|

시장보고서

상품코드

1640323

풍력 터빈용 기어박스 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Wind Turbine Gearbox - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

가격

※ 부가세 별도

한글목차

영문목차

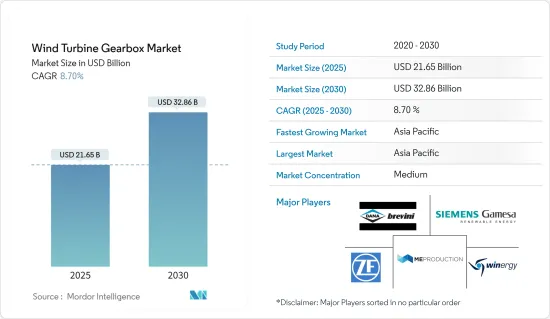

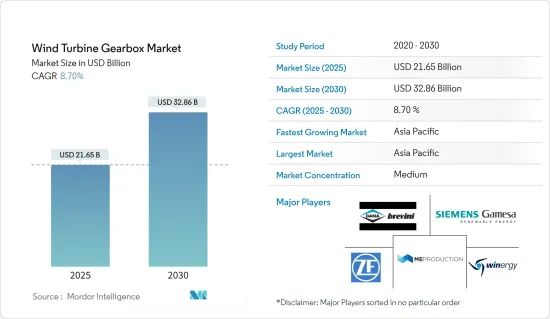

풍력 터빈용 기어박스 시장 규모는 2025년 216억 5,000만 달러로 추정되며, 2030년에는 328억 6,000만 달러에 달할 것으로 예상되며, 예측 기간(2025-2030년) 동안 8.7%의 CAGR을 기록할 것으로 예상됩니다.

주요 하이라이트

- 중기적으로는 풍력에너지 수요 확대와 풍력에너지 프로젝트에 대한 투자 증가 등의 요인이 예측 기간 동안 풍력 터빈용 기어박스 시장의 가장 큰 촉진요인 중 하나가 될 것으로 예상됩니다.

- 한편, 태양광, 수력 등 다른 재생에너지원의 보급이 증가하고 있습니다. 이는 예측 기간 동안 풍력 터빈용 기어박스 시장에 위협이 될 것입니다.

- 풍력에너지와 에너지 저장의 통합과 세계 각지의 야심찬 풍력에너지 건설은 향후 시장에 몇 가지 기회를 창출할 것으로 예상되는 중요한 요인입니다.

- 아시아태평양은 풍력발전 측면에서 큰 점유율을 차지하고 중국, 인도, 일본 등의 국가에 제조 기술 기반이 존재하기 때문에 가장 크고 가장 빠르게 성장하는 시장이 될 것으로 예상됩니다.

풍력 터빈용 기어박스 시장 동향

오프쇼어 부문 높은 성장세 기록

- 해상 풍력발전 부문은 전 세계적으로 빠르게 성장하고 있습니다. 정부와 에너지 기업들은 해상에서 이용 가능한 강력하고 안정적인 풍력 자원을 활용하기 위해 해상 풍력 프로젝트에 대한 투자를 늘리고 있습니다.

- 2022년 세계풍력에너지위원회(Global Wind Energy Council)는 8GW의 해상 풍력발전 용량이 추가될 것이라고 보고했으며, 그 결과 전 세계 설치 용량은 64GW가 될 것으로 예상했습니다. 이는 2021년 설치 용량 56GW에 비해 증가한 수치입니다. 해상 풍력발전 용량의 확대는 해상 풍력발전소 개발을 지원하는 풍력 터빈용 기어박스에 대한 수요 증가로 이어집니다.

- 많은 국가들은 지리적 위치와 양호한 풍황으로 인해 큰 해상 풍력에너지 잠재력을 가지고 있습니다. 북유럽, 미국, 중국, 대만 등의 지역에서는 해상 풍력 자원을 적극적으로 개발하고 있습니다. 이들 지역은 해상 풍력 개발로 인한 수요 증가에 대응하기 위해 풍력 터빈용 기어박스 제조업체에게 큰 시장 기회를 제공하고 있습니다.

- 예를 들어, 독일은 2023년 1월, 2030년까지 30기가와트(GW)의 풍력발전 설비 용량 목표를 달성하기 위해 해상 풍력 터빈 부지에 대한 새로운 개발 전략 수립을 발표했습니다. 연방해수청(BSH)은 설정된 목표를 달성하기 위해 이러한 계획을 수립했습니다.

- 마찬가지로 인도는 7,600km에 달하는 광활한 해안선에 펼쳐진 미개발 해상 풍력발전 잠재력을 활용하여 그린에너지 포트폴리오를 다양화하고자 합니다. 신재생에너지부는 2030년까지 30GW의 해상 풍력발전 용량을 달성하겠다는 목표를 세우고 있습니다. 이러한 야심찬 목표는 대규모 해상 풍력발전 프로젝트 개발에 박차를 가하고 풍력 터빈용 기어박스에 대한 수요를 촉진할 것으로 예상됩니다.

