|

시장보고서

상품코드

1444360

수의 진단 - 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2024-2029)Veterinary Diagnostics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

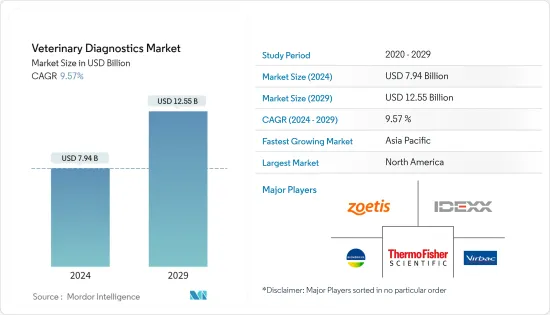

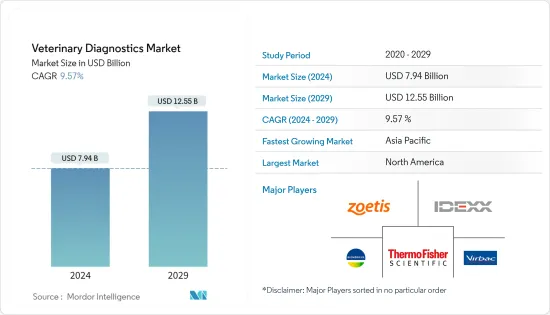

수의 진단 시장 규모는 2024년 79억 4,000만 달러로 추정됩니다. 예측 기간(2024-2029년) 동안 9.57%의 연평균 복합 성장률(CAGR)로 성장하여 2029년까지 125억 5,000만 달러에 달할 것으로 예측됩니다.

코로나19의 발생은 정부 규제로 인해 수의 진단 서비스를 포함한 다양한 의료 서비스가 중단되면서 수의 진단 시장에 큰 영향을 미쳤습니다. 예를 들어, JAAWS가 2022년 2월에 발표한 기사에 따르면, 코로나19로 인해 2020년 캐나다와 미국 동물병원의 70%가 문을 닫았다고 합니다. 따라서 처음에는 코로나19 감염을 최소화하기 위해 수의사 진단 서비스를 일시적으로 중단하여 조사 대상 시장의 성장을 저해했습니다. 그러나 현재 시나리오에서 수의사 진단 서비스 재개로 이어지는 신종 코로나19 사례의 감소와 봉쇄 이후 보고된 반려동물 입양이 크게 증가함에 따라 예측 기간 동안 조사 대상 시장의 안정적인 성장으로 이어질 것으로 예상됩니다.

조사 대상 시장의 성장을 가속하는 요인은 반려동물 입양 및 동물 건강 관리 비용 증가, 인수공통전염병 발생률 증가, 개발도상국의 수의사 수와 가처분 소득 증가 등입니다. 예를 들어, 2022년 5월 캐나다의 2021년 농업 인구조사 보고서에 따르면 캐나다 농장의 돼지 및 돼지 사육두수가 전년(2020년) 대비 3.4% 증가했다고 보고했습니다. 2021년 캐나다에는 1,460만 마리의 돼지와 돼지가 있었습니다. 마찬가지로 APPA가 실시한 2021-2022년 전국 반려동물 소유자 조사에 따르면, 미국에서 반려견의 정기적인 방문에 소요되는 연간 지출은 242달러로 고양이의 178달러와 비교했을 때 2배 이상 높은 것으로 보고됐습니다. 결과적으로 반려동물과 가축의 입양 증가와 동물 건강 관리 비용 증가가 조사 대상 시장의 성장을 주도하고 있습니다.

최근 몇 년동안 동물의 인수공통전염병 발생 건수가 크게 증가하고 있습니다. 환자 수가 증가함에 따라 질병을 치료할 필요성도 크게 증가하고 있으며, 이는 수의 진단 시장의 성장을 가속할 것으로 예상됩니다. 예를 들어, 2022년 7월 세계보건기구(WHO)가 발표한 논문에 따르면, 아프리카는 동물에서 유래한 뒤 종을 바꿔 인간에게 감염되는 원숭이 수두 바이러스와 같은 인수공통전염병 병원체에 의한 전염병의 위험성이 증가하고 있다고 보고했습니다. 지난 10년간 이 지역의 인수공통전염병 발생 건수는 63% 증가했습니다. 이 소식통은 또한 2022년 1월 1일부터 2022년 7월 8일까지 총 2,087건의 원숭이 수두가 발생했으며, 이 중 203건만 확진 판정을 받았다고 보고했습니다. 따라서 동물의 인수공통전염병이 증가함에 따라 수의 진단약에 대한 수요가 증가하고 있으며, 이는 연구 대상 시장의 성장을 가속하고 있습니다.

또한, 시장 기업의 확장도 시장 성장을 가속하고 있습니다. 예를 들어, 2021년 11월 아비아젠 인도는 타밀나두 주에 위치한 수의 진단 실험실를 확장했습니다. 이 연구소는 아비아젠의 번식용 가축의 건강 상태를 정기적으로 모니터링하고 있습니다. 따라서 이러한 확장은 수의 진단에 사용할 수 있는 시설을 증가시켜 시장 성장에 기여할 것입니다.

따라서 반려동물 입양과 동물 건강관리 비용 증가, 인수공통전염병 발생률 증가가 시장 성장을 견인하고 있습니다. 그러나 반려동물 관리 및 영상 장비의 높은 비용과 수의사 부족은 수의 진단 시장의 성장을 저해하고 있습니다.

수의 진단 시장 동향

분자진단 부문은 예측 기간 동안 상당한 성장을 이룰 것으로 예상됩니다.

분자진단 부문은 가축 및 반려동물 소유주들이 빠른 검사 결과와 비용 효율성에 대한 요구가 증가함에 따라 예측 기간 동안 상당한 성장을 보일 것으로 예상됩니다. 이 분야의 확장은 고양이 백혈병, 개 파보바이러스, 필라리아, 전염성 복막염과 같은 유행성 동물 질병을 식별하기 위해 고안된 검사 수가 증가함에 따라 촉진될 것으로 예상됩니다. 또한 반려동물과 가축을 키우는 인구 증가와 동물 건강에 대한 관심 증가, 반려동물과 가축의 질병 확산, 집에서 자주 검사할 수 있는 저렴한 가격의 면역 측정 검사가 더 쉽게 이용할 수 있게 된 것도 한몫을 하고 있습니다.

가축의 조류 인플루엔자 사례가 증가함에 따라 분자진단 테스트에 대한 수요가 증가하여이 분야의 성장을 가속하고 있습니다. 예를 들어, 2022년 4월 캐나다 정부가 발표한 보고서에 따르면 2022년 3월에 다양한 조류, 터키, 오리/닭, 거위, 공작새가 조류독감에 감염되었습니다. 이 질병은 모든 사람에게 빠르게 퍼졌습니다. 따라서 가축 종을 탐지하기위한 분자진단 테스트가 증가하여이 부문의 성장에 기여할 것입니다.

또한 2021년 7월, 유럽펫푸드연맹은 2020년 3월부터 2021년 3월까지 영국에서 약 320만 마리의 반려동물을 입양한 가정이 있을 것으로 추산된다고 발표했습니다. 이처럼 유럽 가정의 반려동물 입양 건수가 증가함에 따라 반려동물 보호자들 사이에서 반려동물의 건강에 대한 인식이 높아지면서 수의학적 진단에 대한 수요가 증가하고 있으며, 이는 이 분야의 성장에 기여하고 있습니다.

시장 기업의 기기 및 기타 제품 출시는 시장 성장을 가속하고 있습니다. 예를 들어, 2021년 8월 HORIBA UK Limited는 POCKIT Central을 위한 몇 가지 새로운 병원체 PCR 테스트를 출시했습니다. 이 제품은 모든 수의학 실험실에서 빠르고 정확한 PCR 검사를 가능하게 하는 사내 수의학 PCR 분석기입니다. 이러한 출시는 시장 부문의 성장을 가속하고 있습니다.

