|

시장보고서

상품코드

1937323

황산 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Sulfuric Acid - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

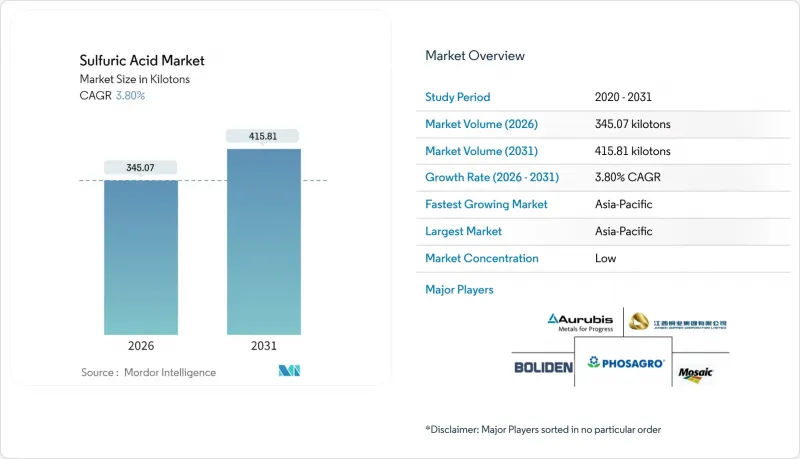

2026년 황산 시장 규모는 345.07 킬로톤으로 추정되고, 2025년 332.44 킬로톤에서 성장이 전망됩니다.

2031년 예측치는 415.81 킬로톤으로 2026년부터 2031년까지 CAGR 3.80%로 확대될 전망입니다.

특히 중국, 인도, 모로코의 인산비료 생산업체들의 견조한 수요가 이러한 성장세를 뒷받침하고 있습니다. 각국 정부가 식량 안보와 작물 수확량 안정성을 우선시하기 때문입니다. 비철금속 제련과 석유정제의 수직적 통합으로 인해 자체 소비를 위한 공급량이 증가하고, 원료 소유자와 다운스트림 산 소비자 간의 역사적 격차가 줄어들고 있습니다. 새로운 배터리 전해질 요건과 초저유황 연료 규제 강화로 인해 고객 기반이 다양해지고 지역 무역 흐름이 재편되고 있습니다. 운임 변동과 ESG 대응에 따른 컴플라이언스 비용 증가로 수익률이 압박을 받고 있는 가운데, 사업자들은 에너지 소비와 배기가스 배출을 억제하는 공정 제어의 고도화와 디지털 성능 관리 도구의 도입을 가속화하고 있습니다.

세계 황산 시장 동향 및 전망

아시아 및 아프리카의 인산 비료 생산능력 확대

모로코에서는 2025년 가동 예정인 유황 연소 프로젝트를 통해 현지 황산 공급량이 증가하여 다운스트림 인산염 생산이 강화될 것입니다. 인도에서는 모리타니와의 정책적 지원 수입 협정을 통해 암석 인산염 원료의 안정적 공급을 확보하여 신규 인산 반응로 가동을 지원하고 황산 수요 확대를 촉진할 것입니다. 미국 지질조사국(USGS)은 2027년까지 세계 인산염 생산능력이 6,910만 톤에 달할 것으로 예측하고 있으며, 브라질, 카자흐스탄, 멕시코, 모로코, 러시아가 동시에 확장에 나서고 있습니다. 이러한 신규 공급은 대서양과 인도양 운송 루트 주변에 새로운 수요를 집중시켜 트레이더들이 현물 화물을 재배치하거나 장기 오프 테이크 계약을 체결하도록 유도하고 있습니다. 공급망은 기존의 중동에서 아시아로 향하던 경로에서 북아프리카와 남아시아를 중심으로 한 역내 유통으로 전환되고 있으며, 이는 독립적인 혼합업체와 유통업체들의 순이익을 압박하고 있습니다.

초저유황 연료 기준 강화로 유황 회수 촉진

북미와 유럽의 연료 규제(황 함량 10ppm 이하 의무화)로 인해 정유사들은 크라우스 설비의 회수율을 극대화하고 회수된 황을 더 많은 자체 황산 스트림으로 전환할 수밖에 없습니다. 통합 에너지 기업은 이산화황(SO2) 전환율 99.7% 이상을 달성하기 위해 배기가스 처리 설비의 개보수를 진행하고 있습니다. 이 업그레이드는 비료 플랜트용 국내 공급원을 직접적으로 확대하는 것입니다. 이러한 투자는 자본 집약적이지만, 배출 페널티에 대한 부채를 상쇄하고, 과거 폐기 비용 센터였던 것을 수익화할 수 있게 해줍니다.

