|

시장보고서

상품코드

1690869

겸상 적혈구증 치료 시장 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)Sickle Cell Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

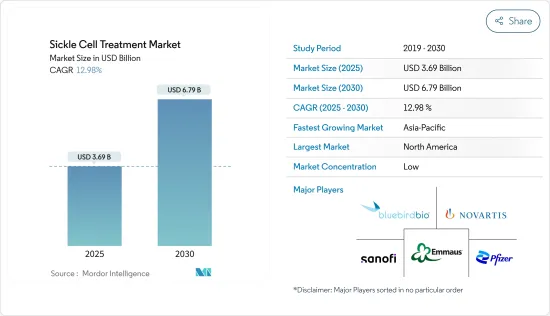

겸상 적혈구증 치료 시장 규모는 2025년에 36억 9,000만 달러로 추정되고, 예측 기간인 2025-2030년 CAGR 12.98%로 성장할 전망이며, 2030년에는 67억 9,000만 달러에 달할 것으로 예측됩니다.

겸상 적혈구증의 유병률 증가와 겸상 적혈구증에 관한 연구개발 활동 활성화 등의 요인이 시장 성장을 뒷받침할 것으로 예상됩니다.

겸상 적혈구증의 큰 부담은 치료의 필요성을 높이고 시장 성장을 가속할 것으로 예상됩니다. 예를 들면, 2024년 8월에 Frontiers in Hematology에 게재된 기사에 의하면, 겸상 적혈구증(SCD)은 널리 만연하고 있어 사하라 이남의 아프리카, 인도, 중동에서는 매년 약 30만 명의 신생아가 이환하고 있습니다. 게다가 나이지리아에서만 연간 약 15만 명의 신생아가 겸상 적혈구증을 앓고 있다고 앞서 언급한 정보원은 보고하고 있습니다. 이처럼 겸상 적혈구증의 높은 유병률은 예측 기간 동안 시장의 성장을 뒷받침할 것으로 예상됩니다.

이 질병을 치료하기 위한 다양한 정부와 민간 단체의 노력이 활발해지고 있는 것이 향후 수년간 시장을 견인할 것으로 예상됩니다. 예를 들면, 2024년 6월, 아프리카 지역의 세계보건기구(WHO)는, 이 지역에서 증가하는 겸상 적혈구증의 부담에 임하는 대처를 강화하기 위해, 혁신적인 새로운 가이드 라인을 도입했습니다. SICKLE 포장은 겸상 적혈구병을 관리하기 위한 포괄적이고 통합적인 전략을 제공하여 필수적인 개입에 대한 접근을 용이하게 하고, 교육과 애드보커시를 촉진하며, 케어의 질을 향상시키고, 환자와 커뮤니티 모두에게 힘을 실어주는 것을 목적으로 설계되었습니다. 이처럼 겸상 적혈구증 치료에 대한 인식을 높이기 위한 정부의 노력이 증가하고 있는 것이 시장의 주요 촉진 요인이며 시장 성장에 기여하고 있습니다.

또한 혁신적인 겸상 적혈구증 치료법을 개발하기 위한 연구개발 활동의 활성화도 시장을 견인할 수 있습니다. 예를 들면, 2024년 10월, 인도 의료 연구 평의회(ICMR)는 Zydus Lifesciences Limited와 겸상 적혈구증 환자를 대상으로 한 Desidustat의 제2상 임상 검사를 개시하기 위한 합의 각서를 체결했습니다. 이 회사는, 인도가 겸상 적혈구증 치료를 위한 혁신적이고 비용대비 효과가 높은 의료 솔루션 개발의 최전선에 계속 있는 것을 보증하는 것을 목적으로 하고 있습니다. 게다가 2024년 6월, 밴더 빌트 대학 메디컬 센터(VUMC)의 연구원은, 겸상 적혈구증(SCD)에 대한 유망한 새로운 근치적 치료법을 실증한 다시설 국제 공동 제2상 임상 검사의 결과를 발표했습니다. 이 치료법은 티오테파와 이식 후 시클로포스파미드(PTCy)를 병용한 비골수분리 하플로아이덴티티컬 골수이식(BMT)을 동반하는 것으로 같은 유효성을 보이며 FDA(식품의약국)가 승인한 골수분리 유전자 치료 대체요법의 5분의 1 비용밖에 들지 않습니다. 이러한 연구개발 노력의 증가는 시장의 성장을 뒷받침할 전망입니다.

