|

시장보고서

상품코드

1910455

페인트 및 코팅용 수지 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Resins In Paints And Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

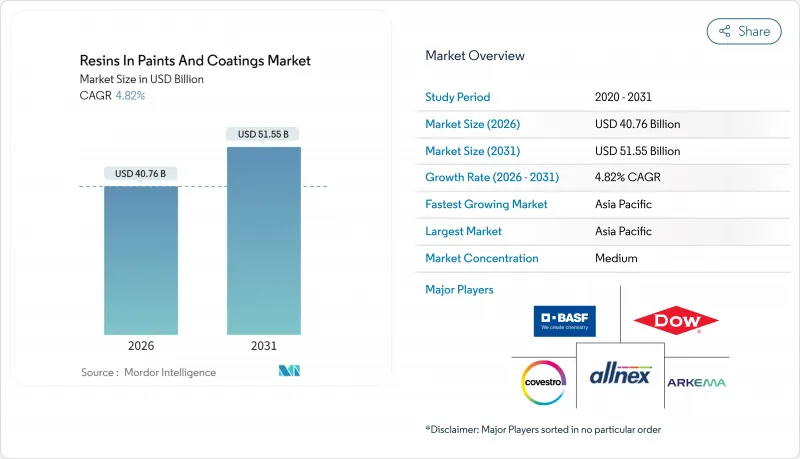

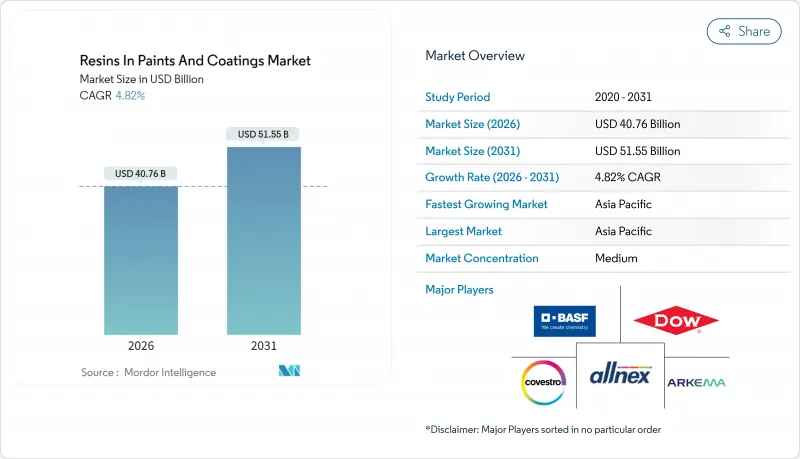

페인트 및 코팅용 수지 시장 규모는 2026년에는 407억 6,000만 달러로 추정되고 있으며, 2025년 388억 9,000만 달러에서 성장이 예상됩니다.

2031년까지의 예측으로는 515억 5,000만 달러에 달하고, 2026년부터 2031년에 걸쳐 CAGR 4.82%를 나타낼 전망입니다.

표면상의 성장률은 겸손하게 보이지만, 정책 주도에 의한 용매계 화학물질로부터의 이행이, 조제업자에게 수성 아크릴, 폴리우레탄 분산체, 기타 바이오 순환 기술을 중심으로 한 제품 포트폴리오의 재구축을 강요하고 있습니다. 3대륙 정부가 2024년부터 2025년에 걸쳐 휘발성 유기화합물(VOC)의 상한치를 강화함으로써 마이그레이션 일정이 가속화되었습니다. 아시아태평양은 인프라 투자로 계속 가치 창조를 주도하고 있습니다. 그러나 북미와 유럽에서는 프리미엄에서 낮은 VOC 수지를 선호하는 다년간 개조 프로그램이 진행 중입니다. 기존 기업이 재생 가능 원료의 통합, 지역 분산 플랜트의 건설, 제품 개발 사이클을 단축하는 디지털 조합 플랫폼의 도입을 진행하는 중, 경쟁의 격화가 진행되고 있습니다.