정유공장 합리화에 따른 유황 공급 변동성

성숙한 시장의 정유사들이 생산능력을 폐쇄하거나 바이오 원료로 전환하면서 원소 황의 생산량은 예측할 수 없을 정도로 변동이 심합니다. 서유럽의 사업자들은 회수된 유황 공급에 수개월에 걸친 공백이 발생하고 있으며, 비료 단지들은 높은 가격으로 수입을 확보해야 하는 상황에 처해있다고 보고하고 있습니다. 황산 시장 진입 기업들은 황철광 로스팅이나 산 재생과 같은 유연한 원료 전략을 채택하여 이러한 위험을 헤지하고 있지만, 이러한 선택은 더 높은 에너지 소비와 규제 당국의 감시를 수반합니다.

부문 분석

2025년 황산 시장 규모에서 원소 황은 생산량의 78.40%를 차지하여 2031년까지 CAGR 3.79%의 기반이 될 것입니다. 천연가스 처리 및 청정 연료 정제로부터의 회수는 황철광 로스팅으로는 달성하기 어려운 비용 우위를 확보하고 있습니다. IntraTech Alert가 기록하는 휘발성 황 벤치마크는 때때로 이 차이를 좁히지만, 통합을 통한 시너지 효과는 여전히 원소 황 경로를 유리하게 만듭니다.

정유소의 황화수소 스트림은 예측 가능한 원료 순도를 제공하고, DCDA 컨버터의 촉매 제어를 단순화합니다. 이를 통해 작업자는 250ppm 미만의 산성 미스트 목표를 달성할 수 있습니다. 원유 조성이 산성화 추세를 보이면 황산 산업은 생산량 증가를 조정하고 비료 수요의 급격한 증가와 균형을 맞출 것입니다. 한편, 유럽 내 정유소의 합리화로 공급이 감소하면서 트레이더들은 페르시아만에서 생산된 황산을 앤트워프나 함부르크 터미널로 옮기는 움직임을 보이고 있습니다.

DCDA 루트는 2025년 세계 생산량의 89.30%를 차지했으며, CAGR 3.86%로 황산 시장의 전체 성장률을 상회할 것입니다. 갱신 주기에는 신속한 점화와 수명 연장을 실현하는 독자 개발한 세슘 촉진제를 배합한 오산화바나듐 촉매를 채용하고 있습니다.

인도네시아와 사우디아라비아의 신규 플랜트에서는 SO3 슬립을 최소화하기 위해 완전 자동화된 패스 간 온도 제어를 사양으로 채택하고 있습니다. 한편, 폴란드의 개보수 공사에서는 열회수형 증기발생기를 활용하여 톤당 최대 25 MJ의 순에너지 사용량을 절감하고 있습니다.

지역별 분석

아시아태평양은 2025년 세계 소비량의 51.20%를 차지했으며, 2031년까지 연평균 4.03%의 CAGR로 선두를 차지할 것으로 예상됩니다. 중국 클라우드남성과 후베이성에 위치한 인산비료 단지에서는 기존 설비의 병목현상 해소가 진행되고 있으며, 인도에서는 신규 인산 반응로가 정부 보조금 제도와 연계되어 국내 생산을 촉진하고 있습니다. 절강성 및 사천성 배터리 소재 단지는 다년간의 오프 테이크 계약에 따라 고순도 제품 공급을 계약하고 있으며, 이에 따라 일반용 산의 추가 수입 수요가 고정되어 있습니다.

북미의 제련소 연동형 회수 네트워크는 성숙한 고객 기반에 공급하고 있으며, 미국 대서양 연안의 생산능력의 합리화로 잉여분이 감소하고 있습니다. 유럽에서는 엄격한 환경 규제가 유지되고 있으며, DCDA(이염화이암모늄) 설비의 개보수 및 2차 스크러버 설치가 광범위하게 추진되고 있습니다. 비료 등급의 수요는 토지 살포 제한 강화로 인해 완만하게 증가하는 반면, 독일과 네덜란드의 특수 화학 산업 집적지에서는 고순도 산의 소비가 증가하고 있습니다.

남미에서는 칠레, 페루, 브라질을 중심으로 아시아를 제외한 지역에서 가장 높은 공급 증가를 기록하고 있습니다. 자급자족형 구리 제련소가 자체 소비용 산을 생산하여 미국 걸프만으로부터의 해상 운송화물을 대체하고 있습니다. 브라질 세라도 지역의 농업 거점에서는 리드타임 단축과 운임 프리미엄 절감을 위해 지역 공급을 우선하여 운송 장애 시 납품가격을 안정화시키고 있습니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSM 26.03.12Sulfuric Acid market size in 2026 is estimated at 345.07 kilotons, growing from 2025 value of 332.44 kilotons with 2031 projections showing 415.81 kilotons, growing at 3.80% CAGR over 2026-2031.