이와 같이 겸상 적혈구증 유병률 상승, 정부의 대처에 대한 의식 고조, 연구개발 활동 활성화 등의 요인이 시장의 성장을 뒷받침할 것으로 예상됩니다. 그러나 치료비의 높은 수준이 이 성장을 억제할 것으로 예상됩니다.

겸상 적혈구증 치료 시장 동향

수혈 부문은 예측 기간 동안 상당한 성장이 예상됩니다.

수혈 부문은 예측 기간 동안 건전한 성장이 예상됩니다. 이 성장은 겸상 적혈구증 치료에 대한 수혈의 높은 수요와 SCD의 유병률 증가에 기인하고 있습니다. 수혈은 정상적인 적혈구 공급을 가능하게 하고, 헤모글로빈 농도를 높여 체내 산소 공급을 개선할 수 있습니다. 따라서 겸상 적혈구에 의한 혈관의 폐색이나 더 많은 겸상 적혈구를 만들려는 욕구는 감소합니다.

겸상 적혈구증 치료를 위한 수혈의 필요성이 높아지고 있다는 것은 이 부문의 성장에 크게 기여할 것으로 예상됩니다. 예를 들면, 2024년 5월에 미국 질병예방관리센터(CDC)가 갱신한 데이터에 의하면, 겸상 적혈구증(SCD) 환자는 생애의 어느 시점에서 1회 이상의 수혈(기증자로부터 건강한 혈액을 받는 것)이 필요하게 될 가능성이 있습니다. 수혈 시 환자의 혈액과 제공된 혈액은 각각의 적혈구 표면에 있는 항원 또는 특정 단백질이 일치해야 합니다.

게다가 2023년 6월에 Canadian Blood Services가 발표한 데이터에 따르면, 캐나다에서는 매년 약 1만 5,000개의 혈액이 겸상 적혈구증 환자에게 수혈되고 있습니다. 이와 같이 수혈은 겸상 적혈구증의 부담을 줄이기 위해 겸상 적혈구증 환자에 의해 대폭 채용되고 있으며, 그것이 이 부문의 성장을 견인하고 있습니다.

겸상 적혈구증에 관한 연구개발 증가도 같은 부문의 성장을 뒷받침할 것으로 예상되고 있습니다. 예를 들어 clinicaltrials.gov 이 업데이트한 데이터에 따르면 2024년 12월 현재 겸상 적혈구증 수혈에 관한 진행 중이고 활성 임상검사는 약 87건이 있습니다. 이처럼 임상검사의 수가 많음에 따라 이 치료에 대한 수혈의 채용이 촉진될 것으로 예상됩니다.

따라서 겸상 적혈구증 관리에서 수혈 사용 증가와 겸상 적혈구증에 대한 연구 개발 증가와 같은 요인이이 부문의 성장을 가속할 것으로 예상됩니다.

예측 기간 동안 북미가 겸상 적혈구증 치료 시장에서 큰 점유율을 차지할 전망

북미는 겸상 적혈구증 치료 시장 전체에서 큰 점유율을 차지할 것으로 예상되며, 그 중에서도 미국이 크게 공헌하고 있습니다. 이 지역의 성장은 겸상 적혈구증(SCD) 치료에 대한 접근성 개선과 잠재적인 파이프라인 후보에 기인하고 있습니다. 미국의 강력한 정부 지원은 시장 개척을 더욱 촉진할 것으로 보입니다. 이 지역에서의 겸상 적혈구증 유병률 상승, 임상검사 수 증가, 제품 출시 증가는 이 지역의 시장 성장을 뒷받침할 것으로 예상됩니다.

북미 국가에서 겸상 적혈구증의 큰 부담은 그 치료를 필요로 하므로 시장 성장을 가속할 것으로 예상됩니다. 예를 들면, 질병관리예방센터(CDC)가 2024년 5월에 갱신한 데이터에 의하면, 겸상 적혈구증(SCD)은 매년 약 10만 명의 미국인이 이환하고 있으며, SCD는 흑인 또는 아프리카계 미국인의 출생 365명 중 1명의 비율로 발생하고 있습니다. 마찬가지로 캐나다 혈액서비스가 2023년 6월 발표한 데이터에 따르면 겸상 적혈구증은 캐나다에서 가장 유행하는 유전성 질환으로 2023년에는 전국적으로 6,000명 이상이 이환했습니다. 따라서 이 지역에서 겸상 적혈구증의 큰 부담은 그 치료 제품에 대한 요구를 부추기고 예측 기간 동안 시장 성장을 촉진합니다.

정부의 이니셔티브 증가도 이 지역 시장 성장을 뒷받침할 것으로 기대됩니다. 예를 들어, 2024년 11월, 클린턴 헬스 액세스 이니셔티브(CHAI)는 겸상 적혈구증(SCD)과 싸우는 이니셔티브를 강화하기 위해 실리콘 밸리 커뮤니티 재단과 관련된 어드바이저드 펀드인 오픈 필란트로피에서 800만 달러의 획기적인 3년간의 조성금을 도입했습니다. 이 보조금은 미국에서 겸상 적혈구증 어린이들의 치료 및 케어 접근성 개선에 기여합니다.

게다가 2023년 10월, Mount Sinai Health System은 겸상 적혈구증의 새로운 치료법을 평가하고 개별 환자에게 가장 효과적인 치료법을 확인하기 위해 국립 심폐 혈액 실험실에서 1,200만 달러의 보조금을 수여받았습니다. REAL(Registry Expansion Analyses to Learn)이라는 제목의 연구는 미국 내 10개 겸상 적혈구 센터가 협력하여 표적 검사의 에뮬레이션으로 알려진 혁신적인 관찰 연구 방법을 활용합니다. 이와 같이 겸상 적혈구증과 관련된 혁신적이고 효과적인 치료법을 개발하기 위한 연구활동을 강화하기 위한 노력이 증가하고 있는 것으로, 이 나라 시장 개척을 촉진할 것으로 예상됩니다.

이와 같이 겸상 적혈구증 유병률 상승, 연구개발 활동 활성화, 정부 대처 등의 요인이 이 지역 시장 성장을 뒷받침할 것으로 예상됩니다.

겸상 적혈구증 치료 산업 개요

겸상 적혈구증 치료 시장은 세분화되어 있으며, 여러 지역 기업과 세계 기업이 존재합니다. 각사는 이 시장에서 신규 치료법의 개발에 임하고 있습니다. 그 중에는 Novartis AG, Emmaus Medical Inc., Sanofi SA, Pfizer, Bluebird bio, Inc. 등이 포함됩니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- 겸상 적혈구증 유병률 증가

- 연구개발 활동 활성화

- 시장 성장 억제요인

- 치료비의 상승

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자 및 소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화

- 치료 모달리티별

- 수혈

- 골수 이식

- 약 요법

- 최종 사용자별

- 병원

- 전문 클리닉

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC 국가

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 기업 프로파일

- Novartis AG

- Emmaus Medical Inc.

- Agios Pharmaceuticals, Inc.

- Medunik USA

- Sarepta Therapeutics

- Sanofi SA

- Bluebird bio, Inc.

- Pfizer Inc.

- Aruvant Sciences Inc.

- Glycomimetics Inc.

- Editas Medicine Inc.

