|

시장보고서

상품코드

1850135

알팔파 건초 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Alfalfa Hay - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

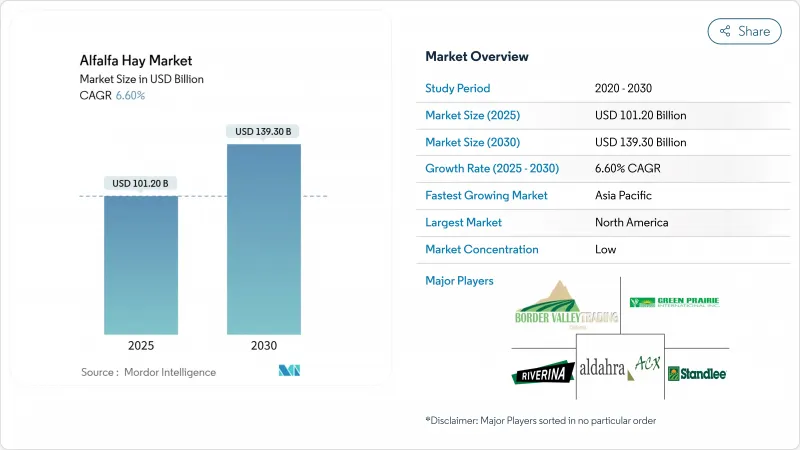

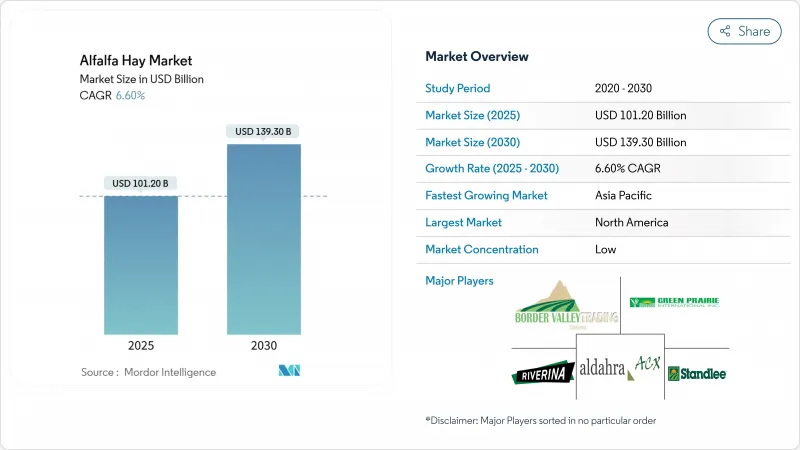

알팔파 건초 시장의 2025년 시장 규모는 1,012억 달러, 2030년에는 1,393억 달러에 이르고, CAGR 6.6%를 보일 것으로 예측됩니다.

시장의 성장은 세계의 알팔파 제작 면적의 46%가 가뭄 상태에 직면하고 있음에도 불구하고 유제품 수요 증가, 알팔파의 높은 영양가, 수효율이 높은 가공 기술에 대한 투자가 견인하고 있습니다. 북미가 최대 시장 자리를 유지하는 한편, 아시아태평양은 단백질 소비 증가와 강력한 사료 수입 프로그램을 통해 급성장을 보여줍니다. 시장은 여전히 세분화되고 있으며, 물, 노동력, 운송 비용의 상승을 관리할 수 있는 자금력 있는 기업에 기회를 가져오고 있습니다. 탄소 신용 프로그램이나 태양광 발전에 의한 탈수 프로세스 등의 지속가능성 이니셔티브의 개발은 이러한 운용 비용의 상쇄에 도움이 되어 알팔파 건초 시장의 장기적 수익성을 향상시킵니다.

