|

시장보고서

상품코드

1521312

3D 프린팅용 파우더 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2024-2029년)3D Printing Powder - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

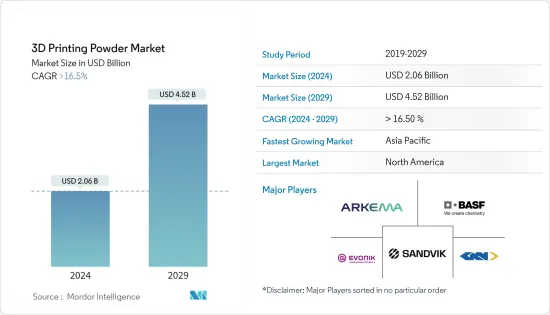

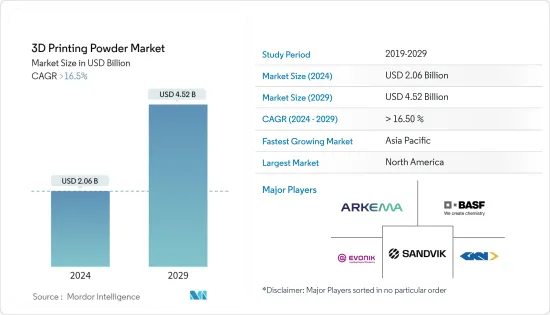

3D 프린팅용 파우더 시장 규모는 2024년 20억 6,000만 달러로 추정되며, 2029년에는 45억 2,000만 달러에 달할 것으로 예상되며, 예측 기간(2024-2029년) 동안 16.5% 이상의 CAGR로 성장할 것으로 예상됩니다.

COVID-19 팬데믹은 3D 프린팅용 파우더 시장에 다양한 영향을 미치고 도전과제를 제시했지만, 혁신과 성장의 기회도 창출했습니다. COVID-19는 헬스케어 등 다양한 산업에서 3D 프린팅의 수용을 가속화하고, 장기적으로 긍정적인 영향을 미칠 것으로 예상됩니다. 기업들이 3D 프린팅 기술과 재료에 투자하여 업무와 회복력을 강화할 것이기 때문입니다.

주요 하이라이트

- 팬데믹으로 인해 의료용 3D 프린팅 파우더에 대한 수요가 급증하고 있습니다. 의료기기 시제품 제작, 개인보호구(PPE) 제조 등 의료용 파우더 시장의 큰 원동력이 되고 있습니다.

- 3D 프린팅의 혁신적 잠재력에도 불구하고, 3D 프린팅용 파우더의 높은 재료비와 후처리 비용으로 인해 이 기술의 보급이 저해되고 있습니다.

- 한 번의 공정으로 여러 재료를 사용해 인쇄할 수 있게 되면서 보다 복잡한 구조와 기능을 가진 제품을 만들 수 있게 되면서 많은 지지를 받고 있습니다. 멀티 머티리얼 프린팅 공정에 대응하는 3D 프린팅 파우더에 비즈니스 기회를 가져다 줄 것으로 보입니다.

- 아시아태평양이 3D 프린팅용 파우더 시장을 독점하고 있으며, 중국, 인도, 일본이 시장 수요에 크게 기여하고 있습니다.

3D 프린팅용 파우더 시장 동향

자동차 산업의 수요 확대

- 자동차 산업은 이 기술을 사용하는 주요 산업으로, 최종사용자 산업 부문에서 큰 비중을 차지하고 있습니다. 수년 동안 자동차 산업은 프로토타입 장비 및 소형 맞춤형 제품의 신속한 제조를 위해 이 기술을 광범위하게 채택해 왔습니다. 특히 자동차 및 주문자상표부착생산(OEM) 업체를 위한 경량 부품 제조에 광범위하게 사용되고 있습니다.

- 3D 인쇄용 분말은 적층 성형의 다양한 공정에 사용됩니다. 주로 자동차, 항공우주 및 방위 제품에 사용되며, 3D 프린팅 하드웨어는 우수한 분말의 연속적인 층을 선택적으로 부착하여 물체를 조형합니다.

- 3D 프린팅에는 다양한 재료를 사용하고 다양한 형태의 분말 부착이 일반적으로 사용됩니다. 나일론, 바이오플라스틱, 세라믹, 왁스, 청동, 스테인리스 스틸, 코발트 크롬, 티타늄 등이 있습니다.

- 3D 프린팅용 파우더는 자동차 분야에서 하우징, 브래킷, 터보차저, 타이어 금형, 변속기 플레이트, 제어 밸브 및 펌프 등의 용도가 있습니다. 또한 냉각 통풍구, 차체 패널, 대시보드, 시트 프레임 및 프로토타이핑, 범퍼 및 기타 엔진 부품에 대한 응용도 포함됩니다.

- 또한, 3D 프린팅용 파우더는 차량 경량화 공정에 도움이 되어 차량의 성능과 효율을 향상시키는 데 도움이 될 수 있습니다.

- OICA에 따르면 세계 자동차 산업은 현재 2022년에 2021년 대비 6%의 큰 성장을 이루었고, 2022년에는 중국, 독일, 한국, 캐나다, 영국, 이탈리아를 포함한 전 세계 여러 선진국과 개발도상국에서 자동차 생산이 증가했으며, 2022년에는 8, 502만 대의 자동차가 생산되었습니다. 502만 대 이상의 자동차가 생산될 것입니다.

- 중국의 자동차 제조 산업은 세계 최대 규모이며, 2021년에는 소폭 증가, 2022년에는 3% 증가하여 생산과 판매가 증가하였습니다. 중국자동차공업협회(CAAM)에 따르면 2022년 승용차 생산량은 2021년 대비 11.2% 증가했습니다.

- 래피드 프로토타이핑 시장 개척, 항공우주 분야 수요 확대, 개발도상국에서의 자동차 기술 발전은 향후 몇 년 동안 3D 프린팅용 파우더 시장의 수요를 견인할 것으로 예상됩니다.

시장을 독점하는 아시아태평양

- 아시아태평양은 중국, 한국, 일본, 인도에서 자동차 부문이 고도로 발전하고 있어 세계 시장을 장악할 것으로 예상됩니다. 이는 수년 동안 이 지역에서 의료 및 항공우주 기술을 발전시키기 위한 지속적인 투자와 함께 이루어지고 있습니다.

- 인도자동차산업협회에 따르면 인도 자동차 산업은 2022년 4월부터 2023년 3월까지 승용차, 상용차, 삼륜차, 이륜차, 사륜차 등 총 2,593만 대의 자동차를 생산했으며, 2021년 4월부터 2022년 3월까지 생산량은 2,304만 대였다고 합니다. 이었습니다.

- 3D 프린팅용 파우더는 항공우주 분야의 다양한 부품 제조에 사용할 수 있습니다. 전환 덕트, 엔진 부품, 항공기 랜딩 기어의 로터 블레이드, 스프레이 바, 프레임 홀더, 라이너, 캐리어 링, 내식성 부품 등이 포함됩니다.

- 최근 몇 년 동안 아시아태평양에서 항공우주 부품의 생산 및 조립 기지가 증가함에 따라 가까운 장래에 3D 프린팅 부품 및 분말 소비에 대한 전망이 열릴 것으로 예상됩니다.

- 일반항공산업협회의 발표에 따르면 2022년 피스톤형 항공기 인도량은 2021년 대비 8.2% 증가하여 총 1,524대를 기록했습니다. 터보프롭 항공기는 10.4% 증가한 582대, 비즈니스 제트기는 710대에서 712대로 소폭 증가했으며, 2022년 항공기 납품 총액은 약 229억 달러로 전년 대비 약 5.8% 증가했습니다. 이는 전년 대비 약 5.8%의 성장을 반영합니다.

- 아시아태평양에서는 개발도상국의 의료 기술 성장이 엄청나게 성장하고 있습니다. 치과용 크라운, 보청기, 정형외과용 교체 부품 등 맞춤형 임플란트 수요가 의료 산업의 성장을 뒷받침하고 있습니다.