- CRISPR Therapeutics

제7장 시장 기회 및 향후 동향

AJY 25.05.09The Sickle Cell Treatment Market size is estimated at USD 3.69 billion in 2025, and is expected to reach USD 6.79 billion by 2030, at a CAGR of 12.98% during the forecast period (2025-2030).

Factors such as the increasing prevalence of sickle cell disease and the growing R&D activities regarding sickle cell disease are expected to boost the market's growth.

The significant burden of sickle cell disease is expected to boost the need for its treatment and drive market growth. For instance, according to an article published in Frontiers in Hematology in August 2024, sickle cell disease (SCD) is widespread, affecting around 300 thousand newborns annually in sub-Saharan Africa, India, and the Middle East. Additionally, the above-mentioned source reported that about 150 thousand infants are born annually with sickle cell disease in Nigeria alone. Thus, the high prevalence of sickle cell disease is expected to boost the market's growth during the forecast period.

The rising initiatives by various governments and private organizations to treat this disease are expected to drive the market in the coming years. For instance, in June 2024, the World Health Organization (WHO) for the African Region introduced innovative new guidelines to bolster efforts to tackle the increasing burden of sickle cell disease in the region. The SICKLE package was designed to offer a comprehensive and integrated strategy for managing sickle cell disease, facilitating access to essential interventions, promoting education and advocacy, improving the quality of care, and empowering both patients and communities. Thus, increasing government initiatives to enhance the awareness of sickle cell disease treatment are the key market drivers and contribute to market growth.

The increasing R&D activities for developing innovative sickle cell disease treatments may also drive the market. For instance, in October 2024, the Indian Council of Medical Research (ICMR) established a Memorandum of Agreement with Zydus Lifesciences Limited to commence phase-2 clinical trials for Desidustat in individuals with sickle cell disease. The company aims to guarantee that India remains at the forefront of developing innovative and cost-effective healthcare solutions for the treatment of sickle cell disease. Additionally, in June 2024, Vanderbilt University Medical Center (VUMC) researchers highlighted findings from a multicenter, international Phase 2 clinical trial that demonstrated a promising new curative treatment for sickle cell disease (SCD). The therapy, which involves a nonmyeloablative haploidentical bone marrow transplant (BMT) combined with thiotepa and posttransplant cyclophosphamide (PTCy), has shown similar effectiveness and costing only one-fifth of the Food and Drug Administration (FDA) approved myeloablative gene therapy alternatives. Thus, such increasing R&D efforts are likely to bolster the market growth.

Thus, factors such as the rising prevalence of sickle cell disease, the increasing awareness of government initiatives, and the rising R&D activities are expected to boost the market's growth. However, the high cost of treatment is expected to restrain this growth.

Sickle Cell Treatment Market Trends

Blood Transfusion Segment is Expected to Witness Significant Growth Over the Forecast Period

The blood transfusion segment is expected to witness healthy growth over the forecast period. This growth is attributed to the high demand for blood transfusion in sickle cell treatment and the increased prevalence of SCD. Blood transfusions enable the supply of normal red blood cells, which can enhance hemoglobin levels to improve oxygen delivery in the body. Thus, sickle cell blockage in blood vessels and the desire to make more sickle cells are reduced.

The growing need for blood transfusions to treat sickle cell disease is anticipated to contribute significantly to the segment growth. For instance, according to the data updated by the Centers for Disease Control and Prevention (CDC) in May 2024, individuals with sickle cell disease (SCD) may necessitate one or more blood transfusions (receiving healthy blood from a donor) at some point during their lifetime. During a blood transfusion, the patient's blood and the donated blood must have matching antigens or particular proteins on the surface of each red blood cell.

Additionally, the data published by the Canadian Blood Services in June 2023 highlighted that around 15,000 blood units are transfused every year to individuals in Canada who have sickle cell disease. Thus, blood transfusion is significantly adopted by the population affected with sickle disease to reduce its burden, which in turn drives the segment's growth.