Robust demand from phosphate fertilizer producers, particularly across China, India, and Morocco, anchors this trajectory as governments prioritize food security and crop-yield resilience. Vertical integration in non-ferrous smelting and petroleum refining yields incremental captive supply, narrowing the historical divide between raw-material owners and downstream acid consumers. New battery-grade electrolyte requirements and tightening ultra-low-sulfur fuel regulations are diversifying the customer base and reshaping regional trade flows. Freight-rate volatility and rising ESG-driven compliance outlays compel margins, prompting operators to accelerate process-control upgrades and digital performance tools that curb energy intensity and tail-gas emissions.

Global Sulfuric Acid Market Trends and Insights

Phosphate-Fertilizer Capacity Expansions in Asia and Africa

Morocco's sulfur-burning projects, scheduled for commissioning in 2025, will raise local acid availability and bolster downstream phosphate output. In India, policy-backed import pacts with Mauritania ensure rock-phosphate feedstock security, supporting new phosphoric-acid reactors that intensify sulfuric acid drawdown. The U.S. Geological Survey expects global phosphate capacity to reach 69.1 million tons by 2027, with Brazil, Kazakhstan, Mexico, Morocco, and Russia expanding simultaneously. These additions cluster fresh demand around Atlantic and Indian Ocean shipping lanes, prompting traders to reposition spot cargoes and sign longer-tenor off-take contracts. Supply chains are shifting from historic Middle East-to-Asia routes toward intra-regional flows centered on North Africa and South Asia, compressing netback margins for independent blenders and distributors.

Tightening Ultra-Low-Sulfur Fuel Specifications Boosting Sulfur Recovery

North American and European fuel regulations that mandate sulfur contents below 10 ppm are compelling refiners to maximize Claus-unit recovery and convert larger volumes of recovered sulfur into captive acid streams. Integrated energy companies are retrofitting tail-gas treating units to achieve more than 99.7% SO2 conversion, an upgrade that directly enlarges domestic supply pools for fertilizer complexes. These investments, while capital intensive, offset emission-penalty liabilities and allow refiners to monetize what was once a disposal cost center.

Sulfur Supply Volatility Linked to Refinery Rationalisation

As mature-market refineries shutter capacity or shift toward bio-feedstocks, elemental-sulfur output fluctuates unpredictably. Operators in Western Europe report multi-month gaps in recovered sulfur availability, compelling fertilizer complexes to secure imports at elevated prices. Sulfuric acid market participants hedge this exposure by adopting flexible feedstock strategies, including Pyrite roasting or acid regeneration, although these options carry higher energy footprints and regulatory scrutiny.

Other drivers and restraints analyzed in the detailed report include:

- Battery-Grade Electrolyte Demand from EVs

- Copper and Zinc Smelter Build-Outs in Latin America

- Rising ESG-Driven Capital Expenditure for Tail-Gas Scrubbing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Elemental sulfur contributed 78.40% of the 2025 output within the sulfuric acid market size and underpinned an anticipated 3.79% CAGR to 2031. Recovery from natural-gas processing and clean-fuel refining secures cost advantages that Pyrite roasting struggles to match. Volatile sulfur benchmarks, documented by Intratec Alerts, occasionally narrow this gap, but integration synergies still favor elemental pathways.

Refinery hydrogen-sulfide streams deliver predictable feedstock purity that simplifies catalyst control in DCDA converters, helping operators meet sub-250 ppm acid-mist targets. When crude slates swing toward higher sourness, the sulfuric acid industry calibrates output upswings, balancing fertilizer demand spikes. Conversely, refinery rationalisation in Europe removes supply, prompting traders to redirect Persian Gulf tonnage toward Antwerp and Hamburg terminals.

The DCDA route accounted for 89.30% of global output in 2025 and is poised to outpace headline sulfuric acid market growth with a 3.86% CAGR. Replacement cycles favor vanadium-pentoxide catalysts with proprietary cesium promoters that deliver fast ignition and extended life.

Emerging plants in Indonesia and Saudi Arabia are specifying fully automated inter-pass temperature controls to minimize SO3 slip, while retrofits in Poland exploit heat-recovery steam generators that trim net energy use by up to 25 MJ per tonne.

The Sulfuric Acid Market Report Segments the Industry by Raw Material Type (Elemental Sulfur, Pyrite Ore, and Other Raw Material Types), Production Process (Single Contact Process and Double Contact Double Absorption (DCDA)), Concentration (Standard (93-98 Wt%) and Oleum/Fuming Acid), End-User Industry (Fertilizer, Chemical and Pharmaceutical, and More), and Geography (Asia-Pacific, North America, Europe, and More).

