|

시장보고서

상품코드

1686630

폴리올레핀(PO) 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Polyolefin (PO) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

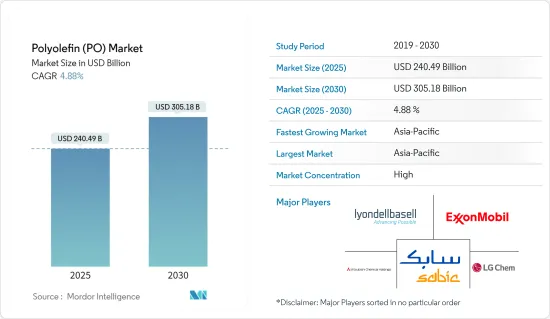

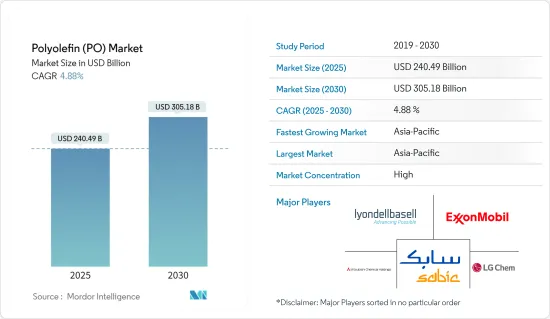

폴리올레핀(PO) 시장 규모는 2025년에 2,404억 9,000만 달러로 추정되고, 2030년에는 3,051억 8,000만 달러에 이를 것으로 예측되며, 예측 기간(2025-2030년)에 CAGR 4.88%로 성장할 전망입니다.

코로나19의 확산은 시장에 심각한 영향을 미쳐 많은 최종 사용자 산업이 문을 닫았습니다. 팬데믹 기간 동안 중국은 포장, 완구 제조, 건설, 자동차 등 강력한 산업으로 인해 폴리올레핀의 주요 소비국 중 하나이기 때문에 폴리올레핀 시장에 집중적으로 타격을 입었습니다. 그러나 2021년에 산업이 제조 활동을 재개함에 따라 연구 대상 시장도 회복될 수 있습니다.

주요 하이라이트

- 폴리올레핀은 고급 특성으로 인해 전자, 자동차 및 기타 산업에서 사용됩니다. 이는 단기적으로 시장 성장에 도움이 될 것으로 예상됩니다.

- 그러나 여러 정부에서 부과하는 플라스틱에 대한 환경 규제가 증가함에 따라 시장이 제한될 수 있습니다.

- 친환경 폴리올레핀에 대한 관심이 높아지면서 향후 몇 년 동안 새로운 기회가 창출될 것으로 보입니다.

- 아시아태평양은 세계 시장을 지배하고 있으며, 인도와 중국에서 가장 많은 소비가 이루어지고 있습니다.

폴리올레핀(PO) 시장 동향

시장 성장을 주도하는 필름 및 시트 부문의 수요 증가

- 필름과 시트는 운송, 포장, 건설 및 건축 산업에서 사용할 수 있습니다.

- 농업 부문은 온실, 멀치 및 사일리지 스트레치 필름용 폴리올레핀 필름과 시트에 대한 수요로 시장 확장을 주도하고 있습니다. 사일리지 시트와 윈도우 필름은 물론 의료 산업에서도 수요가 증가하고 있습니다.

- 폴리올레핀 기반 농업용 필름은 서리, 바람, 비, 해충으로부터 채소를 보호하는 동시에 과일, 채소, 꽃의 숙성 속도를 높여 농부들이 한 해에 여러 작물을 재배할 수 있게 해줍니다. 폴리올레핀 필름은 또한 증발을 줄여 물을 절약하는 데 도움이 됩니다.

- 반면에 폴리올레핀 시트는 건축 산업에서 사용됩니다. 증기 지연제 역할을 하는 폴리에틸렌 시트는 슬래브 아래에 설치됩니다. 이 시트는 성능 저하 없이 더 오랜 시간 동안 증기를 지연시킬 수 있습니다. 그 결과 건설 업계에서 폴리올레핀에 대한 수요가 확대되고 있습니다.

- 아시아태평양의 건설 업계는 세계에서 가장 크고 빠르게 성장하는 산업이 될 것으로 예상되며, 전 세계 건설 지출의 45%가 이 지역에서 발생할 것으로 전망됩니다. 향후 몇 년 동안 더 많은 사람들이 필름과 시트를 선택할 것으로 보입니다.