세계 알팔파 건초 시장 동향과 통찰

유제품 및 동물성 단백질 수요 급증

동물성 단백질로의 세계적인 변화는 사료 조달 전략에 영향을 미칩니다. 인도, 인도네시아, 베트남에서 확대되는 낙농 사업은 일관된 단백질 밀도를 중시하는 공식 구매 계약을 맺고 있으며, 높은 리신 알팔파는 사료 배합에 필수적입니다. 미국의 생우유 가공업자는 조 단백질 알팔파를 18-22% 포함한 사료는 유량과 버터 지방의 질을 향상시킨다고 보고하고 있습니다. 말 분야에서는 퍼포먼스에 중점을 두고 있기 때문에 프리미엄 등급의 구매가 유지되고 고품질 알팔파의 안정적인 가격 프리미엄을 지원합니다. 소군의 확대와 사료전환의 필요성이 조합됨으로써, 생산성의 향상을 목표로 하는 생산자에게 있어서 알팔파 건초가 중요한 요소가 되고 있습니다.

사료 수입 프로그램 확대

명확한 구조를 가진 수입 프로그램은 가격 안정과 일관된 수요 패턴을 수립하는 데 도움이 됩니다. 일본은 외환변동에도 불구하고 2023년에 35만 6,504톤의 수입을 유지했으며, 사우디아라비아는 물사용규제 강화로 수입량을 43만 1,400톤으로 늘렸습니다. 2030년까지 국내 생산 면적을 900만 헥타르까지 확대하는 중국의 계획은 현재 수입 수요를 견인하고 있으며, 2023년 출하량이 47% 감소했음에도 불구하고 북미 수출업체에 안정적인 사업을 제공했습니다. 이러한 프로그램을 기반으로 하는 장기 공급 계약은 명확한 수요 예측을 제공하고 출하 효율을 개선하기 위해 탈수 및 압축 설비에 수출업체의 투자를 지원합니다.

물 발자국과 가뭄 정책의 압력

애리조나 주에서 2024년에 외국인이 소유한 알팔파 농장의 임대 계약이 중단됨에 따라 물집약형 농업에 대한 우려가 높아지고 있는 것이 부각되었습니다. 가뭄은 세계 알팔파 생산지의 약 50%에 영향을 미치며, 농부는 적자 관개 방법을 채택하게 됩니다. 이러한 방법은 수율을 15-20% 감소시키지만, 사료로서의 가치는 높아질 가능성이 있습니다. 정밀 관개 시스템과 가뭄에 강한 품종은 위험 관리에 도움이되지만 비용이 높기 때문에 소규모 농부에게 영향을 미칩니다. 캘리포니아의 저수지 수준 저하와 호주의 물 배분 제한으로 인해 시장 불확실성이 발생하고 알팔파 생산은 북미 전역에서 북상으로 내륙으로 이동하고 있습니다.

부문 분석

2024년 알팔파 건초 시장의 43.0%는 바위이며, 이는 확립된 취급 시스템과 축산업자에의 보급에 지지되고 있습니다. 기계화된 낙농장은 큰 사각형 베일을 선호하는 반면, 둥근 베일은 대규모 쇠고기 관리에 날씨 보호를 제공합니다. 이러한 형태의 다양성은 각 지역에서 일관된 수요를 확보하고 있습니다. 탈수 펠릿은 시장 점유율이 작지만, 자동 사료 공급기과 해상 운송 비용을 삭감하는 컨테이너 적재 밀도 증가로 인해 CAGR은 7.6%가 되고 있습니다. 펠렛은 또한 일관된 품질을 제공하고 낙농 및 말 시장에 서비스를 제공하는 배합 사료 공장의 배합 공정을 단순화합니다.

이동식 펠렛 라인에 대한 투자는 에너지 소비 증가를 보완하고 베일 가격을 초과하는 톤당 30-40달러의 프리미엄을 창출합니다. 큐브와 압축 베일은 사용자가 비용보다 편의성을 선호하는 말과 소형 반추 가축 부문에 해당합니다. 1.5시간 이내에 수분 함량을 12% 이하로 하는 현장 건조기는 수확기의 날씨 위험을 최소화합니다. 이러한 기술적 진보는 알팔파 건초 시장을 강화하고 가공 형식으로의 전환을 가속화합니다.

