|

시장보고서

상품코드

1439877

세계 경화제 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2024-2029년)Curing Agent - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

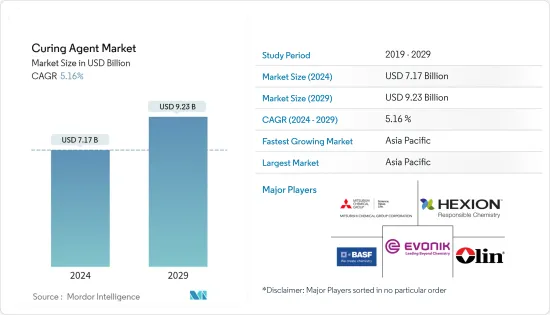

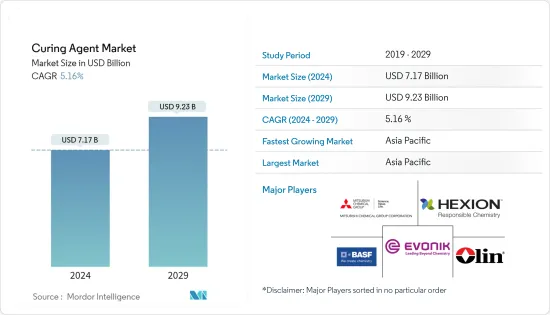

경화제 시장 규모는 2024년에 71억 7,000만 달러로 추정되고, 2029년까지 92억 3,000만 달러에 이를 것으로 예측되며, 예측 기간 동안 복합 연간 성장률(CAGR) 5.16%로 성장할 전망입니다.

경화제 시장은 COVID-19의 유행에 따라 도료, 코팅, 건축 및 건설 등 업계가 봉쇄 조치나 경제적 이유로 생산 지연을 강요하고 생산과 이동이 둔화, 악영향을 받았습니다. 혼란. 현재 시장은 유행에서 회복하고 있습니다. 시장은 2022년에 전염병 이전 수준에 도달했으며 앞으로도 꾸준히 성장할 것으로 예상됩니다.

페인트 및 코팅, 건축 및 건설 업계 수요 증가로 시장 성장이 촉진될 것으로 예상됩니다.

그러나 휘발성 유기화합물(VOC) 배출을 줄이기 위한 경화제와 관련된 엄격한 환경규제가 시장 확대를 방해할 것으로 예상됩니다.

환경 친화적 인 저 VOC 또는 비 VOC 제제의 개발은 시장이 번성 할 수있는 기회를 제공할 것으로 예상됩니다.

아시아태평양은 세계 시장을 독점하고 있으며, 중국, 인도, 일본 등의 국가들이 최대 소비국이 되고 있습니다.

경화제 시장 동향

건축 및 건설 업계에서 에폭시 경화제 수요 증가

- 경화제 중에서도 에폭시 경화제는 다양한 용도로 사용되고 있으며 예측 기간 동안 시장에서 가장 큰 점유율을 차지할 것으로 예상됩니다.

- 건설 산업에서는 에폭시 경화제가 내환경성과 우수한 강도를 제공하는 열경화성 접착제를 제조하기 위해 사용됩니다.

- 에폭시 경화제는 건축 인프라를 제공하고 건설 과제를 극복하기 위해 건축 및 건설을위한 경량 복합재료를 개발하는 데 사용됩니다.

- 에폭시 수지는 습기로부터 콘크리트를 보호하기 위해 프라이머, 실러 및 방수제로 널리 사용됩니다. 에폭시 수지는 콘크리트에 우수한 접착력, 속건성 및 높은 기계적 강도를 제공하므로 콘크리트 경화에 사용됩니다.

- 옥스포드 이코노믹스에 따르면 세계 건설 산업은 2025년까지 13조 3,000억 달러에 이를 것으로 예상되며, 2020년부터 5년간 2조 6,000억 달러의 생산량이 증가하고 있습니다.

- 아시아태평양의 건설 부문은 세계 최대입니다. 중국과 인도의 주택 건설 시장 확대로 아시아태평양에서 주택이 가장 높은 성장을 기록할 것으로 예상됩니다. 이 두 지역은 2030년까지 세계 중산 계급의 43.3% 이상을 차지할 것으로 예상됩니다.

- 또한 중국국가통계국에 따르면 중국의 건설생산액은 2022년 약 4조 1,100억 달러로 피크에 달했습니다. 그 결과 이러한 요인으로 인해 시장 수요가 증가하는 경향이 있습니다.

- 따라서 위와 같은 요인으로 인해 조사 대상 시장은 예측 기간 동안 크게 성장할 것으로 예상됩니다.

아시아태평양이 시장을 독점

- 아시아태평양은 중국, 인도, 일본 등 주요 국가에서 페인트, 코팅, 접착제, 건설 등 산업의 확대로 예측 기간 동안 경화제의 최대 시장을 차지할 것으로 예상됩니다.

- 경화제는 프라이머, 분체 도장, 탑 코트의 배합, 경량 복합재의 제조, 모르타르, 전기 주물 등에 사용됩니다. 수중에서 경화할 수 있기 때문에 해양 용도에도 적합합니다.

- 경화제는 저온 또는 고온에서의 경화, 가변 냄비 수명, 고강도, 뛰어난 내식성 등 다양한 특성을 갖추고 있으므로 다양한 용도로 사용할 수 있습니다.

- 중국 페인트 산업 협회에 따르면 아시아태평양은 페인트 산업의 주요 성장 원동력이 계속되고 있습니다. 중국은 1,000개가 넘는 코팅 회사가 운영하고 있으며 업계의 주요 기업이 되고 있습니다.

- 이러한 성장으로 일본 페인트, 악조노벨, 중국 마린 페인트, PPG 인더스트리즈, BASF SE, 액살타 코팅스 등 중국에 제조 거점을 마련하고 있는 세계 주요 페인트 제조업체로부터의 투자가 모여 있습니다.

- 2022년 7월 BASF SE는 자회사인 BASF Coatings(Guangdong)(BCG)를 통해 중국 남부 광동성 장문시에 위치한 이 회사의 코팅 거점에서 자동차 수리 코팅의 제조 능력을 확장했습니다. 이 회사는 이 확장 프로젝트를 통해 생산 능력을 연간 3만 톤으로 강화했습니다.

- 또한 인도의 페인트 및 코팅 산업도 지난 20년간 상당한 성장을 이루었습니다. 이 업계는 3,000개 이상의 페인트 제조업체로 구성되어 있으며, 국내에는 주요 세계 기업이 존재합니다.

- 2023년 1월, 아시아 페인트는 인도의 매디아 프라데시 주에 연간 4억 리터의 생산 능력을 갖춘 새로운 수성 페인트 제조 공장에 200억 루피(2억 4,053만 달러)의 투자를 승인했습니다. 이 시설의 제조는 3년 이내에 가동 개시될 예정입니다.

- 따라서 위의 요인은 아시아태평양 시장이 성장하는 건설 산업이 예측 기간 동안 조사 대상 시장에 긍정적인 영향을 미칩니다는 것을 보여줍니다.

경화제 산업 개요

경화제 시장은 본질적으로 부분적으로 세분화됩니다. 조사 대상 시장의 주요 기업(순부동)에는 BASF SE, Hexion, Olin Corporation, Mitsubishi Chemical Co., Ltd. 및 Evonik Industries AG 등이 포함됩니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 성장 촉진요인

- 도료 및 코팅 업계로부터 수요 증가

- 건축 및 건설 업계에 있어서의 에폭시 경화제 수요의 확대

- 기타 촉진요인

- 억제요인

- 엄격한 환경 규제

- 기타 구속구

- 업계의 밸류체인 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체 제품 및 서비스의 위협

- 경쟁도

제5장 시장 세분화(금액 기준 시장 규모)

- 유형

- 에폭시

- 폴리우레탄

- 고무

- 아크릴

- 기타 유형(실리콘 등)

- 용도별

- 건축 및 건설

- 복합재료

- 페인트 및 코팅

- 접착제 및 실란트

- 전기 및 전자

- 기타 용도(풍력에너지 등)

- 지역

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 이탈리아

- 프랑스

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 합병과 인수, 합작사업, 협업 및 계약

- 시장 점유율(%)**/랭킹 분석

- 유력 기업이 채용한 전략

- 기업 프로파일

- Alfa Chemicals

- BASF SE

- Cardolite Corporation

- DIC Corporation

- Evonik Industries AG

- Hexion

- Huntsman International LLC

- Mitsubishi Chemical Corporation

- Olin Corporation

- Supreme Polytech Pvt. Ltd.

제7장 시장 기회와 미래 동향

- 환경 친화적 인 저 VOC 또는 비 VOC 경화제 개발

- 기타 기회

The Curing Agent Market size is estimated at USD 7.17 billion in 2024, and is expected to reach USD 9.23 billion by 2029, growing at a CAGR of 5.16% during the forecast period (2024-2029).

The curing agent market was negatively impacted by the COVID-19 pandemic as there was a slowdown in production and mobility wherein industries, such as paints and coatings, building and construction, etc., were forced to delay their production due to containment measures and economic disruptions. Currently, the market has recovered from the pandemic. The market reached pre-pandemic levels in 2022 and is expected to grow steadily in the future.

The increasing demand from the paints and coatings and building and construction industries is expected to fuel market growth.

However, stringent environmental regulations associated with curing agents to reduce volatile organic compounds (VOC) emissions are anticipated to hamper market expansion.

The development of environmentally friendly low or non-VOC agents is expected to provide opportunities for the market to flourish.

The Asia-Pacific region dominated the market around the world, with countries like China, India, and Japan being the biggest consumers.

Curing Agent Market Trends

Growing Demand for Epoxy Curing Agents In Building and Construction Industry

- Among curing agents, epoxy curing agents are used for a variety of applications and are expected to account for the largest share of the market during the forecast period.

- In the construction industry, epoxy curing agents are used to produce thermosetting adhesives that provide environmental resistance and superior strength.

- Epoxy curing agents are used to develop lightweight composites for building and construction to provide architectural infrastructure and overcome construction challenges.

- Epoxy resins as primers, sealers, and waterproofing agents are extensively used to protect concrete from moisture. Epoxy resins are used in curing concrete as they provide great adhesion, fast drying, and high mechanical strength to concrete.

- According to Oxford Economics, the global construction industry is expected to reach USD 13.3 trillion by 2025 - adding USD 2.6 trillion to output in five years from 2020.

- The construction sector in the Asia-Pacific region is the largest in the world. The highest growth for housing is expected to be registered in the Asia-Pacific region, owing to the expanding housing construction markets in China and India. These two regions are expected to represent over 43.3% of the global middle class by 2030.

- Also, according to the National Bureau of Statistics of China, China's construction output peaked in 2022 at about USD 4.11 trillion. As a result, these factors tend to increase the market demand.

- Therefore, owing to such factors mentioned above, the studied market is expected to grow significantly during the forecast period.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region is expected to account for the largest market for curing agents during the forecast period owing to the expanding industries such as paints and coatings, adhesives, construction, etc., in major countries such as China, India, Japan, etc.

- Curing agents are used in primer, powder coating, and topcoat formulations, production of lightweight composites, mortars, electrical castings, and many more. They are even suitable for marine applications because of their underwater cure.

- Curing agents can be used for a variety of applications because of their wide range of properties, such as low or high-temperature cure, variable pot life, higher strength, and excellent corrosion resistance.

- According to the China Paint Industry Association, Asia-Pacific continues to be a major growth driver for the coatings industry. With more than 1000 coating companies in operation, China has become a major player in the industry.

- This growth has attracted investments from leading global coating manufacturers such as Nippon Paint, AkzoNobel, Chugoku Marine Paints, PPG Industries, BASF SE, and Axalta Coatings, which have established manufacturing bases in China.

- In July 2022, BASF SE, through its subsidiary BASF Coatings (Guangdong) Co., Ltd. (BCG), expanded its manufacturing capabilities for automotive refinish coatings at its coatings site in Jiangmen, Guangdong Province in South China. The company increased its production capacity to 30,000 tons annually through this expansion project.

- Further, the Indian paint and coatings industry also witnessed significant growth over the past two decades. The industry comprises more than 3,000 paint manufacturers, with the presence of major global players in the country.

- In January 2023, Asian Paints approved an investment of INR 20 billion (USD 240.53 million) for a new waterborne paint manufacturing plant with 400 million liters per annum capacity in Madhya Pradesh, India. The facility's manufacturing is expected to be commissioned in three years.

- Therefore, the factors mentioned above indicate a positive influence of the growing construction industry in the Asia-Pacific market on the studied market over the forecast period.

Curing Agent Industry Overview

The curing agent market is partially fragmented in nature. The major players in the studied market (not in any particular order) include BASF SE, Hexion, Olin Corporation, Mitsubishi Chemical Corporation, and Evonik Industries AG, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand from the Paints and Coatings Industry

- 4.1.2 Growing Demand for Epoxy Curing Agents in Building and Construction Industry

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Stringent Environmental Regulations

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 Epoxy

- 5.1.2 Polyurethane

- 5.1.3 Rubber

- 5.1.4 Acrylic

- 5.1.5 Other Types (Silicone, etc.)

- 5.2 By Application

- 5.2.1 Building and Construction

- 5.2.2 Composites

- 5.2.3 Paints and Coatings

- 5.2.4 Adhesives and Sealants

- 5.2.5 Electrical and Electronics

- 5.2.6 Other Applications (Wind Energy, etc.)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Alfa Chemicals

- 6.4.2 BASF SE

- 6.4.3 Cardolite Corporation

- 6.4.4 DIC Corporation

- 6.4.5 Evonik Industries AG

- 6.4.6 Hexion

- 6.4.7 Huntsman International LLC

- 6.4.8 Mitsubishi Chemical Corporation

- 6.4.9 Olin Corporation

- 6.4.10 Supreme Polytech Pvt. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Development of Environmental Friendly Low or Non-VOC Curing Agents

- 7.2 Other Opportunities