- 중국, 일본, 한국, 인도의 항공우주 및 방위 분야의 성장은 신흥국의 건축 및 건설 산업을 증가시켰습니다. 의료 분야의 놀라운 성장은 향후 몇 년 동안 3D 프린팅 파우더 시장을 주도할 것으로 예상됩니다.

3D 프린팅용 파우더 산업 개요

3D 프린팅용 분말 시장은 그 특성상 부분적으로 통합되어 있습니다. 주요 기업으로는 Sandvik AB, Arkema, BASF SE, GKN Powder Metallurgy, Evonik Industries AG 등이 있습니다.

기타 혜택:

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 소개

- 조사 성과

- 조사 가정

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 성장 촉진요인

- 항공우주 산업과 자동차 산업의 용도 증가

- 의료 분야에서의 수요 확대

- 기타 촉진요인

- 성장 억제요인

- 높은 재료비와 후 가공비

- 위험한 성질

- 업계 밸류체인 분석

- Porter's Five Forces 분석

- 공급 기업의 교섭력

- 구매자의 교섭력

- 신규 참여업체의 위협

- 대체품의 위협

- 경쟁 정도

제5장 시장 세분화(금액 기준 시장 규모)

- 파우더 유형

- 플라스틱 파우더

- 금속 파우더

- 세라믹 파우더

- 유리 파우더

- 기타 유형(복합 파우더 등)

- 최종 이용 산업

- 자동차

- 항공우주 및 방위

- 의료

- 건축

- 기타 최종 이용 산업(소비재, 산업 등)

- 지역

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카공화국

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 상황

- M&A, 합작투자, 제휴, 협정

- 시장 점유율(%)**/순위 분석

- 주요 기업의 전략

- 기업 개요

- Arkema

- BASF SE

- ERASTEEL

- Evonik Industries AG

- ExOne

- GENERAL ELECTRIC

- GKN Powder Metallurgy

- Hoganas AB

- Metalysis

- Sandvik AB

제7장 시장 기회와 향후 동향

- 건축 분야의 혁신

- 멀티 재료 인쇄에 대한 수요 상승

The 3D Printing Powder Market size is estimated at USD 2.06 billion in 2024, and is expected to reach USD 4.52 billion by 2029, growing at a CAGR of greater than 16.5% during the forecast period (2024-2029).

The COVID-19 pandemic had a mixed impact on the 3D printing powder market, presenting challenges but also creating opportunities for innovation and growth. The pandemic accelerated the acceptance of 3D printing in various industries, such as healthcare, and the long-term impact is expected to be positive. It is because companies invest in 3D printing technologies and materials to enhance their operations and resilience.

Key Highlights

- The pandemic spurred demand for 3D printing powders used in medical applications. It is a major driving factor for this market, such as creating prototypes of medical devices and manufacturing personal protective equipment (PPE).

- Despite the transformative potential of 3D printing, the widespread adoption of this technology is hindered by the high material and post-processing cost of 3D printing powder.

- The ability to print with multiple materials in a single process is gaining traction, allowing the creation of products with more complex structures and functionalities. It will provide an opportunity for 3D printing powders that are compatible with multi-material printing processes.

- The Asia-Pacific region dominated the market for 3D printing powder, with China, India, and Japan being the major contributors to the market demand.

3D Printing Powders Market Trends

Growing Demand from Automobile Sector

- The automotive industry is a primary industry that utilizes this technology, holding a significant share in the end-user industries segment. Over the years, the automotive sector extensively employed this technology for the rapid production of prototype equipment and small custom products. Its widespread use is particularly notable in the manufacturing of lightweight components for both automobiles and Original Equipment Manufacturers (OEMs).

- 3D printing powder is used in different processes in additive manufacturing. It is being majorly used in automobile, aerospace, and defense products. 3D printing hardware builds an object by selectively sticking together successive layers of excellent powder.

- Various forms of powder adhesion are commonly used to 3D print, using a wide range of materials. These include nylon, bio-plastics, ceramics, wax, bronze, stainless steel, cobalt chrome, and titanium.

- 3D printing powder finds applications in the automobile sector in the form of housing and brackets, turbochargers, tire molds, transmission plates, and control valves and pumps. It also includes applications in cooling vents, body panels, dashboards, seat frames and prototyping, bumpers, and other engine components.