세계의 페인트 및 코팅용 수지 시장 동향과 인사이트

아시아태평양의 건설 붐

공공 부문의 인프라 계획은 건축용 및 보호용 페인트에 여전히 가장 큰 수요원입니다. 인도의 국가 인프라 계획만으로도 2025년까지 누계 1조 4,000억 달러의 자본 지출을 목표로 했으며, 에폭시 수지나 폴리우레탄 수지를 다용하는 교량·항만·철도용 도료 수요를 여러 해에 걸쳐 견인합니다. 싱가포르 건설청은 2025년 이후의 신규 공공 주택 프로젝트 모두에 그린마크 플래티넘 성능을 의무화해, 공장 도장 패널에의 수성 아크릴 또는 폴리우레탄 화학제품의 채용을 사실상 요구하고 있습니다. 필리핀은 2024년 'Build Better More' 프로그램에 1조 1,000억 페소(약 200억 달러)를 배분하여 공업용 페인트를 많이 사용하는 공항, 도로, 에너지 자산을 포함하고 있습니다. 지역 전체에서는 국유 개발 사업자가 낮은 VOC 사양을 입찰 서류에 통합하는 움직임이 가속화되고 분산 기술의 도입이 진행되고 있습니다. 이에 따라 수지 제조업체는 인도네시아와 베트남에 분산반응장치의 설치를 발표하고, 리드타임 단축과 수송시 배출량 감축을 목표로 하고 있습니다. 이러한 움직임은 세계 기업의 생산량의 헤지가 되는 한편, 지역의 조제 제조업체가 공급을 현지화하는 것을 가능하게 합니다.

VOC 배출 규제 강화

고용제 수지의 적합기간은 급속히 축소되고 있습니다. 2025년 1월, 미국 환경보호청(EPA)은 에어로졸 페인트의 VOC 함량을 중량비 25%로 제한(종래 카테고리 상한 45%에서 인하)하여 바인더 선정의 즉각 전환을 강요했습니다. 조지아는 이에 이어 2025년 7월 시행 규칙 391-3-1-.02(7)(c)에서 건축용 플랫 페인트의 VOC 함량을 50g/리터로 제한했습니다. 유럽에서는 더욱 기준이 인상되어 유럽위원회가 2024년 10월에 공표한 에코 라벨 기준안에서는 내장용 도료에 대해 30그램/리터의 상한을 부과했습니다. 이 기준을 달성할 수 있는 것은 고고형분 아크릴계 또는 하이브리드계 시스템뿐입니다. 중국은 GB 18582-2024 표준에서 EU 임계값을 반영하여 세계 최대 건설 시장이 더 이상 VOC 규제가 느슨한 대피 장소가 될 수 없음을 보여주었습니다. 특히 아크릴계 및 폴리우레탄계 분산액 등 즉시 스케일업 가능한 수성 제품군을 보유한 수지 공급업체는 배합 제조업체가 급격한 규제 강화에 대응하는 가운데 점유율을 확대하고 있습니다.

원료 가격의 변동성

프로파일렌, 벤젠, 에틸렌의 가격 변동은 여전히 큰 역풍입니다. ICIS Chemical Business에 따르면 아시아 계약 프로파일렌 가격은 3건의 예기치 않은 크래커 정지로 2024년 2분기에 전기 대비 25% 상승했습니다. 유럽에서도 비슷한 감소에 의해 에틸렌 유도체의 마진이 마이너스로 바뀌고, 중소 에폭시 제조업체는 플랜트의 가동 정지를 강요했습니다. 업스트림 석유화학 부문을 통합하지 않은 수지 제조업체는 가격에 민감한 건축용 수지 분야에서 60-90일간의 가격 전가 지연에 직면하고 있습니다. 부분적인 대책도 나타나고 있으며, 코베스트로사는 폐식용유 유래의 바이오 순환형 폴리올을 공표. 2024년까지 화석 원료와의 가격 차이를 해소하고 나프타 가격 변동에 대한 의존도를 줄였습니다. 그러나, 바이오 원료의 채용이 확대될 때까지, 상품 가격과의 연동성이 마진을 계속 제한할 것입니다.

