 Payment & Risk Adjustment

- 5.2.6 Health Information Exchange (HIE)

- 5.2.7 Patient Engagement & Portals

- 5.2.8 Other Applications

- 5.3 By Deployment Mode

- 5.3.1 Cloud-Based

- 5.3.2 On-Premise

- 5.3.3 Hybrid

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 SMEs

- 5.5 By End-User

- 5.5.1 Healthcare Providers

- 5.5.2 Healthcare Payers

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Competitive Benchmarking

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Aledade, Inc.

- 6.4.2 Arcadia Solutions, LLC

- 6.4.3 athenahealth, Inc.

- 6.4.4 Conifer Health Solutions, LLC

- 6.4.5 CVS Health Corporation

- 6.4.6 eClinicalWorks, LLC

- 6.4.7 Epic Systems Corporation

- 6.4.8 Evolent Health LLC

- 6.4.9 Exlservice Holdings, Inc.

- 6.4.10 Health Catalyst, Inc.

- 6.4.11 Lumeris, Inc.

- 6.4.12 McKesson Corporation

- 6.4.13 Medecision, Inc.

- 6.4.14 Merative L.P.

- 6.4.15 Oracle Corporation

- 6.4.16 Persivia, Inc.

- 6.4.17 Signify Health, Inc.

- 6.4.18 UnitedHealth Group

- 6.4.19 Veradigm, Inc.

- 6.4.20 ZeOmega, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment