|

시장보고서

상품코드

1910722

액체 지붕재 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Liquid Roofing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

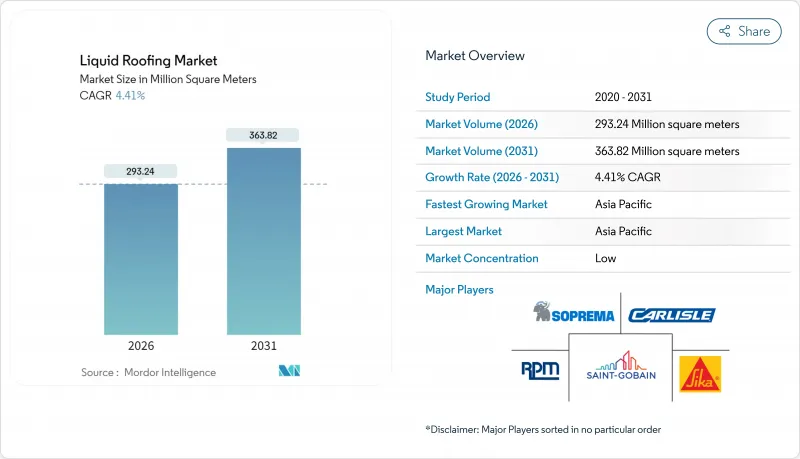

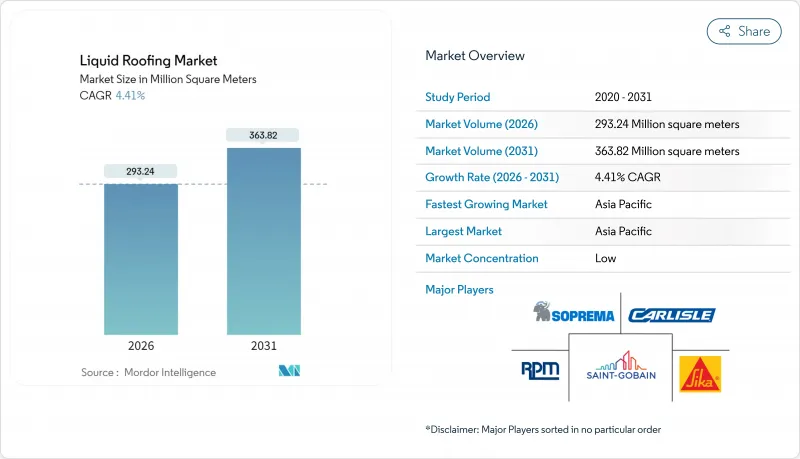

액체 지붕재 시장은 2025년 2억 8,085만 평방미터에서 2026년에는 2억 9,324만 평방미터로 성장하고, 2026년에서 2031년에 걸쳐 CAGR 4.41%로 성장을 지속하여 2031년까지 3억 6,382만 평방미터에 이를 것으로 예측되고 있습니다.

급속한 인프라 근대화, 빈발하는 폭풍우, 보다 엄격한 에너지 기준에 의해 지붕의 교체 사이클이 단축되어, 현장 경화형 이음매 없는 코팅재에 대한 사양 선택이 촉진되고 있습니다. 시공업자는 절단이나 용접을 필요로 하지 않고 관통부를 감싸는 액체 시스템을 선호하여 도입하고 있으며, 이로써 누수 리스크와 현장 폐기물이 저감됩니다. 휘발성 유기화합물(VOC)의 허용치를 강화하는 규제의 움직임은 수성화학제품을 더욱 유리하게 하고, 한편 쿨루프에 대한 정부의 우대조치는 고온지역과 온난지역에서의 도입을 촉진하고 있습니다. 동시에 프라이빗 에퀴티에 의한 인수의 물결이 유통망을 재구축하고 있어 입찰 결정에서 공급의 확실성이 가격과 동등한 중요성을 띠고 있습니다.

세계의 액체 지붕재 시장의 동향 및 인사이트

기후 변화에 따른 비정상적인 기상을 배경으로 지붕 개보수 수요 급증

강풍, 우박, 강수량의 격화로 인해 건물 소유자는 보증 기간 만료 전에 노후화된 지붕의 개보수를 요구받고 있습니다. 액체 시스템은 습윤 환경 하에서도 경화되어 토치 용접이나 용제 용접을 필요로 하지 않고 미세한 균열을 보수할 수 있는 점에서 우수합니다. 카테고리 4 폭풍우 후에는 계약자에게 수개월 분의 수주가 적체되므로 보험사는 미래 보험금 청구를 경감하는 원활한 코팅(연속막)을 우선시합니다. 지자체의 부흥 자금은 특히 허리케인 다발 지역에 있는 학교나 의료시설을 대상으로 하는 공공 지붕 개보수 프로그램을 가속화하고 있습니다. 기존의 기재에 액체 제품을 스프레이 또는 롤러로 도포할 수 있는 특성은 매립 처분 비용의 절감으로 이어져 폭풍우 피해를 입은 구조물의 조기 재이용을 촉진합니다.

현장 다운타임을 단축하는 속경화 폴리우레아 및 하이브리드 시스템

순수한 폴리우레아 멤브레인은 단 30초 만에 완전 경화를 달성하여 당일 보행 및 신속한 기계설비 공사 준비를 가능하게 합니다. 하이브리드 아크릴 폴리우레탄계 화학 조성은 낮은 비용과 건조 가속을 양립하여 시공업자는 비수기에 일일 생산 프레임의 확대를 실현합니다. 시설 관리자는 영업을 중단하지 않고 소매점 지붕을 복구할 수 있는 옵션을 높이 평가합니다. 조기 도입 사례로는 가동 중단이 직접적인 처리 능력 손실로 이어지는 물류 창고와 지속적인 환경 제어가 필요한 데이터센터가 있습니다. 경화 프로파일이 개선됨에 따라 설계자는 엄격한 일정이 부과된 중요한 공정 프로젝트에서도 액체 재료의 도입에 확신을 갖게 되었습니다.

휘발성 이소시아네이트와 아스팔트 가격 상승이 계약자의 이익률을 압박

폴리우레탄 액체 시스템은 MDI나 HDI 등의 이소시아네이트 단량체에 의존하고 있지만, 2024년에 유럽 공장의 유지보수 정지에 따라 그 가격이 15-20% 급등했습니다. 중소규모의 지붕 공업자는 발주가 스팟 가격으로 전환되면서 자금 조달에 어려움을 겪었습니다. 이 가격 변동은 석유화학 파생품을 사용하지 않는 수성 아크릴계 또는 실리콘계에 대한 대안을 가속화하고 있습니다. 대량 주문 계약을 맺은 계약자는 원재료로 거슬러 올라가는 공급업체를 통해 비용 변동을 헤지하고 있습니다. 선도적인 OEM 제조업체는 추가 요금의 전가가 용이하기 때문에 경쟁 격차가 확대되고 추가적인 산업 재편이 진행되고 있습니다.

부문 분석

아크릴계 도료는 2025년 수요의 51.47%를 차지하였으며 VOC 규제와 쿨루프 기준에 대한 적합성이 높이 평가되었습니다. 폴리머의 지속적인 개량에 의한 인장 강도와 내수 축적성의 향상에 의해 2031년까지 연평균 복합 성장률(CAGR) 4.74%가 전망됩니다. 아크릴계 액체 지붕재 시장의 규모는 폭넓은 기초재와의 적합성에 의해 뒷받침되고 있어 시공업자는 노후화한 단층 방수 시트를 철거하지 않고도 재도장이 가능합니다. 폴리우레탄계 시스템은 뛰어난 내마모성이 요구되는 화학처리시설이나 냉장시설에 있어서 여전히 필수적이지만 높은 가격감응도가 확대를 억제하고 있습니다. 실리콘계 제품은 연간 자외선 노출 일수가 300일이 넘는 사막 기후 지역에서 기반을 확대하고 있습니다.

아크릴계 제품의 도입은 청소의 용이함과 낮은 설비 투자로부터도 혜택을 받고 있으며 롤러나 에어리스 스프레이 장치를 갖춘 소규모 시공업자도 시장 진입이 가능해집니다. 수성 기술로의 규제 전환으로 솔벤트 기반 아스팔트 제품의 시장 침식이 가속화되고 있습니다. 에폭시 수지 및 PMMA(폴리메틸메타크릴레이트)와 같은 틈새 솔루션은 석재 및 역사적 기재에 대한 접착성이 비용을 초과하는 중공업 분야 및 역사적 건축물 분야에서 활용되고 있습니다. 전체적으로 향후 시행될 마이크로플라스틱 배출규제에 적합한 화학제품이 미래 점유율을 획득할 전망입니다.

액체 지붕재 보고서는 유형별(폴리우레탄 코팅, 아크릴 코팅, 아스팔트계 코팅, 실리콘 코팅 등), 용도별(돔 지붕, 경사지붕, 평지붕), 최종 사용자 산업별(주택, 상업, 산업 및 공공시설, 인프라), 지역별(아시아태평양, 북미, 유럽 등)으로 분류됩니다. 시장 예측은 수량(제곱미터) 기준으로 제공됩니다.

지역별 분석

아시아태평양은 2025년 세계 시장의 41.18%를 차지하였으며 2031년까지 연평균 복합 성장률(CAGR) 4.82%로 확대될 것으로 전망됩니다. 이는 현장 경화 방수 시트를 선호하는 철도, 공항 및 데이터센터 파이프라인에 의해 지원됩니다. 중국에서는 지방 도시의 개보수 보조금에 의해 노후화한 주택단지의 방수 개보수가 추진되고, 인도에서는 스마트 시티 입찰에 지붕 냉각 시스템이 통합되고 있습니다. ASEAN 국가에서는 정부-민간 연계에 의해 학교 및 진료소에서 액체 사양을 추진하여 유지 관리 예산의 절감을 도모하고 있습니다. 인도네시아와 베트남에서는 지역에 혼합 플랜트를 보유한 공급업체가 국경을 넘어 물류상의 마찰을 줄이고 현지 조달 규제를 충족합니다.

북미 시장은 2005년부터 2010년에 건설된 소매 대형 상점과 창고 지붕의 교체 주기에 의해 여전히 중요한 시장입니다. 인프라 투자 및 고용법에 의해 교통 거점이나 수처리 시설에 자금이 투입되어 부속 건물에 액체 방수가 도입되고 있습니다. 콜로라도 등의 주에서는 에너지 기준의 개정에 의해 캘리포니아의 반사율 기준이 도입되어 아크릴계 백색 지붕에 대한 수요가 자극되고 있습니다. 텍사스주와 오클라호마주에서는 격렬한 우박의 발생에 의해 내충격성 폴리우레탄 엘라스토머를 이용한 지붕의 교체가 가속하고 있습니다.

유럽에서는 고휘발성 유기화합물(VOC) 함유 재료의 단계적 폐지에 의한 환경규제 준수를 중시하고 있으며, 쿨루프 도입에 대해 고정자산세 공제에 의한 우대조치를 강구하고 있습니다. 독일에서 제안되고 있는 그린 자극책에서는 공공 건축물의 개보수가 우선시되어, 역사적 슬레이트 지붕의 외관을 손상시키지 않고 실리콘계 탑 코트를 시공하는 기회가 태어나고 있습니다. 영국에서는 '미래 주택 기준'의 실현을 향해, 여름철의 과열을 억제하는 반사성 방수 시트의 도입을 건설업자에게 촉구하고 있습니다. 남유럽의 호스피탈리티 리조트에서는 비수기에 실시되는 방수 도장 공사 도중에 숙박객의 이동을 피하기 위해 액체 방수재의 도입이 지정되어 있습니다.

기타 혜택

- 시장 예측(ME) 엑셀 시트

- 3개월 애널리스트 서포트

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 촉진요인

- 기후 변화에 의한 이상 기상을 배경으로 한 지붕 개보수 수요의 급증

- 속경화 폴리우레아 및 하이브리드 시스템에 의한 현장의 다운타임 감소

- 미국 및 EU에서의 차열 및 반사 지붕에 대한 세제 우대 조치

- 아시아태평양의 주요 도시에서의 인프라 자극책

- 드론을 활용한 스프레이식 시공에 의한 노동 생산성 향상

- 억제요인

- 이소시아네이트 및 아스팔트 가격의 변동이 계약자의 이익률을 압박

- 고휘발성 유기 화합물(VOC) 제품에 대한 지역적 금지 조치

- 신흥 경제국에서의 숙련 시공자 부족

- 밸류체인 분석

- Porter's Five Forces

- 공급자의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모 및 성장 예측

- 유형별

- 폴리우레탄 코팅

- 아크릴 코팅

- 아스팔트계 코팅

- 실리콘 코팅

- 에폭시 수지 코팅

- 기타 유형

- 용도별

- 돔형 지붕

- 경사지붕

- 평지붕

- 최종 사용자 산업별

- 주택용

- 상업용

- 산업 및 기관

- 인프라

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 말레이시아

- 태국

- 인도네시아

- 베트남

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 북유럽 국가

- 튀르키예

- 러시아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 콜롬비아

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 나이지리아

- 카타르

- 이집트

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율(%) 및 순위 분석

- 기업 프로파일

- 3M

- Akzo Nobel NV

- Alumasc Building Products

- Carlisle Companies Incorporated

- Fosroc, Inc.

- Garland Company, Inc.

- Johns Manville(A Berkshire Hathaway Company)

- Kemper System Ltd

- Langley UK Ltd

- Mapei SpA

- PPG Industries, Inc.

- RPM INTERNATIONAL INC.

- Saint-Gobain

- SIG plc

- Sika AG

- SOPREMA Group

- Standard Industries Inc.

제7장 시장 기회 및 미래 전망

CSM 26.01.28The Liquid Roofing Market is expected to grow from 280.85 million square meters in 2025 to 293.24 million square meters in 2026 and is forecast to reach 363.82 million square meters by 2031 at 4.41% CAGR over 2026-2031.

Rapid infrastructure modernization, more frequent storm events, and stricter energy codes shorten reroofing cycles and shift specification preferences toward seamless coatings that cure in-place. Contractors gravitate to liquid systems that wrap penetrations without cutting or welding, thereby lowering leak liability and jobsite debris. Regulatory moves that tighten volatile organic compound (VOC) thresholds further advantage waterborne chemistries, while government incentives for cool roofs reinforce adoption across hot and temperate zones. A concurrent wave of private-equity-backed rollups reshapes distribution reach, putting supply certainty on par with price in bid decisions.

Global Liquid Roofing Market Trends and Insights

Surging Reroofing Demand Amid Climate-Induced Extreme Weather

Escalating wind, hail, and precipitation intensities push building owners to upgrade aging roofs before warranty expiry. Liquid systems excel because they cure under damp conditions and bridge minor cracks without torching or solvent welding. Contractors report multi-month backlogs after Category 4 storms, and insurers prioritize seamless coatings that mitigate future claims through continuous membranes. Municipal recovery funds accelerate public reroofing programs, especially for schools and healthcare facilities located in hurricane corridors. The ability to spray or roll liquid products over existing substrates limits landfill fees and promotes faster re-occupancy of storm-damaged structures.

Fast-Curing Polyurea and Hybrid Systems Reducing Site Downtime

Pure polyurea membranes now reach full cure in as little as 30 seconds, enabling same-day foot traffic and rapid staging for mechanical trades. Hybrid acrylic-polyurethane chemistries combine lower cost with accelerated drying, allowing applicators to widen daily production windows during shoulder seasons. Facility managers value the option to restore roofs over occupied retail space without suspending operations. Early adopters include logistics warehouses where downtime translates directly into lost throughput, and data centers that require continuous environmental control. As cure profiles improve, specifiers gain confidence in deploying liquids on critical-path projects with tight schedules.

Volatile Isocyanate and Bitumen Prices Squeezing Contractor Margins

Polyurethane liquid systems rely on isocyanate monomers such as MDI and HDI whose prices spiked 15-20% in 2024 during maintenance shutdowns at European plants. Small and mid-sized roofing firms faced cash-flow stress as purchase orders shifted to spot pricing. The volatility accelerates substitution toward waterborne acrylics and silicones that sidestep petrochemical derivatives. Contractors with volume commitments hedge cost swings via integrated suppliers that backward-integrate into raw materials. Larger OEMs pass through surcharges more easily, widening the competitive gap and encouraging further consolidation.

Other drivers and restraints analyzed in the detailed report include:

- Tax Incentives for Cool and Reflective Roofs in the United States and European Union

- Infrastructure Stimulus Packages Across APAC Megacities

- Regional Bans on High-VOC Products

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Acrylic coatings accounted for 51.47% of 2025 demand, illustrating their successful alignment with VOC and cool-roof criteria. The segment is projected to post a 4.74% CAGR to 2031 as continuous polymer improvements boost tensile strength and ponding resistance. The liquid roofing market size for acrylics is supported by broad substrate compatibility, allowing contractors to recoat aged single-ply membranes rather than remove them. Polyurethane systems remain essential in chemical processing and cold-storage facilities that require superior abrasion resistance, though price sensitivity curbs expansion. Silicone offerings gain a foothold in desert climates where UV exposure exceeds 300 days annually.

Acrylic adoption also benefits from ease of cleanup and lower equipment investment, enabling small contractors to enter the arena with rollers and airless sprayers. Regulatory migration toward waterborne technology accelerates cannibalization of solvent-based bituminous products. Epoxy and PMMA niche solutions serve heavy-duty industrial or heritage-building sectors where adhesion to masonry or historic substrates outweighs cost. Overall, chemistries able to comply with the upcoming microplastic emission rules will capture future share.

The Liquid Roofing Report is Segmented by Type (Polyurethane Coatings, Acrylic Coatings, Bituminous Coatings, Silicone Coatings, and More), Application (Domed Roofs, Pitched Roof, and Flat Roofed), End-User Industry (Residential, Commercial, Industrial/Institutional, and Infrastructure), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Volume (Square Meters).

Geography Analysis

Asia-Pacific accounted for 41.18% of global coverage in 2025 and is set for a 4.82% CAGR to 2031, supported by rail, airport, and data-center pipelines that prefer onsite-cured membranes. China's Tier-3 city retrofit subsidies target waterproofing upgrades in aging housing blocks, while India integrates roof cooling into Smart City tenders. ASEAN economies push liquid specifications in public-private partnership schools and clinics to cut maintenance budgets. Suppliers with regional blending plants mitigate cross-border logistics frictions and satisfy local content rules in Indonesia and Vietnam.

North America remains a substantial market through replacement cycles in retail big-box and warehouse roofs built between 2005 and 2010. The Infrastructure Investment and Jobs Act channels funding into transit hubs and water treatment facilities that incorporate liquid roofing in ancillary buildings. Energy-code revisions in states such as Colorado adopt California's reflectance thresholds, stimulating acrylic white-roof demand. Severe hail outbreaks in Texas and Oklahoma accelerate reroofing with impact-resistant polyurethane elastomers.

Europe emphasizes environmental compliance by phasing out high-VOC materials and rewarding cool roofs via property tax credits. Germany's proposed green stimulus prioritizes public building retrofits, opening opportunities for silicone topcoats over historic slate roofs without altering appearance. The United Kingdom progresses toward the Future Homes Standard, nudging builders to select reflective membranes that cut summer overheating. Southern European hospitality resorts specify liquid waterproofing to avoid guest relocation during coating work performed in shoulder seasons..

- 3M

- Akzo Nobel N.V.

- Alumasc Building Products

- Carlisle Companies Incorporated

- Fosroc, Inc.

- Garland Company, Inc.

- Johns Manville (A Berkshire Hathaway Company)

- Kemper System Ltd

- Langley UK Ltd

- Mapei S.p.A.

- PPG Industries, Inc.

- RPM INTERNATIONAL INC.

- Saint-Gobain

- SIG plc

- Sika AG

- SOPREMA Group

- Standard Industries Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging reroofing demand amid climate-induced extreme weather

- 4.2.2 Fast-curing polyurea and hybrid systems reducing site downtime

- 4.2.3 Tax incentives for cool/reflective roofs in the US and EU

- 4.2.4 Infrastructure stimulus packages across APAC megacities

- 4.2.5 Drone-enabled spray-on application improving labor productivity

- 4.3 Market Restraints

- 4.3.1 Volatile isocyanate and bitumen prices squeezing contractor margins

- 4.3.2 Regional bans on high-VOC products

- 4.3.3 Skilled-applicator shortage in emerging economies

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Type

- 5.1.1 Polyurethane Coatings

- 5.1.2 Acrylic Coatings

- 5.1.3 Bituminous Coatings

- 5.1.4 Silicone Coatings

- 5.1.5 Epoxy Coatings

- 5.1.6 Other Types

- 5.2 By Application

- 5.2.1 Domed Roofs

- 5.2.2 Pitched Roof

- 5.2.3 Flat Roofed

- 5.3 By End-user Industry

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Industrial/Institutional

- 5.3.4 Infrastructure

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Thailand

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Nordic Countries

- 5.4.3.7 Turkey

- 5.4.3.8 Russia

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Nigeria

- 5.4.5.4 Qatar

- 5.4.5.5 Egypt

- 5.4.5.6 United Arab Emirates

- 5.4.5.7 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Akzo Nobel N.V.

- 6.4.3 Alumasc Building Products

- 6.4.4 Carlisle Companies Incorporated

- 6.4.5 Fosroc, Inc.

- 6.4.6 Garland Company, Inc.

- 6.4.7 Johns Manville (A Berkshire Hathaway Company)

- 6.4.8 Kemper System Ltd

- 6.4.9 Langley UK Ltd

- 6.4.10 Mapei S.p.A.

- 6.4.11 PPG Industries, Inc.

- 6.4.12 RPM INTERNATIONAL INC.

- 6.4.13 Saint-Gobain

- 6.4.14 SIG plc

- 6.4.15 Sika AG

- 6.4.16 SOPREMA Group

- 6.4.17 Standard Industries Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment