|

시장보고서

상품코드

1445511

후안부 질환 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2024-2029년)Posterior Segment Eye Disorders - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

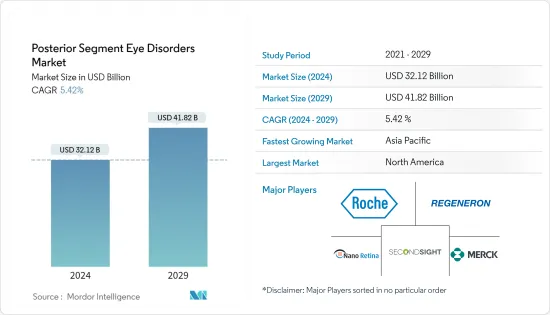

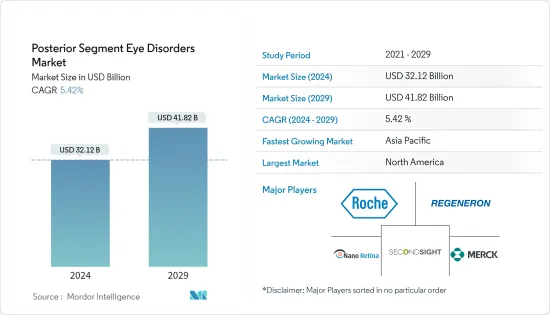

후안부 질환 시장 규모는 2024년 321억 2,000만 달러로 추정되며, 2029년까지 418억 2,000만 달러에 달할 것으로 예상되며, 예측 기간(2024-2029년) 동안 5.42%의 CAGR로 성장할 것으로 예상됩니다.

COVID-19 감염병의 대유행으로 인해 COVID-19 이외의 다른 질환에 대한 치료제 및 의약품 연구 개발 활동이 중단되었습니다. 이는 전 세계 의약품 및 의료기기의 치료 절차 및 공급망, 그리고 후안부 질환 시장에 영향을 미쳤습니다. 예를 들어, 2021년 3월 Offtalmologer-Barraker 잡지가 발표한 건강 관련 기사에 따르면, COVID-19는 질병이 매우 빠르게 진행되어 검사 기관에서 추적 관찰할 수 없는 녹내장 환자에게 심각하고 돌이킬 수 없는 결과를 초래했다고 합니다. 경우에 따라서는 시력 상실로 이어지기도 했습니다. 따라서 COVID-19가 후안부 질환 시장에 미치는 전반적인 영향은 주로 후안부 관련 질환의 진단 및 치료 절차의 감소로 인해 후안부 질환 시장에 부정적인 영향을 미쳤습니다. 그러나 전염병 관련 제한으로 인해 발생한 수술 미수술을 해소하기 위해 전 세계적으로 안과 질환 수술이 증가하여 전염병 후반기에 시장 성장을 보완했습니다.

후안부 질환은 전 세계 시각 장애의 주요 원인 중 하나입니다. 안과 질환, 당뇨병 및 안과 질환에 취약한 노인 인구의 증가로 인해 유병률이 점차 증가하고 있습니다. 이러한 질병의 부담이 증가함에 따라 전 세계적으로 진단 및 치료에 대한 수요가 증가하여 연구 시장의 성장을 주도하고 있습니다.

세계녹내장협회(WGA)의 2022년 최신 정보에 따르면 2020년에는 약 7,960만 명이 녹내장을 앓고 있으며, 그 수는 2020년까지 1억 1,180만 명에 달할 것으로 예측됩니다. 또한 녹내장 환자의 50% 이상이 녹내장을 인지하지 못하고 있다는 점도 강조했습니다. 일부 신흥국에서는 녹내장 환자의 약 90%가 발견되지 않고 있습니다. 따라서 녹내장의 급격한 증가는 결국 예측 기간 동안 후안부 질환 시장을 견인할 것으로 예상됩니다.

신제품 출시, R&D, 협업, 합병 및 인수합병으로 인해 후안부 질환 시장은 예측 기간 동안 성장할 것으로 예상됩니다. 예를 들어, 일리덱스 코퍼레이션은 2022년 6월 중국 국가약품감독관리국(NMPA)으로부터 녹내장 치료용 Cyclo G6 플랫폼의 중국 내 판매 및 판매에 대한 규제 당국의 승인을 획득했습니다.

안질환에 대한 인식이 높아짐에 따라 후안부 질환 시장은 예측 기간 동안 건전한 성장을 기록할 것으로 예상됩니다. 그러나 각국의 엄격한 규제 정책과 개발도상국 및 저개발국가의 적절한 의료 인프라 부족 등의 요인으로 인해 이러한 성장이 억제될 수 있습니다.

후안부 질환 시장 동향

제약 부문별 소분자는 예측 기간 동안 상당한 시장 점유율을 유지할 것으로 예상

질병을 치료하기 위해 생화학적 과정을 변화시킬 수 있는 저분자량 화합물을 저분자 약물이라고 합니다. 안과 질환의 부담 증가, 새로운 치료법 혁신을 위한 연구 개발 증가, 제품 출시 등의 요인이 이 부문의 성장을 주도하고 있습니다.

국립의학도서관이 2021년 11월에 발표한 연구에 따르면, 2020년 전 세계적으로 약 1억 312만 명의 성인이 당뇨병성 망막증을 앓고 있으며, 2045년까지 1억 6050만 명으로 늘어날 것으로 예측됩니다. 따라서 안질환에 대한 부담이 증가하고 있습니다. 이에 따라 치료에 대한 수요가 증가할 가능성이 높으며, 이는 이 부문을 견인할 것으로 보입니다.

이 시장 부문은 임상 연구의 증가와 시장 참여자 간의 협력에 힘입어 성장세를 보이고 있습니다. 예를 들어, 2021년 12월 AbbVie Inc.(Aragan)는 미국 FDA로부터 VUITY(피로카르핀 염산염 점안액) 1.25%를 노안 치료제로 승인받아 미국 약국에서 처방전 없이 구입할 수 있게 되었습니다. 이러한 출시는 시장 부문의 성장을 촉진할 것으로 예상됩니다. 따라서 소분자 부문은 예측 기간 동안 성장할 것으로 예상됩니다.

북미는 예측 기간 동안 주요 시장 점유율을 유지할 것으로 예상

북미 지역은 탄탄한 의료 인프라, 주요 시장 기업의 존재, 신제품 출시 및 이 지역의 후안부 질환 부담 증가로 인해 상당한 시장 성장이 예상됩니다.

합병 및 인수합병의 증가는 시장 성장의 주요 원인 중 하나입니다. 예를 들어, 2021년 11월 알콘은 Ivantis Inc.를 인수하여 수술용 녹내장용 Hydrus 마이크로 스텐트를 추가하여 제품 포트폴리오를 확장했습니다. Hydrus 마이크로 스텐트는 캐나다의 주요 제품 중 하나입니다. 이번 인수를 통해 알콘은 시장에서의 입지를 확대했습니다.

2021년 9월, Zilia Inc.는 시드 파이낸싱을 통해 316만 달러를 투자받았습니다. 이는 후안부 질환의 진단 건수를 증가시켜 안과 진단 분야로의 진입을 촉진할 것으로 보입니다. 이 제품은 녹내장, 당뇨망막병증, 노화 황반변성 등 안질환의 중요한 바이오마커인 눈의 산소포화도를 측정할 수 있습니다.

따라서 이러한 요인으로 인해 북미 시장은 예측 기간 동안 더 빠른 성장을 이룰 것으로 예상됩니다.

후안부 질환 산업 개요

후안부 질환 시장은 적당히 세분화되어 있습니다. 시장 참여자들은 시장 점유율을 확대하기 위해 신제품 출시, 제품 혁신, 지역 확장 및 협업에 초점을 맞추고 있습니다. 시장에서 활동하는 주요 시장 기업으로는 F. Hoffmann-La Roche AG, Regeneron Pharmaceuticals Inc, Rainbow Medical Ltd(Nano Retina), Second Sight Medical, Merck & Co. 등이 있습니다.

기타 혜택

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

목차

제1장 서론

- 조사 가정과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- 증가하는 안후부 질환 부담

- 후안부 질환 치료를 위한 새로운 치료법을 향한 연구개발 확대

- 시장 성장 억제요인

- 엄격한 규제 정책

- Porter's Five Forces 분석

- 신규 참여업체의 위협

- 구매자의 교섭력

- 공급 기업의 교섭력

- 대체 제품의 위협

- 경쟁 기업간 경쟁 강도

제5장 시장 세분화

- 제품별

- 약물

- 저분자

- 생물학적 제제

- 디바이스

- 치료 기기

- 진단 장비

- 약물

- 용도별

- 황반변성

- 녹내장

- 당뇨망막병증

- 기타 용도

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카공화국

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 상황

- 기업 개요

- Alcon Inc.

- Abbvie Inc.(Allergen PLC)

- Bausch Health Companies Inc.

- F Hoffmann-La Roche

- Merck &Co. Inc.

- Novartis AG

- Santen Pharmaceuticals

- Rainbow Medical Ltd(Nano Retina)

- Regeneron Pharmaceuticals Inc.

- Second Sight Medical Products Inc.

- Aerie Pharmaceuticals

제7장 시장 기회와 향후 동향

ksm 24.03.18The Posterior Segment Eye Disorders Market size is estimated at USD 32.12 billion in 2024, and is expected to reach USD 41.82 billion by 2029, growing at a CAGR of 5.42% during the forecast period (2024-2029).

The COVID-19 pandemic disrupted the research and development activities of other therapies and drugs for medical conditions other than COVID-19. It impacted the treatment procedures and supply chains of pharmaceuticals and medical devices worldwide and the market for posterior segment eye disorders. For instance, according to a health article published in March 2021 by Oftalmologaa Barraquer, COVID-19 caused severe and irreversible consequences for people with glaucoma who suffered a very rapid evolution of the disease and have not been able to carry out follow-ups by the specialist, which, in some cases, resulted in a loss of the visual field. Therefore, the overall impact of COVID-19 on the posterior segment eye disorders market was adverse, primarily due to the decline in the diagnostics and treatment procedures of the diseases associated with the posterior segment of the eye. However, the rise in eye disorder surgeries worldwide to clear the backlogs of surgical procedures caused by the pandemic-related restrictions compensated for the market's growth in the later phase of the pandemic.

Posterior segment eye disorders are one of the major causes of visual impairments worldwide. Their prevalence is increasing gradually due to the increase in the prevalence of eye diseases, diabetes, and geriatric populations that are more vulnerable to eye ailments. With the increase in the burden of these diseases, the demand for diagnostics and treatment is increasing worldwide, driving the growth of the studied market.

According to the World Glaucoma Association (WGA) 2022 update, around 79.6 million people were living with glaucoma in 2020, and the number is projected to reach 111.8 million people by 2040. It also highlighted that at least 50% of glaucoma sufferers are unaware of their condition, and around 90% of glaucoma cases in some developing countries are undetected. Thus, the surge in glaucoma is ultimately projected to boost the posterior segment eye disorders market over the forecast period.

With the launch of new products, research and development, collaboration, mergers, and acquisitions, the market for posterior segment eye disorders is expected to grow during the forecast period. For instance, in June 2022, Iridex Corporation received regulatory approval to market and sell its Cyclo G6 platform for the treatment of glaucoma diseases in China from its National Medical Products Administration (NMPA).

