|

시장보고서

상품코드

1441592

자동차용 인테리어 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2024-2029년)Automotive Interior - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

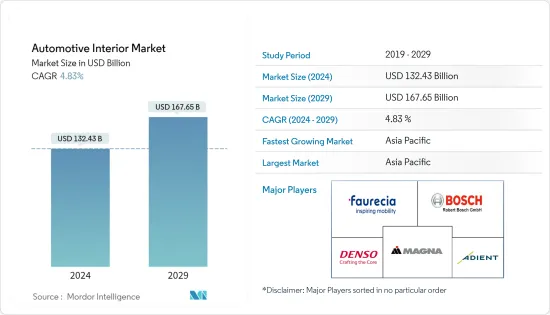

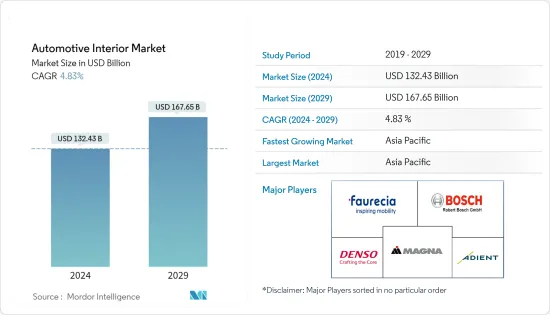

자동차용 인테리어 시장 규모는 2024년 1,324억 3,000만 달러로 추정되고, 2029년까지 1,676억 5,000만 달러에 이를 것으로 예측되며, 예측 기간(2024-2029년) 동안 4.83%의 연평균 복합 성장률(CAGR)로 성장할 전망입니다.

신형 코로나 바이러스 감염(COVID-19)의 팬데믹은 차량 생산에 미치는 영향으로 자동차용 인테리어 시장의 성장을 방해하고 있습니다. 그러나 2020년 이후 자동차 생산의 꾸준한 회복은 향후 수년간 이 시장의 발전을 지원할 것입니다. 예를 들어 말렐리는 2020년 첫 2분기에 COVID-19에 의해 전체 생산에 심각한 영향을 미쳤습니다. 이 회사는 2020년 3월에 시작된 전국 봉쇄 이후 국내 시설을 약 2주간 폐쇄해야 했습니다. 그러나 회사는 필요한 조치를 취한 후 2020년 4월에 영업을 재개했습니다.

자동차 인포테인먼트 시스템에 이어 몇 가지 기술적 이점이 있으며, 자동차용 인테리어 시장의 성장을 크게 뒷받침해 왔습니다. 예를 들면:

주요 하이라이트

- 자동차 인포테인먼트 시스템에 스마트폰 기능이 탑재되는 케이스가 늘고 있습니다. 북미와 유럽에서는 성인의 90% 이상이 휴대전화를 통해 인터넷에 접속하고 있으며, 이는 다른 지역 중에서도 가장 높은 수준입니다. 휴대폰의 이용이 늘어나면서 같은 목적으로 차내에 스마트폰을 두는 사람도 늘어나고 있습니다.

- 제조업체는 터치 스크린의 인포테인먼트 시스템을 도입하고 있어, 사내의 객실 체험이 완전히 바뀌었습니다. 현재 터치스크린 인포테인먼트 시스템에 몇 가지 새로운 진보가 보이고 있으며, 제조업체는 실제로 화면을 건드리지 않고 지시에 따른 예측 터치스크린 기능을 도입하고 있습니다. 이로 인해 촉진요인인 쾌적성 및 조작성이 향상되어 기세가 증가했습니다.

소비자의 안전에 대한 우려가 높아지고, 기술이 발전하고, 고급차 수요가 급증함에 따라 시장 성장이 촉진될 것으로 예상됩니다. 가볍고 안전한 차량에 대한 정부의 지원으로 시장 성장이 급속히 진행될 수 있습니다.

자동차용 인테리어 재료 시장에서는 아시아태평양이 소비량에서 가장 큰 점유율을 차지했습니다. 일본과 중국이 이 지역의 증가하는 수요를 주로 지원하게 됩니다. 또한 인도의 제품 수요 전망 개선도 잠재적인 성장 요인이 됩니다. 자동차 제조업체의 대규모 OEM 기반을 가진 유럽도 인테리어 재료 시장에서의 수주를 더욱 늘릴 것으로 보입니다.

자동차용 인테리어 시장 동향

자동차용 인테리어 시장을 독점할 것으로 예상되는 인포테인먼트 시스템

인포테인먼트 시스템은 자동차용 인테리어 시장에서 가장 큰 부문입니다. 이전에는 자동차에 제공되는 인포테인먼트 스크린은 단 하나였지만, 기술이 발전함에 따라 인포테인먼트 스크린의 수와 치수도 증가하고 있습니다.

그러므로 인포테인먼트 스크린은 모든 자동차 제조업체들에게 주요 초점을 맞추고 있으며, 이러한 스크린에는 최신 기술 기능이 가득합니다. 2022년에 메르세데스 벤츠가 인도 시장을 위한 S클래스 차량을 출시한 것처럼, 즉 S350d 및 S450은 150대의 신차를 수입했습니다. 차내 인포테인먼트 시스템은 소비자를 놀라게 합니다. 64색 앰비언트 라이트와 뒷좌석 인포테인먼트 스크린을 갖춘 이 자동차는 궁극의 편안함과 고급 스러움을 제공합니다.

자동차 제조업체는 고객에게 최고의 기능과 기술을 제공하기 위해 인포테인먼트 시스템을 지속적으로 업그레이드하고 있습니다. 최근 출시와 모델의 일부는 다음과 같습니다.

- 지프는 또한 2022년에 지프 그랜드 체로키 2022년 모델의 후방 좌석에 2개의 인포테인먼트 스크린을 탑재해, 전석 승무원이 촉진요인인 네비게이션 시스템과 상호 작용할 수 있도록 대시보드에 스크린을 탑재할 가능성이 있다고 제안했습니다.

- 2022년 도요타는 3.5리터 V6 트윈터보 하이브리드 엔진을 탑재한 새로운 부문 탄도라 TRD 트랙을 출시했습니다. 소비자의 관점에서 보면 픽업 트럭의 인테리어는 유망하게 보입니다. 자연광을 변화시키지 않고 밝기를 랜덤하게 변화시키는 인 대시 인포테인먼트 시스템이 탭재되어 있습니다.

- 2022년 리비안은 중요한 소비자의 모든 요구 사항을 고려하여 새로운 전기 픽업 트럭을 출시했습니다. 이 새로 출시된 픽업 트럭은 대시 인포테인먼트 시스템 보드에 장식된 애쉬 우드를 갖추고 있습니다. 이 시스템은 자동차의 HVAC 통풍구 바로 위에 내장된 12.3장의 가로 화면으로 구성되어 있습니다.

자동차가 더 많은 연결 기능을 탑재함에 따라 통신 및 기술 기업은 주요 자동차 기업과 제휴하여 고객에게 최적의 연결 및 인포테인먼트 솔루션을 개발하고 있습니다.

위의 모든 요인과 자동차 인포테인먼트 시스템의 개발을 고려하면 자동차용 인테리어 시장은 예측 기간에 번영할 것으로 예상됩니다.

아시아태평양이 자동차용 인테리어 시장을 선도합니다.

아시아태평양 시장은 소형 및 경제 자동차 부문에 의해 견인되고 있으며, 내부 부품의 채용률이 높아집니다. 도요타, 혼다, 현대 등 이 지역의 선도적인 자동차 제조업체들은 첨단 시트 시스템, 조명, 전자 제품 및 다양한 안전 시스템의 장점을 활용하여 자체 차종 전체에 필수적인 기능이 되었습니다. 일본, 중국, 인도 등 주요 경제국에서 전기차의 상승이 시장가치를 더욱 뒷받침하고 있습니다.

2022년 4월 중국의 승용차 생산은 99만 6,000대에 이르고 판매량은 96만 5,000대에 달했습니다. 이는 전년 대비 생산량과 매출액이 각각 41.9%, 43.4% 감소한 것을 보여줍니다. 2022년 1월부터 4월까지 승용차 생산 대수는 전년 대비 2.6% 감소한 64억 9,400만대가 됐습니다.

중국에서는 현지 기업이 협력하여 최고의 인테리어 제품을 생산하고 있습니다. 예를 들어 BAIC Yunxiang Automobile은 ADAYO와 협력하여 차량 인포테인먼트 시스템을 개발했습니다. 이 파트너십은 BAIC Yinxiang의 새로운 플랫폼을 구축하고 지능형 차량 제조를 위한 플랫폼 생산 모드를 재구성하는 데 도움이 됩니다. 중국 기업은 시장에 성장을 가져오는 새로운 비전을 가지고 시장에 진출하고 있습니다. 예를 들어, 2021년 11월, 중국의 주요 자동차용 인테리어 부품 공급업체인 Yanfeng Automotive Interiors(YFAI)는 TCL 및 그 자회사인 TCL CSOT와 공동 개발한 업계 최초 패널 언더 패널 온보드 인텔리전트 스크린 카메라를 도입했습니다.

고급 인테리어, 편안함, 헤드업 디스플레이 및 네비게이션 시스템과 같은 새롭고 혁신적인 기능에 대한 수요가 안전 기준을 충족하는 데 주목이 높아짐에 따라이 지역 시장을 견인하고 있습니다. 중국, 일본, 인도, 한국 등 이 지역의 주요 국가에서는 새로운 기술이 빠르게 도입될 것으로 예상됩니다. 중국은 높은 자동차 생산 능력으로 아시아태평양 시장 성장에 크게 기여할 것으로 기대됩니다.

아시아태평양에서는 각국의 보조금이나 세제 우대 등 정부의 대처에 의해 자동차 OEM이 지역의 제조 공장을 건설하도록 유치되고 있습니다.

자동차용 인테리어 업계 개요

주요 자동차용 인테리어 시장 진출 기업은 Continental AG, Magna International Inc., Denso Corporation, Faurecia, Adient 등입니다. 자동차용 인테리어 시장은 경쟁 우위를 확보하기 위한 중요한 제품 제조업체에 의한 집중적인 연구개발 활동, 신제품 개발, 인수 등 다양한 전략으로 향후 몇 년간 경쟁이 예상됩니다. 예를 들어,

- 2022년 5월-자동차 기술인 Lear Corporation은 시트 히터, 액티브 냉각, 시트 센서 및 기타 내부 부품 공급업체인 IG Bauerhin을 인수할 것이라고 발표했습니다.

- 2021년 9월-Addient는 Cardion 사용을 시작합니다. 코베스트로에 따르면, 코베스트로의 CO2 기술을 사용하여 제조된 폴리올은 2021년 11월에 열경화 성형 폴리우레탄 폼을 제조하기 위한 지속가능한 원료로 사용됩니다. 이 양식은 Adient의 최첨단 자동차 시트 시스템의 쿠션으로 사용됩니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제 조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 성장 촉진요인

- 시장 성장 억제요인

- 업계의 매력-Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체 제품의 위협

- 경쟁 기업간 경쟁 관계의 격렬

제5장 시장 세분화(금액별 시장 규모)

- 차종별

- 승용차

- 상용차

- 컴포넌트 유형별

- 기기 패널

- 인포테인먼트 시스템

- 인테리어 조명

- 바디 패널

- 기타 컴포넌트 유형

- 지역별

- 북미

- 미국

- 캐나다

- 북미의 다른 지역

- 유럽

- 독일

- 영국

- 프랑스

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 벤더의 시장 점유율

- 기업 프로파일

- Adient PLC

- Grupo Antolin

- Panasonic Corp.

- Faurecia

- Magna International

- Toyota Boshuku Corporation

- Hyundai Mobis Co.

- Pioneer Corporation

- JVCKENWOOD Corporation

- Robert Bosch GmbH

제7장 시장 기회 및 미래 동향

AJY 24.03.15The Automotive Interior Market size is estimated at USD 132.43 billion in 2024, and is expected to reach USD 167.65 billion by 2029, growing at a CAGR of 4.83% during the forecast period (2024-2029).

The COVID-19 pandemic has hindered the growth of the automotive interior market due to its impact on vehicle production. However, a steady recovery post-2020 in vehicle production will support the development of this market in the coming years. For instance, Marelli had a significant impact on COVID-19 on its overall production in the first two quarters of 2020. The company had to shut its facilities for around two weeks in the country after the nationwide lockdown, which started in March 2020. However, the company resumed its operations in April 2020 with the necessary measures.

There have been several technological dominance followed in-vehicle infotainment systems, which has provided a significant boost to the automotive interiors market growth. For instance:

Key Highlights

- There is a rise in smartphone functions built into in-vehicle infotainment systems. In North America and Europe, over 90% of adults have access to the internet through their mobile phones, which is also among the highest among other regions. As mobile phone use has risen, smartphones for the same purposes in their cars have also increased.

- Manufacturers are introducing a touchscreen infotainment system, which has completely changed the in-house cabin experience. Today, after several new advancements seen by the touch screen infotainment system, manufacturers have introduced a predictive touchscreen feature that shall follow the instruction without actually touching the screen. This has improved drivers' comfort and ease, thus gaining momentum.

Increasing consumer safety concerns, rising technological advancements, and a surge in demand for luxurious vehicles are expected to boost the market growth. Government support for lightweight and safe vehicles will likely surge the market growth.

Asia-Pacific accounted for the largest share in terms of consumption in the automotive interior materials market. Japan and China will be the primary support for the region's increasing demand. Moreover, an improved outlook for product demand in India is another potential factor for growth. With its sizeable OEM base of automobile manufacturers, Europe will also add to the order in the interior material market.

Automotive Interior Market Trends

Infotainment System Expected to Dominate the Automotive Interiors Market

The infotainment system is the largest segment in the automotive interiors market. Earlier, cars were offered only one infotainment screen, but as technology advances, the number and dimension of infotainment screens are also increasing.

As such, the infotainment screens have become the main focal point for every automaker, and these screens are packed with the latest technology capabilities, as In 2022, Mercedes-Benz launched its S-class fleet for the Indian market, namely, S350d and S450 importing 150 new cars. The infotainment system in the vehicle amazes the consumer; with 64-colour ambient lighting and rear seat infotainment screens, the car offers ultimate comfort and luxury.

Automakers constantly upgrade their infotainment systems to provide their customers with the best features and technologies. Some of the recent launches and models are:

- In 2022, Jeep also proposed that Jeep Grand Cherokee 2022 model may have two rear seat infotainment screens with a screen in the dashboard for the front-seat passenger to interact with the driver's navigation system.

- In 2022, Toyota launched its new segment Tundra TRD truck, powered by the 3.5-liter V6 twin-turbo hybrid engine. The pickup truck's interior seems promising from a consumer's point of view. It is equipped with the in-dash infotainment system, which changes brightness randomly without a change in natural lighting.

- In 2022, Rivian launched its new electric pickup truck considering all the requirements of critical consumers. This newly launched pickup truck is equipped with decorated ash wood on the dash infotainment system board. The system comprises of 12.3 landscape-oriented screen inbuilt placed just above the HVAC vents of the car.

As the cars come with more connected features, the telecom and technology players are partnering with major automotive players to develop the best connectivity and infotainment solutions for the customers.

Considering all the factors above and the development of in-vehicle infotainment systems, the automotive interiors market is expected to witness prosperity in the forecast period.

Asia-Pacific is Leading the Automotive Interiors Market

The Asian-Pacific market is driven by the small/economy car segment, which accounts for higher adoption of interior components. Leading automakers in this region, such as Toyota, Honda, and Hyundai, are embracing the advantages of advanced seating systems, lighting, electronics, and various safety systems, making them essential features across their car models. The emergence of electric vehicles in major economies, including Japan, China, and India, further supports the market value.

In April 2022, Chinese passenger car production reached 996,000 units, with sales registering 965,000 units. This accounts for the downfall of 41.9% and 43.4% respectively in production and sales compared to the previous year. In 2022, from January to April, passenger car production decreased by 2.6% year-on-year, registering 6,494 million units.

In China, local players are collaborating to produce the best interior products. For instance, BAIC Yunxiang Automobile Co. Ltd collaborated with ADAYO to develop vehicle infotainment systems. This partnership will build new platforms for BAIC Yinxiang and helps to restructure the platform production mode for intelligent vehicle manufacturing. Chinese players are debuting in the market with a new vision to provide growth to the market. For instance, In November 2021, China's leading automotive supplier for interior components, Yanfeng Automotive Interiors (YFAI), introduced an industry-first camera under panel onboard intelligent screen, which is co-developed with TCL and its subsidiary TCL CSOT.

The demand for premium interiors, comfort, and new and innovative features, like head-up displays and navigation systems, along with the growing focus on sufficing the safety standards, is driving the market in the region. Major countries in this region, such as China, Japan, India, and South Korea, are anticipated to witness the rapid adoption of new technologies. Due to its high vehicle production capacity, China is expected to contribute to Asia-Pacific's market growth significantly.

In Asia-Pacific, government initiatives, such as subsidies and tax concessions, across various countries are attracting automotive OEMs to build their regional manufacturing plants.

Automotive Interior Industry Overview

Key automotive interior market participants are Continental AG, Magna International Inc., Denso Corporation, Faurecia, Adient, and Others. The automotive interiors market is likely to expect competition in the coming years, owing to various strategies, such as focused research and development activities, new product developments, acquisitions, etc., by significant product manufacturers to gain a competitive advantage. For instance,

- In May 2022, Lear Corporation, an automotive technology, announced that it is acquiring I.G. Bauerhin, a seat heating supplier, active cooling, seat sensor, and other interior components.

- In September 2021, Adient will begin using cardyon; a polyol made using Covestro's CO2 technology, as a sustainable feedstock for the production of hot cure molded polyurethane foam in November 2021, according to Covestro. These foams are used as cushioning in Adient's cutting-edge automotive seating systems.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in Value USD Billlion)

- 5.1 By Vehicle Type

- 5.1.1 Passenger Cars

- 5.1.2 Commercial Vehicles

- 5.2 By Component Type

- 5.2.1 Instrument Panels

- 5.2.2 Infotainment Systems

- 5.2.3 Interior Lighting

- 5.2.4 Body Panels

- 5.2.5 Other Component Types

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.1 North America

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 South Africa

- 5.3.5.4 Rest of Middle-East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Adient PLC

- 6.2.2 Grupo Antolin

- 6.2.3 Panasonic Corp.

- 6.2.4 Faurecia

- 6.2.5 Magna International

- 6.2.6 Toyota Boshuku Corporation

- 6.2.7 Hyundai Mobis Co.

- 6.2.8 Pioneer Corporation

- 6.2.9 JVCKENWOOD Corporation

- 6.2.10 Robert Bosch GmbH