|

시장보고서

상품코드

1444166

농업용 트랙터 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2024-2029년)Agricultural Tractors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

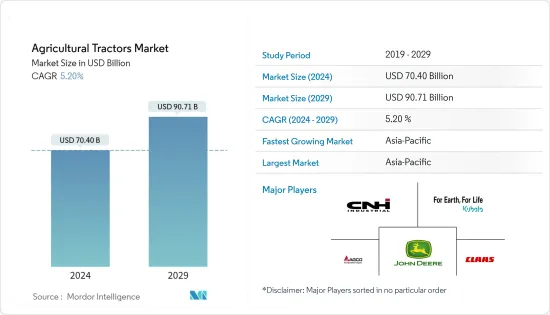

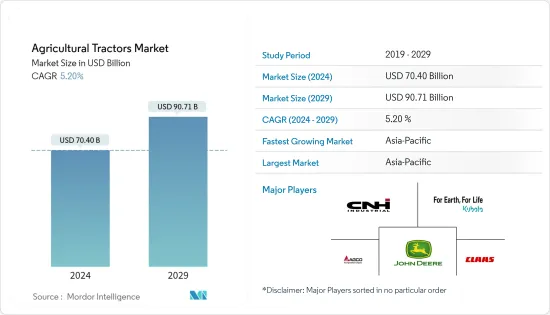

농업용 트랙터 시장 규모는 2024년 704억 달러로 추정되며 2029년까지 907억 1,000만 달러에 달할 것으로 예상되며, 예측 기간(2024-2029년) 동안 연평균 5.20%의 CAGR로 성장할 것으로 예상됩니다.

주요 하이라이트

- 트랙터는 경작, 경작, 모내기 등 농작업을 하는 데 사용되는 농기계입니다. 또한 비료 살포, 덤불 벌채 및 기타 활동에도 사용됩니다. 도시화와 도시로의 인구 이동으로 인해 인건비가 크게 상승하고 있습니다. 농장의 노동력 비용은 생산 비용에 정비례합니다. 기계화로 인해 노동자의 임금이 감소할 수 있습니다. 노동 임금 상승과 농업 노동력 부족으로 기계화율이 상승하고 있습니다.

- 또한, 높은 수확량을 얻기 위해 농업 기계화에 대한 정부 보조금 증가도 트랙터 보급 증가에 기여하고 있습니다. 또한, 기술 발전은 기계화의 증가와 함께 농업 기계화의 이점에 대한 농부들의 인식이 높아지면서 기계화의 증가에 대응하고 있습니다.

- 많은 기업들이 새로운 농업용 트랙터를 출시하고 있으며, 더 빠른 제품 출시와 발전으로 시장을 독점할 수 있게 되었습니다. 일부 주요 시장 기업은 최첨단 장비를 생산하고 시장에서 강력한 위치를 유지하기 위해 연구 개발에 자금을 투자하고 있습니다. 이 요인은 시장에서 트랙터 판매를 촉진합니다. 예를 들어, 2020년 Deere & Company는 8R 휠 트랙터, 8RT 2 트랙 트랙터, 업계 최초의 고정 프레임 4 트랙 트랙터를 포함한 새로운 8 제품군 트랙터 라인업을 출시했습니다. 이 새로운 트랙터에는 최신 정밀 농업 기술이 탑재되어 있어 고객은 작업에 가장 적합한 기계 구성, 옵션 및 마력을 선택할 수 있습니다. 한편, 특수한 최신 트랙터를 조작할 수 있는 적절한 숙련공의 부족은 트랙터 시장을 억제하는 요인으로 작용할 수 있습니다.

농업용 트랙터 시장 동향

개발도상국 시장에서의 농업 기계화 증가

- 정밀 농업과 생산량을 늘리기 위한 농업 기술의 채택이 증가함에 따라 트랙터에 대한 수요가 증가하고 있습니다. 농업 장비는 고정밀 포지셔닝 시스템(GPS 및 GNSS, 자동 조향 시스템, 지오 매핑, 센서, 원격 감지 등) 및 통합 전자 통신과 같은 기술을 사용하여 기계 작동에서 우수한 결과를 생성 할 수 있습니다. 예를 들어, Deere &Company는 트랙터 및 기타 품목과 같은 농업 기계에 Precision AG 기술을 제공합니다. 이 회사는 디스플레이 시스템, 파종 및 심기, 수확을위한 수신기, 밭 준비 및 경작 장비를 제공합니다. 이러한 품목의 출시는 농업용 트랙터 시장의 성장에 큰 영향을 미칩니다.

