|

시장보고서

상품코드

1521327

수은 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2024-2029년)Mercury - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

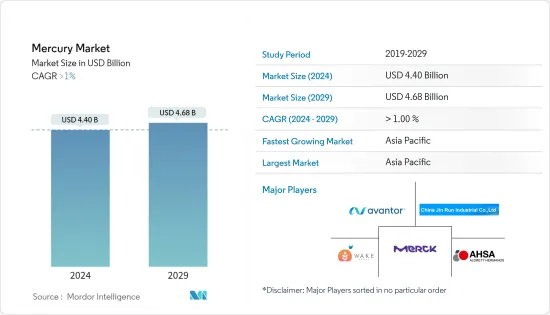

수은 시장 규모는 2024년 44억 달러로 추정되며, 2029년에는 46억 8,000만 달러에 달할 것으로 예상되며, 예측 기간(2024-2029년) 동안 1% 이상의 CAGR을 기록할 것으로 예상됩니다.

COVID-19는 수은 시장에 다양한 영향을 미쳤습니다. 한편으로는 경제 활동 감소로 인해 제조업, 건설업 등 일부 산업에서 수은에 대한 수요가 감소했습니다. 다른 한편으로는 정부와 기업이 제품과 환경에 수은 오염이 없는지 확인하기 위해 수은 검사 서비스에 대한 수요를 증가시켰습니다. 전반적으로 COVID-19가 수은 시장에 미치는 영향은 상대적으로 작을 것으로 예상됩니다.

조사 대상 시장을 주도하는 주요 요인은 측정 및 제어 장비에 대한 수요입니다.

수은의 위험한 특성은 시장 성장 억제요인으로 작용할 가능성이 높습니다. 수은의 위험한 특성으로 인해 많은 국가에서 수은이 함유된 배터리, 온도계, 기압계, 혈압계를 금지하고 있으며, 이는 조사 대상 시장에 영향을 미치고 있습니다.

수은 시장은 화학 공정의 촉매, 특정 의료기기 등 아직 대체품이 없는 특정 틈새 응용 분야에서의 수요 증가로 인해 성장하고 있습니다.

아시아태평양이 세계 시장의 대부분을 차지하고 중국과 타지키스탄의 수요가 대부분을 차지할 것으로 예상됩니다.

수은시장 동향

측정 및 제어 장비가 가장 큰 부문으로 부상

- 수은은 온도계, 자동차 부품, 온도 조절기 프로브, 기압계, 기압계, 진공계, 화염 센서, 유량계, 비중계, 습도계/건습계, 압력계, 고온계, 의료기기 등 다양한 기기에 사용됩니다.

- 수은은 혈압을 측정하는 혈압계에 대규모로 사용됩니다. 또한 혈압 측정은 다양한 임상 상태를 진단하고 모니터링하는 데 중요한 역할을 합니다. 전통적으로 혈압은 혈압계를 사용하여 비침습적으로 측정되어 왔습니다. 이는 여전히 혈압 측정의 '골드 스탠다드'로 인식되고 있습니다.

- 2022년 전 세계적으로 약 2,200톤의 수은이 생산된 것으로 추산됩니다. 수은은 주로 전기 및 전자 제품과 산업용 화학제품 제조에 사용됩니다.

- 그러나 수은에 대한 환경 문제로 인해 유럽 일부 국가에서는 수은을 금지하고 있으며, 영국에서는 현재 의료용 수은 공급이 제한되고 있습니다. 수은은 세계보건기구(WHO)에 의해 공중보건에 심각한 우려를 초래하는 10대 화학제품 또는 화학제품군 중 하나로 간주되고 있습니다.

아시아태평양이 시장을 지배

- 수은의 가장 큰 시장은 아시아태평양입니다. 아시아태평양에서는 중국과 키르기스스탄이 수은의 주요 생산국입니다. 이 외에도 중국은 세계 최대의 수은 광산 생산량과 매장량을 보유하고 있습니다. 또한 중국에서는 수은 화합물이 석탄을 원료로 한 염화비닐 모노머 생산의 촉매로 사용되었습니다.

- 따라서 중국은 2022년 세계 최대 수은 생산국이 될 것이며, 광산 생산량은 2,000톤에 달할 것입니다. 2위 수은 생산국 타지키스탄의 같은 해 생산량은 약 120톤입니다.

- 전 세계적으로 1,000만-2,000만 명이 장인적 소규모 금 채굴(ASGM) 부문에서 일하고 있으며, 이들 중 상당수가 일상적으로 수은을 사용하고 있습니다.

- 장인 소규모 금 채굴(ASGM)은 전 세계 인위적 수은 배출의 가장 큰 원인(37.7%)이며, 석탄의 고정식 연소(21%)가 그 뒤를 잇습니다.

- USGS에 따르면 중국, 키르기스스탄, 멕시코, 페루, 러시아, 슬로베니아, 스페인, 우크라이나는 전 세계 수은 자원의 대부분인 약 60만 톤을 보유하고 있습니다.

- 또한, 장인 소규모 금광(ASGM)은 아시아, 남미, 아프리카 55개국 이상에서 광범위하게 운영되고 있으며, ASGM은 이들 국가에 미시경제의 원천으로 작용하고 있지만, ASGM은 환경과 건강에 악영향을 미치고 있습니다.

- 중국에서는 치과용 아말감의 사용은 서기 1000년으로 거슬러 올라갑니다. 오늘날 치과용 아말감은 수은과은, 주석 및 구리의 금속 합금으로 구성됩니다.

- 앞서 언급한 모든 요인은 이 지역의 수은 소비를 증가시킬 것으로 예상됩니다.

수은 산업 개요

수은 시장은 부분적으로 단편화되어 있습니다. 주요 업체로는 Avantor Inc.(Thermo Fisher Scientific), AHSA, Aldrett Hermanos SA de CV, Merck KGaA, Wake Group, China Jin Run Industrial 등이 있습니다.

기타 혜택:

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 소개

- 조사 가정

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 성장 촉진요인

- 측정·제어 기기의 수요

- 혈압 측정용 혈압계 수요

- 광업 분야에서 금 추출에 널리 사용

- 성장 억제요인

- 수은의 위험한 특성

- 기타 제약

- 산업 밸류체인 분석

- Porter's Five Forces 분석

- 신규 참여업체의 위협

- 구매자의 교섭력

- 공급 기업의 교섭력

- 대체품의 위협

- 경쟁 정도

제5장 시장 세분화(금액 기준 시장 규모)

- 제품 유형

- 금속

- 합금

- 화합물

- 용도

- 배터리

- 치과 용도

- 측정·제어장치

- 램프

- 전기 및 전자기기

- 금 가공

- 기타 용도(헬스케어, 의약품, 배터리)

- 지역

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 말레이시아

- 태국

- 인도네시아

- 베트남

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 노르딕

- 터키

- 러시아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 콜롬비아

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카공화국

- 나이지리아

- 카타르

- 이집트

- 아랍에미리트

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 상황

- M&A, 합작투자, 제휴, 협정

- 시장 점유율/순위 분석

- 주요 기업의 전략

- 기업 개요

- Aldrett Hermanos

- Antares Chem Private Limited

- Avantor Performance Materials

- Bethlehem Apparatus Co. Inc.

- China Jin Run Industrial Co. Ltd

- Mayasa

- Merck KGaA

- Powder Pack Chem

- Special Metals

- Tamilnadu Engineering Instruments

- Wake Group

제7장 시장 기회와 향후 동향

제8장 틈새 용도에서의 수은 수요 확대

제9장 기타 기회

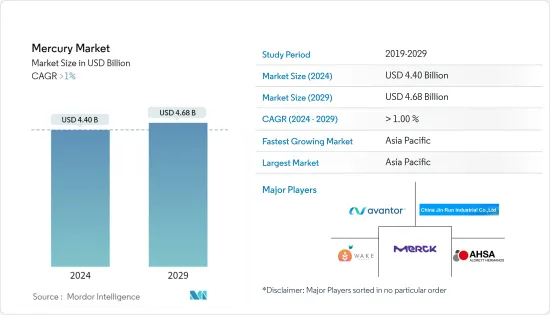

ksm 24.07.31The Mercury Market size is estimated at USD 4.40 billion in 2024, and is expected to reach USD 4.68 billion by 2029, growing at a CAGR of greater than 1% during the forecast period (2024-2029).

The COVID pandemic had a mixed impact on the mercury market. On the one hand, the decline in economic activity led to a decrease in demand for mercury in some industries, such as the manufacturing and construction sectors. On the other hand, the pandemic also led to an increase in demand for mercury testing services, as governments and businesses sought to ensure that their products and environments were free of mercury contamination. Overall, the impact of COVID-19 on the mercury market is expected to be relatively modest.

The major factor driving the market studied is the demand for measuring and controlling devices.

The hazardous properties of mercury are likely to act as a restraint to the growth of the market. Owing to its hazardous nature, many countries have banned mercury-containing batteries, thermometers, barometers, and blood pressure monitors, thus affecting the market studied.

