|

시장보고서

상품코드

1444266

외과용 실란트 및 접착제 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2024-2029년)Surgical Sealant and Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

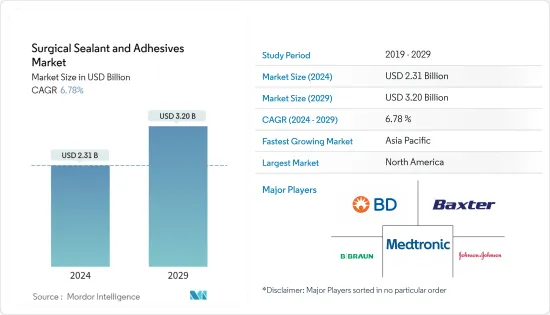

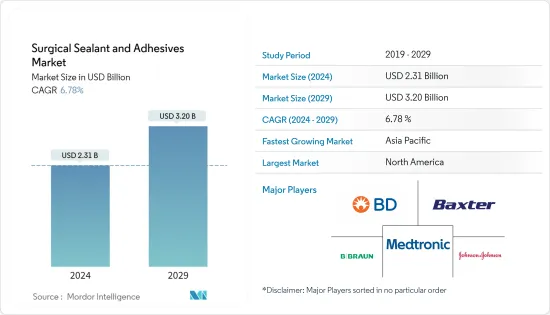

외과용 실란트 및 접착제 시장 규모는 2024년 23억 1,000만 달러로 추정되며, 2029년까지 32억 달러에 달할 것으로 예상되며, 예측 기간(2024-2029년) 동안 6.78%의 CAGR로 성장할 것으로 예상됩니다.

팬데믹은 다양한 수술 방식에 영향을 미쳤으며, COVID-19 팬데믹 상황에서도 외과 의사들이 안전하고 효과적인 치료를 제공하기 위해 각 전문 분야에 엄격한 가이드라인이 도입되어 준수되고 있습니다. 긴급하지 않은 모든 수술을 피해야 한다는 규제 당국의 엄격한 지침으로 인해 COVID-19 팬데믹 기간 동안 수술 건수가 크게 감소하여 수술 센터의 수술용 실란트 및 접착제 조달에 영향을 미쳤습니다. 수술이 지연되고 수술 건수도 감소했습니다. 2021년 10월 미국 국립보건원에 발표된 논문에 따르면, 전 세계적으로 일반 외과 입원이 42.8% 감소했다고 합니다. British Journal of Surgery의 보고서에 따르면 2020년 5월 기준 인도에서는 주당 약 4만 8,728건의 수술이 취소되었으며, 12주 동안 약 58만 5,000건의 수술이 취소된 것으로 추산됩니다. 이러한 수술 기술 저하로 인해 수술용 실란트 및 접착제에 대한 수요가 감소했습니다. 그러나 수술 치료에 대한 엄격한 봉쇄 제한이 완화되면서 연기된 수술이 재개되면서 예측 기간 동안 시장 성장에 기여했습니다.

전 세계적으로 만성 질환의 유병률과 부담이 증가함에 따라 외과적 시술이 수반되는 효과적이고 진보된 치료법에 대한 수요가 증가하고 있습니다. 이러한 요인으로 인해 전 세계적으로 수행되는 수술 건수가 증가하고 있으며, 가까운 시일 내에 더욱 증가할 것으로 예상되며, 이는 연구 예측 기간 동안 수술용 실란트 및 접착제 시장의 성장에 큰 영향을 미칠 것으로 예상됩니다.

2020년 9월에 발표된 NCBI의 연구에 따르면, 전 세계 질병 부담의 약 11%는 외과적 치료, 마취 치료 또는 두 가지 모두를 필요로 하며, 인도 국민의 외과적 요구를 충족시키기 위해서는 연간 3,646건의 수술이 필요한 것으로 추정됩니다. 전 세계적으로 인구 10만 명당 5,000건의 수술이 이루어지고 있는 것으로 추산됩니다. 따라서 전 세계적으로 수술에 대한 수요가 증가함에 따라 수술용 실란트 및 접착제의 필요성이 증가하여 시장 성장을 촉진할 것으로 예상됩니다. 마찬가지로 2021년 6월에 발표된 NCBI의 연구에 따르면, 총 92,809건의 수술이 고전적인 의미의 심장 수술로 분류되며, 그 중 29,444건이 단독 관상동맥 우회술, 35,469건이 단독 심장판막 수술로 분류되어 매년 시행되는 심장 수술 및 수술 건수가 많기 때문에 수술용 실란트-접착제 시장의 성장을 촉진할 것으로 예상됩니다.