- Also, 3D printing powder helps in vehicle weight reduction processes that support increasing the performance and efficiency of the vehicles.

- As per OICA, the Global Automotive Industry is currently growing at a substantial rate of 6% in 2022 over 2021. In 2022, various developed and developing countries across the world, including China, Germany, South Korea, Canada, the United Kingdom, and Italy, experienced an increase in automotive production. In 2022, over 85.02 million units of Motor vehicles were manufactured.

- The Chinese automotive manufacturing industry is the largest in the world. The industry witnessed a slight increase in 2021, with a 3% increase in 2022, wherein production and sales inclined. According to the China Association of Automobile Manufacturers (CAAM), the production of passenger cars increased by 11.2% in 2022 over 2021.

- Increasing applications for rapid prototyping, growing demand for the aerospace sector, and technological advancements in automobiles in developing regions are driving the demand for the 3D printing powder market through the years to come.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific is expected to dominate the global market owing to the highly developed automobile sector in China, Korea, Japan, and India. It is coupled with the continuous investments done in the region to advance medical and aerospace technologies through the years.

- As per the Society of Indian Automobile Manufacturers, the Automotive Industry in India manufactured a combined total of 25.93 million vehicles. The vehicles include passenger vehicles, commercial vehicles, three-wheelers, two-wheelers, and quadricycles during the period from April 2022 to March 2023, in comparison to 23.04 million units produced from April 2021 to March 2022.

- 3D printing powder can be used for manufacturing various components in the aerospace sector. It includes transition ducts, engine components, aircraft landing gear rotor blades, spray bars, flame holders, liners, carrier rings, and corrosion-resistant components.

- The growing production and assembly bases for aerospace components in the Asia-Pacific regions in recent years are expected to provide scope for the consumption of 3D-printed components and powders in the near future.

- As per the General Aviation Manufacturers Association, there was an 8.2% rise in piston airplane deliveries in 2022 compared to 2021, totaling 1,524 units. Turboprop airplane deliveries increased by 10.4%, reaching 582 units, while business jet deliveries experienced a marginal increase from 710 to 712 units. The total value of airplane deliveries in 2022 amounted to approximately USD 22.9 billion. It reflected a growth of around 5.8% over the previous year.

- In Asia-Pacific, the growth in medical technology in developing countries is immense. The need for customized implants like tooth crowns, hearing aids, and orthopedic replacement parts is supporting the expansion of the medical industry.

- The growth in aerospace and defense sectors in China, Japan, Korea, and India increased the architectural and construction industries in developing countries. The tremendous growth in the medical sector is expected to drive the market for 3D printing powder through the years to come.

3D Printing Powders Industry Overview

The 3D printing powder market is partially consolidated in nature. The major players (not in any particular order) include Sandvik AB, Arkema, BASF SE, GKN Powder Metallurgy, and Evonik Industries AG, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Applications in Aerospace and Automobile Industries

- 4.1.2 Growing Demand from Medical Sector

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 HIgh Material and Post Processing Cost

- 4.2.2 Hazardous in Nature

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Powder Type

- 5.1.1 Plastic Powder

- 5.1.2 Metal Powder

- 5.1.3 Ceramic Powder

- 5.1.4 Glass Powder

- 5.1.5 Other Types (Composite Powder, etc.)

- 5.2 End-user Industry

- 5.2.1 Automotive

- 5.2.2 Aerospace and Defense

- 5.2.3 Medical

- 5.2.4 Architecture

- 5.2.5 Other End-user Industries (Consumer Goods, Industrial, etc.)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Arkema

- 6.4.2 BASF SE

- 6.4.3 ERASTEEL

- 6.4.4 Evonik Industries AG

- 6.4.5 ExOne

- 6.4.6 GENERAL ELECTRIC

- 6.4.7 GKN Powder Metallurgy

- 6.4.8 Hoganas AB

- 6.4.9 Metalysis

- 6.4.10 Sandvik AB

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Innovations in Architectural Sector

- 7.2 Increasing Demand for Multi-Material Printing