슈프림 등급 알팔파 건초는 2024년 시장 점유율의 28.3%를 차지했고 CAGR 6.1%로 가장 높은 성장률을 달성했는데, 이는 단백질이 풍부한 사료에 대한 수요 증가를 보여주고 있습니다. 프리미엄 등급(RFV 170-185)은 비용과 원유 생산 목표의 최적 균형을 제공함으로써 상업 낙농장 사이에서 지배적인 지위를 유지합니다. 좋은 등급은 주로 비용 효율적인 소화 단백질 함량을 중시하는 육우 경영에 공급됩니다. 공정 등급과 유틸리티 등급은 구매자가 마이코톡신과 오염물질의 제한을 엄격하게 하기 때문에 시장에서의 존재감이 떨어지고 있습니다.

품질평가에서는 검사한 중국산 샘플 모두에 마이코톡신이 검출되었기 때문에 프리미엄 바이어는 북미공급자로 이동하고 있습니다. 정확한 수확 시기, 효율적인 현장 건조 방법, 고급 저장 모니터링 시스템을 도입하고 있는 생산자는 톤당 50-60달러의 가격 프리미엄을 확보할 수 있어 품질 기준에 근거한 시장의 가치 차별화를 실증하고 있습니다.

알팔파 건초 시장 보고서는 제품 유형(베일 등), 등급(슈프림 등), 가공 기술(현장 건조 기존 등), 유통 채널(직접 농장 게이트 등), 축산 용도(유우 사료 등), 최종 용도 섹터(상업 농장 등), 지역(북미 등)별로 분류하고 있습니다. 시장 예측은 금액(달러)과 수량(메트릭톤)으로 제공됩니다.

지역 분석

북미는 2024년 매출의 36.2%를 차지했으며, 기계화된 운영, 고품질 등급 시스템, 태평양 수출 터미널에 대한 액세스를 지원합니다. 미국의 건목초 생산량은 3.3% 증가한 1억 2,250만 톤이 되었지만, 애리조나주와 캘리포니아주에서의 수 정책의 변경이 생산지에 리스크를 가져왔습니다. 위스콘신은 생산량을 75% 증가한 303만 톤으로 지역적 적응을 보였으나, 이는 수자원이 확보된 지역으로 재배 전환의 가능성을 시사하고 있습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR) 6.8%로 성장할 것으로 예측됩니다. 인도와 동남아시아의 낙농경영 근대화가 사료 수요를 견인하는 한편 중국은 수량조정에도 불구하고 88만 6,661톤으로 최대 수입국으로서의 지위를 유지하고 있습니다. 중국은 국내 생산의 확대를 목표로 하고 있지만, 소군 증가에 의해 단기적인 수입 수요는 계속됩니다. 나물디 프로젝트의 중단과 관련된 호주 건초 공급 제약은 기후 관련 취약점을 돋보이게 합니다.

유럽은 지속가능성과 추적성에 중점을 두어 안정적인 수요를 유지하고 있으며, 탄소 인증을 획득한 생산자가 시장에서 우위를 차지하고 있습니다. 남미는 특히 칠레와 아르헨티나에서 적절한 기후 조건과 개선된 항만 시설의 혜택을 받아 경쟁력 있는 수출국으로 개발되고 있습니다. 중동 시장은 물의 제약으로부터 계속 수입에 의존하고 있으며, 2024년에는 사우디아라비아가 일본을 제치고 2위의 수입국이 되었습니다. 아프리카에서는 케냐와 나이지리아에서 상업적 낙농 사업이 확대되고 알팔파 건초 시장 전망 기회를 제시하는 초기 성장 가능성을 보여줍니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 유제품과 동물성 단백질 수요 급증

- 사료 수입 프로그램의 확대

- 우수한 단백질과 섬유 프로파일

- 탄소 크레딧과 토양 건전성의 수익화

- 이동 중 건조 및 베일 압축 기술로 손실 감소

- DDGS(증류건조곡물 가용성곡물) 가격의 상승이 사료단백질의 사용량 증가를 촉진

- 시장 성장 억제요인

- 물 발자국과 가뭄 정책에 대한 압력

- 해상운임과 컨테이너운임의 변동

- 수경 사료와 대체 조 사료의 상승

- 수출 레인의 식물 검역상의 장벽

- 밸류체인/공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 제품 유형별

- 베일

- 라운드 베일

- 스퀘어 베일

- 펠렛

- 큐브

- 탈수 펠릿

- 압축 베일

- 베일

- 등급/품질별

- 최상(RFV 185 이상)