실란트와 접착제는 모든 수술에 없어서는 안 될 부분입니다. 그들은 조직 치유를 돕기 때문에 수술에서 중요한 역할을 합니다. 만성 질환의 유병률이 증가함에 따라 대부분의 만성 질환의 말기에 수술이 필요하기 때문에 수술이 증가하고 있습니다. 2022년 7월 호주 치매에 대한 최신 정보에 따르면, 2020년에는 459,000명 이상의 호주인이 치매를 앓고 있으며, 약 160만 명이 요양원에 입원해 있는 것으로 나타났습니다. 치매 환자 수는 2058년까지 110만 명에 달할 것으로 추정되며, 향후 5년간 치매는 국내 사망 원인 중 2위를 차지할 것으로 예상됩니다.

최근 몇 년 동안 무릎 및 고관절 교체 수술 건수가 증가하면서 수술용 실란트 및 접착제에 대한 수요가 증가하여 조사 대상 시장에 긍정적인 영향을 미치고 있습니다. 수술이 증가함에 따라 그 주문도 증가할 것으로 예상되며, 조사 대상 시장도 성장할 것으로 예상됩니다. 이러한 외과 수술의 증가는 수술용 실란트 및 접착제에 대한 수요를 촉진하여 시장 성장에 기여할 것으로 예상됩니다.

그러나 수술용 실란트 및 접착제에 대한 비우호적인 상환 정책 및 대체 방법의 가용성은 수술용 실란트 및 접착제 시장의 성장을 억제할 것으로 예상됩니다.

외과용 실란트 및 접착제 시장 동향

일반외과 부문이 예측 기간 동안 시장을 독점할 것으로 예상

일반 외과 부문은 시장 성장에서 큰 비중을 차지할 것으로 예상됩니다. 일반 수술은 식도, 위, 소장, 대장, 간, 췌장, 담낭, 맹장, 담관, 그리고 종종 갑상선을 포함한 복부 부위에 초점을 맞추고 있습니다. 일반적으로 피부, 유방, 연조직, 말초혈관 수술, 탈장 등의 질환을 치료합니다. 복부 수술은 전 세계적으로 가장 흔한 수술 중 하나입니다. 자궁 적출술, 담낭 수술, 탈장 수술, 전립선 절제술 및 담낭 절제술은 전 세계적으로 대규모 수술입니다. 경제협력개발기구(OECD)에 따르면 2021년 독일과 이탈리아에서 각각 약 229.5건과 134.6건의 담낭절제술이 시행됐습니다.

2020년 독일과 이탈리아에서 각각 약 113,862건과 32,755건의 맹장절제술이 시행되었습니다. 복부 수술 건수는 전 세계적으로 증가하고 있으며, 이는 전체 시장 성장에 긍정적인 영향을 미치고 있습니다. 접착제는 일반 수술에서 중요한 역할을 합니다. 일반 수술 건수가 증가함에 따라 접착제와 실란트는 수술의 필수적인 부분이기 때문에 수요와 조달도 증가할 것으로 예상됩니다. 따라서 이는 시장 성장을 촉진할 것으로 예상됩니다.

전 세계적으로 탈장 사례의 발생률이 증가함에 따라 병원 진료 현장에서 외과용 실란트 및 접착제에 대한 수요가 증가함에 따라 조사 대상 시장이 상승 할 것으로 예상됩니다. 예를 들어, 미국 마취과 학회에 따르면 2021년 11 월에 업데이트 된 데이터에 따르면 복벽 탈장 복구는 가장 일반적인 수술 중 하나입니다. 미국에서는 매년 100만 건 이상의 탈장 수술이 시행되고 있으며, 전 세계적으로 연간 2,000만 건 이상의 수술이 시행되는 것으로 추정됩니다. 이 중 사타구니 탈장은 미국에서 연간 약 800,000 건의 탈장 수술 중 약 80 만 건을 차지합니다. 따라서 이 부문은 위의 요인으로 인해 예측 기간 동안 상당한 성장을 이룰 것으로 예상됩니다.

