|

시장보고서

상품코드

1443996

농업용 훈증제 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2024-2029년)Agricultural Fumigants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

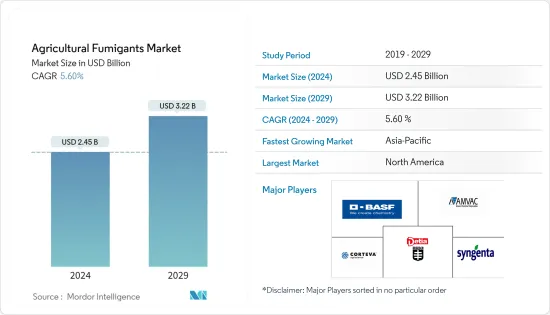

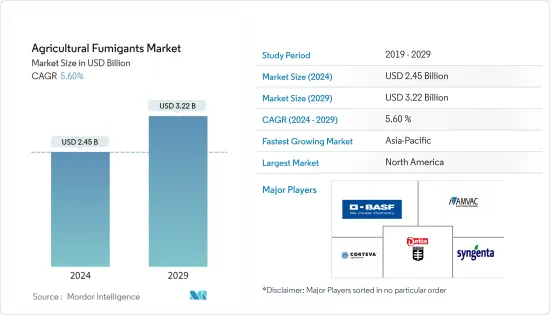

농업용 훈증제 시장 규모는 2024년 24억 5,000만 달러에 이를 것으로 추정됩니다. 2029년까지 32억 2,000만 달러에 달할 것으로 예상되며, 예측 기간(2024-2029년) 동안 5.60%의 연평균 복합 성장률(CAGR)을 나타낼 전망입니다.

COVID19 팬데믹으로 인해 훈증제를 포함한 농약 시장 운영이 혼란에 빠졌습니다. 전염병은 공급망 네트워크에 영향을 미쳐 기업과 농가에 손실을 가져왔습니다. 공급 측면에서는 유통 병목 현상으로 인한 단기적인 이주 노동자 부족으로 인해 생산에 필요한 노동자 수와 큰 격차가 발생했습니다. 기타 제한 사항으로는 통관, 수출 허가, 수입 허가, 식물 검역 증명서 등이 있습니다.

농업용 훈증제 시장은 농업 분야의 급속한 기술 발전, 수확 후 손실에 대한 우려 증가, 수확량 증가로 이어진 선진 농업 관행의 변화 등의 요인에 의해 주도되고 있습니다. 저장 중에 훈증제를 사용하면 저장 손실을 줄이는 데 도움이 됩니다. 따라서 훈증제 사용은 수확 후 손실을 줄이는 효과적이고 경제적 인 방법이기 때문에 훈증제에 대한 수요가 증가할 것으로 예상됩니다.

포스핀계 훈증제는 곤충과 설치류로부터 농산물을 보호하면서 농산물을 보관하는 데 널리 사용되고 있으며, 전 세계 모든 유형의 훈증제 중 가장 큰 부문으로 부상하고 있습니다. 북미가 시장을 독점하고 있습니다. 기술 및 R&D에 대한 급속한 투자로 인해 독성이 낮고 효율성이 개선된 새로운 유형의 제품이 많이 개발되고 있습니다. 농업용 훈증제 시장의 성장은 농산물의 품질 향상에 대한 소비자 선호도 증가, 농업 관행의 변화, 첨단 저장 기술 등 여러 가지 요인에 기인하는 것으로 보입니다. 그러나 훈증제는 작물의 유형과 품종, 계절적 조건, 습도, 온도, 훈증제 농도, 처리 기간에 따라 식물 독성 가능성 등 여러 가지 문제를 야기할 수 있습니다. 따라서 호흡기 독으로 독성이 높기 때문에 전문 훈 증가만 사용하는 것이 좋습니다.

농업용 훈증제 시장 동향

농업 생산의 확대

농업 생산량이 증가함에 따라 훈증제에 대한 수요는 수년 동안 증가 추세에 있습니다. 훈증은 곡물 및 종자 공급망의 모든 단계에서 훈증 사용이 증가하고 있으며 농장 수준의 주요 곤충 관리 옵션으로 부상하고 있습니다. 농장 수준의 저장 및 사일로 내 훈증은 해충의 저항성을 피하면서 해충 침입의 축적을 방지하는 가장 바람직한 방법 중 하나입니다. 그러나 법적 제한으로 인해 사용 가능한 활성 물질은 제한된 수의 훈증제 및 저장 살충제로 제한되어 있습니다. 메틸브로마이드(MB) 훈증은 제품이 식물 검역상의 위험을 최소화하기 위한 효과적인 처리입니다. 유럽연합은 MB 사용을 금지했지만 캐나다는 여전히 MB를 일부 제품의 검역 및 선적 전 적용을 위해 승인된 유일한 치료법으로 요구하고 있습니다.

유엔식량농업기구(FAO)는 늘어나는 식량 수요를 충족시키기 위해 2050년까지 농업 생산성이 70% 증가할 것으로 예측했습니다. 농작물 수요는 2050년까지 약 67억 5,900만 톤으로 증가할 것으로 예상됩니다. 세계 곡물 생산량은 2018년 29억 6,500만 톤에서 2020년 29억 9,610만 톤으로 증가했습니다. 따라서 농업용 창고, 저장 기술 및 다음과 같은 관련 제품에 대한 수요가 증가하고 있습니다. 훈증제는 장기적으로 증가할 것으로 예상됩니다. 창고에서 대부분의 작물이 해충에 의해 피해를 입어 훈증제를 사용하면 농산물의 손실을 줄일 수 있습니다. 따라서 이는 전 세계 농업용 훈증제 시장 수요를 증가시킬 것으로 예상됩니다.

세계 시장을 선도하는 북미

북미는 농업용 훈증제의 가장 큰 시장이며, 주요 국가에서 250개 이상의 인증 제품을 사용할 수 있습니다. 식품 및 곡물 가공 및 저장 산업에서 저장 제품의 곤충 관리는 큰 관심사이며 광범위하게 연구되고 있는 주제입니다.

이 지역에서 저장 및 토양 사용 모두에 훈증제를 소비하는 주요 품목은 옥수수, 쌀, 보리, 감자, 토마토, 밀, 딸기, 양배추 등입니다. 북미에서는 미국이 가장 큰 시장으로 절반 이상을 차지합니다. 지역 시장 점유율. 미국 시장의 주요 훈증제에는 클로로피클린, 불화 설프릴, 인화 알루미늄, 에틸렌 산화물 등이 포함됩니다. 캐나다에는 90개 이상의 훈증제 기반 제품이 등록되어 있으며, 25개사가 생산하고 있습니다. 주요 기업으로는 AMVAC Chemicals, Degesch America Inc., Syngenta Canada Inc.

농업용 훈증제 산업 개요

세계 농업용 훈증제 시장은 통합되어 있으며, 몇몇 기업이 가장 큰 시장 점유율을 차지하고 있습니다. 북미와 유럽 시장은 고도로 통합되어 있으며, 소수의 대기업이 큰 시장 점유율을 차지하고 있어 높은 수준의 경쟁이 벌어지고 있습니다. 신제품 도입의 근간이 되는 연구개발을 통한 포트폴리오 다변화는 성숙한 시장에서 더욱 치열하게 경쟁하기 위해 적용되고 있는 두드러진 전략 중 하나입니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 성장 촉진요인

- 시장 성장 억제요인

- Porter의 Five Forces 분석

- 공급 기업의 교섭력

- 바이어의 교섭력

- 신규 진출업체의 위협

- 대체 제품의 위협

- 경쟁 기업간 경쟁도

제5장 시장 세분화

- 유형

- Methyl Bromide

- Chloropicrin

- Phosphine

- Metam Sodium

- 1,3-Dichloropropene

- 기타

- 적용 방법

- 토양

- 창고

- 형태

- 고체

- 액체

- 가스

- 작물 적용

- 작물 기반

- 비작물 기반

- 지역

- 북미

- 미국

- 캐나다

- 멕시코

- 기타 북미

- 유럽

- 독일

- 영국

- 프랑스

- 러시아

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 아프리카

- 남아프리카공화국

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 가장 많이 채택되고 있는 전략

- 시장 점유율 분석

- 기업 개요

- DowDuPont

- Amvac Chemical Corporation

- Syngenta AG

- UPL Group

- Detia Degesch GmbH

- ADAMA Agricultural Solution Ltd

- BASF SE

- Cytec Solvay Group

- FMC Corporation

- Fumigation Services

- Ikeda Kogyo Co. Ltd

- Industrial Fumigation Company

- Isagro SpA

- Lanxess

- Reddick Fumigants LLC

- Trical Inc.

- TriEst Ag Group Inc.

- VFC

- Industrial Fumigation Company

제7장 시장 기회와 향후 동향

제8장 COVID-19가 시장에 미치는 영향 평가

LSH 24.03.13The Agricultural Fumigants Market size is estimated at USD 2.45 billion in 2024, and is expected to reach USD 3.22 billion by 2029, growing at a CAGR of 5.60% during the forecast period (2024-2029).

The COVID-19 pandemic disrupted the operations of the crop protection chemicals market, including fumigants. The pandemic affected supply chain networks, resulting in losses for companies and farmers. In terms of supply, a short-term shortage of migrant laborers amid distribution bottlenecks created a wide gap between the number of workers required for production. Some other restraints included customs clearances, export permits, import permits, and phytosanitary certificates.

The agricultural fumigants market is driven by factors, like rapid technological advancements in the agricultural sector, growing concerns over post-harvest losses, and a shift in the advanced farming practices, which have led to increased yields. The use of fumigants during storage helps in the reduction of storage loss. Thus, the demand for fumigants is expected to increase as the use of fumigants is an effective and economical method to reduce post-harvest losses.

A widely used fumigant for storing agricultural commodities while offering protection against insects and rodents, phosphine-based fumigants have emerged as the largest segment among all types of global fumigants. North America dominates the market. With rapid investments in technology and R&D, many new varieties of products are being developed with less toxicity and more efficiency. The growth of the agricultural fumigants market can be attributed to several factors, such as the increased inclination of consumers for improving the quality of agricultural output, changing farming practices, and advanced storage technology. However, fumigants cause several problems, including possible phytotoxicity, depending on the type of crop and its variety, seasonal conditions, humidity, temperature, fumigant concentration, and duration of treatment. Therefore, it is recommended to be used by professional fumigators only due to its high toxicity as a respiratory poison.

Agricultural Fumigants Market Trends

Growing Agricultural Production

In line with increasing agricultural production, the demand for fumigants has been witnessing an upward trend over the years. The use of fumigation has increased at all levels of the grain and oilseeds supply chain, emerging as the main insect management option at the farm level. For farm-level storage and in silos, fumigation is among the most preferred methods to prevent the build-up of insect infestations while avoiding pest resistance. However, the available active substances are constrained to a limited number of fumigants and storage insecticides due to legislative restrictions. Methyl bromide (MB) fumigation is an effective treatment to ensure that products pose a minimal phytosanitary risk. While the European Union has banned the use of MB, Canada still requires it as the only approved treatment for the quarantine and pre-shipment applications of some products.

The Food and Agriculture Organization (FAO) of the United Nations has predicted that agricultural productivity is likely to increase by 70% by 2050 in order to meet the growing demand for food. The demand for agricultural crops is expected to rise to around 6,759 million ton by 2050. Global cereal production increased from 2906.5 million ton in 2018 to 2996.1 million ton in 2020. Thus, the demand for agricultural warehouses, storage technologies, and associated products, like fumigants, is anticipated to grow in the long run. In warehouses, pests damage most crops, and the use of fumigants decrease the loss of agricultural products. Therefore, this is expected to boost demand for the agricultural fumigants market across the world.

North America Leading the Global Market

North America is the largest market for agricultural fumigants, with over 250 authorized products available in its major countries. Management of stored product insects is a major concern and widely researched topic in the food and grain processing and storage industry.

The major commodities consuming fumigants for both storage and soil applications in the region are corn, rice, barley, potato, tomato, wheat, strawberry, cabbage, etc. In North America, the United States is the largest market, accounting for more than half of the regional market's share. The major fumigants in the US market include chloropicrin, sulfuryl fluoride, aluminum phosphide, ethylene oxide, etc. Over 90 fumigant-based products are registered in Canada, manufactured by 25 companies. A few key players are AMVAC Chemicals, Degesch America Inc., Syngenta Canada Inc., United Phosphorus Inc., etc.

Agricultural Fumigants Industry Overview

The global agricultural fumigants market is consolidated, with a few companies occupying the largest market share. The markets in North America and Europe are highly consolidated, with a few major players occupying large market shares and having a high level of competition. Diversification of portfolios through R&D, which is the backbone of the introduction of new products, is one of the prominent strategies being applied to the matured markets for further intensification.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Methyl Bromide

- 5.1.2 Chloropicrin

- 5.1.3 Phosphine

- 5.1.4 Metam Sodium

- 5.1.5 1,3-Dichloropropene

- 5.1.6 Other Agricultural Fumigants

- 5.2 Method of Application

- 5.2.1 Soil

- 5.2.2 Warehouse

- 5.3 Form

- 5.3.1 Solid

- 5.3.2 Liquid

- 5.3.3 Gas

- 5.4 Crop Application

- 5.4.1 Crop-based

- 5.4.2 Non-crop-based

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Russia

- 5.5.2.5 Spain

- 5.5.2.6 Italy

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 DowDuPont

- 6.3.2 Amvac Chemical Corporation

- 6.3.3 Syngenta AG

- 6.3.4 UPL Group

- 6.3.5 Detia Degesch GmbH

- 6.3.6 ADAMA Agricultural Solution Ltd

- 6.3.7 BASF SE

- 6.3.8 Cytec Solvay Group

- 6.3.9 FMC Corporation

- 6.3.10 Fumigation Services

- 6.3.11 Ikeda Kogyo Co. Ltd

- 6.3.12 Industrial Fumigation Company

- 6.3.13 Isagro SpA

- 6.3.14 Lanxess

- 6.3.15 Reddick Fumigants LLC

- 6.3.16 Trical Inc.

- 6.3.17 TriEst Ag Group Inc.

- 6.3.18 VFC

- 6.3.19 Industrial Fumigation Company