- 따라서, 위의 관점에서 볼 때, 예측 기간 동안 오프쇼어 부문이 시장을 독점할 것으로 예상됩니다.

아시아태평양이 괄목할 만한 성장을 이뤄

- 아시아태평양은 풍력발전 설비 용량이 크게 증가하고 있습니다. 중국, 인도, 일본, 호주 등의 국가들은 증가하는 전력 수요를 충족하고 온실 가스 배출을 줄이기 위해 풍력발전 프로젝트에 많은 투자를 하고 있습니다. 이 지역의 풍력발전 용량의 확대는 풍력 터빈용 기어박스에 대한 수요를 촉진하고 있습니다.

- Global Wind Energy Council에 따르면, 아시아태평양은 2022년에만 약 37GW의 풍력발전 용량을 추가하여 이 지역의 풍력에너지가 크게 성장할 것으로 예상됩니다.

- 아시아태평양의 많은 국가들은 풍력발전을 포함한 재생에너지를 촉진하기 위한 지원책과 인센티브를 시행하고 있습니다. 이러한 정책은 풍력에너지 개발을 위한 환경을 조성하고 풍력 터빈 설치에 대한 투자를 유치하고 있습니다.

- 예를 들어, 아세안 각국 정부는 2021-2025년 아세안 에너지 협력을 위한 아세안 행동계획(APAEC) 2단계의 일환으로 야심찬 5개년 지속가능성 계획을 발표했습니다. 이 계획에 따라 아세안 국가 에너지 장관들은 2025년까지 아세안 전체 1차 에너지 공급량에서 재생에너지의 비중을 23%, 아세안 발전설비 용량에서 재생에너지의 비중을 35%까지 늘리기로 합의했습니다. 이러한 목표를 달성하기 위해서는 2025년까지 약 35GW-40GW의 재생에너지 용량을 추가해야 합니다. 대부분의 국가에서 풍력발전의 잠재력이 높기 때문에 이 지역에서는 풍력발전 설치가 증가할 것으로 예상됩니다.

- 향후 10년간 풍력 터빈용 기어박스 수리 및 개조 시장은 아시아태평양의 급속히 확대되는 설치 기반과 정부 지원 정책에 힘입어 큰 성장 기회를 맞이할 것으로 예상됩니다.

풍력 터빈용 기어박스 산업 개요

풍력 터빈용 기어박스 시장은 적당히 통합되어 있습니다. 주요 기업으로는 Siemens Gamesa Renewable Energy SA, Dana Brevini SpA, ME Production A/S, Winergy Group, ZF Friedrichshafen AG 등이 있습니다.

기타 혜택

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

목차

제1장 소개

- 조사 범위

- 시장 정의

- 조사 가정

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

- 소개

- 2028년까지 시장 규모와 수요 예측(단위 : 달러)

- 최근 동향과 개발

- 정부 정책 및 규정

- 시장 역학

- 성장 촉진요인

- 풍력에너지 도입 증가

- 풍력에너지에 대한 투자 증가

- 성장 억제요인

- 기타 재생에너지원 보급 확대

- 성장 촉진요인

- 공급망 분석

- Porter's Five Forces 분석

- 공급 기업의 교섭력

- 소비자의 협상력

- 신규 참여업체의 위협

- 대체품의 위협

- 경쟁 기업 간의 경쟁 강도

제5장 시장 세분화

- 전개 장소

- 온쇼어

- 오프쇼어

- 2028년까지 시장 규모·수요 예측(지역별)

- 북미

- 미국

- 캐나다

- 기타 북미

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 기타 아시아태평양

- 유럽

- 영국

- 독일

- 프랑스

- 스페인

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 칠레

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트

- 남아프리카공화국

- 기타 중동

- 북미

제6장 경쟁 구도

- M&A, 합작투자, 제휴, 협정

- 주요 기업의 전략

- 기업 개요

- Dana Brevini SpA

- Siemens Gamesa Renewable Energy SA

- ME Production AS

- Stork Gears & Services BV

- Winergy Group

- ZF Friedrichshafen AG

- Turbine Repair Solutions

- Elecon Engineering Company Limited

제7장 시장 기회와 향후 동향

- 에너지 저장의 통합

The Wind Turbine Gearbox Market size is estimated at USD 21.65 billion in 2025, and is expected to reach USD 32.86 billion by 2030, at a CAGR of 8.7% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as growing demand for wind energy and increasing investment in wind energy projects are expected to be one of the most significant drivers for the wind turbine gearbox market during the forecast period.

- On the other hand, increasing penetration of other sources of renewable energy such as solar, hydro and others. This poses a threat to the wind turbine gearbox market during the forecast period.

- Nevertheless, energy storage integration with wind energy and ambitious wind energy tsrgets acrossb the globe are significant factors expected to create several opportunities for the market in the future.

- The Asia-Pacific region is expected to be the largest and fastest-growing market, owing to the significant share in terms of wind power generation and the presence of manufacturing and technology hubs in countries like China, India, Japan, etc.

Wind Turbine Gearbox Market Trends

Offshore Segment to Register Higher Growth

- The offshore wind sector has been experiencing rapid growth worldwide. Governments and energy companies increasingly invest in offshore wind projects to harness the strong and consistent wind resources available at sea.

- In 2022, the Global Wind Energy Council reported the addition of 8 GW of offshore wind energy capacity, resulting in a global installed capacity of 64 GW. This marks an increase compared to the 56 GW installed capacity in 2021. The expansion of offshore wind capacity translates into higher demand for wind turbine gearboxes to support the development of offshore wind farms.

- Many countries possess significant offshore wind energy potential due to their geographical location and favorable wind conditions. Regions such as Northern Europe, the United States, China, and Taiwan are actively developing their offshore wind resources. These regions offer substantial market opportunities for wind turbine gearbox manufacturers to cater to the growing demand driven by offshore wind development.

- For instance, in January 2023, Germany announced the formulation of new development strategies for offshore wind turbine sites in order to achieve a target of 30 gigawatts (GW) of installed wind power capacity by 2030. The Federal Maritime and Hydrographic Agency (BSH) has devised these plans to ensure the successful attainment of the set target.

- In a similar vein, India aims to diversify its green energy portfolio by tapping into the untapped offshore wind energy potential across its extensive 7,600-kilometer coastline. The Ministry of New and Renewable Energy has established a target of achieving 30 GW of offshore wind capacity by 2030. These ambitious goals are projected to spur the development of large-scale offshore wind projects, thereby driving the demand for wind turbine gearboxes.

- Therefore as per the above-mentioned points the offshore segment is expected to dominate the market during the forecasted period.

Asia-Pacific to Witness Significant Growth

- The Asia Pacific region has been witnessing substantial growth in wind power capacity installations. Countries like China, India, Japan, and Australia are making significant investments in wind energy projects to meet their growing electricity demands and reduce greenhouse gas emissions. This region's expansion of wind power capacity drives the demand for wind turbine gearboxes.

- According to Global Wind Energy Council the Asia-Pacific region added almost 37GW of wind energy capacity in 2022 alone signifying significant growth of wind energy in the region with China contributing 87% of its 2022 additions consequently driving the demand for wind turbine gearboxes.

- Many countries in the Asia Pacific region have implemented supportive policies and incentives to promote renewable energy, including wind power. These policies create a conducive environment for wind energy development and attract investments in wind turbine installations.

- For instance, ASEAN governments have unveiled an ambitious five-year sustainability plan as part of the second phase of the ASEAN Plan of Action for Energy Cooperation (APAEC) from 2021 to 2025. As per this plan, energy ministers from ASEAN countries have agreed to a target of achieving a 23% share of renewable energy in the total primary energy supply across the region, along with a 35% share in ASEAN's installed power capacity by 2025. Meeting these targets would necessitate the addition of approximately 35GW-40GW of renewable energy capacity by 2025. This is expected to increase the installations of wind energy in the region due to the high wind energy potential in the majority of the countries.

- Over the next decade, the wind turbine gearbox repair and refurbishment market is anticipated to witness substantial growth opportunities driven by the rapidly expanding installed base in the Asia-Pacific region and supportive government policies.

Wind Turbine Gearbox Industry Overview

The wind turbine gearbox market is moderately consolidated. Some of the major companies (in no particular order) include Siemens Gamesa Renewable Energy SA, Dana Brevini SpA, ME Production A/S, Winergy Group, and ZF Friedrichshafen AG, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Adoption of Wind Energy

- 4.5.1.2 Growing Investments in Wind Energy

- 4.5.2 Restraints

- 4.5.2.1 Increasing Penetration of Other Sources of Renewable Energy

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Location of Deployment

- 5.1.1 Onshore

- 5.1.2 Offshore

- 5.2 Geography [Market Size and Demand Forecast till 2028 (for regions only)]

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Rest of North America

- 5.2.2 Asia-Pacific

- 5.2.2.1 China

- 5.2.2.2 India

- 5.2.2.3 Japan

- 5.2.2.4 Asutralia

- 5.2.2.5 Rest of Asia-Pacific

- 5.2.3 Europe

- 5.2.3.1 United Kingdom

- 5.2.3.2 Germany

- 5.2.3.3 France

- 5.2.3.4 Spain

- 5.2.3.5 Rest of Europe

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Chile

- 5.2.4.4 Rest of South America

- 5.2.5 Middle-East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 United Arab Emirates

- 5.2.5.3 South Africa

- 5.2.5.4 Rest of Middle East

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Dana Brevini SpA

- 6.3.2 Siemens Gamesa Renewable Energy SA

- 6.3.3 ME Production AS

- 6.3.4 Stork Gears & Services BV

- 6.3.5 Winergy Group

- 6.3.6 ZF Friedrichshafen AG

- 6.3.7 Turbine Repair Solutions

- 6.3.8 Elecon Engineering Company Limited

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Energy Storage Integration