- 2022년도 인도의 폴리올레핀 총 생산 능력은 1만 2,000킬로톤을 초과했습니다. 대부분의 폴리올레핀은 인도 전체 폴리올레핀 생산 능력의 약 47%를 차지하는 릴라이언스 인더스트리(Reliance Industries Limited)에서 생산했습니다.

- 따라서 이러한 요인으로 인해 폴리올레핀 시장은 필름과 시트에 대한 수요가 증가함에 따라 향후 몇 년 동안 성장할 것으로 보입니다.

아시아태평양이 시장을 독점

- 중국이 전 세계 폴리올레핀의 주요 소비국이기 때문에 아시아 태평양 지역은 폴리올레핀 시장의 지배적인 지역입니다. 택배 사업의 호조로 플라스틱 포장재에 대한 수요가 급증하면서 전자상거래가 증가함에 따라 성장을 주도하고 있습니다. 중국의 제조업은 중국 경제에 크게 기여하는 산업 중 하나입니다.

- 중국 정부는 향후 10년간 2억 5,000만 명의 인구를 새로운 대도시로 이주시킬 계획을 포함한 대규모 건설 계획을 발표했습니다. 이는 건설 과정에서 건물의 특성을 개선하기 위해 건설용 화학 물질이 다양한 방식으로 사용될 수 있는 큰 기회입니다.

- 스마트폰, OLED TV, 태블릿 및 기타 가전제품과 같은 전자제품은 시장에서 가장 빠른 성장을 기록하고 있습니다. 중산층의 주머니에 돈이 많아지면 전자 제품에 대한 수요가 늘어날 것이며, 이는 중국 내 폴리올레핀 수요를 견인할 수 있습니다.

- 중국의 전자 부문은 2023년 말까지 3,850억 달러 이상에 달할 것으로 예상됩니다.

- 위에서 언급한 모든 요인이 예측 기간 동안 폴리올레핀에 대한 수요를 증가시킬 것으로 예상됩니다.

폴리올레핀(PO) 산업 개요

폴리올레핀 시장은 본질적으로 통합되어 있습니다. 주요 기업(특정한 순서 없음)에는 LyondellBasell Industries Holdings BV, ExxonMobil Corporation, SABIC, LG Chem, Mitsubishi Chemical Holdings Corporation 등이 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 성장 촉진요인

- 경질 포장으로부터 연포장으로의 선호도 변화

- 저비용 인테리어 가구에 대한 수요 증가

- 억제요인

- 환경 규제 증가

- 업계 밸류체인 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 세분화

- 재료 유형

- 폴리에틸렌(PE)

- 고밀도 폴리에틸렌(HDPE)

- 저밀도 폴리에틸렌(LDPE)

- 선형 저밀도 폴리에틸렌(LLDPE)

- 폴리프로필렌(PP)

- 폴리에틸렌(PE)

- 용도

- 필름 및 시트

- 사출 성형

- 블로우 성형

- 압출 코팅

- 섬유와 라피아

- 지역

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 이탈리아

- 프랑스

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- M&A, 합작사업, 제휴, 협정

- 시장 점유율 및 랭킹 분석

- 주요 기업의 전략

- 기업 프로파일

- Arkema Group

- BASF SE

- Braskem

- Chevron Phillips Chemical Company

- China National Petroleum Corporation

- China Petrochemical Corporation

- Daelim

- Dow

- ExxonMobil Corporation

- Formosa Plastics Corporation

- Japan Polypropylene Corporation

- LG Chem Ltd.

- LyondellBasell Industries Holdings BV

- Mitsubishi Chemical Holdings Corporation

- Mitsui Chemicals Incorporated

- Nova Chemicals Corporation

- PetroChina Company Limited

- Reliance Industries Limited

- SABIC(Saudi Basic Industries Corporation)

- Sasol Ltd.

- Tosoh Corporation

제7장 시장 기회와 앞으로의 동향

- 친환경 폴리올레핀에 대한 관심 고조

The Polyolefin Market size is estimated at USD 240.49 billion in 2025, and is expected to reach USD 305.18 billion by 2030, at a CAGR of 4.88% during the forecast period (2025-2030).

The spread of COVID-19 severely affected the market, causing many end-user industries to shut down. During the pandemic, China hampered the polyolefins market intensively, as it is one of the major consumers of polyolefins owing to its strong industries such as packaging, toy manufacturing, construction, and automotive. However, as the industries resumed their manufacturing activities in 2021, the market studied may also recover.

Key Highlights

- Polyolefin is used in electronics, cars, and other industries because of its advanced properties. This is expected to help the market grow in the short term.

- However, growing environmental regulations on plastic imposed by various governments may restrain the market.

- The growing focus on green polyolefin is likely to create new opportunities in the coming years.

- Asia-Pacific dominated the market worldwide, with the largest consumption coming from India and China.

Polyolefin (PO) Market Trends

Increasing Demand in the Films and Sheets Segment to Drive Market Growth

- Films and sheets can be used in the transportation, packaging, construction, and building industries.

- The agricultural sector is driving the market's expansion, with demand for polyolefin films and sheets for greenhouses, mulch, and silage stretch films. The demand is also seen in silage sheets and window films, as well as in the medical industry.

- Polyolefin-based agricultural films also protect vegetables from frost, wind, rain, and pests while speeding up the ripening of fruits, vegetables, and flowers, allowing farmers to grow several crops in a year. Polyolefin films also help reduce evaporation, thus saving water.

- On the other hand, polyolefin sheets are used in the building industry. Polyethylene sheeting, which works as a vapor retarder, is installed beneath the slab. These sheets can retard for a longer time without degrading. As a result, the demand for polyolefin from the construction industry is expanding.

- The Asia-Pacific construction industry is projected to become the world's largest and fastest-growing industry, with a 45% share of global construction spending coming from the region. In the coming years, this is likely to make more people opt for films and sheets.

- In fiscal year 2022, India had a total polyolefins production capacity of over 12 thousand kilotons. Most polyolefins were made by Reliance Industries Limited, which made up almost 47% of India's total polyolefins production capacity.

- Thus, due to these factors, the polyolefin market is likely to grow in the coming years as the demand for films and sheets rises.

Asia-Pacific to Dominate the Market

- Asia-Pacific is the dominant region in the polyolefins market, owing to China being the major consumer of polyolefins worldwide. The growth is driven by increasing e-commerce, as the strong courier business led to a spike in demand for plastic packaging. The country's manufacturing industry is one of the major contributors to its economy.

- The Chinese government announced big building plans for the next 10 years, including plans to move 250 million people to new megacities. This is a big chance for construction chemicals to be used in a variety of ways to improve building properties during construction.

- Electronic items, such as smartphones, OLED TVs, tablets, and other consumer electronics, are recording the fastest growth in the market. With more money in the pockets of the middle class, there will be more demand for electronics, which may drive the demand for polyolefins in the country.

- In China, the electronics segment was projected to reach over USD 385 billion by the end of 2023.

- All the above-mentioned factors are expected to increase the demand for polyolefins over the forecast period.

Polyolefin (PO) Industry Overview

The polyolefin market is consolidated in nature. Some of the major players (not in any particular order) include LyondellBasell Industries Holdings BV, ExxonMobil Corporation, SABIC, LG Chem, and Mitsubishi Chemical Holdings Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Shift in Preferences from Rigid Packaging to Flexible Packaging

- 4.1.2 Growing Demand for Low-Cost Interior Furnishings

- 4.2 Restraints

- 4.2.1 Growing Environmental Regulations

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Material Type

- 5.1.1 Polyethylene (PE)

- 5.1.1.1 High Density Polyethylene (HDPE)

- 5.1.1.2 Low Density Polyethylene (LDPE)

- 5.1.1.3 Linear Low-density Polyethylene (LLDPE)

- 5.1.2 Polypropylene (PP)

- 5.1.1 Polyethylene (PE)

- 5.2 Application

- 5.2.1 Films and Sheets

- 5.2.2 Injection Molding

- 5.2.3 Blow Molding

- 5.2.4 Extrusion Coating

- 5.2.5 Fibers and Raffia

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Arkema Group

- 6.4.2 BASF SE

- 6.4.3 Braskem

- 6.4.4 Chevron Phillips Chemical Company

- 6.4.5 China National Petroleum Corporation

- 6.4.6 China Petrochemical Corporation

- 6.4.7 Daelim

- 6.4.8 Dow

- 6.4.9 ExxonMobil Corporation

- 6.4.10 Formosa Plastics Corporation

- 6.4.11 Japan Polypropylene Corporation

- 6.4.12 LG Chem Ltd.

- 6.4.13 LyondellBasell Industries Holdings BV

- 6.4.14 Mitsubishi Chemical Holdings Corporation

- 6.4.15 Mitsui Chemicals Incorporated

- 6.4.16 Nova Chemicals Corporation

- 6.4.17 PetroChina Company Limited

- 6.4.18 Reliance Industries Limited

- 6.4.19 SABIC (Saudi Basic Industries Corporation)

- 6.4.20 Sasol Ltd.

- 6.4.21 Tosoh Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Focus on Green Polyolefin