|

시장보고서

상품코드

1851120

항공 엔진용 복합재료 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Aeroengine Composites - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

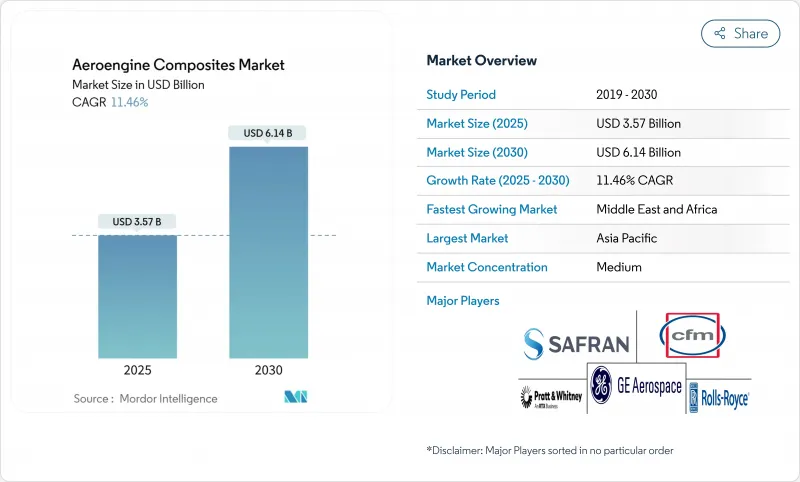

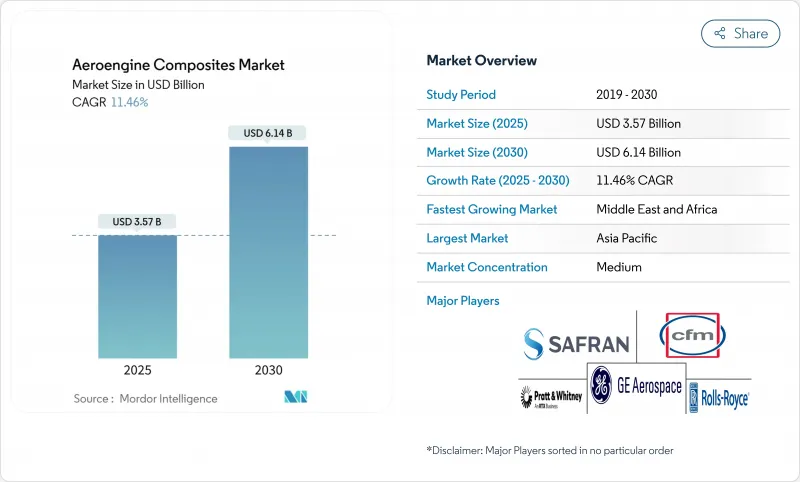

항공 엔진용 복합재료 시장의 2025년 시장 규모는 35억 7,000만 달러로 추정되고, 2030년에는 61억 4,000만 달러에 이를 전망이며, CAGR 11.46%로 성장할 것으로 예측됩니다.

항공기 갱신 증가, 탈탄소화 의무화, 연료 가격 상승으로 항공사 및 엔진 제조업체는 보다 엄격한 배출 규제를 충족하면서 연료 소비를 최대 20% 절감하는 경량 추진 시스템을 요구하고 있습니다. 세라믹 매트릭스 복합재료(CMC)는 이제 1,300℃를 견딜 수 있게 되어 코어 온도의 상승 및 열효율의 개선이 가능하게 되었습니다. 자동화된 섬유 배치와 오토클레이브 밖에서의 경화에 의해 파운드당의 비용이 30% 가까이 저하되어, 복합재가 내로우 바디 프로그램으로 경제적으로 실행 가능하게 되고 있습니다. GE 에어로 스페이스가 2024년에 10%의 납기 부족에 빠진 것으로, 고압 터빈 블레이드 조달의 병목이 노출되었기 때문에 공급망의 탄력성은 여전히 중요합니다.