부문 분석

아크릴 수지는 낮은 VOC 수성 시스템에의 적합성이 뛰어나기 때문에 2025년 페인트 및 코팅 시장에서 수지 점유율의 30.02%를 차지했습니다. 5.28%의 연평균 복합 성장률(CAGR)과 함께 규제 당국이 배출 상한을 강화하는 가운데 가치 이행의 기반을 구축하고 있습니다. 에폭시 수지는 선박이나 풍력 터빈 산업 등 고응력 용도에 사용되고 헥시온사는 2024년 보고서에서 터빈 OEM으로부터의 견조한 수주를 보고했습니다. 폴리우레탄 분산액은 EV 배터리의 이용 사례로 수요를 확대. 분말 도료의 주력인 폴리에스테르는 저온 경화형 폴리에스테르·에폭시 하이브리드의 채용 확대에 의해 이익률의 압축에 직면하고 있습니다. 알키드 수지는 용제계 건축용 도료의 기간으로서 오랫동안 사용되어 왔지만, 건조 시간이 길고 VOC(휘발성 유기 화합물)가 높기 때문에 주류의 벽용 도료 라인에서는 쇠퇴하고 있습니다. 한편, 고급 목질 마감재에서는 틈새 시장을 유지하고 있습니다. 스칸디나비아 국가에서는 ISO 14040에 근거한 라이프사이클 평가가 공공 조달로 의무화되어 환경 선언이 인증된 수지로의 점유율 전환이 진행되고 있습니다.

아크릴 수지의 뛰어난 분산성은 모듈식 주택용 공장 도장 패널 라인의 기반이 되고 있습니다. 조립식 현장에서는 엄격한 택트 타임에 대응하기 때문에 속건성으로 단공정 도장이 가능한 도료가 선호되어 수성 아크릴이 자연스러운 선택지가 되고 있습니다. 에폭시 수지 벤더는 소성 곡선을 단축하는 나노 개질 시스템으로 대응하고, 폴리우레탄 벤더는 강제 공기식 오븐을 필요로 하지 않는 습기 경화형을 추진하고 있습니다. 페인트 및 코팅 시장에 있어서 수지 전반으로, 공급업체의 혁신은 CO2 삭감 원료에 수렴하고 있습니다. BASF가 2026년까지 재생 가능 프로파일렌을 아크릴 밸류 체인에 통합한다고 표명한 것이 그 증거입니다. 이 원료 전략은 바이오 함량 20% 이상의 재료에 가격 프리미엄을 부여하는 유럽 공공 조달 규칙과 일치합니다.

지역별 분석

2025년 시점에서 아시아태평양은 페인트 및 코팅용 수지 시장의 44.12%를 차지하며 5.33%의 연평균 복합 성장률(CAGR)로 가장 빠르게 성장했습니다. 이는 중국의 건설업 회복과 인도의 메가 프로젝트 계획에 견인됩니다. 중국에서는 2024년 지방자치단체가 대출규제를 완화함으로써 주택착공건수가 회복되어 대출실행액 증가로 이어졌습니다. 인도의 국가 인프라 계획은 교량·철도용 보호 도료 수지의 소비를 견인해, 인도네시아의 IKN 누산타라 수도권 개발이나 필리핀의 “Build Better More” 프로그램이 지역 기준선 수요를 밀어 올리고 있습니다. 일본의 내진 개수 보조금 제도나 한국의 그린 뉴딜 정책은 공공 조달에 있어서 낮은 VOC 도료를 의무화해, 현지 가공업자 경유로의 아크릴·폴리우레탄 분산액의 사용을 촉진하고 있습니다.

북미의 성장은 2024년에 4,850억 달러에 달한 주택 개수 지출에 의해 지원되었으며, 에너지 절약 외장과 사이딩 교환이 지출의 주축이 되었습니다. 미국 환경보호청(EPA)의 2025년 VOC 규제는 수성 페인트 채용을 가속화시키고 샤윈 윌리엄스는 저취기 에멀젼 페인트의 프리미엄 가격 설정이 이익률 향상에 기여한다고 표명하고 있습니다. 캐나다의 탄소 가격은 2024년 1톤당 80캐나다 달러에 이르렀으며, 냉각 부하 감소를 위한 높은 알베도 지붕 페인트를 포함한 리노베이션 패키지를 건물 소유자에게 촉구하고 있습니다.

유럽에서는 '개수의 물결'과 '산업 배출 지령'을 견인역으로 저용제·분말 화학을 우선하는 중간 정도의 단일 자리 성장을 이루고 있습니다. 북유럽 지자체에서는 입찰 시에 제품 고유의 환경 제품 선언을 요구하는 움직임이 넓어져, 완전히 감사가 끝난 분산형 제품 라인을 가지는 공급자가 우위성을 얻고 있습니다. 남미, 중동 및 아프리카는 코팅 수지 시장 규모에서 비교적 작은 점유율을 차지하지만, 브라질, 사우디아라비아, 아랍에미리트(UAE)에서 석유, 가스, 광업, 경기장 건설과 관련된 국소 성장이 예상됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 지원(3개월간)

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 아시아태평양의 건설 붐

- 강화되는(VOC) 배출규제

- 2024년 이후의 자동차 생산 회복

- OECD 국가의 주택 개수 붐

- 현장에서의 3D 프린팅 수리용 수지

- 시장 성장 억제요인

- 원료 가격의 변동성

- 분말 전용 시스템으로의 이행

- 마이크로 플라스틱 단계적 폐지 규칙

- 밸류체인 분석

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모와 성장 예측

- 유형별

- 에폭시

- 아크릴

- 폴리우레탄

- 폴리에스테르

- 폴리프로필렌

- 알키드

- 기타 유형

- 최종 사용자 업계별

- 산업

- 건축

- 자동차

- 포장

- 기타 최종 사용자

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ASEAN 국가

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 남아프리카

- 이집트

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율/랭킹 분석

- 기업 프로파일

- Allnex GmbH

- Arkema

- BASF SE

- Covestro AG

- Dow

- Evonik Industries AG

- Hexion

- Huntsman International LLC

- Kangnam Chemical

- KANSAI HELIOS

- Mitsubishi Shoji Chemical Corporation

- Mitsui Chemicals Inc.

- Olin Corporation.

- Reichhold LLC 2

- Solvay

- Synthomer plc

- Uniform Synthetics

- Vil Resins

- Wanhua

제7장 시장 기회와 향후 전망

KTH 26.01.22Resins In Paints And Coatings market size in 2026 is estimated at USD 40.76 billion, growing from 2025 value of USD 38.89 billion with 2031 projections showing USD 51.55 billion, growing at 4.82% CAGR over 2026-2031.

Although the headline growth rate appears measured, policy-driven shifts away from solvent-borne chemistries are forcing formulators to retool their portfolios around waterborne acrylic, polyurethane dispersion, and other biocircular technologies. Governments on three continents tightened volatile-organic-compound (VOC) ceilings in 2024-2025, accelerating the transition timeline. The Asia-Pacific region continues to dominate value creation, thanks to infrastructure spending. However, North America and Europe are staging multi-year renovation programs that favor premium, low-VOC resins. Competitive intensity is rising as incumbents integrate renewable feedstocks, build regional dispersion plants, and deploy digital formulation platforms to compress product-development cycles.

Global Resins In Paints And Coatings Market Trends and Insights

Construction Boom Across the Asia-Pacific

Public-sector infrastructure pipelines remain the single largest demand engine for architectural and protective coatings. India's National Infrastructure Pipeline alone targets USD 1.4 trillion in cumulative capital outlays through 2025, generating a multi-year pull-through for epoxy- and polyurethane-rich bridge, port, and rail coatings. Singapore's Building and Construction Authority now requires Green Mark Platinum performance on all new public housing projects from 2025, effectively mandating water-based acrylic or polyurethane chemistries for factory-applied panels. The Philippines allocated PHP 1.1 trillion (approximately USD 20 billion) to its Build Better More program in 2024, which includes industrial coating-intensive airports, roads, and energy assets. Across the region, state-owned developers are bundling low-VOC specifications into tender documents, accelerating the adoption of dispersion technology. Resin suppliers have responded by announcing the establishment of dispersion reactors in Indonesia and Vietnam, aiming to shorten lead times and reduce freight emissions. These moves provide global incumbents with a volume hedge while enabling regional formulators to localize their supply.

Tightening VOC-Emission Regulations

The compliance window for high-solvent resins is narrowing rapidly. In January 2025 the U.S. Environmental Protection Agency capped aerosol-coating VOC content at 25% by weight-down from prior category ceilings of 45%-forcing an immediate shift in binder selection. Georgia followed with Rule 391-3-1-.02(7)(c), effective July 2025, limiting flat architectural finishes to 50 grams per liter. Europe raised the bar again when the European Commission published draft Ecolabel criteria in October 2024 that impose a 30 grams-per-liter ceiling for interior paints, achievable only with high-solids acrylic or hybrid systems. China mirrored the EU thresholds in its GB 18582-2024 standard, signaling that the world's largest construction market can no longer serve as a VOC-light haven. Resin suppliers with ready-to-scale waterborne portfolios-especially acrylic- and polyurethane-based dispersions-are winning share as formulators scramble to meet the cliff.

Feedstock Price Volatility

Price swings for propylene, benzene, and ethylene remain a significant headwind. ICIS Chemical Business reported that Asian contract propylene prices increased by 25% quarter-on-quarter in Q2 2024, following three unplanned cracker outages. Similar squeezes in Europe turned ethylene-derivative margins negative, compelling smaller epoxy producers to idle plants. Resin makers without upstream petrochemical integration face 60- to 90-day pass-through lags in the price-sensitive architectural channel. Partial insulation is emerging; Covestro has disclosed bio-circular polyols derived from waste vegetable oils that reached price parity with fossil feedstock by 2024, thereby trimming exposure to naphtha volatility. Still, the commodity link will limit margins until bio-feedstock adoption scales.

Other drivers and restraints analyzed in the detailed report include:

- Automotive Output Revival Post-2024

- Refurbishment Wave in OECD Housing

- Shift Toward Powder-Only Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Acrylic resins commanded 30.02% of the 2025 resins in paints and coatings market share, supported by their superior fit in low-VOC waterborne systems. Coupled with a 5.28% CAGR, they anchor value migration as regulators tighten emission ceilings. Epoxy resins are used in high-stress applications, such as those in the marine and wind-turbine industries; Hexion noted robust orders from turbine OEMs in its 2024 report. Polyurethane dispersions benefit from EV battery use cases. Polyester, a workhorse for powder coatings, faces margin compression as buyers mix polyester-epoxy hybrids that cure at lower temperatures. Alkyds, long the backbone of solvent-borne architectural paints, retain a niche in premium wood finishes but fade in mainstream wall-coating lines due to their slower dry time and higher VOC. ISO 14040 life-cycle assessments are now mandatory in Scandinavian public tenders, funneling share toward resins with verified environmental declarations.

Acrylic's dispersion superiority also underpins factory-applied panel lines for modular housing. Prefabrication sites prefer quick-dry, single-pass coatings to meet tight takt times, making waterborne acrylic a natural choice. Epoxy suppliers are responding with nano-modified systems that cut bake curves, while polyurethane vendors push humidity-cure versions that eliminate forced-air ovens. Across the resins in paints and coatings market, supplier innovation is converging on CO2-reduced feedstocks, evidenced by BASF's pledge to integrate renewable propylene into its acrylic value chain by 2026. This feedstock strategy aligns with European public-procurement rules granting price premiums to materials with >=20% bio-content.

The Resins in Paints and Coatings Market Report is Segmented by Type (Epoxy, Acrylic, Polyurethane, Polyester, Polypropylene, Alkyd, Other Types), End-User Industry (Industrial, Architectural, Automotive, Packaging, Other End-Users), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific accounted for a 44.12% share of the resins in paints and coatings market in 2025 and is growing fastest at a 5.33% CAGR, propelled by China's construction recovery and India's megaproject pipelines. China's residential completions rebounded in 2024 as municipal authorities eased credit, translating into higher drawdowns. India's National Infrastructure Pipeline drives protective-coating resin consumption for bridges and railways, while the IKN Nusantara capital-city buildout in Indonesia and the Philippines' Build Better More program lift regional baseline volumes. Japan's seismic-retrofit subsidy and South Korea's Green New Deal mandate low-VOC coatings in public procurement, driving the use of acrylic and polyurethane dispersions through local converting channels.

North America's momentum rests on remodeling spending that hit USD 485 billion in 2024, with energy-efficient exteriors and siding replacements at the top of the wallet. The EPA's 2025 VOC rule accelerates waterborne adoption, and Sherwin-Williams has flagged premium pricing on low-odor emulsions as margin-accretive. Canada's carbon price reached CAD 80 per metric ton in 2024 and is nudging building owners toward retrofit packages that include high-albedo roof coatings to cut cooling loads.

Europe advances at a mid-single-digit pace led by the Renovation Wave and the Industrial Emission Directive, both of which prioritize low-solvent or powder chemistries. Nordic municipalities now require product-specific environmental product declarations in tenders, advantaging suppliers with fully audited dispersion lines. South America and the Middle East and Africa collectively account for a smaller share of coating resins market size but offer pocket-growth linked to oil-and-gas, mining, and stadium construction in Brazil, Saudi Arabia, and the United Arab Emirates.

- Allnex GmbH

- Arkema

- BASF SE

- Covestro AG

- Dow

- Evonik Industries AG

- Hexion

- Huntsman International LLC

- Kangnam Chemical

- KANSAI HELIOS

- Mitsubishi Shoji Chemical Corporation

- Mitsui Chemicals Inc.

- Olin Corporation.

- Reichhold LLC 2

- Solvay

- Synthomer plc

- Uniform Synthetics

- Vil Resins

- Wanhua

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Construction boom across Asia-Pacific

- 4.2.2 Tightening (VOC)-emission regulations

- 4.2.3 Automotive output revival post-2024

- 4.2.4 Refurbishment wave in OECD housing

- 4.2.5 On-site 3-D printing repair resins

- 4.3 Market Restraints

- 4.3.1 Feed-stock price volatility

- 4.3.2 Shift toward powder-only systems

- 4.3.3 Micro-plastic phase-out rules

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Epoxy

- 5.1.2 Acrylic

- 5.1.3 Polyurethane

- 5.1.4 Polyester

- 5.1.5 Polypropylene

- 5.1.6 Alkyd

- 5.1.7 Other Types

- 5.2 By End-user Industry

- 5.2.1 Industrial

- 5.2.2 Architectural

- 5.2.3 Automotive

- 5.2.4 Packaging

- 5.2.5 Other End-users

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Egypt

- 5.3.5.5 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Allnex GmbH

- 6.4.2 Arkema

- 6.4.3 BASF SE

- 6.4.4 Covestro AG

- 6.4.5 Dow

- 6.4.6 Evonik Industries AG

- 6.4.7 Hexion

- 6.4.8 Huntsman International LLC

- 6.4.9 Kangnam Chemical

- 6.4.10 KANSAI HELIOS

- 6.4.11 Mitsubishi Shoji Chemical Corporation

- 6.4.12 Mitsui Chemicals Inc.

- 6.4.13 Olin Corporation.

- 6.4.14 Reichhold LLC 2

- 6.4.15 Solvay

- 6.4.16 Synthomer plc

- 6.4.17 Uniform Synthetics

- 6.4.18 Vil Resins

- 6.4.19 Wanhua

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment