|

시장보고서

상품코드

1444032

세계 임상 의사 결정 지원 시스템 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2024-2029년)Clinical Decision Support Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

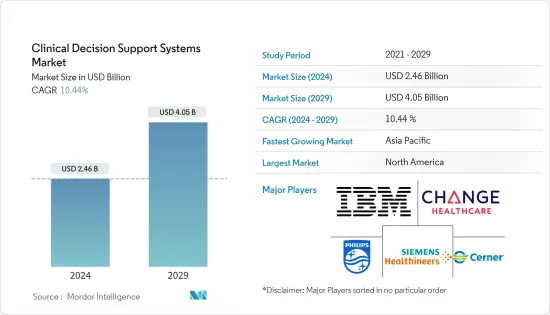

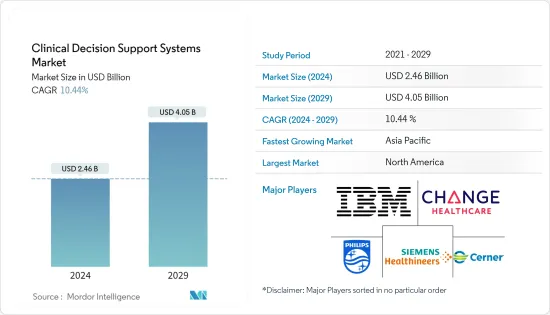

임상 의사 결정 지원 시스템 시장 규모는 2024년 24억 6,000만 달러로 추정되며, 2029년 40억 5,000만 달러에 이를 것으로 예측되며, 예측 기간(2024-2029년)의 CAGR은 10.44%로 성장할 전망입니다.

COVID-19가 유행하는 가운데, 각국의 의료 시스템은 온라인 서비스에 크게 의존하고 있었습니다. 헬스케어 전문가들은 가상의 출처를 통해 환자의 진찰을 받았습니다. 이는 주로 팬데믹의 초기 단계에서 각국 정부가 엄격한 봉쇄규제를 부과했기 때문입니다. 게다가 COVID-19가 세계에서 유행했기 때문에 임상 판단 지원 시스템은 환자의 자원과 서비스를 지원하는 데 중요한 역할을 했습니다. 예를 들어, 2021년 3월에 발표된 Plos One 잡지의 논문에서 COVID-19의 실시간 임상 진단을 위한 의사결정 지원 도구의 개발은 환자의 치료를 지원하고 위험한 환자에게 자원을 할당에 매우 중요하다고합니다. 일부 국가에서는 온라인 서비스 제공이 증가하고 있으며, 이는 시장을 밀어 올리고 있습니다. 또한 다양한 시장 기업들이 COVID-19 데이터와 통찰력 관리를 위한 임상 의사결정 지원 시스템을 출시했습니다. 예를 들어, 2022년 5월, Epocrates는 임상 의사결정 지원 가이드라인 라이브러리를 확장하기 위해 최신 업데이트를 통합한 혁신적인 긴 COVID-19 도구를 출시했습니다. 이와 같이 임상 의사결정 지원 시스템의 도입과 출시 증가는 유행 기간 동안 시장 성장을 뒷받침했습니다.

의료비 절감에 대한 수요 증가, 케어의 질 향상에 대한 요구, 병원의 건강 관리 IT의 기술적 진보는 임상 의사 결정 지원 시스템(CDSS) 시장의 성장을 뒷받침하는 주요 요인입니다. 또한 경제협력개발기구(OECD)의 조사 보고서에 따르면 2021년 1인당 평균 의료비는 독일에서 약 7,382.6달러, 노르웨이에서 7,064.8달러, 스웨덴에서 6,262.3달러였습니다. 따라서 의료비의 높이도 시장 성장에 기여할 것으로 예상됩니다.

2022년 11월에 발표된 Science direct의 연구에 따르면, 하이브리드 최적화 학습 알고리즘은 정확도, 감도, 특이도 지표를 가졌습니다. 그 결과, 제안된 모델은 사회 불안 장애의 진단에 매우 적합하고, 다른 연구 결과와 일치하는 것으로 나타났습니다. 임상 의사 결정 지원 시스템의 이러한 효율성은 시장 성장에 기여할 것으로 예상됩니다.

또한 노년 인구 증가도 시장 성장에 기여할 것으로 예상됩니다. 2022년 10월에 발표된 WHO 데이터에 따르면 60세 이상 인구는 2030년에는 14억 명으로 증가했으며 2050년에는 21억 명에 이를 것으로 예측됩니다. 2022년 유엔 보고서는 65세 이상의 인구에서 차지하는 비율이 2022년의 10%에서 2050년에는 16%로 상승할 것으로 예측됩니다. 만성 질환을 발병하기 쉽고 질병 예방을 위해 정기적인 건강 진단 및 치료가 필요한 노년 인구는 고급 임상 의사 결정 지원 시스템 수요를 촉진하고 시장 성장에 기여할 것으로 예상됩니다.

또한 임상 의사결정 지원 시스템 개발을 위한 공동 연구와 파트너십 등의 이니셔티브 증가가 시장 성장에 기여할 것으로 기대되고 있습니다. 예를 들어, 2021년 6월 구글 클라우드는 전국 병원 체인의 HCA 건강 관리와 다년간 계약을 체결하고 임상 의사 결정을 개선하기 위해 맞춤형 건강 관리 알고리즘을 만들었습니다.

따라서 의료비 증가 및 임상 의사결정 지원 시스템 시장 개척을 위한 노력 증가는 시장 성장에 기여할 것으로 기대됩니다. 그러나 CDSS는 개발의 초기 단계에 있기 때문에 시스템에 대한 신뢰 부족, 숙련 노동자 부족, 불필요한 진단 검사를 CDSS에서 제안하는 등이 시장 개척의 방해가 되고 있습니다.

CDSS 시장 동향

예측 기간 동안 클라우드 기반 부문이 큰 시장 점유율을 차지할 전망

헬스케어 지출 증가와 클라우드 컴퓨팅의 채용이 클라우드 기반 부문 시장 확대의 주요 요인이 되고 있습니다. 유럽의 각국 정부는 건강 관리에서 정보 기술의 성장을 지원하기 위해 노력하고 있습니다. 예를 들어 영국 정부는 2021년 2월 완전히 연결된 클라우드 중심의 의료 서비스를 채택하는 이니셔티브를 시작했습니다. 이 이니셔티브에 따라 2백만 개 이상의 NHS(국민 보건 서비스) 사서함이 Microsoft의 Azure Cloud로 마이그레이션되었습니다. 이를 통해 NHS 조직과 부서를 넘어 직원 간의 원활하고 효율적인 커뮤니케이션이 가능하며 정보에 대한 액세스도 개선됩니다. 이로 인해 영국에서의(Healthcare Information Technology) HCIT 변경 관리 서비스의 이용이 증가하고 시장 성장이 촉진됩니다.

또한 임상 의사결정 지원 시스템(CDSS)의 로컬 지식 관리는 대규모 처리 능력과 스토리지 용량을 필요로 할 수 있으며 운영 비용이 높아질 수 있습니다. 대조적으로 클라우드 기반 용도는 원격지 서버에서 작동하기 때문에 실행 시 사용자 단말기에 대량의 계산 능력이나 대용량 스토리지가 필요하지 않습니다.

클라우드 기반 용도는 웹 브라우저에 의존하지 않으므로 웹 기반 용도보다 본질적으로 안전합니다. 클라우드 기반 임상 판단 지원 시스템에서 처리 장치는 원격지 서버에 호스팅되며, 서버는 세계 여러 데이터센터에 배치될 수 있으므로 사이버 공격에 취약성이 낮습니다. 클라우드 기술을 사용할 수 있게 되면 클라우드 기반 CDSS의 사용이 예측 기간 동안 증가할 것으로 예상됩니다.

예측기간 중 북미가 시장에서 큰 점유율을 차지할 전망

북미의 임상 의사결정 지원 시스템(CDSS) 시장은 CDSS의 기술적 진보, 환자의 높은 인지도, 건강 관리 IT 솔루션에 대한 투자 증가로 인한 것입니다.

또한 북미의 건강 관리 지원을 위한 정부의 자금 지원이 증가하고 있는 것도 미국에서 시장 성장의 요인이 되고 있습니다. 예를 들어, 미국 의회 예산국(2021년)은 지난 수십년간 국립위생연구소(NIH)에 대한 연방 정부의 자금이 총 7,000억 달러를 초과했다고 발표했습니다.

게다가, 다양한 시장 선수들이 이 지역에서 점점 더 진보된 제품을 출시하는 것은 시장 성장에 기여할 것으로 예상됩니다. 예를 들어, 2021년 8월, First Databank, Inc.는 라스베가스에서 개최된 2021 HIMSS Global conference and exhibition에서 FDB CDS Analytics를 발표했습니다. 이 솔루션을 통해 의료 제공업체 조직은 전자 의료 기록에서 임상 의사 결정 지원을 쉽게 식별, 모니터링 및 사용자 정의할 수 있습니다.

마찬가지로, 2021년 6월 캐나다의 건강 관리 회사 Pathway는 공급자에게 증거 기반 임상 지원을 제공했으며, 최초의 자금 조달 라운드에서 130만 달러를 조달했습니다. 이 자금 조달을 통해 회사는 임상 의사 결정 지원 시스템을 강화하고 궁극적으로 건강 관리의 효율성을 높이는 것을 목표로했습니다.

투자 증가, CDSS 출시, 의학적 자금 지원 등 북미의 CDSS 시장 예측 기간 동안 성장을 가속할 수 있습니다.

CDSS 산업 개요

임상 의사 결정 지원 시스템 시장에는 국제적, 지역적, 지역적으로 다양화된 기업이 존재합니다. 그러나 일부 국제적인 대기업들은 브랜드 이미지와 시장 도달범위로 시장을 독점하고 있습니다. 시장은 세분화되고 경쟁이 심합니다. 주요 시장 기업은 Siemens Healthcare, Koninklijke Philips NV, IBM, Cerner Corporation, Change Healthcare 등이 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- 병원에서의 건강 관리 IT 기술 진보

- 헬스케어 지출 삭감에 대한 수요 증가

- 의료 질 향상과 휴먼 에러 삭감의 필요성

- 시장 성장 억제요인

- 클라우드 기반 CDSS에 대한 개인정보 보호 및 데이터 보안 우려

- 숙련된 전문가의 부족

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자/소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화

- 모델별

- 지식형 CDSS

- 비지식형 CDSS

- 제공 형태별

- 클라우드 기반

- 온프레미스

- 컴포넌트별

- 하드웨어

- 소프트웨어

- 서비스

- 제품별

- 통합형 CDSS

- 독립형 CDSS

- 용도별

- 의료진단

- 알림 및 알림

- 처방 결정 지원

- 정보 검색

- 기타 용도

- 지역

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 기업 프로파일

- Cerner Corporation

- Epic Systems Corporation

- IBM

- Change Healthcare

- Medical Information Technology Inc.

- Koninklijke Philips NV

- Siemens Healthcare

- Allscripts Healthcare Solutions Inc.

- Wolters Kluwer NV

- Mckesson Corporation

- Zynx Health Inc.

- Elsevier

- NextGen Healthcare Inc.

- Agfa-Gevaert Group

- Athenahealth Inc.

- VisualDx

제7장 시장 기회와 앞으로의 동향

JHS 24.03.15The Clinical Decision Support Systems Market size is estimated at USD 2.46 billion in 2024, and is expected to reach USD 4.05 billion by 2029, growing at a CAGR of 10.44% during the forecast period (2024-2029).

Amid the COVID-19 pandemic, the health systems of countries were majorly dependent on online services. Healthcare professionals were taking up a consultation with the patients through virtual sources. This was mainly due to the strict lockdown regulations imposed by various governments during the initial stages of the pandemic. Moreover, due to the COVID-19 outbreak across the world, clinical decision support systems played a vital role in assisting patient resources and services. For instance, the Journal Plos One article published in March 2021 mentioned that the development of decision support tools for real-time clinical diagnosis of COVID-19 is of prime importance of assist patient triage and allocating resources for patients at risk. Several countries are increasingly providing online services, which is boosting the market. Additionally, various market players launched clinical decision support systems for the management of COVID-19 data and insights. For instance, in May 2022, Epocrates launched an innovative long COVID-19 tool that incorporates late-breaking updates to expand the library of clinical decision support guidelines. Thus the increased adoption and launches of clinical decision support systems boosted the growth of the market during the pandemic.

The rising demand for reducing healthcare expenditure, the need for improvement in the quality of care, and technological advancements in healthcare IT in hospitals are the major factors that are likely to boost the growth of the clinical decision support systems (CDSS) market. Furthermore, according to the Organization for Economic Co-operation and Development (OECD) Survey Report, in 2021, the average per capita health expenditure was about USD 7,382.6 in Germany, USD 7,064.8 in Norway, and USD 6,262.3 in Sweden. Thus, the high healthcare expenditure is also expected to contribute to the growth of the market.

According to the Science direct study published in November 2022, the hybrid optimization learning algorithm had accuracy, sensitivity, and specificity metrics. The results revealed that the proposed model was quite appropriate for social anxiety disorder diagnosis and in line with the findings of other studies. Such efficiency of clinical decision support systems is expected to contribute to the growth of the market.

Additionally, the rising geriatric population is also expected to contribute to the growth of the market. According to the WHO data published in October 2022, the population aged 60 years and over will increase to 1.4 billion in 2030 and is expected to reach 2.1 billion by 2050. The UN report in 2022 mentioned that the share of the population aged 65 years or over is projected to rise from 10% in 2022 to 16% in 2050. The geriatric population who are vulnerable to developing chronic diseases and needs regular health checks and treatments for the prevention of diseases is expected to drive the demand for advanced clinical decision support systems, thereby contributing to the growth of the market.

Moreover, increasing initiatives such as collaborations and partnerships to develop clinical decision support systems are expected to contribute to the growth of the market. For instance, in June 2021, Google cloud entered into a multi-year agreement with the national hospital chain HCA healthcare to create customized healthcare algorithms to improve clinical decision-making.

Thus, the increasing healthcare expenditure and increasing initiatives for the development of clinical decision support systems are expected to contribute to the growth of the market. However, lack of trust in the systems, as CDSS are in the initial stages of development, lack of skilled labor, and suggestions from CDSS for unnecessary diagnostic testing hinder the market growth.

CDSS Market Trends

The Cloud-based Segment is Expected to Hold a Major Market Share Over the Forecast Period

The increasing healthcare expenditure and adoption of cloud computing are the major drivers for the expansion of the cloud-based segment of the market. The government in various countries in the European region are taking initiatives to support the growth of information technology in healthcare. For instance, in February 2021, the UK government launched an initiative to adopt a fully connected cloud-driven health service. Under this initiative, over two million National Health Services (NHS) mailboxes were moved to Microsoft's Azure Cloud. This will enable smoother and more efficient communication between staff across NHS organizations and departments and provide improved access to information. This will increase the usage of (Healthcare Information Technology) HCIT Change Management services in the United Kingdom and boost the market's growth.

Furthermore, local knowledge management of clinical decision support systems (CDSS) may require extensive processing power and storage capacity, which can result in high operating costs. In contrast, cloud-based applications are operated on remote servers, and executing them does not require a large amount of computational power or large storage space in the user's device.

Cloud-based applications do not depend on web browsers, which makes them inherently safer than web-based applications. In a cloud-based clinical decision support system, processing units are hosted on remote servers, which can be located in multiple data centers across the world, making them less vulnerable to cyberattacks. The increasing availability of cloud technology, owing to its benefit, is expected to drive the usage of cloud-based CDSS over the forecast period.

North America is Expected to Hold a Significant Share in the Market During the Forecast Period

The clinical decision support systems (CDSS) market in North America is driven due to the rise in the technological advancement in CDSS, the high awareness among patients, and rising investments in healthcare IT solutions in the region.

Also, the increasing funding from the government in North America for supporting healthcare is an attributing factor to the growth of the market in the United States. For instance, the Congressional Budget Office,2021, published that in the past few decades, federal funding for the National Institute of Health (NIH) has totaled over USD 700 billion.

Additionally, the increasingly advanced product launches in this region by various market players are also expected to contribute to the growth of the market. For instance, in August 2021, First Databank, Inc launched the FDB CDS Analytics, during the 2021 HIMSS Global conference and exhibition in Las Vegas. The solution enables healthcare provider organizations to easily identify, monitor, and customize clinical decision support in their electronic health record.

Similarly, in June 2021, a Canadian Healthcare company Pathway which offers, evidence-based clinical support to providers, raised USD 1.3 million in its first round of financing. With this financing, the company aimed to enhance clinical decision support systems which eventually increase healthcare efficiency.

These factors such as increasing investments, CDSS launches, and high funding for healthcare, may fuel the growth of the CDSS market over the forecast period in North America.

CDSS Industry Overview

The clinical decision support systems market has the presence of well-diversified international, regional, and local players. However, some big international players dominate the market, owing to their brand image and market reach. The market is fragmented and competitive in nature. some of the major market players include Siemens Healthcare, Koninklijke Philips NV, IBM, Cerner Corporation, Change Healthcare and Others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Technological Advancement in Healthcare IT in Hospitals

- 4.2.2 Rising Demand to Reduce Healthcare Expenditure

- 4.2.3 Need for Improvement in Quality of Care and Reducing Human Errors

- 4.3 Market Restraints

- 4.3.1 Privacy and Data Security Concerns Related to Cloud-based CDSS

- 4.3.2 Lack of Skilled Professionals

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Model

- 5.1.1 Knowledge-based CDSS

- 5.1.2 Non-knowledge CDSS

- 5.2 By Mode of Delivery

- 5.2.1 Cloud-based

- 5.2.2 On-premise

- 5.3 By Component

- 5.3.1 Hardware

- 5.3.2 Software

- 5.3.3 Services

- 5.4 By Product

- 5.4.1 Integrated CDSS

- 5.4.2 Standalone CDSS

- 5.5 By Application

- 5.5.1 Medical Diagnosis

- 5.5.2 Alerts and Reminders

- 5.5.3 Prescription Decision Support

- 5.5.4 Information Retrieval

- 5.5.5 Other Applications

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Cerner Corporation

- 6.1.2 Epic Systems Corporation

- 6.1.3 IBM

- 6.1.4 Change Healthcare

- 6.1.5 Medical Information Technology Inc.

- 6.1.6 Koninklijke Philips NV

- 6.1.7 Siemens Healthcare

- 6.1.8 Allscripts Healthcare Solutions Inc.

- 6.1.9 Wolters Kluwer NV

- 6.1.10 Mckesson Corporation

- 6.1.11 Zynx Health Inc.

- 6.1.12 Elsevier

- 6.1.13 NextGen Healthcare Inc.

- 6.1.14 Agfa-Gevaert Group

- 6.1.15 Athenahealth Inc.

- 6.1.16 VisualDx