|

시장보고서

상품코드

1445785

당뇨병 치료제 : 일본 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2024-2029년)Japan Diabetes Drugs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

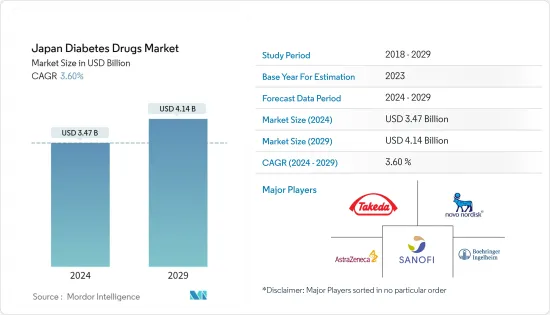

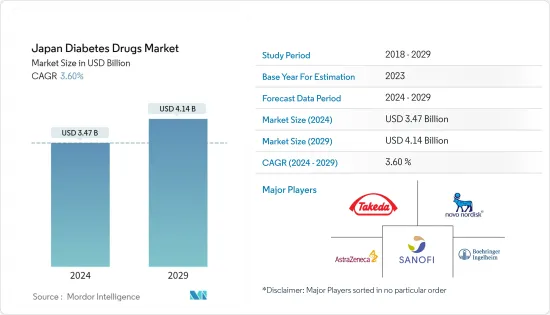

일본의 당뇨병 치료제 시장 규모는 2024년 34억 7,000만 달러로 추정됩니다. 2029년까지 41억 4,000만 달러에 달할 것으로 예측되며, 예측 기간(2024-2029년) 동안 3.60%의 연평균 복합 성장률(CAGR)을 나타낼 것으로 예상됩니다.

코로나19 팬데믹은 당뇨병 치료제 시장에 큰 영향을 미치고 있으며, 코로나19 감염으로 입원한 환자의 당뇨병 유병률과 혈당 조절이 개선되면 SARS-CoV-2 환자의 예후가 개선되고 입원 기간이 단축될 수 있다는 인식 당뇨병 치료 기기의 중요성이 강조되고 있습니다. 미국당뇨병학회(ADA)의 제81회 가상 과학 세션에서 후향적 분석이 발표되어 당뇨병이 일본 코로나19 환자의 중증도 가속화의 주요 위험 요소임을 보여주었습니다.

당뇨병은 코로나19 팬데믹 기간 동안 코로나19의 심각한 위험 요인으로 남아있습니다. 당뇨병과 코로나19를 앓고 있는 입원 환자 10명 중 1명은 입원 후 7일 이내에 사망했습니다.

팬데믹은 또한 의료 제공업체와 당뇨병 환자 간의 가상 상담과 당뇨병 기술 활용을 통해 당뇨병 치료제 제공에 있어 혁신을 지속하고 확대할 수 있는 기회를 부각시켰습니다. 위기 관리로 인해 환자와 의료 서비스 제공업체 모두 원격 의료에 대한 전례 없는 관심이 생겨나면서 수년간의 많은 규제 장벽이 제거되었습니다. 이처럼 코로나19 사태는 일본 당뇨병 치료제 시장의 성장을 가속화했습니다.

1형 당뇨병은 면역 체계의 기능 장애로 인해 발생하는 반면, 2형 당뇨병은 앉아서 생활하는 생활 습관과 관련이 있으며, 그 결과 인슐린에 대한 내재적 저항이 발생하게 됩니다. 따라서 1형 당뇨병은 인슐린 요구성 당뇨병, 2형 당뇨병은 인슐린 의존성 당뇨병으로 구분할 수 있습니다. 일본은 세계에서 가장 많은 노인인구를 보유하고 있으며, 2형 당뇨병에 걸리기 쉬운 나라입니다. 일본은 고령화가 진행되면서 당뇨병 유병률도 증가하고 있습니다. 심혈관 질환, 신장 질환 및 기타 여러 증상과 같은 부작용을 피하기 위해 혈당 모니터링 및 관리가 증가하고 있습니다.

따라서 앞서 언급한 요인으로 인해 조사 대상 시장은 분석 기간 동안 성장할 것으로 예상됩니다.

일본의 당뇨병 치료제 시장 동향

경구용 당뇨병 치료제 부문은 올해 일본 당뇨병 치료제 시장에서 가장 높은 시장 점유율을 차지함

경구용 당뇨병 치료제 부문은 올해 일본 당뇨병 치료제 시장에서 약 69%의 가장 높은 시장 점유율을 차지하고 있습니다.

경구용 항당뇨병제는 전 세계적으로 사용 가능하며, 생활습관 관리와 함께 2형 당뇨병 치료의 단계적 확대가 필요한 경우 사용을 권장하고 있습니다. 경구용 항당뇨병제는 효과, 안전성 및 작용기전이 광범위하기 때문에 일반적으로 제 2형 당뇨병 치료에 가장 먼저 사용되는 약물입니다. 항당뇨병제는 당뇨병 환자의 상태를 조절하고 당뇨병 합병증의 위험을 낮추는 데 도움이 될 수 있습니다. 당뇨병 환자는 혈당을 조절하고 저혈당이나 고혈당을 피하기 위해 평생 동안 항당뇨병제를 복용해야 할 수도 있습니다. 경구용 항 당뇨병 약물은 관리가 쉽고 비용이 저렴하다는 장점이 있습니다. 따라서 인슐린을 대체할 수 있는 매력적인 대안이 되어 치료 순응도를 높일 수 있습니다.

일본에서는 모든 연령층에서 당뇨병 유병률이 증가하고 있으며, 이는 비만 인구 증가, 건강에 해로운 식습관, 앉아서 생활하는 생활습관 등이 원인으로 추정됩니다. 당뇨병의 높은 유병률로 인해 당뇨병은 의료 기관, 개인 및 정부의 재정적 부담을 증가시키는 것으로 널리 우려되고 있습니다. 일본의 의료 시스템에는 일본 당뇨병 교육 및 관리 협회가 시행하는 여러 가지 질병 관리 프로그램이 포함되어 있습니다. 일본은 당뇨병 공중 보건 정책에서 아시아태평양의 리더 중 하나입니다. 이 나라는 국민들의 인식을 높이고 성인 발병 당뇨병의 가능성을 줄일 수 있는 생활습관 및 식단 조절에 초점을 맞춘 예방 정책을 채택하고 있습니다.

위 요인으로 인해 시장은 앞으로도 계속 성장할 가능성이 있습니다.

나트륨-포도당 공수송체-2(SGLT-2) 억제제 부문은 예측 기간 동안 일본 당뇨병 치료제 시장에서 가장 높은 CAGR을 기록할 것으로 예상

나트륨-포도당 공수송체-2(SGLT-2) 억제제 부문은 예측 기간 동안 일본 당뇨병 치료제 시장에서 약 8%의 가장 높은 CAGR을 기록할 것으로 예상됩니다.

SGLT-2 억제제는 2형 당뇨병 환자의 고혈당 수치를 낮추기 위해 사용되는 의약품의 일종으로, SGLT-2 억제제는 췌장 베타 세포의 기능과 독립적으로 작용하며, SGLT-2 약물은 혈압, 심장 기능, 항염증 작용과 같은 심혈관 위험 요인을 크게 관리합니다. SGLT-2 억제제는 헤모글로빈 A1c 수치를 낮추고 체중 감소를 개선하는 데 효과적입니다. 저혈당증의 위험이 낮고 일반적으로 잘 견딜 수 있습니다.

이 기간 동안 기술 발전이 진행되어 SGLT-2 억제제 및 개발중인 제형에 몇 가지 변경이 이루어졌습니다. IDF 2021 데이터에 따르면 일본에는 약 1,100만 명의 당뇨병 환자가 있으며, 당뇨병은 일본 후생노동성에서 중점 건강관리 대상으로 지정하고 있습니다. 당뇨병은 일본 후생노동성에 의해 중점 건강관리로 지정되어 있으며, 2형 당뇨병의 높은 유병률은 심각한 경제적 부담과 관련이 있습니다. 고혈압, 고지혈증과 같은 동반질환을 앓고 있거나 합병증을 앓고 있는 환자에서 당뇨병의 비용은 증가합니다. 합병증 수가 증가하면 비용도 증가합니다. 일본에서는 의료보험제도가 잘 정비되어 있어 당뇨병에 대한 의료비를 전액 부담하고, 당뇨병 환자는 자유롭게 진찰을 받을 수 있습니다. 이러한 장점으로 인해 일본 시장에서 이러한 제품의 채택이 증가했습니다.

일본의 당뇨병 치료제 산업 개요

일본의 당뇨병 치료제 시장은 적당히 통합되어 있으며, Eli Lilly, Sanofi, Novo Nordisk, AstraZeneca와 같은 대형 업체들이 이 지역에서 존재감을 드러내고 있습니다. 시장의 주요 점유율은 전략에 기반한 M&A를 병행하며 새로운 수익원을 창출하고 기존 수익원을 확대하기 위해 지속적으로 시장에 진입하는 업체들이 차지하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- 시장 성장 억제요인

- Porter의 Five Forces 분석

- 공급 기업의 교섭력

- 소비자의 교섭력

- 신규 진출업체의 위협

- 대체 제품 및 서비스의 위협

- 경쟁 기업간 경쟁도

제5장 시장 세분화

- 인슐린

- 기초 인슐린 또는 지효성 인슐린

- Lantus (Insulin Glargine)

- Levemir (Insulin Detemir)

- Toujeo (Insulin Glargine)

- Tresiba (Insulin Degludec)

- Basaglar (Insulin Glargine)

- 볼루스 또는 속효형 인슐린

- NovoRapid/Novolog (Insulin Aspart)

- Humalog (Insulin Lispro)

- Apidra (Insulin Glulisine)

- 기존 인간 인슐린

- Novolin/Actrapid/Insulatard

- Humulin1`

- Insuman

- 바이오시밀러 인슐린

- Insulin Glargine Biosimilars

- Human Insulin Biosimilars

- 기초 인슐린 또는 지효성 인슐린

- 경구 당뇨병 치료제

- Biguanides

- Metformin

- Alpha-Glucosidase Inhibitors

- Alpha-Glucosidase Inhibitors

- Dopamine D2 receptor agonist

- Bromocriptin

- SGLT-2 inhibitors

- Invokana (Canagliflozin)

- Jardiance (Empagliflozin)

- Farxiga/Forxiga (Dapagliflozin)

- Suglat (Ipragliflozin)

- DPP-4 inhibitors

- Onglyza (Saxagliptin)

- Tradjenta (Linagliptin)

- Vipidia/Nesina(Alogliptin)

- Galvus (Vildagliptin)

- Sulfonylureas

- Sulfonylureas

- Meglitinides

- Meglitinides

- Biguanides

- Non-Insulin Injectable drugs

- GLP-1 receptor agonists

- Victoza (Liraglutide)

- Byetta (Exenatide)

- Bydureon (Exenatide)

- Trulicity (Dulaglutide)

- Lyxumia (Lixisenatide)

- Amylin Analogue

- Symlin (Pramlintide)

- GLP-1 receptor agonists

- Combination drugs

- Insulin combinations

- NovoMix (Biphasic Insulin Aspart)

- Ryzodeg (Insulin Degludec and Insulin Aspart)

- Xultophy (Insulin Degludec and Liraglutide)

- Oral Combinations

- Janumet (Sitagliptin and Metformin)

- Insulin combinations

제6장 시장 지표

- 1형 당뇨병 인구

- 2형 당뇨병 인구

제7장 경쟁 구도

- 기업 개요

- Novo Nordisk A/S

- Takeda

- Pfizer

- Eli Lilly

- Janssen Pharmaceuticals

- Astellas

- Boehringer Ingelheim

- Merck And Co.

- AstraZeneca

- Bristol Myers Squibb

- Novartis

- Sanofi Aventis

- 기업 점유율 분석

- Novo Nordisk A/S

- Sanofi Aventis

- Eli Lilly

- Merck And Co.

- Others

제8장 시장 기회와 향후 동향

LSH 24.03.19The Japan Diabetes Drugs Market size is estimated at USD 3.47 billion in 2024, and is expected to reach USD 4.14 billion by 2029, growing at a CAGR of 3.60% during the forecast period (2024-2029).

The COVID-19 pandemic has had a substantial impact on the diabetes drugs market. The prevalence of diabetes in people hospitalized with COVID-19 infection and the recognition that improved glycemic control might improve outcomes and reduce the length of stay in patients with SARS-CoV-2 have underlined the importance of diabetes care devices. A retrospective analysis was presented at the virtual 81st Scientific Sessions of the American Diabetes Association (ADA) which showed diabetes was the main risk factor for the accelerated advancement to a severe state in Japanese COVID-19 patients.

Throughout the pandemic, diabetes has persisted as a significant risk factor for COVID-19. In hospitalized patients with diabetes and COVID-19, one in 10 people died within seven days of admission.

The pandemic also highlighted opportunities for continuing and expanding innovations in the delivery of diabetes drugs, through virtual consultations between healthcare providers and people with diabetes, and the use of diabetes technology. Crisis management has created unprecedented interest in remote care from both patients and providers and removed many long-standing regulatory barriers. Thus, the COVID-19 outbreak increased the Japanese diabetes drugs market's growth.

While Type 1 diabetes is caused by an immune system malfunction, Type 2 diabetes is linked to leading a sedentary lifestyle, which results in the development of inherent resistance to insulin. Hence, Type 1 diabetes can be characterized as insulin-requiring, while Type 2 diabetes can be characterized as insulin-dependent diabetes. Japan has one of the largest elderly populations in the world which is more susceptible to the onset of type 2 diabetes. As Japan's population continues to age, the prevalence of diabetes increases as well. The monitoring and management of blood glucose levels are on the rise, to avoid negative consequences, such as cardiovascular diseases, kidney disorders, and many other conditions.

Therefore, owing to the aforementioned factors the studied market is anticipated to witness growth over the analysis period.

Japan Diabetes Drugs Market Trends

The oral anti-diabetic drugs segment holds the highest market share in the Japan Diabetes Drugs Market in the current year

The oral anti-diabetic drugs segment holds the highest market share of about 69% in the Japan Diabetes Drugs Market in the current year.

Oral Anti-Diabetic Drugs are available internationally and are recommended for use when escalation of treatment for type 2 diabetes is required along with lifestyle management. Oral agents are typically the first medications used in treating type 2 diabetes due to their wide range of efficacy, safety, and mechanisms of action. Anti-diabetic drugs help diabetes patients control their condition and lower the risk of diabetes complications. People with diabetes may need to take anti-diabetic drugs for their whole lives to control their blood glucose levels and avoid hypoglycemia and hyperglycemia. Oral anti-diabetic agents present the advantages of easier management and lower cost. So they became an attractive alternative to insulin with better acceptance, which enhances adherence to the treatment.

The prevalence of diabetes is growing among all ages in Japan, which can be attributed to the growing obese population, unhealthy diets, and sedentary lifestyles. Diabetes mellitus is of wide concern with its high prevalence, resulting in increased financial burdens for clinical systems, individuals, and governments. The Japanese healthcare system includes a few disease management programs conducted by the Japan Association for Diabetes Education and Care. Japan is one of the regional leaders in Asia-Pacific in terms of diabetic public health policies. The country promotes public awareness and embraces preventive policies focusing on lifestyle and dietary adjustments, which can lessen the likelihood of adult-onset diabetes.

Owing to the above factors, the market will likely continue to grow.

Sodium-glucose cotransport -2 (SGLT-2) inhibitor segment is expected to register the highest CAGR in the Japan Diabetes Drugs Market over the forecast period

Sodium-glucose cotransport -2 (SGLT-2) inhibitor segment is expected to register the highest CAGR of about 8% in the Japan Diabetes Drugs Market over the forecast period.

SGLT-2 inhibitors, also called gliflozins, are a medicine class used to lower high blood glucose levels in people with type 2 diabetes. SGLT-2 inhibitors act independently of beta-cell function in the pancreas. SGLT-2 drugs significantly manage cardiovascular risk factors, including blood pressure, cardiac function, and antiinflammatory activity.SGLT-2 inhibitors are effective at lowering hemoglobin A1c levels and improving weight loss. They include a low risk of hypoglycemia and are usually well tolerated.

Technological advancements increased over the period leading to several modifications in the SGLT-2 inhibitors or the formulations being developed. Diabetes emerged as a global epidemic. Japan contains around 11 million people with diabetes, according to IDF 2021 data. Diabetes is identified as a healthcare priority by the Ministry of Health, Labour, and Welfare. The high prevalence of type 2 diabetes is associated with a significant economic burden. The costs of diabetes are increased in patients with co-morbidities such as hypertension and hyperlipidemia and in patients who develop complications. Costs increase with an increasing number of complications. Well-organized medical insurance systems cover all medical fees for diabetes mellitus, and people with diabetes can visit doctors freely in Japan. Such advantages helped the increased adoption of these products in the Japanese market.

Japan Diabetes Drugs Industry Overview

The Japan Diabetes Drugs Market is moderately consolidated, with major manufacturers, namely Eli Lilly, Sanofi, Novo Nordisk, AstraZeneca, and other generic players, holding a presence in the region. A major share of the market is held by manufacturers concomitant with strategy-based M&A operations and constantly entering the market to generate new revenue streams and boost existing ones.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Insulins

- 5.1.1 Basal or Long Acting Insulins

- 5.1.1.1 Lantus (Insulin Glargine)

- 5.1.1.2 Levemir (Insulin Detemir)

- 5.1.1.3 Toujeo (Insulin Glargine)

- 5.1.1.4 Tresiba (Insulin Degludec)

- 5.1.1.5 Basaglar (Insulin Glargine)

- 5.1.2 Bolus or Fast Acting Insulins

- 5.1.2.1 NovoRapid/Novolog (Insulin Aspart)

- 5.1.2.2 Humalog (Insulin Lispro)

- 5.1.2.3 Apidra (Insulin Glulisine)

- 5.1.3 Traditional Human Insulins

- 5.1.3.1 Novolin/Actrapid/Insulatard

- 5.1.3.2 Humulin

- 5.1.3.3 Insuman

- 5.1.4 Biosimilar Insulins

- 5.1.4.1 Insulin Glargine Biosimilars

- 5.1.4.2 Human Insulin Biosimilars

- 5.1.1 Basal or Long Acting Insulins

- 5.2 Oral Anti-diabetic drugs

- 5.2.1 Biguanides

- 5.2.1.1 Metformin

- 5.2.2 Alpha-Glucosidase Inhibitors

- 5.2.2.1 Alpha-Glucosidase Inhibitors

- 5.2.3 Dopamine D2 receptor agonist

- 5.2.3.1 Bromocriptin

- 5.2.4 SGLT-2 inhibitors

- 5.2.4.1 Invokana (Canagliflozin)

- 5.2.4.2 Jardiance (Empagliflozin)

- 5.2.4.3 Farxiga/Forxiga (Dapagliflozin)

- 5.2.4.4 Suglat (Ipragliflozin)

- 5.2.5 DPP-4 inhibitors

- 5.2.5.1 Onglyza (Saxagliptin)

- 5.2.5.2 Tradjenta (Linagliptin)

- 5.2.5.3 Vipidia/Nesina(Alogliptin)

- 5.2.5.4 Galvus (Vildagliptin)

- 5.2.6 Sulfonylureas

- 5.2.6.1 Sulfonylureas

- 5.2.7 Meglitinides

- 5.2.7.1 Meglitinides

- 5.2.1 Biguanides

- 5.3 Non-Insulin Injectable drugs

- 5.3.1 GLP-1 receptor agonists

- 5.3.1.1 Victoza (Liraglutide)

- 5.3.1.2 Byetta (Exenatide)

- 5.3.1.3 Bydureon (Exenatide)

- 5.3.1.4 Trulicity (Dulaglutide)

- 5.3.1.5 Lyxumia (Lixisenatide)

- 5.3.2 Amylin Analogue

- 5.3.2.1 Symlin (Pramlintide)

- 5.3.1 GLP-1 receptor agonists

- 5.4 Combination drugs

- 5.4.1 Insulin combinations

- 5.4.1.1 NovoMix (Biphasic Insulin Aspart)

- 5.4.1.2 Ryzodeg (Insulin Degludec and Insulin Aspart)

- 5.4.1.3 Xultophy (Insulin Degludec and Liraglutide)

- 5.4.2 Oral Combinations

- 5.4.2.1 Janumet (Sitagliptin and Metformin)

- 5.4.1 Insulin combinations

6 MARKET INDICATORS

- 6.1 Type-1 Diabetic Population

- 6.2 Type-2 Diabetic Population

7 COMPETITIVE LANDSCAPE

- 7.1 COMPANY PROFILES

- 7.1.1 Novo Nordisk A/S

- 7.1.2 Takeda

- 7.1.3 Pfizer

- 7.1.4 Eli Lilly

- 7.1.5 Janssen Pharmaceuticals

- 7.1.6 Astellas

- 7.1.7 Boehringer Ingelheim

- 7.1.8 Merck And Co.

- 7.1.9 AstraZeneca

- 7.1.10 Bristol Myers Squibb

- 7.1.11 Novartis

- 7.1.12 Sanofi Aventis

- 7.2 COMPANY SHARE ANALYSIS

- 7.2.1 Novo Nordisk A/S

- 7.2.2 Sanofi Aventis

- 7.2.3 Eli Lilly

- 7.2.4 Merck And Co.

- 7.2.5 Others