Due to the rising awareness about eye disorders and the factors mentioned above, the posterior segment eye disorders market is expected to register healthy growth over the forecast period. However, factors such as stringent regulatory policies of different countries and the lack of proper healthcare infrastructure in developing and under-developing countries are likely to restrain this growth.

Posterior Segment Eye Disorders Market Trends

Small Molecules by Drugs Segment is Expected to Hold a Significant Market Share Over the Forecast Period

Compounds with a low molecular weight that can change the biochemical processes for treating diseases are known as small-molecule drugs. Factors such as the growing burden of eye disorders, increasing R&D for the innovation of new therapeutics, and the launch of products are driving segmental growth.

As per the study published in November 2021 by the National Library of Medicine, around 103.12 million adults were living with diabetic retinopathy globally in 2020, and the number is projected to increase to 160.50 million by 2045. Thus, the growing burden of eye disorders is likely to increase the demand for their treatment, thus driving the segment.

The market segment is also boosted by increasing clinical studies and collaboration among the market players. For instance, in December 2021, AbbVie Inc. (Allergan) received approval for VUITY (pilocarpine HCl ophthalmic solution) 1.25% by the US FDA to treat presbyopia and be available by prescription in pharmacies in the United States. Such launches are expected to drive the growth of the market segment. Thus, the small molecules segment is expected to project growth over the forecast period.

North America is Expected to Hold a Major Market Share Over the Forecast Period

North America is anticipated to have significant market growth owing to its well-established healthcare infrastructure, the presence of key market players, new product launches, and the rising burden of posterior eye disorders in the region.

The growing mergers and acquisitions are one of the key reasons for the market's growth. For instance, in November 2021, Alcon acquired Ivantis Inc. to expand its product portfolio by adding the Hydrus micro stent for surgical glaucoma. Hydrus micro stent is one of the key products in Canada. With this acquisition, Alcon expanded its presence in the market.

In September 2021, Zilia Inc. received USD 3.16 million through seed financing. This would aid the company's entry into ocular diagnostics by increasing the number of posterior segment eye disorders diagnoses. The product can measure oxygen saturation in the eye, an important biomarker for eye diseases such as glaucoma, diabetic retinopathy, and age-related macular degeneration.

Hence, owing to such factors, the North American market is expected to have faster growth over the forecast period.

Posterior Segment Eye Disorders Industry Overview

The market for posterior segment eye disorders is moderately fragmented. Market players are focusing on new product launches, product innovation, regional expansions, and collaborations to increase their market share. The key market players operating in the market include F. Hoffmann-La Roche AG, Regeneron Pharmaceuticals Inc., Rainbow Medical Ltd (Nano Retina), Second Sight Medical, and Merck & Co. Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Burden of Back of the Eye Disorders

- 4.2.2 Growing R&D for New Therapies for the Treatment of Posterior Segment Eye Disorders

- 4.3 Market Restraints

- 4.3.1 Stringent Regulatory Policies

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Product

- 5.1.1 Drugs

- 5.1.1.1 Small Molecules

- 5.1.1.2 Biologics

- 5.1.2 Devices

- 5.1.2.1 Therapeutic Devices

- 5.1.2.2 Diagnostic Devices

- 5.1.1 Drugs

- 5.2 By Application

- 5.2.1 Macular Degeneration

- 5.2.2 Glaucoma

- 5.2.3 Diabetic Retinopathy

- 5.2.4 Other Applications

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Alcon Inc.

- 6.1.2 Abbvie Inc. (Allergen PLC)

- 6.1.3 Bausch Health Companies Inc.

- 6.1.4 F Hoffmann-La Roche

- 6.1.5 Merck & Co. Inc.

- 6.1.6 Novartis AG

- 6.1.7 Santen Pharmaceuticals

- 6.1.8 Rainbow Medical Ltd (Nano Retina)

- 6.1.9 Regeneron Pharmaceuticals Inc.

- 6.1.10 Second Sight Medical Products Inc.

- 6.1.11 Aerie Pharmaceuticals