- 농기계 사용을 광범위하게 촉진하는 농업 교육 프로그램의 증가도 트랙터 산업에 힘을 실어주고 있습니다. 엔진 용량이 1,500cc 이하인 트랙터는 공간을 적게 차지하여 보다 유연하게 사용할 수 있습니다. 커스터마이징이 용이하기 때문에 실험이 용이하며, 그 결과 제조업체는 고출력 부품과 기술로 전환하기 전에 이 분야의 새로운 부품과 기술을 적극적으로 시도하려고 합니다. 저마력 트랙터는 강 유역과 같은 부드러운 토양 조건에서 잘 작동합니다. 40마력 미만의 트랙터는 주로 원예에 사용됩니다. 신흥국에서는 농가의 가처분 소득이 낮고 인건비가 높기 때문에 저마력 트랙터에 대한 수요가 높습니다. 농부들은 농지의 크기가 작기 때문에 농업용 맞춤형 소형 트랙터를 선호합니다. 또한 소형 트랙터로 인한 연료 소비 감소는 소규모의 한계 농가에 힘을 실어줄 수 있습니다. 인도와 같은 신흥국 정부는 장비 구매에 보조금을 지급하거나 프런트 엔드 에이전트를 통해 대량 구매를 지원함으로써 농업 기계화를 촉진하고 있습니다.

- 또한 신흥국의 수요 증가로 인해 시장의 주요 기업들이 신제품을 혁신하고 있습니다. 예를 들어, TAFE는 2021년 2 월에 새로운 DYNATRACK 시리즈를 출시했습니다. 이 제품은 역동적 인 성능, 정교한 기술, 탁월한 실용성 및 다재다능함을 제공하는 단일 강력한 트랙터로 설계된 고급 트랙터입니다. 이러한 요인들은 예측 기간 동안 시장을 주도할 수 있습니다.

아시아태평양이 시장을 독점

- 아시아태평양에서는 중국, 일본, 인도가 트랙터 판매량에서 선두를 달리고 있습니다. 중국 농업 활동의 약 60 %가 기계화되어 있습니다. 중국 국가 통계국의 데이터에 따르면 대형 및 중형 트랙터는 점차 소형 트랙터로 대체되고 있습니다. 2020년 말 현재 중국에는 440만 대의 대형 및 중형 트랙터가 있었습니다. 정부는 '중국 제조 2025' 캠페인에 농기계를 포함시켰습니다. 이 프로그램을 통해 중국은 대부분의 농기계를 국내에서 생산할 수 있게 되어 중국 내 트랙터 판매가 증가할 것으로 예상됩니다.

- 인도 대부분의 사람들은 농업에 의존하고 있습니다. 인도 브랜드 자산 재단에 따르면 인도 전체 인구의 58%가 농민입니다. 따라서 인도에는 큰 트랙터 시장이 존재합니다. 인도의 농업 부문에서는 동물의 힘과 인간의 힘의 사용이 크게 감소하고 있습니다. 대신 트랙터와 디젤 엔진과 같은 화석 연료로 구동되는 차량이 사용되고 있으며, 그 결과 전통적인 농업 공정에서 보다 기계화된 공정으로 전환되고 있습니다.

- 인도 정부는 기계화 수준을 높이기 위해 각종 장비에 대한 보조금 지급, 프런트 엔드 대리점의 대량 구매 지원 등 '균형 잡힌 농업 기계화'를 추진하고 있어 인도 트랙터 시장 강화가 기대됩니다. 예를 들어, 인도 정부는 트랙터 구매에 대한 융자 및 보조금 등 농업 기계에 대한 다양한 제도를 제공하고 있습니다. 또한 NABARD의 기준에 따르면, 8에이커의 토지를 소유한 농가는 9년 동안 12.5%의 이자율로 트랙터 대출을 받을 수 있습니다. 따라서 이 지역 정부의 프로그램 시행과 전국적인 트랙터 사용량 증가는 예측 기간 동안 시장을 견인할 것으로 예상됩니다.