예측 기간 동안 북미 지역이 시장을 독점할 것으로 예상

북미 지역은 예측 기간 동안 전체 시장을 지배할 것으로 예상됩니다. 북미 지역에서는 미국이 가장 큰 시장 점유율을 차지하고 있습니다. 이는 수술 도구에 대한 규제가 개선되고 부상이나 만성 질환 문제가 발생했을 때 그러한 절차에 대한 대중의 인식이 높아졌기 때문입니다.

국가안전위원회(NSC)에 따르면 2021년 7월 개인 운동으로 인한 부상은 526,000건, 농구로 인한 부상은 500,000건, 자전거로 인한 부상은 457,000건, 축구로 인한 부상은 341,000건으로 보고되었습니다. NSC는 또한 19만 9,000건의 수영 부상으로 응급실에서 치료를 받았다고 밝혔습니다. 척추, 어깨, 머리, 무릎 부상이 전체 부상의 50% 이상을 차지했습니다. 따라서 의사의 진찰이 필요한 부상 건수가 증가하면 조사 대상 시장이 확대될 것입니다.

또한 질병통제예방센터에 따르면 2020년 미국에서 매년 약 600만 명의 여성이 자궁 적출술을 받았고, 약 460만 명의 미국 거주자가 담낭 절제술을 받았으며, 130만 명의 임산부가 미국을 찾았다고 합니다. 미국에서는 외과 수술이 많이 이루어지기 때문에 수술용 실란트 및 접착제에 대한 수요가 증가하여 이 지역에서 조사되는 시장의 성장에 기여할 것으로 예상됩니다. 따라서 시장은 앞서 언급한 요인으로 인해 예측 기간 동안 상당한 성장을 이룰 것으로 예상됩니다.

외과용 실란트 및 접착제 산업 개요

조사 대상 시장에는 현지 기업과 세계 기업이 존재하며, 적당한 경쟁이 존재합니다. 수술용 실란트 및 접착제의 대부분은 국제적인 기업들이 생산하고 있습니다. 주요 업체로는 Becton, Dickinson and Company, B. Braun Melsungen AG, Baxter International Inc, Johnson & Johnson, Medtronic PLC 등이 있습니다.

기타 혜택

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

목차

제1장 서론

- 조사 가정과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- 증가하는 외과수술

- 테크놀러지 진보

- 시장 성장 억제요인

- 외과용 실란트 및 접착제를 우대하지 않는 상환 폴리시

- 대체 방법 이용 가능성

- Porter's Five Forces 분석

- 신규 참여업체의 위협

- 구매자의 교섭력

- 공급 기업의 교섭력

- 대체 제품의 위협

- 경쟁 기업간 경쟁 강도

제5장 시장 세분화

- 제품별

- 천연/생물 유래 실란트·접착제

- 피브린 실란트

- 젤라틴 기반 접착제

- 콜라겐 기반 접착제

- 합성·반합성 접착제

- 시아노아크릴레이트

- 고분자 하이드로겔

- 폴리에틸렌 글리콜 폴리머

- 기타

- 천연/생물 유래 실란트·접착제

- 용도별

- 일반외과

- 구강외과

- 심혈관외과

- 미용외과

- 신경외과

- 정형외과

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카공화국

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 상황

- 기업 개요

- B. Braun Melsungen AG

- Baxter International Inc.

- Becton, Dickinson and Company

- Cardinal Health Inc.

- Cohera Medical Inc.

- CryoLife

- CSL Limited

- Johnson &Johnson

- Medline Industries Inc.

- Medtronic PLC

- Ocular Therapeutix

- Sanofi SA

- Stryker Corporation

- Terumo Corporation

- Vivostat A/S

제7장 시장 기회와 향후 동향

ksm 24.03.14The Surgical Sealant and Adhesives Market size is estimated at USD 2.31 billion in 2024, and is expected to reach USD 3.20 billion by 2029, growing at a CAGR of 6.78% during the forecast period (2024-2029).