세계의 항공 엔진용 복합재료 시장 동향 및 인사이트

가볍고 연료 효율적인 추진 시스템으로 이동

항공사는 변동하는 연료 가격을 상쇄하기 위해 15-20%의 연료 절감을 필요로 하며, 나셀의 중량을 삭감하고 바이패스비를 높이는 복합재료에 급속한 축족을 움직이고 있습니다. GE 에어로 스페이스의 RISE 오픈 팬 시연기는 바이패스 비율이 60인 탄소섬유 팬 블레이드를 사용하여 20% CO2 감소를 목표로 하고 있습니다. 에어버스는 100% 지속가능한 항공연료와 결합한 탄소섬유 강화 열가소성 플라스틱 구조의 비행 시험을 실시하고 있으며, 20%의 연료 소비 절감을 약속하고 있습니다. 월별 100대가 넘는 내로우 바디의 생산량은 확장 가능하고 자동화된 복합재료 생산의 긴급성을 높이고 있습니다.

LEAP 및 차세대 항공기 엔진 생산량 확대

4,000대 이상의 항공기가 LEAP 엔진을 탑재해 비행하고 있기 때문에 사프란은 브뤼셀, 하이데라바드, 케레타로, 카사블랑카에 있는 새로운 MRO 시설에 10억 유로(11억 6,000만 달러)를 투자해, 2028년까지 연간 1,200건의 공장 방문에 대응합니다. GE는 6,400만 유로(7,405만 달러)를 LEAP 및 GE9X 프로그램을 지원하는 유럽 테스트 셀 및 공구에 충당했습니다. 고압 터빈 블레이드를 중심으로 한 부품 부족은 269억 달러의 상업 수익에도 불구하고 2024년 엔진 납품을 10% 절감하여 다양한 복합재 공급망의 필요성을 부각시켰습니다.

CMC 취약성 및 검사 복잡성

CMC 팬 블레이드는 세라믹 미세 구조가 충격 하중으로 깨질 수 있으므로 이물질 손상의 위험이 있습니다. 종래의 초음파법이나 X선법에서는 마이크로크랙의 검출이 곤란하기 때문에 OEM은 CT 스캔이나 전문가 트레이닝에 대한 투자를 강요하고 있습니다. 다결정 다이아몬드 공구를 사용하는 새로운 가공 방법은 가공 시간을 70% 단축하기 때문에 자본 비용이 상승하고 소규모 공급업체에게는 채용이 어려워지고 있습니다.

부문 분석

상용 엔진은 2024년에 항공 엔진용 복합재료 시장 점유율의 70.05%를 차지했는데, 이는 수천 개의 LEAP와 GEnx 유닛이 복합재 팬 블레이드와 케이스를 통합하여 최대 20%의 연료 절약을 실현하고 있기 때문입니다. 군사 프로그램과 관련된 항공 엔진용 복합재료 시장 규모는 XA100 클래스의 추진력과 극초음속 실증기가 CMC 슈라우드를 채용하기 때문에 2030년까지 연평균 복합 성장률(CAGR) 12.74%로 가장 급속히 확대될 전망입니다.

비즈니스 제트기와 지역 항공기의 운항 회사는 기술의 하류로의 전환에 따라 복합재를 다용한 엔진의 개수를 시작하고 있습니다. GE 에어로스페이스와 크레이토스 디펜스와 같은 파트너십은 CMC 터빈과 합리적인 생산 방법을 결합한 소형 클래스 엔진을 계획하고 고객 기반을 확장하고 있습니다. 이를 통해 민간 예산과 방위 예산에 걸친 위험이 분산되어 공급업체의 주문 안정성이 향상됩니다.

팬 블레이드는 2024년 매출의 37.98%를 차지했으며, 이는 탄소섬유 구조가 고강성 대 중량을 실현하고 관성을 줄여 추력 응답을 개선하기 때문입니다. 팬 케이스는 13.48%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측되며, 규제 저장 테스트는 복합재 쉘을 선호하므로 저장 하드웨어 항공 엔진용 복합재료 시장 규모를 늘립니다.