또한 2022년 1월, Ringbio는 Flexy Pet Rapid Test를 판매하기 위해 petrapidtest.com이라는 전문 웹사이트를 개설했습니다. 이 키트는 반려동물의 질병을 검출하기 위해 측면 유동 면역 분석, ELISA 및 실시간 PCR을 기반으로 하여 반려동물 보호자와 동물병원에 도움이 될 수 있습니다. 이 중 실시간 PCR은 소규모 동물병원을 위해 특별히 설계된 제품으로 바이러스, 마이코플라즈마, 기생충 감염을 확인할 수 있습니다. 기업이 취한 이러한 마케팅 전략은 이 부문의 성장을 가속할 것입니다.

따라서 가축의 조류 인플루엔자 사례 증가, 반려동물 입양 증가, 신제품 출시로 인해 이 부문은 위의 요인으로 인해 예측 기간 동안 상당한 성장을 보일 것으로 예상됩니다.

북미는 예측 기간 동안 큰 폭의 성장을 이룰 것으로 예상됩니다.

북미는 미국, 캐나다, 멕시코의 3개국으로 구성되어 있습니다. 조사 대상 시장은 반려동물 및 가축 입양 증가, 더 나은 진단 시설의 가용성, 주요 시장 기업의 존재로 인한 기술 개발로 인해 이 지역에서 상당한 성장이 예상됩니다.

가축 입양 증가 추세도 이 지역 시장 성장을 가속하고 있습니다. 예를 들어, 2022년 3월 멕시코 농업부는 2021년 멕시코의 소 수입량이 크게 증가했다고 보고했습니다. 이 소식통은 또한 2021년 멕시코의 축산 부문 성장률이 5.4%를 나타낼 것이라고 보고했습니다. 따라서 멕시코의 가축 수가 증가함에 따라 수의학 질환의 위험이 증가하여 국내 수의 진단 의약품에 대한 수요가 증가하여 연구 대상 동물의 성장을 가속하고 있습니다. 시장.

또한, 수의사 수 증가도 조사 대상 시장의 성장을 가속하고 있습니다. 예를 들어, 2022년 9월 미국 노동 통계국은 수의사 고용이 2021년부터 2031년까지 19% 증가할 것으로 예상되며, 이는 전체 직업 평균보다 훨씬 빠른 속도라고 보고했습니다. 또한 이 소식통은 10년 동안 매년 평균 약 4,800명의 수의사 일자리가 생길 것으로 예상했습니다. 따라서 수의사 수 증가는 수의 진단 서비스 증가로 이어져 조사 대상 시장의 성장을 가속할 것입니다.

예방 진단 도구의 개발도 수의사 진료 및 예방 치료 증가에 기여하고 있습니다. 예를 들어, 2021년 4월 Mars Veterinary Health의 자회사인 Antech Diagnostics는 73만 건의 수의사 진료 후향적 조사에서 얻은 모든 고양이가 레날텍 양성 또는 음성 판정을 받은 후 개선된 예방적 치료를 받았다는 새로운 데이터를 발표했습니다. 발표했습니다. RenalTech는 고양이의 CKD가 발생하기 2년 전에 이를 예측합니다. 데이터에 따르면, 예측 진단 도구로 인해 수의사 방문이 31%나 증가한 것으로 나타났습니다. 이러한 연구와 예측 진단 도구의 개발은 이 나라 시장 성장을 가속하고 있습니다.

시장 관계자들의 진단 테스트 출시 증가도 시장 성장을 가속하고 있습니다. 예를 들어, 2021년 7월 Vidium Animal Health는 SpotLight Repair를 출시했습니다. 개 림프종에 대한 고정밀하고 빠른 분자진단 검사입니다. Vidio는 City of Hope의 계열사인 Translational Genomics Research(TGen) 및 Ethos Discovery와 공동으로 개발했습니다.