The pandemic had ramifications for ways of working on various surgical procedures. There were strict guidelines for each specialty implemented and followed for surgeons to continue providing safe and effective care during the COVID-19 pandemic. The volume of surgeries significantly declined during the pandemic, owing to the stringent guidelines by regulatory authorities to avoid all non-emergent surgeries, impacting the procurement of surgical sealants and adhesives in surgical centers. The surgical procedures were delayed, and the number of surgical procedures decreased. According to the article published in the National Institute of Health in October 2021, there was a 42.8% decline in general surgery admission across the globe. According to the British Journal of Surgery report, in May 2020, around 48,728 surgical procedures per week were canceled in India, estimating about 585,000 surgical procedures for 12 weeks. This decline in surgical techniques led to decreased demand for surgical sealants and adhesives. However, the resumption of postponed surgeries after the relaxation of strict lockdown restrictions on surgical care contributed to the market's growth over the forecast period.

The increasing prevalence and burden of chronic diseases worldwide drive the demand for effective and advanced treatment involving surgical procedures. Due to this factor, the number of surgical procedures performed worldwide is increasing and further expected to rise shortly, which is expected to significantly impact the growth of the surgical sealant and adhesives market during the forecast period of the study.

As per the NCBI research study published in September 2020, about 11% of the global burden of disease requires surgical, or anesthesia care or both, and an estimated 3,646 surgeries would be required annually to meet the surgical needs of the Indian population as compared to the global estimate which is 5,000 surgeries per 100,000 people. Thus, with the rising demand for surgical procedures worldwide, the need for surgical sealants and adhesives is expected to increase, driving the market's' growth. Similarly, according to the NCBI research study published in June 2021, a total of 92,809 operations were classified as heart surgery procedures in the classical sense, of which 29,444 were isolated coronary artery bypass grafting procedures, 35,469 were isolated heart valve procedures, and the number of isolated heart transplantation increased by 2% to 340. Hence, the high number of heart procedures and surgeries performed yearly is anticipated to boost growth in the surgical sealants and adhesives market.

Sealants and adhesives are an integral part of any surgery. They play a vital role in surgeries as they help the tissues to heal. Due to the rising prevalence of chronic diseases, surgeries have increased as most chronic diseases in later stages demand surgeries. As per Dementia Australia updates from July 2022, more than 459,000 Australians were living with dementia in 2020, and about 1.6 million were involved in their center for care. It is estimated that the number of people with dementia is expected to reach 1.1 million by 2058, and dementia will become the second-leading cause of death in the country in the next five years.

The volume of knee and hip replacement surgeries increased in recent years, increasing the demand for surgical sealants and adhesives and positively impacting the market studied. With the increase in surgical procedures, their order is expected to increase, and the studied market will grow. For instance, as per the June 2021 report of the Canadian Institute of Health Information, 63,496 hip replacements and 75,073 knee replacements were performed in 2020 in Canada, and there was an average increase of about 5% in recent years in the knee and hip replacement procedures in the country. Such an increase in surgical procedures is expected to drive the demand for surgical sealants and adhesives, thereby contributing to the market's growth.

However, reimbursement policies not favoring surgical sealants and adhesives and the availability of alternative methods are expected to restrain the growth of the surgical sealant and adhesives market.

Surgical Sealants and Adhesives Market Trends

The General Surgery Segment is Expected to Dominate the Market in the Forecast Period

The general surgery segment is expected to hold a significant share of the market's growth. General surgery focuses on the abdominal area, including the esophagus, stomach, small intestine, large intestine, liver, pancreas, gall bladder, appendix, bile ducts, and often the thyroid gland. It generally deals with diseases involving the skin, breast, soft tissue, peripheral vascular surgery, and hernias. Abdominal surgery is one of the most common types of surgery worldwide. Hysterectomies, gall bladder surgeries, hernia surgeries, prostatectomies, and cholecystectomies are major surgeries worldwide. According to the Organization for Economic Cooperation and Development (OECD), in 2021, around 229.5 and 134.6 cholecystectomies were performed in Germany and Italy, respectively.

As the same source mentioned, in 2020, around 113,862 and 32,755 appendectomies were performed in Germany and Italy, respectively. The volume of abdominal surgeries is rising globally, positively impacting the overall market's growth. Adhesives play a vital role in general surgeries. Natural and synthetic polymeric materials generate threedimensional networks that physically or chemically bind to target tissues and act as hemostats, sealants, or adhesives. As the number of general surgeries increases, the demand and procurement of adhesives and sealants are expected to increase, considering they are a vital part of the surgery. Hence, this is expected to boost the market's growth.

The growing incidence of hernia cases globally is expected to boost the market studied because of the increasing demand for surgical sealants and adhesives in hospital care settings. For instance, according to the American Society of Anesthesiologists, data updated November 2021, abdominal wall hernia repair is one of the most common types of surgery. More than 1 million hernia repairs are performed each year in the United States, and worldwide these surgeries are estimated to top 20 million annually. Among these, inguinal hernias account for approximately 800,000 annual hernia repair surgeries in the United States. Thus, the segment is expected to witness significant growth over the forecast period due to the abovementioned factors.

North America is Expected to Dominate the Market in the Forecast Period

North America is expected to dominate the overall market throughout the forecast period. In the North American region, the United States holds the largest market share, and this is due to better regulations of surgical devices and growing awareness among the population to approach such procedures in case of injuries and chronic disease problems.

According to the National Safety Council (NSC), in July 2021, 526,000 injuries were reported due to personal exercise, 500,000 players were injured due to basketball, 457,000 due to bicycling, and 341,000 due to football. NSC also said that 199,000 swimming injuries were treated in the emergency room. Spine, shoulder, head, and knee injuries accounted for more than 50% of these total injuries. Thus, increasing the number of injuries requiring medical attention boosts the studied market.

Additionally, according to the Centers for Diseases Control and Prevention, in 2020, about 600,000 women in the United States had a hysterectomy every year, about 460,000 United States residents had a cholecystectomy, and 1.3 million pregnant women sought C-section in the United States. The high volume of surgical procedures in the United States is expected to drive the demand for surgical sealants and adhesives, thereby contributing to the growth of the market studied in this region. Thus, the market is expected to witness significant growth over the forecast period due to the factors mentioned earlier.

Surgical Sealants and Adhesives Industry Overview

The market studied is moderately competitive, with local and global companies. International companies manufacture the majority of surgical sealants and adhesives. Some significant players include Becton, Dickinson and Company, B. Braun Melsungen AG, Baxter International Inc, Johnson & Johnson, and Medtronic PLC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Surgical Procedure

- 4.2.2 Advancement in Technology

- 4.3 Market Restraints

- 4.3.1 Reimbursement Policies not Favoring Surgical Sealants and Adhesives

- 4.3.2 Availability of Alternative Methods

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Products

- 5.1.1 Natural or Biological Sealants and Adhesives

- 5.1.1.1 Fibrin Sealant

- 5.1.1.2 Gelatin-based Adhesives

- 5.1.1.3 Collagen-based Adhesive

- 5.1.2 Synthetic and Semi-synthetic Adhesives

- 5.1.2.1 Cyanoacrylates

- 5.1.2.2 Polymeric Hydrogels

- 5.1.2.3 Polyethylene Glycol Polymer

- 5.1.2.4 Other Synthetic and Semi-synthetic Adhesives

- 5.1.1 Natural or Biological Sealants and Adhesives

- 5.2 By Application

- 5.2.1 General Surgery

- 5.2.2 Dental Surgery

- 5.2.3 Cardiovascular Surgery

- 5.2.4 Cosmetic Surgery

- 5.2.5 Neuro-surgery

- 5.2.6 Orthopaedic Surgery

- 5.2.7 Other Applications

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 B. Braun Melsungen AG

- 6.1.2 Baxter International Inc.

- 6.1.3 Becton, Dickinson and Company

- 6.1.4 Cardinal Health Inc.

- 6.1.5 Cohera Medical Inc.

- 6.1.6 CryoLife

- 6.1.7 CSL Limited

- 6.1.8 Johnson & Johnson

- 6.1.9 Medline Industries Inc.

- 6.1.10 Medtronic PLC

- 6.1.11 Ocular Therapeutix

- 6.1.12 Sanofi SA

- 6.1.13 Stryker Corporation

- 6.1.14 Terumo Corporation

- 6.1.15 Vivostat A/S