슈라우드, 가이드 베인, O-링 씰을 모놀리식 복합재 구조에 통합함으로써 부품 수와 조립 시간을 줄이고 마진을 건전하게 유지할 수 있습니다. AFP 기능을 갖춘 공급업체는 복잡한 에어로 코일을 단일 패스로 가공하여 성능의 일관성을 높일 수 있습니다.

지역 분석

중국이 C919용 CJ-1000과 추력 35톤의 CJ-2000과 같은 토착 프로그램을 가속화했기 때문에 아시아태평양은 2024년 32.18%의 점유율을 차지했습니다. 중국의 터빈 블레이드는 현재 단결정 주조와 3D 프린터를 통한 냉각 채널에 의해 1,700℃를 견딜 수 있게 되었습니다. 일본과 한국은 고강도 섬유와 프리프레그를 공급하고 인도의 와이드 바디 수주가 이 지역 수요를 밀어 올리고 있습니다.

북미는 여전히 기술 리더입니다. GE 에어로 스페이스의 2024년에 269억 달러의 상용 엔진 매출은 복합재료를 충분히 사용한 LEAP와 GEnx 프로그램에 기인하는 것이지만, 재료 부족으로 납품이 10% 감소했습니다. NASA의 HyTEC 이니셔티브는 단일 통로 효율을 높이기 위해 CMC 날개를 코팅하고 연구개발 파이프라인을 유지합니다.

중동 및 아프리카는 걸프 경력이 복합재료를 다용한 엔진을 추가하고 지역 세력이 차세대 전투기에 투자하기 때문에 CAGR 13.15%로 가장 빠른 성장이 예측됩니다. 사프란 MTU의 EURA 엔진은 유럽 헬리콥터 업그레이드의 핵심이 되고 EU 클린 에비에이션의 오픈 팬 실증기는 대구경 복합재 팬에 의한 20%의 CO2 삭감을 지원합니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 경량으로 저연비 추진 시스템으로의 시프트

- LEAP와 GEnx 엔진의 생산량 확대

- 탈탄소 로드맵이 고온 CMC 수요 견인

- 애프터마켓의 소비는 복합 보수 부품으로 시프트

- 제조 공정의 자동화에 의한 비용 절감

- 극초음속 및 6세대 전투기 제조를 위한 자금 증가

- 시장 성장 억제요인

- CMC의 취성과 검사의 복잡성

- 한정된 고온 수지 공급 베이스

- 신라인에 대한 설비투자를 연기하는 불안정한 건설률

- FAA/EASA 파트 21 규칙에 따른 5-7년에 걸친 재료 및 프로세스 적격성 확인 사이클

- 밸류체인 분석

- 규제 및 기술의 전망

- Porter's Five Forces 분석

- 구매자의 협상력

- 공급기업의 협상력

- 신규 진입업자의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 용도별

- 민간 항공기

- 내로우 바디

- 와이드 바디

- 지역 제트

- 군용기

- 일반 항공기

- 비즈니스 제트

- 기타

- 민간 항공기

- 컴포넌트별

- 팬 블레이드

- 팬 케이스

- 가이드 베인

- 슈라우드

- 기타 부품

- 소재 유형별

- 폴리머 매트릭스 복합재료(PMC)

- 세라믹 매트릭스 복합재료(CMC)

- 최종 사용자별

- OEM

- 애프터마켓

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 영국

- 프랑스

- 독일

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 남미

- 브라질

- 기타 남미

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 기타 중동

- 아프리카

- 남아프리카

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- GE Aerospace(General Electric Company)

- CFM International

- Rolls-Royce plc

- Pratt & Whitney(RTX Corporation)

- Safran SA

- GKN Aerospace

- FACC AG

- Spirit AeroSystems Inc.

- Hexcel Corporation

- Toray Industries, Inc.

- Solvay

- Albany International Corp.

- Meggitt PLC

- General Dynamics Corporation

- SGL Carbon

- Renegade Materials Corporation

- Materion Corporation

- IHI Corporation

- MTU Aero Engines AG

제7장 시장 기회 및 향후 전망

AJY 25.11.12The aeroengine composites market is valued at USD 3.57 billion in 2025 and is forecasted to reach a market size of USD 6.14 billion by 2030, advancing at an 11.46% CAGR.

Growing fleet renewal, decarbonization mandates, and rising fuel prices push airlines and engine makers toward lighter propulsion systems that cut fuel burn by up to 20% while meeting stricter emission limits. Ceramic matrix composites (CMC) now withstand 1,300°C, allowing higher core temperatures and improved thermal efficiency. Automated fiber-placement and out-of-autoclave curing are lowering the cost per pound by nearly 30%, making composites economically viable for narrowbody programs. Supply-chain resilience remains critical after GE Aerospace's 10% delivery shortfall in 2024 exposed bottlenecks in high-pressure turbine blade sourcing.

Global Aeroengine Composites Market Trends and Insights

Shift toward lightweight, fuel-efficient propulsion systems

Airlines need 15-20% fuel savings to offset volatile fuel prices, driving a rapid pivot toward composites that cut nacelle weight and boost bypass ratios. GE Aerospace's RISE open-fan demonstrator targets 20% CO2 reductions using carbon-fiber fan blades with bypass ratios up to 60. Airbus is flight-testing carbon-fiber reinforced thermoplastic structures that pair with 100% sustainable aviation fuel and promise 20% fuel burn cuts. Narrowbody output above 100 aircraft per month heightens the urgency for scalable, automated composite production.

Ramp-up of LEAP and next generation aircraft engine production volumes

Over 4,000 aircraft fly with LEAP engines, prompting Safran to invest EUR 1 billion (USD 1.16 billion) in new MRO facilities in Brussels, Hyderabad, Queretaro, and Casablanca to handle 1,200 annual shop visits by 2028. GE earmarked EUR 64 million (USD 74.05 million) for European test cells and tooling that support the LEAP and GE9X programs. Component shortages, chiefly high-pressure turbine blades, trimmed 2024 engine deliveries by 10% despite USD 26.9 billion in commercial revenue, underscoring the need for diversified composite supply chains.

Brittleness and inspection complexity of CMCs

CMC fan blades risk foreign object damage because their ceramic microstructure can crack under impact loads. Traditional ultrasonic or X-ray methods struggle to detect microcracks, forcing OEMs to invest in computed-tomography scanning and specialist training. New machining methods using polycrystalline diamond tools cut processing time by 70%, raising capital costs and making adoption harder for smaller suppliers.

Other drivers and restraints analyzed in the detailed report include:

- Decarbonization roadmaps driving high-temperature CMC demand

- Shifting aftermarket spend toward composite replacement parts

- Protracted qualification cycles under FAA/EASA Part 21 rules

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Commercial engines captured 70.05% of the aeroengine composites market share in 2024 because thousands of LEAP and GEnx units integrate composite fan blades and cases that deliver up to 20% fuel savings. The aeroengine composites market size tied to military programs will expand the fastest at a 12.74% CAGR through 2030 as XA100-class propulsion and hypersonic demonstrators adopt CMC shrouds.

Business jets and regional aircraft operators are beginning to retrofit composite-rich engines as technology migrates downstream. Partnerships like GE Aerospace and Kratos Defense plan small-class engines that marry CMC turbines with affordable production methods, widening the customer base. This diffuses risk across civil and defense budgets, improving supplier order stability.

Fan blades retained 37.98% of 2024 revenue because carbon-fiber construction delivers high stiffness-to-weight and reduces inertia for better thrust response. Fan cases are projected to grow at 13.48% CAGR, lifting the aeroengine composites market size for containment hardware as regulatory containment tests favor composite shells.

Integrating shrouds, guide vanes, and O-ring seals into monolithic composite structures will keep margins healthy by reducing part count and assembly hours. Suppliers with AFP capability can machine complex aerofoils in a single pass, enhancing performance consistency.

The Aeroengine Composites Market Report is Segmented by Application (Commercial Aircraft, Military Aircraft, and General Aviation), Component (Fan Blades, Fan Case, Guide Vanes, Shrouds, and Other Components), Material Type (Polymer Matrix Composites and Ceramic Matrix Composites), End-User (OEM and Aftermarket), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held a 32.18% share in 2024 as China accelerated Indigenous programs like the CJ-1000 for the C919 and the 35-ton-thrust CJ-2000, which are rich in composite hot-section parts. China's turbine blades now tolerate 1,700 °C through single-crystal casting and 3D-printed cooling channels. Japan and South Korea supply high-strength fibers and prepregs, while India's widebody orders boost regional demand.

North America remains a technology leader. GE Aerospace's USD 26.9 billion commercial engines revenue in 2024 stemmed from composite-laden LEAP and GEnx programs, though material shortages cut deliveries by 10%. NASA's HyTEC initiative is coating CMC airfoils to raise single-aisle efficiency, sustaining R&D pipelines.

The Middle East and Africa is projected to witness the fastest growth at 13.15% CAGR as the Gulf carriers add composite-rich engines and regional forces invest in next-generation fighters. Safran-MTU's EURA engine will anchor European helicopter upgrades, while EU Clean Aviation's open-fan demonstrator supports 20% CO2 cuts via large-diameter composite fans.

- GE Aerospace (General Electric Company)

- CFM International

- Rolls-Royce plc

- Pratt & Whitney (RTX Corporation)

- Safran SA

- GKN Aerospace

- FACC AG

- Spirit AeroSystems Inc.

- Hexcel Corporation

- Toray Industries, Inc.

- Solvay

- Albany International Corp.

- Meggitt PLC

- General Dynamics Corporation

- SGL Carbon

- Renegade Materials Corporation

- Materion Corporation

- IHI Corporation

- MTU Aero Engines AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shift toward lightweight, fuel-efficient propulsion systems

- 4.2.2 Ramp-up of LEAP and GEnx engine production volumes

- 4.2.3 Decarbonization roadmaps driving high-temperature CMC demand

- 4.2.4 Shifting aftermarket spend toward composite replacement parts

- 4.2.5 Cost reductions from automated manufacturing processes

- 4.2.6 Increasing funding for hypersonic and 6th-gen fighter manufacturing

- 4.3 Market Restraints

- 4.3.1 Brittleness and inspection complexity of CMCs

- 4.3.2 Limited high-temperature resin supply base

- 4.3.3 Volatile build-rates deferring CAPEX on new lines

- 4.3.4 Protracted 5- to 7-year material/process qualification cycles under FAA/EASA Part 21 rules

- 4.4 Value Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Buyers

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Application

- 5.1.1 Commercial Aircraft

- 5.1.1.1 Narrow-Body

- 5.1.1.2 Wide-Body

- 5.1.1.3 Regional Jet

- 5.1.2 Military Aircraft

- 5.1.3 General Aviation Aircraft

- 5.1.3.1 Business Jet

- 5.1.3.2 Others

- 5.1.1 Commercial Aircraft

- 5.2 By Component

- 5.2.1 Fan Blades

- 5.2.2 Fan Case

- 5.2.3 Guide Vanes

- 5.2.4 Shrouds

- 5.2.5 Other Components

- 5.3 By Material Type

- 5.3.1 Polymer Matrix Composites (PMC)

- 5.3.2 Ceramic Matrix Composites (CMC)

- 5.4 By End-User

- 5.4.1 OEM

- 5.4.2 Aftermarket

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 France

- 5.5.2.3 Germany

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 GE Aerospace (General Electric Company)

- 6.4.2 CFM International

- 6.4.3 Rolls-Royce plc

- 6.4.4 Pratt & Whitney (RTX Corporation)

- 6.4.5 Safran SA

- 6.4.6 GKN Aerospace

- 6.4.7 FACC AG

- 6.4.8 Spirit AeroSystems Inc.

- 6.4.9 Hexcel Corporation

- 6.4.10 Toray Industries, Inc.

- 6.4.11 Solvay

- 6.4.12 Albany International Corp.

- 6.4.13 Meggitt PLC

- 6.4.14 General Dynamics Corporation

- 6.4.15 SGL Carbon

- 6.4.16 Renegade Materials Corporation

- 6.4.17 Materion Corporation

- 6.4.18 IHI Corporation

- 6.4.19 MTU Aero Engines AG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment