|

시장보고서

상품코드

1440355

정신건강 앱 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2024-2029년)Mental Health Apps - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

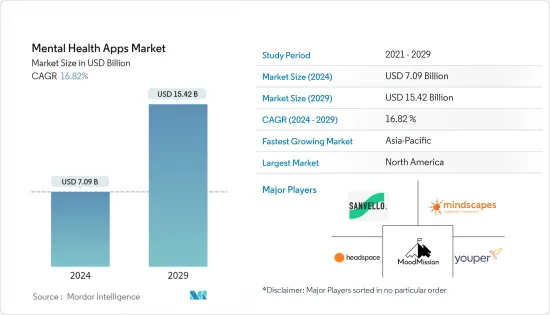

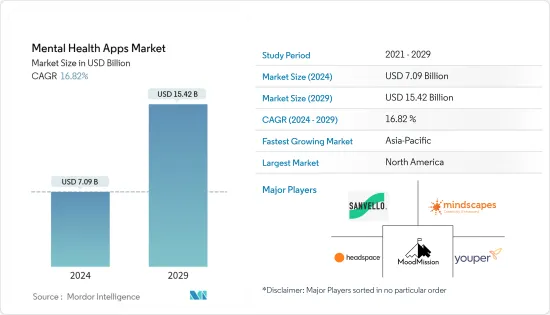

정신건강 앱 시장 규모는 2024년에 70억 9,000만 달러로 추정되며, 2029년까지 154억 2,000만 달러에 달할 것으로 예측되고 있으며, 예측 기간(2024-2029년) 중 16.82%의 CAGR로 성장합니다.

신종 코로나바이러스 감염증(COVID-19) 사태는 정신건강 앱 시장에 큰 영향을 미쳤으며, 전 세계 디지털 헬스 산업을 크게 성장시켰습니다. 팬데믹 단계에서는 사회적 거리두기, 고립의 한계와 제한으로 인한 상황에 대처하기 위해 정신건강 앱 사용이 급증하여 개인의 정신 상태에 영향을 미쳤습니다. 예를 들어 PubMed가 2021년 12월에 발표한 기사에 따르면 정신건강 전문가의 서비스에 대한 수요가 증가함에 따라 많은 사람들이 대면 서비스에 접근하는 데 어려움을 겪고 있으며, 그 결과 온라인 및 원격의료 서비스에 대한 수요가 증가했다고 합니다. 18-25세 호주 젊은이들이 온라인 정신건강 상담을 받는 횟수가 50% 증가했으며, 정신건강 앱 다운로드가 증가했습니다. 또한 2021년 3월 PubMed에 게재된 기사에 따르면 가장 많이 다운로드된 16개 앱 중 10개는 명상 관련 앱, 13개 앱은 다운로드 수가 증가했으며, 11개 앱은 팬데믹이 시작된 이후 다운로드 수가 10% 증가했다고 합니다. 분석에 따르면 정신건강에 대한 인식이 높아지고 m-health 서비스의 기술 발전이 증가함에 따라 시장은 팬데믹 이후 단계에 성장할 것으로 예상된다고 합니다.

또한 정신건강 앱의 성장을 이끄는 주요 요인은 정신건강의 중요성에 대한 인식 증가, 정신 장애의 급격한 증가, 정신 헬스케어 산업 내에서 여러 회사가 시행하는 전략적 노력 증가, 정신건강 사용 증가입니다. 건강 용도. 예를 들어 2022년 미국 정신건강 상태 보고서에 따르면 심각한 주요 우울증 에피소드(MDE)를 경험 한 청소년의 수는 2021년데이터 세트에서 197,000 명 증가했습니다. 따라서 우울 장애 발생률 증가는 정신건강 앱에 대한 수요 급증으로 이어져 예측 기간 중 시장 성장을 가속할 것으로 예상됩니다.