Rising R&D for sickle cell disease is also expected to boost the segment's growth. For instance, according to data updated by clinicaltrials.gov, there are around 87 ongoing and active clinical trials for blood transfusion in sickle cell disease as of December 2024. Thus, the large number of clinical trials is expected to boost the adoption of blood transfusion for this treatment.

Thus, factors such as the increasing use of blood transfusion for its management and the rising R&D for sickle cell disease are expected to enhance the segment's growth.

North America is Expected to Hold a Significant Share in the Sickle Cell Treatment Market During the Forecast Period

North America is expected to hold a significant share of the overall sickle cell treatment market, with the United States being the major contributor. The growth in the region is attributed to improving access to sickle cell disease (SCD) treatment and potential pipeline candidates. The strong government support in the United States will further foster the market's development. The rising prevalence of sickle cell disease in the region, the increasing number of clinical trials, and the rising product launches are expected to boost the market's growth in the region.

The substantial burden of sickle cell disease in North American countries is expected to necessitate its treatment, thereby promoting market growth. For instance, according to the data updated by the Centers for Disease Control and Prevention (CDC) in May 2024, sickle cell disease (SCD) affects approximately 100,000 Americans every year, and SCD occurs among about 1 out of every 365 black or African American births. Similarly, according to the data published by the Canadian Blood Services in June 2023, sickle cell disease is Canada's most prevalent hereditary condition, with more than 6,000 individuals affected nationwide in 2023. Thus, the huge burden of sickle cell disease in the region fuels the need for its treatment products and drives the market growth over the forecast period.

The government's increasing initiatives are also expected to boost the market's growth in the region. For instance, in November 2024, the Clinton Health Access Initiative (CHAI) introduced a groundbreaking three-year grant of USD 8 million from Open Philanthropy, an advised fund associated with the Silicon Valley Community Foundation, to enhance initiatives to combat sickle cell disease (SCD). This funding will contribute to improving access to treatment and care for children affected by SCD in the United States.

Moreover, in October 2023, the Mount Sinai Health System awarded a USD 12 million grant from the National Heart, Lung, and Blood Institute to evaluate new treatment alternatives for sickle cell disease and identify the most effective options for individual patients. This research, titled REAL (Registry Expansion Analyses to Learn) Answers, involves collaboration among 10 sickle cell centers in the United States and will utilize an innovative observational study method known as target trial emulation. Thus, increasing initiatives to enhance research activities for developing innovative and effective treatments associated with sickle cell disease is anticipated to drive market growth in the country.

Thus, factors such as the rising prevalence of sickle cell disease, rising R&D activities, and government initiatives are expected to boost the market's growth in the region.

Sickle Cell Treatment Industry Overview

The sickle cell treatment market is fragmented, with the presence of several regional and global companies. Companies are taking initiatives to develop novel therapies in the market studied. Some of the players include Novartis AG, Emmaus Medical Inc., Sanofi SA, Pfizer, and Bluebird bio, Inc., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Prevalence of Sickle Cell Disease

- 4.2.2 Increasing R&D Activity

- 4.3 Market Restraints

- 4.3.1 High Cost of Treatment

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1 By Treatment Modality

- 5.1.1 Blood Transfusion

- 5.1.2 Bone Marrow Transplant

- 5.1.3 Pharmacotherapy

- 5.2 By End-User

- 5.2.1 Hospitals

- 5.2.2 Specialty Clinics

- 5.2.3 Other End-Users

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Novartis AG

- 6.1.2 Emmaus Medical Inc.

- 6.1.3 Agios Pharmaceuticals, Inc.

- 6.1.4 Medunik USA

- 6.1.5 Sarepta Therapeutics

- 6.1.6 Sanofi SA

- 6.1.7 Bluebird bio, Inc.

- 6.1.8 Pfizer Inc.

- 6.1.9 Aruvant Sciences Inc.

- 6.1.10 Glycomimetics Inc.

- 6.1.11 Editas Medicine Inc.

- 6.1.12 CRISPR Therapeutics