농업용 트랙터 산업 개요

농업용 트랙터 시장은 통합되어 있으며, 주요 기업들이 큰 시장 점유율을 차지하고 있습니다. Deere and Company, Kubota Corporation, CNH Industrial NV, AGCO Corporation, CLAAS KGaA mbH가 시장의 주요 기업입니다. 신제품 출시, 제휴 및 인수는 세계 시장의 주요 기업들이 채택하는 주요 전략입니다.

기타 혜택

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

목차

제1장 서론

- 조사 가정과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- 시장 성장 억제요인

- 업계의 매력 - Porter's Five Forces 분석

- 공급 기업의 교섭력

- 구매자의 교섭력

- 신규 참여업체의 위협

- 대체 제품에 의한 위협

- 경쟁 기업간 경쟁 강도

제5장 시장 세분화

- 마력별

- 40 마력 미만

- 40 마력-99 마력

- 100 마력-150 마력

- 151 마력-200 마력

- 201 마력-270 마력

- 271 마력-350 마력

- 350마력 이상

- 유형별

- 과수원용 트랙터

- 줄뿌림 작물용 트랙터

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 기타 북미

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 러시아

- 폴란드

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 아프리카

- 남아프리카공화국

- 기타 아프리카

- 북미

제6장 경쟁 상황

- 가장 많이 채용되고 있는 전략

- 시장 점유율 분석

- 기업 개요

- Claas KGaA mbH

- Deere &Company

- Mahindra &Mahindra Ltd

- CNH Industrial NV

- Kubota Corporation

- AGCO Corporation(Massey Ferguson Limited)

- Tractors and Farm Equipment Ltd

- Iseki &Co. Ltd

- Yanmar Holdings Co. Ltd

제7장 시장 기회와 향후 동향

ksm 24.03.14The Agricultural Tractors Market size is estimated at USD 70.40 billion in 2024, and is expected to reach USD 90.71 billion by 2029, growing at a CAGR of 5.20% during the forecast period (2024-2029).

Key Highlights

- Tractors are agriculture equipment that is used to perform farming operations such as plowing, tilling, and planting. They are also used for spreading fertilizers, clearing bushes, and other activities. The cost of labor has been increasing at significantly high rates due to the urbanization and migration of people to urban areas. The cost of farm labor is directly proportional to the cost of production. Mechanization can reduce labor wages. The increasing labor wages and the lack of farm labor have led to increasing rates of mechanization.

- Furthermore, the increased government support to raise farm mechanization for obtaining high yield by providing subsidies is helping to increase the number of tractors. Moreover, technological advancements are also catering to the increased mechanization and raising awareness among farmers about the benefits of farm mechanization.

- Numerous businesses have been releasing new agricultural tractors, allowing them to dominate the market with speedier product launches and advancements. Several major market players are spending on research and development in order to produce cutting-edge equipment and retain a strong market position. This factor drives the sales of tractors in the market. For instance, in 2020, Deere & Company launched a new 8 Family Tractor line-up that included 8R wheel tractors, 8RT two-track tractors, and the industry's first fixed-frame four-track tractors. These new tractors come equipped with the latest precision agriculture technology and allow customers to choose the machine configuration, options, and horsepower to best fit their operation. On the other hand, the lack of properly skilled labor for operating specialized and modern tractors may become a restraining factor for the tractor market.

Agricultural Tractors Market Trends

Increasing Farm Mechanization in Developing Markets

- Precision farming and the increasing adoption of farm technology to boost production are driving up demand for tractors. Agricultural equipment can use technology like high-precision positioning systems (such as GPS and GNSS, automated steering systems, geo-mapping, sensors, and remote sensing) and integrated electronic communication to produce superior results from machine operations. For instance, Deere & Company provides Precision AG technology for farm machinery like tractors and other items. The company provides display systems, receivers for seeding and planting, harvesting, and field preparation and tillage equipment. The launch of such items has a substantial impact on the growth of the agricultural tractor market.

- The increasing number of farm training programs promoting the use of agricultural machinery on a wide scale is also driving the tractor industry. With an engine volume of not more than 1,500 CC, these tractors occupy less space and can be used with greater flexibility. Ease of customization makes them more amenable to experimentation, and consequentially, manufacturers are willing to try new components and technologies in this segment before moving on to high-powered ones. Low-horsepower tractors work well in soft soil conditions, such as river basins. The lesser than 40 HP tractors are mainly used for horticulture. In developing countries, the demand for lower HP tractors is high due to the low disposable income of farmers and high labor costs. Farmers prefer small and customized tractors for agricultural purposes due to small farmland sizes. Moreover, lesser fuel consumption by small tractors helps empower small and marginal farmers. Governments in developing countries like India promote farm mechanization by subsidizing equipment purchases and supporting bulk buying through front-end agencies.

- Furthermore, due to the increasing demand from developing countries, the major players in the market are innovating new products. For instance, in February 2021, TAFE launched a new DYNATRACK Series, which is an advanced range of tractors that offer dynamic performance, sophisticated technology, unmatched utility, and versatility, engineered into a single powerful tractor. These factors are likely to drive the market during the forecast period.

Asia-Pacific Dominating the Market

- In the Asia-Pacific, China, Japan, and India lead in terms of the number of tractors sold. Around 60% of China's farm activities are mechanized. According to data from the National Bureau of Statistics of China, large and medium-sized tractors are gradually being replaced by small tractors. At the end of 2020, there were 4.4 million large- and medium-sized tractors in the country. The government included agricultural machinery in its 'Made in China 2025' campaign. The program is expected to help the country produce most of its farm equipment domestically, which is expected to increase the sales of tractors in China.

- Most people in India are agriculture-dependent. According to the Indian Brand Equity Foundation, 58% of the total population in India are farmers. Thus, there is a great market for tractors in India. The agriculture sector in India has witnessed a substantial decline in the use of animal and human power in the agriculture sector. Fossil fuel-operated vehicles, such as tractors and diesel engines, are being used instead, which has resulted in a shift from the traditional agriculture process to a more mechanized process.

- In order to increase the mechanization level, the Indian government is promoting 'Balanced Farm Mechanization' by providing subsidies on various equipment and supporting bulk buying through front-end agencies, which is expected to strengthen the tractors market in India. For instance, the government of India offers various schemes for agricultural equipment, such as loan-cum-subsidy for the purchase of tractors. In addition, as per NABARD norms, any farmer with eight acres of land can take a tractor loan for a period of nine years with a 12.5% rate of interest. Thus, the implementation of programs by governments in the region, along with the increasing tractor usage across, is expected to drive the market during the forecast period.

Agricultural Tractors Industry Overview

The agricultural tractor market is consolidated, with major players occupying a significant market share. Deere and Company, Kubota Corporation, CNH Industrial NV, AGCO Corporation, and CLAAS KGaA mbH are the major players in the market. New product launches, partnerships, and acquisitions are the major strategies being adopted by the leading companies in the global market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat from Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Horse Power

- 5.1.1 Lesser than 40 HP

- 5.1.2 40 HP to 99 HP

- 5.1.3 100 HP to 150 HP

- 5.1.4 151 HP to 200 HP

- 5.1.5 201 HP to 270 HP

- 5.1.6 271 HP to 350 HP

- 5.1.7 Greater than 350 HP

- 5.2 By Type

- 5.2.1 Orchard Tractors

- 5.2.2 Row-crop Tractors

- 5.2.3 Other Types

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Spain

- 5.3.2.5 Italy

- 5.3.2.6 Russia

- 5.3.2.7 Poland

- 5.3.2.8 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Africa

- 5.3.5.1 South Africa

- 5.3.5.2 Rest of Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Claas KGaA mbH

- 6.3.2 Deere & Company

- 6.3.3 Mahindra & Mahindra Ltd

- 6.3.4 CNH Industrial NV

- 6.3.5 Kubota Corporation

- 6.3.6 AGCO Corporation (Massey Ferguson Limited)

- 6.3.7 Tractors and Farm Equipment Ltd

- 6.3.8 Iseki & Co. Ltd

- 6.3.9 Yanmar Holdings Co. Ltd