사람들의 인식이 높아짐에 따라 여러 기업, 조직 및 정부 기관이 다양한 플랫폼에서 정신건강 앱을 개발하고 출시하기 위해 노력하고 있습니다. 예를 들어 2021년 4월, GOI는 모든 연령대의 행복을 증진하기 위해 'MANAS' 앱을 사실상 출시했습니다. 또한 많은 기업이 정신 장애를 가진 개인을 지원하기 위해 새로운 앱을 시장에 출시하는 데 관여하고 있습니다. 예를 들어 2021년 10월 Y Combinator가 지원하는 MentalHappy 앱은 앱 내에서 저비용의 동료 지원 그룹을 개발하여 정신 헬스케어를 접근하기 쉽고 저렴하며 편견이 없는 것을 목표로 시작했습니다. 불안, 이혼 후 생활, 흑인의 정신건강. 마찬가지로 2021년 11월, 구 앱 &Fortis는 세계 정신건강의 날을 맞아 인식 개선 캠페인을 시작했습니다. 또한 2022년 4월, 가상 행동 건강 서비스 프로바이더인 Talkspace는 경영진, 관리자 및 팀이 마음의 지능지수(EQ)와 정신건강을 우선순위를 정하고 구축할 수 있도록 설계된 고용주를 위한 일련의 서비스인 Talkspace Self- Guided를 출시했습니다. Guided를 출시했습니다.

따라서 정신건강 문제 증가와 새로운 정신건강 용도의 출시가 급증함에 따라 시장은 예측 기간 중 상당한 성장을 이룰 것으로 예상됩니다. 그러나 데이터 프라이버시 및 조사 우려는 시장 성장을 저해하는 주요 요인입니다.

정신건강 앱 시장 동향

우울증 및 불안증 관리 부문은 예측 기간 중 큰 폭의 성장세를 보일 것으로 예상

우울증 및 불안 관리 부문은 우울증 및 불안에 대한 부담 증가, 우울증 및 불안에 대한 노력 확대, 우울증 및 불안 관리를 위한 여러 정신건강 앱 출시 등의 요인으로 인해 분석 기간 중 상당한 성장을 보일 것으로 예상됩니다.

예를 들어 세계보건기구(WHO)의 2021년 9월 최신 정보에 따르면 우울증은 전 세계에서 흔한 정신질환으로, 성인의 5.0%와 60세 이상 성인의 5.7%를 포함한 인구의 3.8%가 앓고 있는 것으로 추정됩니다. 또한 Mental Health America 2022 보고서에 따르면 텍사스 주에서 정신질환을 앓고 있는 사람의 수는 2022년 360만 명에 달할 것으로 나타났습니다. 우울증, 불안증과 같은 정신 질환의 발병률이 증가함에 따라 의료 서비스 이용 가능성도 높아질 것입니다. 정신건강 앱의 인기가 높아지면서 시장 부문의 성장을 가속할 것입니다. 따라서 통계에 따르면 근본적인 정신적 스트레스 요인을 추적하기 위해 인공지능 및 머신러닝과 같은 첨단 기술에 대한 접근 및 통합이 용이 해짐에 따라 이러한 정신 상태를 해결하기위한 정신건강 앱의 사용이 향후 수년간 급증할 것으로 예상됩니다.

또한 여러 시장 기업이 정신건강 앱을 출시하여이 분야의 성장에 기여하고 있습니다. 예를 들어 2021년 8월, 헤드스페이스와 온디맨드 정신 헬스케어 앱인 진저는 불안에서 우울증, 더 복잡한 진단에 이르기까지 다양한 정신건강 증상에 대한 지원을 제공하고 소비자와 소비자에게 직접 판매하기 위해 헤드스페이스 헬스(Headspace Health)라는 단일 회사로 합병할 것이라고 보고했습니다. 고용주. 마찬가지로 2021년 9월 델리 AIIMS는 불안과 우울증에 대처하는 환자를 돕기 위해 Shaksham과 Dasha라는 두 개의 모바일 앱을 개발했습니다.

따라서 우울증 및 불안 문제 증가와 새로운 정신건강 용도의 출시가 급증함에 따라 우울증 및 불안 부문은 예측 기간 중 성장할 것으로 예상됩니다.

북미는 시장에서 중요한 점유율을 차지할 것으로 예상되며, 예측 기간 중에도 비슷한 점유율을 차지

북미의 정신건강 앱 시장은 탄탄한 헬스케어 IT 산업, 첨단 기술 인프라, 모바일 애플리케이션 사용 증가, 스트레스, 우울증, 불안감 증가 등의 요인으로 인해 성장할 것으로 예상됩니다. 시장 성장을 가속하는 다른 요인으로는 정신건강에 대한 인식 증가와 시장 참여자들의 노력 등이 있습니다.

예를 들어 NAMI(National Alliance on Mental Illness)의 2022년 2월 최신 정보에 따르면 미국에서는 총 2,630만 명의 성인이 가상 정신건강 서비스를 받고 있습니다. 같은 자료에 따르면 미국 성인 5명 중 1명이 정신질환을 경험했으며, 미국 성인 20명 중 1명은 심각한 정신질환을 경험한 것으로 나타났습니다. 따라서 이것은 미국인들 사이에서 정신 앱의 사용을 크게 자극하여 궁극적으로 시장 성장을 가속했습니다.

또한 2021년 8월에는 저렴한 가격의 맞춤형 의료 서비스를 제공하는 미국의 데이터베이스 가상 1차 진료 플랫폼인 K Health가 정신건강 통합을 위한 주문형 텍스트 기반 치료로 사람들과 의료 서비스 프로바이더를 연결해 주는 정신건강 앱인 트러스트를 인수했습니다. 그리고 신체 건강은 기존 의료 시스템에서 종종 따로따로 취급되는 분야입니다. 또한 2021년 4월, 미국에 본사를 둔 Life Clips, Inc.는 자회사인 Cognitive Apps Software가 정신건강을 이해하고 관리할 수 있는 느슨한 3-in-1 툴을 성공적으로 출시했다고 보고했습니다. 또한 2022년 2월에는 정신건강에 초점을 맞춘 혁신적인 신생 기업 Noble이 새로운 앱을 출시하여 세션 간 자동 지원과 치료사가 만든 연구로 지원되는 컨텐츠를 고객에게 제공했습니다. 이러한 발전은 국내 정신건강 앱에 대한 수요가 증가하고 있으며, 이는 시장 성장에 기여하고 있습니다.

따라서 정신질환 증가와 수많은 새로운 정신건강 앱의 출시로 인해 북미에서는 예측 기간 중 정신건강 앱 시장이 성장할 것으로 예상됩니다.

정신건강 앱 산업 개요

정신건강 앱 시장은 세분화되어 있으며, 세계 및 국내의 여러 기업이 존재합니다. 주요 기업은 파트너십, 계약, 협업, 신제품 출시, 지역적 확장, 합병, 인수 합병 등 다양한 성장 전략을 채택하여 시장에서의 입지를 강화하기 위해 노력하고 있습니다. 시장의 주요 기업으로서는 CVS Health Corporation, Sanvello Health, Inc., Mindscapes, Headspace, Inc., Youper, Inc. 등이 있습니다.

기타 혜택

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 촉진요인

- 정신건강의 중요성에 대한 의식의 향상

- 전 세계에서 정신 상태가 급증

- 시장 억제요인

- 프라이버시와 조사의 우려

- Porter's Five Forces 분석

- 신규 진출업체의 위협

- 구매자의 교섭력

- 공급 기업의 교섭력

- 대체품의 위협

- 경쟁 기업간 경쟁의 강도

제5장 시장 세분화

- 플랫폼 유형별

- Android

- iOS

- 기타 플랫폼 유형

- 용도별

- 우울증과 불안증 관리

- 스트레스 관리

- 명상 관리

- 기타 용도 유형

- 최종사용자별

- 홈케어 환경

- 정신병원

- 기타 최종사용자

- 지역

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카공화국

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 기업 개요

- MoodMission

- Sanvello Health, Inc.

- Mindscapes

- Headspace Inc.

- Youper Inc.

- K Health Inc.

- Calm

- Happify Health

- MoodTools

- CVS Health Corporation

- Zavfit

- Talkspace

- Real

- Wysa

제7장 시장 기회와 향후 동향

KSA 24.03.12The Mental Health Apps Market size is estimated at USD 7.09 billion in 2024, and is expected to reach USD 15.42 billion by 2029, growing at a CAGR of 16.82% during the forecast period (2024-2029).

The COVID-19 outbreak substantially impacted the mental health apps market and greatly boosted the digital health industry worldwide. The pandemic phase witnessed an upsurge in the usage of mental health apps for coping with conditions due to the limitations and restrictions on social distancing and isolation, affecting individuals' mental states. For instance, as per the article published in December 2021 by PubMed, due to the increased demand for services from mental health professionals, many people struggled to access in-person services, which led to an augmented demand for online and telehealth services, including a 50% increase in the number of Australian young people aged 18-25 who were accessing online mental health help and increased the downloads of mental health apps. Additionally, as per the article published in March 2021 in PubMed, among the 16 most downloaded apps, 10 were meditational, 13 showed increased downloads, and 11 apps showed a 10% increase in downloads after the pandemic started. As per the analysis, the market is anticipated to witness growth in the post-pandemic phase due to the rise in awareness regarding mental health and the increase in technological advancements in m-health services.

Furthermore, the major factors boosting the growth of mental health apps are the increasing awareness of the importance of mental health, the surge in mental disorders, the rise in strategic initiatives undertaken by several companies within the mental healthcare industry, and the growing usage of mental health applications. For instance, as per the State of Mental Health in America 2022 report, the number of youths experiencing a severe major depressive episode (MDE) increased by 197,000 from the 2021 dataset. Thus, the rise in the incidence of depressive disorders leads to a surge in demand for mental health apps, which is thereby expected to boost market growth over the forecast period.

Owing to the increasing awareness among the population, several companies, organizations, and governmental bodies are engaged in developing and launching mental health apps across various platforms. For instance, in April 2021, the GOI virtually launched the "MANAS" app to promote well-being across age groups. Furthermore, numerous companies are involved in launching newer apps into the market to help individuals with mental disorders. For instance, in October 2021, the Y Combinator-backed MentalHappy app initiated the goal of making mental health care accessible, affordable, and stigma-free by developing low-cost peer support groups within the app to boost access to conditions such as coping with anxiety, life after divorce, and black mental health. Similarly, in November 2021, Koo App & Fortis launched an awareness campaign on World Mental Health Day. Furthermore, in April 2022, Talkspace, a provider of virtual behavioral health services, launched Talkspace Self-Guided, a suite of offerings for employers designed to help executives, managers, and teams prioritize and build emotional intelligence (EQ) and mental wellness in and out of the workplace.

Thus, due to the rise in mental health issues and the surge in new mental health application launches, the market is expected to witness significant growth over the forecast period. However, data privacy and research concerns are major factors hindering the market's growth.

Mental Health Apps Market Trends

Depression and Anxiety Management Segment is Expected to Witness Significant Growth Over the Forecast Period

The depression and anxiety management segment is expected to witness significant growth over the analysis period owing to factors such as the increasing burden of depression and anxiety, growing initiatives about depression and anxiety, and the launch of several mental health apps for managing depression and anxiety.

For instance, as per the September 2021 update by the WHO, depression is a common mental disorder worldwide, with an estimated 3.8% of the population affected, including 5.0% of adults and 5.7% of adults older than 60 years. Moreover, as per the Mental Health America 2022 report, the number of people affected by mental illness in Texas is found to be 3.6 million in 2022. As the number of mental illness cases, such as depression or anxiety, increases, the chance of utilizing mental health apps rises, thereby boosting market segment growth. Thus, the statistics indicate that the use of mental health apps for coping with these mental conditions is anticipated to surge over the coming years owing to the ease of access and integration of advanced technologies such as artificial intelligence and machine learning for tracking the underlying mental stressors.

Additionally, several market players are launching mental health apps, contributing to the segment's growth. For instance, in August 2021, Headspace and the on-demand mental healthcare app Ginger reported merging into a single company, called Headspace Health, to offer support for mental health symptoms ranging from anxiety to depression to more complex diagnoses and sell directly to consumers and employers. Similarly, in September 2021, Delhi AIIMS developed two mobile apps, Shaksham and Disha, to assist patients dealing with anxiety and depression.

Thus, due to the rise in depression and anxiety issues and the surge in new mental health application launches, the depression and anxiety segment is expected to witness growth over the forecast period.

North America is Expected to Hold a Significant Share in the Market and Expected to do Same in the Forecast Period

North America is anticipated to witness growth in the mental health apps market owing to factors such as the well-established healthcare IT industry, sophisticated technological infrastructure, the rising usage of mobile applications, and the increasing burden of stress, depression, and anxiety. Some other factors boosting the market's growth include the rising awareness about mental health and the initiatives undertaken by the market players.

For instance, as per a February 2022 update by the National Alliance on Mental Illness (NAMI), in the United States, a total of 26.3 million adults received virtual mental health services. As per the same source, 1 in 5 adults in the United States experiences mental illness, whereas 1 in 20 adults in the United States experiences serious mental illness. Thus, this has greatly stimulated the use of mental apps among Americans, ultimately augmenting the market's growth.

Likewise, in August 2021, K Health, a United States-based data-driven virtual primary care platform providing affordable, personalized healthcare, acquired Trust, the mental health app that connects people and providers for on-demand text-based therapy to integrate mental and physical health, disciplines that are often treated separately in the traditional healthcare system. Additionally, in April 2021, Life Clips, Inc., based in the United States, reported that its subsidiary Cognitive Apps Software had successfully launched its Yuru 3-in-1 tool for understanding and managing mental health. Moreover, in February 2022, Noble, a new innovative, mental health-focused company, launched its new app, offering automated between-session support and therapist-created, research-backed content for clients. Such developments indicate the growing demand for mental health apps in the country, thereby contributing to market growth.

Thus, as a result of the rise in mental illness and the huge number of new mental health app launches, North America is expected to witness growth in the mental health app market over the forecast period.

Mental Health Apps Industry Overview

The mental health apps market is fragmented, with several global and domestic players. The key players are adopting different growth strategies to enhance their market presence, such as partnerships, agreements, collaborations, new product launches, geographical expansions, mergers, and acquisitions. Some key players in the market are CVS Health Corporation, Sanvello Health, Inc., Mindscapes, Headspace, Inc., and Youper, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Awareness Pertaining to the Importance of Mental Health

- 4.2.2 Upsurge in Mental Conditions Worldwide

- 4.3 Market Restraints

- 4.3.1 Privacy and Research Concerns

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Platform Type

- 5.1.1 Android

- 5.1.2 iOS

- 5.1.3 Other Platform Types

- 5.2 By Application

- 5.2.1 Depression and Anxiety Management

- 5.2.2 Stress Management

- 5.2.3 Meditation Management

- 5.2.4 Other Application Types

- 5.3 By End User

- 5.3.1 Home Care Settings

- 5.3.2 Mental Hospitals

- 5.3.3 Other End Users

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 MoodMission

- 6.1.2 Sanvello Health, Inc.

- 6.1.3 Mindscapes

- 6.1.4 Headspace Inc.

- 6.1.5 Youper Inc.

- 6.1.6 K Health Inc.

- 6.1.7 Calm

- 6.1.8 Happify Health

- 6.1.9 MoodTools

- 6.1.10 CVS Health Corporation

- 6.1.11 Zavfit

- 6.1.12 Talkspace

- 6.1.13 Real

- 6.1.14 Wysa