- 위(RFV 170-185)

- 양호(RFV 150-169)

- 가능(RFV 130-149)

- 유틸리티(RFV 130 미만)

- 처리 기술별

- 야외 건조 기존

- 강제 공기 이동식 건조기

- 회전 드럼 탈수

- 태양광을 이용한 탈수

- 유통 채널별

- 직접 팜 게이트

- 수출 무역

- 사료 통합자 및 밀

- 전자상거래/온라인 플랫폼

- 가축 용도별

- 젖소 사료

- 육우 사료

- 가금 사료

- 말용 사료

- 소형 반추동물용 사료

- 낙타과 동물과 기타

- 최종 용도 섹터별

- 상업농장

- 배합 사료 제조업체

- 가정/취미로 동물을 기르는 사람

- 반려동물 식품과 특수 영양

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 기타 북미

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 뉴질랜드

- 한국

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 칠레

- 기타 남미

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 이집트

- 케냐

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- AL Dahra ACX Global Inc.

- Anderson Hay & Grain Co., Inc.

- Standlee Premium Products, LLC

- Border Valley Trading

- Alfalfa Monegros

- Grupo Oses(Nafosa)

- Gruppo Carli

- Green Prairie International Inc

- Cubeit Hay Company

- Haykingdom Inc.

- SL Follen Company

- Riverina

- McCracken Hay Company

- Bailey Farms International

- Hay USA Inc

제7장 시장 기회와 장래의 전망

SHW 25.11.17The alfalfa hay market is valued at USD 101.2 billion in 2025 and is projected to reach USD 139.3 billion by 2030, growing at a CAGR of 6.6%.

The market growth is driven by increasing dairy demand, alfalfa's high nutritional value, and investments in water-efficient processing technologies, despite 46% of global alfalfa acreage facing drought conditions. North America maintains its position as the largest market, while the Asia-Pacific region shows the fastest growth due to increased protein consumption and strong forage import programs. The market remains fragmented, creating opportunities for well-funded companies capable of managing increased water, labor, and transportation costs. The development of sustainability initiatives, including carbon credit programs and solar-powered dehydration processes, helps offset these operational costs and improves long-term profitability in the alfalfa hay market.

Global Alfalfa Hay Market Trends and Insights

Dairy and Animal-Protein Demand Surge

The global shift toward animal-based proteins is influencing feed procurement strategies. Expanding dairy operations across India, Indonesia, and Vietnam are establishing formal purchasing contracts that emphasize consistent protein density, making high-lysine alfalfa essential in feed formulations. U.S. milk processors report that feed rations containing 18-22% crude-protein alfalfa improve milk yield and butter-fat quality. The equine sector maintains premium grade purchases due to its focus on performance, supporting stable price premiums for high-quality alfalfa. The combination of expanding herds and feed-conversion requirements establishes alfalfa hay as a key component for producers aiming to increase productivity.

Expansion of Forage-Import Programs

Import programs with defined structures help stabilize prices and establish consistent demand patterns. Japan maintained imports of 356,504 metric tons in 2023 despite currency fluctuations, while Saudi Arabia increased imports to 431,400 metric tons following stricter water-use regulations. China's plan to expand domestic production area to 9 million hectares by 2030 drives current import demand, providing steady business for North American exporters despite a 47% decline in 2023 shipments. The long-term supply agreements under these programs provide clear demand forecasts and support exporter investments in dehydration and compression facilities to improve shipping efficiency.

Water-Footprint and Drought Policy Pressure

The 2024 termination of foreign-owned alfalfa farm leases in Arizona highlighted growing concerns over water-intensive agriculture. Drought affects approximately 50% of global alfalfa production areas, leading farmers to adopt deficit-irrigation methods. These practices reduce yields by 15-20% but may enhance feeding value. While precision irrigation systems and drought-resistant varieties help manage risks, their high costs impact smaller farms. Declining reservoir levels in California and water allocation restrictions in Australia create market uncertainty, driving alfalfa production to shift northward and inland across North America.