The mercury market is experiencing growth due to increasing demand in specific niche applications, such as catalysts in chemical processes and certain medical devices, where alternatives are not yet available.

Asia-Pacific is expected to dominate the global market, with the majority of the demand coming from China and Tajikistan.

Mercury Market Trends

Measuring and Controlling Devices to be the largest segment

- Mercury is used in various devices such as thermometers, automotive parts, thermostat probes, barometers, vacuum gauges, flame sensors, flowmeters, hydrometers, hygrometers/psychrometers, manometers, pyrometers, medical devices, and more.

- Mercury is used on a large scale in the sphygmomanometer for the measurement of blood pressure. Also, the measurement of blood pressure is important in the diagnosis and monitoring of a wide range of clinical conditions. Traditionally, blood pressure is measured non-invasively using a sphygmomanometer. This is still recognized as the 'gold standard' for the measurement of blood pressure.

- In 2022, an estimated 2,200 metric tons of mercury was produced worldwide. It is mainly used in the manufacturing of electrical and electronic goods and industrial chemicals.

- However, environmental concerns regarding mercury have led to the imposition of bans in some European countries, and the supply of healthcare in the United Kingdom is now restricted. Mercury is considered by the World Health Organisation (WHO) as one of the top 10 chemicals or groups of chemicals of major public health concern.

Asia-Pacific to Dominate the Market

- The Asia-Pacific region is the largest market for mercury. In the Asia-Pacific region, China and Kyrgyzstan are the major producers of mercury. In addition to this, China has the world's largest mine production and reserves of mercury. Also, Mercury compounds were used as catalysts in the coal-based manufacture of vinyl chloride monomers in China.

- Therefore, China is the world's largest producer of mercury in 2022, with a mine production volume of 2,000 metric tons. The second leading producer of mercury, Tajikistan, produced approximately 120 metric tons in the same year.

- Globally, 10-20 million people work in the Artisanal and Small-Scale Gold Mining (ASGM) sector, and many of them use mercury on a daily basis.

- Artisanal and Small-Scale Gold Mining (ASGM) is the largest source of anthropogenic mercury emissions (37.7%) globally, followed by stationary combustion of coal (21%).

- According to USGS, China, Kyrgyzstan, Mexico, Peru, Russia, Slovenia, Spain, and Ukraine have most of the world's estimated 600,000 tons of mercury resources.

- Furthermore, Artisanal Small-Scale Gold Mining (ASGM) has extensive operations spanning over 55 countries across Asia, South America, and Africa. ASGM acts as a microeconomic source for these countries; however, ASGM has adverse environmental and health impacts.

- In China, the use of dental amalgams dates back to 1000 AD; today, dental amalgams consist of mercury and a metal alloy of silver, tin, and copper.

- All the aforementioned factors, in turn, are expected to augment the consumption of mercury in the region.

Mercury Industry Overview

The mercury market is partially fragmented in nature. The major players (not in any particular order) include Avantor Inc. (Thermo Fisher Scientific), AHSA, Aldrett Hermanos SA de CV, Merck KGaA, Wake Group, and China Jin Run Industrial Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Demand from Measuring and Controlling Devices

- 4.1.2 Demand for Sphygmomanometer for the Measurement of Blood Pressure

- 4.1.3 Widely Used in the Mining Sector for the Extraction of Gold

- 4.2 Restraints

- 4.2.1 Hazardous Properties of Mercury

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Product Type

- 5.1.1 Metal

- 5.1.2 Alloy

- 5.1.3 Compounds

- 5.2 Application

- 5.2.1 Batteries

- 5.2.2 Dental Applications

- 5.2.3 Measuring and Controlling Devices

- 5.2.4 Lamps

- 5.2.5 Electrical and Electronics Devices

- 5.2.6 Processing of Gold

- 5.2.7 Other Applications (Healthcare, Pharmaceuticals, and Batteries)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 NORDIC

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.6 Saudi Arabia

- 5.3.7 South Africa

- 5.3.8 Nigeria

- 5.3.9 Qatar

- 5.3.10 Egypt

- 5.3.11 UAE

- 5.3.12 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share/Ranking Analysis**

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Aldrett Hermanos

- 6.4.2 Antares Chem Private Limited

- 6.4.3 Avantor Performance Materials

- 6.4.4 Bethlehem Apparatus Co. Inc.

- 6.4.5 China Jin Run Industrial Co. Ltd

- 6.4.6 Mayasa

- 6.4.7 Merck KGaA

- 6.4.8 Powder Pack Chem

- 6.4.9 Special Metals

- 6.4.10 Tamilnadu Engineering Instruments

- 6.4.11 Wake Group