Geography Analysis

Asia Pacific commanded 51.20% of global consumption in 2025, and is projected to widen its lead at a 4.03% CAGR to 2031. China's phosphate-fertilizer complexes in Yunnan and Hubei continue brownfield debottlenecking, while India's new phosphoric-acid reactors align with government subsidy schemes that reward local production. Battery-material parks in Zhejiang and Sichuan are contracting high-purity supply under multi-year offtakes, anchoring additional merchant-acid import needs.

North America's refinery-linked recovery network supplies a mature customer base, yet capacity rationalisation in the U.S. Atlantic seaboard trims surplus. Europe maintains stringent environmental compliance, driving widespread DCDA retrofits and secondary scrubber installations. Fertilizer-grade demand grows modestly as land-application caps tighten, yet high-purity acid consumption rises within specialty chemical corridors in Germany and the Netherlands.

South America, led by Chile, Peru, and Brazil, records the strongest incremental supply growth outside Asia. Autogenous copper smelters generate captive acid that displaces seaborne cargoes from the U.S. Gulf. Agricultural hubs in Brazil's Cerrado prefer regional supply due to shorter lead times and reduced freight premiums, stabilizing delivered prices during shipping upsets.

- Aarti Industries Ltd.

- Aluminum Corporation of China

- Aurubis AG

- BASF

- Boliden Group

- Chemtrade Logistics

- GRUPO MEXICO

- Hindustan Zinc

- Jiangxi Copper Corporation

- KANTO KAGAKU

- Mosaic

- Nouryon

- OCP

- Panoli Intermediates India Pvt. Ltd.

- PhosAgro Group

- PVS

- Sumitomo Metal Mining Co., Ltd.

- Vale

- WeylChem International GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Phosphate-fertilizer Capacity Expansions in Asia and Africa

- 4.2.2 Tightening Ultra-Low-Sulfur Fuel Specs Boosting Sulfur Recovery

- 4.2.3 Battery-grade Electrolyte Demand from EVs (Lead-acid and Emerging Zn-ion)

- 4.2.4 Copper and Zinc Smelter Build-outs in Latin America

- 4.2.5 Growing Demand from Chemical and Pharmaceutical Industries

- 4.3 Market Restraints

- 4.3.1 Sulfur Supply Volatility Linked to Refinery Rationalisation

- 4.3.2 Rising ESG-Driven Cap-ex for Tail-Gas Scrubbing

- 4.3.3 Freight Rate Spikes on Key Sulfuric Acid Trade Routes

- 4.4 Value Chain Analysis

- 4.5 Trade Analysis

- 4.6 Feedstock Analysis

- 4.7 Regional Propduction Capacity

- 4.8 Porter's Five Forces

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Raw Material Type

- 5.1.1 Elemental Sulfur

- 5.1.2 Pyrite Ore

- 5.1.3 Other Raw Material Types

- 5.2 By Production Process

- 5.2.1 Single Contact Process

- 5.2.2 Double Contact Double Absorption (DCDA)

- 5.3 By Concentration

- 5.3.1 Standard (93-98 wt%)

- 5.3.2 Oleum/Fuming Acid

- 5.4 By End-user Industry

- 5.4.1 Fertilizer

- 5.4.2 Chemical and Pharmaceutical

- 5.4.3 Automotive

- 5.4.4 Petroleum Refining

- 5.4.5 Other End-user Industries (Pulp and Paper, Metal Processing)

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Indonesia

- 5.5.1.6 Malaysia

- 5.5.1.7 Thailand

- 5.5.1.8 Vietnam

- 5.5.1.9 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Nordics

- 5.5.3.7 Russia

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Qatar

- 5.5.5.4 Egypt

- 5.5.5.5 South Africa

- 5.5.5.6 Nigeria

- 5.5.5.7 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Aarti Industries Ltd.

- 6.4.2 Aluminum Corporation of China

- 6.4.3 Aurubis AG

- 6.4.4 BASF

- 6.4.5 Boliden Group

- 6.4.6 Chemtrade Logistics

- 6.4.7 GRUPO MEXICO

- 6.4.8 Hindustan Zinc

- 6.4.9 Jiangxi Copper Corporation

- 6.4.10 KANTO KAGAKU

- 6.4.11 Mosaic

- 6.4.12 Nouryon

- 6.4.13 OCP

- 6.4.14 Panoli Intermediates India Pvt. Ltd.

- 6.4.15 PhosAgro Group

- 6.4.16 PVS

- 6.4.17 Sumitomo Metal Mining Co., Ltd.

- 6.4.18 Vale

- 6.4.19 WeylChem International GmbH

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

- 7.2 Growing Use of Oleum in Medical and Other Industries