Other drivers and restraints analyzed in the detailed report include:

- Superior Protein and Fiber Profile

- Carbon-Credit and Soil-Health Monetization

- Ocean-Freight and Container-Rate Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Bales account for 43.0% of the alfalfa hay market in 2024, supported by established handling systems and widespread adoption among livestock operators. Mechanized dairy farms prefer large square bales, while round bales provide weather protection for extensive beef operations. This format diversity ensures consistent demand across different regions. Dehydrated pellets, representing a smaller market share, are experiencing a 7.6% CAGR, driven by automated feeding systems and increased container-load density that reduces ocean transportation costs. Pellets also provide consistent quality, simplifying formulation processes for compound-feed mills serving dairy and equine markets.

Mobile pellet line investments generate premiums of USD 30-40 per metric ton above bale prices, compensating for increased energy consumption. Cubes and compressed bales serve equine and small-ruminant segments where users prioritize convenience over cost. Field dryers that reduce moisture content to below 12% within 1.5 hours minimize weather-related risks during harvest periods. These technological advancements strengthen the alfalfa hay market and accelerate the transition to processed formats.

Supreme grade alfalfa hay captured 28.3% of the 2024 market share and achieved the highest growth rate at 6.1% CAGR, indicating increased demand for protein-rich feed. Premium grade (RFV 170-185) maintains its dominant position among commercial dairy farms by providing an optimal balance between cost and milk production targets. Good grade serves primarily beef cattle operations that focus on cost-effective digestible protein content. Fair and Utility grades show declining market presence as buyers implement stricter mycotoxin and contaminant limits.

Quality assessments revealed mycotoxin presence in all tested Chinese samples, prompting premium buyers to shift toward North American suppliers. Producers who implement precise harvest timing, efficient field drying methods, and advanced storage monitoring systems can secure price premiums of USD 50-60 per metric ton, demonstrating the market's value differentiation based on quality standards.

The Alfalfa Hay Market Report is Segmented by Product Type (Bales and More), Grade (Supreme and More), Processing Technology (Field-Dried Conventional and More), Distribution Channel (Direct Farm Gate and More), Livestock Application (Dairy Cattle Feed and More), End-Use Sector (Commercial Farms and More), and Geography (North America and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Geography Analysis

North America accounted for 36.2% of 2024 revenue, supported by mechanized operations, quality grading systems, and access to Pacific export terminals. U.S. hay production increased by 3.3% to 122.5 million metric tons, though water policy changes in Arizona and California pose risks to production areas. Wisconsin demonstrated regional adaptation by increasing production by 75% to 3.03 million tons, suggesting a potential shift of cultivation to regions with secure water resources.

Asia-Pacific is anticipated to grow at a 6.8% CAGR through 2030. The modernization of dairy operations in India and Southeast Asia drives feed demand, while China maintains its position as the largest importer at 886,661 metric tons despite volume adjustments. While China aims to expand domestic production, near-term import requirements persist due to herd growth. Australia's hay supply constraints following the Nammuldi project suspension highlight climate-related vulnerabilities.

Europe maintains a stable demand with an emphasis on sustainability and traceability, where producers with carbon certifications gain market advantages. South America is developing as a competitive exporter, particularly in Chile and Argentina, benefiting from suitable climate conditions and improved port facilities. Middle Eastern markets continue to depend on imports due to water limitations, with Saudi Arabia becoming the second-largest importer in 2024, surpassing Japan. Africa shows initial growth potential as commercial dairy operations expand in Kenya and Nigeria, indicating future opportunities in the alfalfa hay market.

- AL Dahra ACX Global Inc.

- Anderson Hay & Grain Co., Inc.

- Standlee Premium Products, LLC

- Border Valley Trading

- Alfalfa Monegros

- Grupo Oses (Nafosa)

- Gruppo Carli

- Green Prairie International Inc

- Cubeit Hay Company

- Haykingdom Inc.

- SL Follen Company

- Riverina

- McCracken Hay Company

- Bailey Farms International

- Hay USA Inc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Dairy and Animal-Protein Demand Surge

- 4.2.2 Expansion of Forage-Import Programs

- 4.2.3 Superior Protein and Fiber Profile

- 4.2.4 Carbon-Credit and Soil-Health Monetization

- 4.2.5 On-the-Go Drying and Bale-Compression Tech Cuts Losses

- 4.2.6 Distiller's Dried Grains with Solubles (DDGS) Inflation Driving Forage Protein Use

- 4.3 Market Restraints

- 4.3.1 Water-Footprint and Drought Policy Pressure

- 4.3.2 Ocean-Freight and Container-Rate Volatility

- 4.3.3 Rise of Hydroponic Fodder and Alternative Roughage

- 4.3.4 Phytosanitary Barriers in Export Lanes

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Product Type

- 5.1.1 Bales

- 5.1.1.1 Round Bales

- 5.1.1.2 Square Bales

- 5.1.2 Pellets

- 5.1.3 Cubes

- 5.1.4 Dehydrated Pellets

- 5.1.5 Compressed Bales

- 5.1.1 Bales

- 5.2 By Grade/Quality

- 5.2.1 Supreme (RFV More Than 185)

- 5.2.2 Premium (RFV 170-185)

- 5.2.3 Good (RFV 150-169)

- 5.2.4 Fair (RFV 130-149)

- 5.2.5 Utility (RFV Less Than 130)

- 5.3 By Processing Technology

- 5.3.1 Field-Dried Conventional

- 5.3.2 Forced-Air Mobile Dryer

- 5.3.3 Rotary Drum Dehydration

- 5.3.4 Solar-Assisted Dehydration

- 5.4 By Distribution Channel

- 5.4.1 Direct Farm Gate

- 5.4.2 Export Trading Houses

- 5.4.3 Feed Integrators and Mills

- 5.4.4 E-commerce/Online Platforms

- 5.5 By Livestock Application

- 5.5.1 Dairy Cattle Feed

- 5.5.2 Beef Cattle Feed

- 5.5.3 Poultry Feed

- 5.5.4 Equine Feed

- 5.5.5 Small Ruminant Feed

- 5.5.6 Camelids and Other

- 5.6 By End-Use Sector

- 5.6.1 Commercial Farms

- 5.6.2 Compound Feed Manufacturers

- 5.6.3 Household/Hobby Animal Owners

- 5.6.4 Pet-food and Specialty Nutrition

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.1.4 Rest of North America

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Spain

- 5.7.2.5 Italy

- 5.7.2.6 Russia

- 5.7.2.7 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 Japan

- 5.7.3.3 India

- 5.7.3.4 Australia

- 5.7.3.5 New Zealand

- 5.7.3.6 South Korea

- 5.7.3.7 Rest of Asia-Pacific

- 5.7.4 South America

- 5.7.4.1 Brazil

- 5.7.4.2 Argentina

- 5.7.4.3 Chile

- 5.7.4.4 Rest of South America

- 5.7.5 Middle East

- 5.7.5.1 Saudi Arabia

- 5.7.5.2 United Arab Emirates

- 5.7.5.3 Turkey

- 5.7.5.4 Rest of Middle East

- 5.7.6 Africa

- 5.7.6.1 South Africa

- 5.7.6.2 Egypt

- 5.7.6.3 Kenya

- 5.7.6.4 Rest of Africa

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 AL Dahra ACX Global Inc.

- 6.4.2 Anderson Hay & Grain Co., Inc.

- 6.4.3 Standlee Premium Products, LLC

- 6.4.4 Border Valley Trading

- 6.4.5 Alfalfa Monegros

- 6.4.6 Grupo Oses (Nafosa)

- 6.4.7 Gruppo Carli

- 6.4.8 Green Prairie International Inc

- 6.4.9 Cubeit Hay Company

- 6.4.10 Haykingdom Inc.

- 6.4.11 SL Follen Company

- 6.4.12 Riverina

- 6.4.13 McCracken Hay Company

- 6.4.14 Bailey Farms International

- 6.4.15 Hay USA Inc