따라서 반려동물과 가축의 입양 증가, 더 나은 진단 시설의 가용성, 기술 개발로 인해 북미는 예측 기간 동안 상당한 성장을 보일 것으로 예상됩니다.

수의 진단 산업 개요

수의 진단 시장은 경쟁이 치열하고 세분화되어 있습니다. 주요 시장 기업들은 동물 관리, 특히 기상 조건의 변화로 인한 질병으로부터 동물을 보호하기 위한 진단 기술 향상에 초점을 맞추었습니다. 수의 진단 서비스를 제공하는 기업으로는 BioMerieux SA, Heska Corporation, Indexx Laboratories, IDVet, Randox Laboratories Ltd. Corporation, Zoetis Inc., BIOCHEK BV, INDICAL Bioscience GmbH, Neogen Corporation 등이 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- 시장 성장 억제요인

- Porter의 Five Forces 분석

- 신규 진출업체의 위협

- 바이어의 교섭력

- 공급 기업의 교섭력

- 대체 제품의 위협

- 경쟁 기업간 경쟁도

제5장 시장 세분화

- 제품 유형별

- 기기

- 키트 및 시약

- 소프트웨어 및 서비스

- 기술별

- 면역진단

- 임상생화학

- 분자진단

- 혈액학

- 기타 기술

- 동물 유형별

- 반려동물

- 개

- 고양이

- 기타 반려동물

- 가축

- 소

- 돼지

- 가금류

- 기타 가축

- 반려동물

- 지역

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카공화국

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 기업 개요

- BioMerieux SA

- Heska Corporation

- Idexx Laboratories

- IDVet

- Randox Laboratories Ltd.

- Thermo Fisher Scientific Inc.

- Virbac Corporation

- Zoetis Inc.

- BIOCHEK BV

- INDICAL Bioscience GmbH

- Neogen Corporation

- Bio-Rad Inc.

제7장 시장 기회와 향후 동향

LSH 24.03.19The Veterinary Diagnostics Market size is estimated at USD 7.94 billion in 2024, and is expected to reach USD 12.55 billion by 2029, growing at a CAGR of 9.57% during the forecast period (2024-2029).

The outbreak of COVID-19 has had a substantial impact on the veterinary diagnostics market because government regulations led to the suspension of various healthcare services, including veterinary diagnostics services. For instance, an article published by the JAAWS, in February 2022 reported that COVID-19 led to the shutting down of 70% of veterinary clinics in Canada and the US in 2020. Thus, initially, the studied market's growth was hampered due to the suspension of veterinary diagnostic services to minimize the COVID-19 infection. However, in the current scenario, it is anticipated that the decreasing COVID-19 cases leading to the resumption of veterinary diagnostic services and a significant increase in pet adoption reported after the lockdown will lead to the stable growth of the studied market over the forecast period.

The factors driving the growth of the studied market are the increased pet adoption and animal healthcare expenditure, rising incidence of zoonotic diseases, and the growing number of veterinary practitioners and disposable income in developing regions. For instance, in May 2022, Canada's 2021 Census of Agriculture report stated that farms in Canada reported a 3.4% increase in the number of hogs and pigs from the previous year (2020). In 2021, there were 14.6 million hogs and pigs in Canada. Similarly, the National Pet Owners Survey 2021-2022, conducted by the APPA, reported that the annual expenditure on routine visits for dogs accounts for USD 242 compared to USD 178 for cats in the United States. As a result, the increased pet and livestock adoption coupled with increasing animal healthcare expenditure are driving the growth of the studied market.

The number of zoonotic disease cases in animals has risen significantly in recent years. With the rise in the number of cases, the necessity to treat the disorders has also risen extensively, which is expected to propel the growth of the veterinary diagnostic market. For instance, an article published by WHO in July 2022, reported that Africa is facing a growing risk of outbreaks caused by zoonotic pathogens, such as the monkeypox virus which originated in animals and then switched species and infected humans. There has been a 63% increase in the number of zoonotic outbreaks in the region in the decade. The same source also reported that from 1 January 2022 to 8 July 2022 there have been 2,087 cumulative monkeypox cases, of which only 203 were confirmed. Thus, the increase in zoonotic diseases in animals is increasing the demand for veterinary diagnostics, thereby driving the growth of the studied market.

Furthermore, the expansion by the market players is also boosting the market's growth. For instance, in November 2021, Aviagen India expanded its veterinary diagnostic laboratory in Tamil Nadu. The laboratory monitors the health of the Aviagen breeding stock regularly. Thus, such expansion increases the facility available for veterinary diagnosis and contributes to the market's growth.

Thus, due to the increased pet adoption and animal healthcare expenditure, rising incidence of zoonotic diseases, are driving the growth of the market. However, the high cost of pet care and imaging devices and the lack of veterinarians are impeding the veterinary diagnostics market growth.

Veterinary Diagnostics Market Trends

The Molecular Diagnostics Segment is Estimated to Witness Significant Growth Over the Forecast Period.

The molecular diagnostics segment is expected to witness significant growth over the forecast period due to livestock and pet owners growing preference for quick test results and their cost-effectiveness. The segmental expansion is anticipated to be driven by the rising number of tests designed to identify prevalent animal diseases such as feline leukemia, canine parvovirus, heartworm, and infectious peritonitis. Furthermore, the increasing number of pet and livestock owners and the growing concern for their animal health, the rise in the prevalence of companion animal and livestock animal diseases, and the accessibility of affordable immunoassay tests that allow for frequent testing at home are also contributing to the growth of this segment.

The increasing cases of avian influenza in livestock animals are increasing the demand for molecular diagnostic tests, thereby driving the growth of this segment. For instance, in April 2022, as per the report published by the Government of Canada in April 2022, various avian species, turkeys, ducks/chickens, geese, and peafowls were infected by avian influenza in March 2022. The disease spreads rapidly among all livestock species, thus increasing molecular diagnostic tests for its detection, thereby contributing to the segment's growth.

Similarly, in July 2021, European Pet Food Federation reported that between March 2020 and March 2021, it was estimated families adopted around 3.2 million pets in Britain. Thus, the high number of pet adoption in European families is increasing awareness among pet owners about the health of pet animals, which is increasing the demand for veterinary diagnostics, thereby contributing to the growth of this segment.

The market players' launch of instruments and other products is augmenting the market's growth. For instance, in August 2021, HORIBA UK Limited launched several new pathogen PCR tests for its POCKIT Central. It is an in-house veterinary PCR analyzer with the potential for fast, accurate PCR testing in every veterinary lab. Such launches are also propelling the growth of the market segment.

Furthermore, in January 2022, Ringbio launched a professional website names petrapidtest.com to market Flexy Pet Rapid Test. These kits are based on lateral flow immunoassay, ELISA, and real-time PCR to detect companion animal diseases, which can be helpful for pet owners and vet clinics. Among these products, real-time PCR is specially designed for small vet clinics and can confirm infection of viruses, mycoplasma, and parasite. Such marketing initiatives taken by the players also augment the segment's growth.

Thus, with the increasing cases of avian influenza in livestock animals, increased pet adoption, and new product launches, the segment is expected to show significant growth over the forecast period due to the abovementioned factors.

North America is Expected to Witness a Significant Growth Over the Forecast Period.

The North American region comprises of following three countries United States, Canada, and Mexico. The studied market is expected to witness significant growth in the region due to the increasing adoption of pet and livestock animals, availability of better diagnostics facilities, and technological developments due to the presence of key market players.

The increasing trend for livestock adoption also propels the market's growth in the region. For instance, in March 2022, USDA reported that in the year 2021, Mexico's cattle imports considerably increased. The source also reported that 5.4% growth in Mexico's livestock farming sector in 2021. Thus, the increasing livestock number in Mexico is increasing the risk of veterinary diseases which is increasing the demand for veterinary diagnostics in the country, thereby driving the growth of the studied market.

Moreover, the growing number of veterinary practitioners is also driving the growth of the studied market. For instance, in September 2022, the US Bureau of Labor Statistics reported that employment of veterinarians is projected to grow 19% from 2021 to 2031, much faster than the average for all occupations. Also, the same source reported that about 4,800 openings for veterinarians are projected each year, on average, over the decade. Thus, the increasing number of veterinary practitioners is leading to increasing veterinary diagnostic services, thereby driving the growth of the studied market.

The development of preventive diagnostic tools also contributes to the increasing number of veterinary visits and preventive care. For instance, in April 2021, Antech Diagnostics, a part of Mars Veterinary Health, released new data that shows that all cats from a retrospective review of 730,000 veterinary visits received improved preventive care following a positive or negative RenalTech. RenalTech predicts CKD in cats two years before it occurs. The data shows that the predictive diagnostic tool increased veterinary visits by as much as 31%. Such studies and the development of predictive diagnostics tools are also driving the market growth in the country.

The increasing number of launches of diagnostic tests by the market players is also propelling the market's growth. For instance, in July 2021, Vidium Animal Health launched SpotLight repair. It is a highly accurate and rapid molecular diagnostic test for canine lymphoma. Vidio developed it in collaboration with the Translational Genomics Research Institute (TGen), an affiliate of the City of Hope, and Ethos Discovery.

Thus, due to the increasing adoption of pet and livestock animals, availability of better diagnostics facilities, and technological developments, North America is expected to project significant growth over the forecast period.

Veterinary Diagnostics Industry Overview

The veterinary diagnostics market is competitive and fragmented. The major market players are focusing on improved diagnostics techniques for animal care, especially protecting animals from diseases due to changing weather conditions. Some companies that provide veterinary diagnostic services are BioMerieux SA, Heska Corporation, Idexx Laboratories, IDVet, Randox Laboratories Ltd., Thermo Fisher Scientific Inc., Virbac Corporation, Zoetis Inc., BIOCHEK BV, INDICAL Bioscience GmbH, Neogen Corporation, and Bio-Rad Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Adoption of Pet Ownership and Animal Health Expenditure

- 4.2.2 Increased Burden of Animal Zonotic Diseases

- 4.2.3 Growing Pet Insurance and Animal Health Investments by Pharmaceutical Companies

- 4.3 Market Restraints

- 4.3.1 Lack of Veterinarians

- 4.3.2 High Cost of Pet Care and Imaging Devices

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Product Type

- 5.1.1 Instruments

- 5.1.2 Kits and Reagents

- 5.1.3 Software and Services

- 5.2 By Technology

- 5.2.1 Immunodiagnostics

- 5.2.2 Clinical Biochemistry

- 5.2.3 Molecular Diagnostics

- 5.2.4 Hematology

- 5.2.5 Other Technologies

- 5.3 By Animal Type

- 5.3.1 Companion Animals

- 5.3.1.1 Dogs

- 5.3.1.2 Cats

- 5.3.1.3 Other Companion Animals

- 5.3.2 Livestock Animals

- 5.3.2.1 Cattle

- 5.3.2.2 Swine

- 5.3.2.3 Poultry

- 5.3.2.4 Other Livestock Animals

- 5.3.1 Companion Animals

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 BioMerieux SA

- 6.1.2 Heska Corporation

- 6.1.3 Idexx Laboratories

- 6.1.4 IDVet

- 6.1.5 Randox Laboratories Ltd.

- 6.1.6 Thermo Fisher Scientific Inc.

- 6.1.7 Virbac Corporation

- 6.1.8 Zoetis Inc.

- 6.1.9 BIOCHEK BV

- 6.1.10 INDICAL Bioscience GmbH

- 6.1.11 Neogen Corporation

- 6.1.12 Bio-Rad Inc.