|

시장보고서

상품코드

1521638

우주용 파워 일렉트로닉스 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2024-2029년)Space Power Electronics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

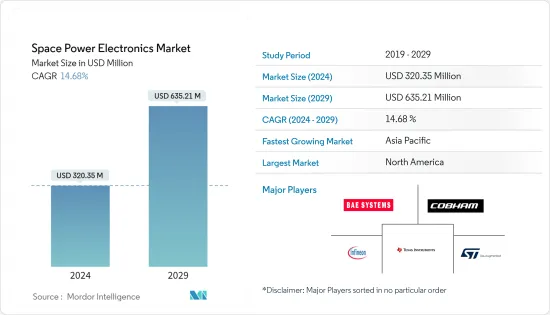

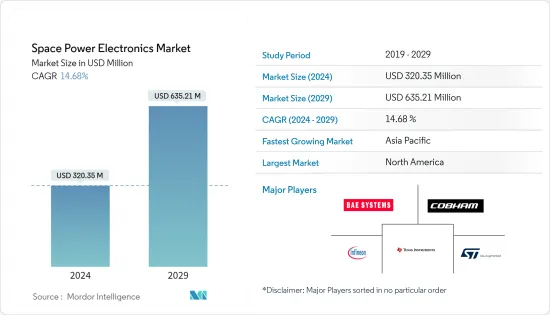

우주용 파워 일렉트로닉스 시장 규모는 2024년 3억 2,035만 달러로 추정되며, 2029년에는 6억 3,521만 달러에 달할 것으로 예상되며, 예측 기간(2024-2029) 동안 연평균 14.68%의 CAGR로 성장할 것으로 예상됩니다.

우주용 파워 일렉트로닉스의 개발은 반도체 기술의 발전과 효율적인 전력 관리 시스템의 필요성에 의해 추진되어 왔습니다. 예를 들어, 광대역 갭 반도체는 기존 재료보다 성능이 향상되어 중요한 기술 혁신으로 등장했습니다. 우주에서의 전력 전자 시스템에는 입출력 전원 포트를 통해 전원과 부하에 연결되는 모듈식 전력 전자 서브시스템(PESS)도 포함됩니다. 이러한 시스템은 위성, 우주선, 로켓, 로버 등의 작동에 필수적이며, 이러한 기능을 수행하는 데 필요한 전력을 보장합니다.

우주용 파워 일렉트로닉스 시장은 저궤도(LEO) 위성과 재사용 로켓의 시장 개척이 증가함에 따라 성장세를 보이고 있습니다. 이러한 발전은 우주 임무의 장기적인 지속가능성과 효율성에 필수적인 고급 전력 관리 장치, 배터리 및 전력 변환기에 대한 수요를 촉진하고 있습니다.

그러나 이러한 복잡한 시스템의 설계 및 개발에 따른 높은 비용과 우주 응용 분야에 필요한 엄격한 통합 및 품질 검사 프로세스와 같은 큰 도전에 직면해 있습니다. 이러한 어려움에도 불구하고, 업계의 연구개발 노력은 이러한 장애요인을 극복하고 예측 기간 동안 상당한 성장세를 보일 것으로 예상됩니다.

우주용 파워 일렉트로닉스 시장 동향

예측 기간 동안 위성이 시장을 독점할 것으로 예상

통신, 내비게이션, 지구관측 등 다양한 용도의 위성 수요가 증가함에 따라 예측 기간 동안 위성 분야가 시장을 주도할 것으로 예상됩니다. 소형 위성 분야는 지난 10년간 급격한 성장세를 보였으며, 기술 발전, 산업 상업화, 민간 자본의 유입이 그 원동력이 되었습니다. 우주 탐사에 대한 관심의 증가와 자세 제어, 궤도 제어, 궤도 이동, 책임감 있는 종말 궤도 이탈 전략과 같은 복잡한 작업을 수행할 수 있는 소형 위성의 필요성이 이러한 성장의 원동력이 되었습니다.

파워 일렉트로닉스의 소형화는 큐브샛의 성능과 신뢰성을 향상시키는 데 특히 유리합니다. 동시에 급성장하는 뉴 스페이스 산업은 모듈화를 채택하고 있으며, 소형화된 방사선 경화 MOSFET, 게이트 촉진제, DC-DC 컨버터, 솔리드 스테이트 릴레이와 같은 구성요소가 표준이 되어 보다 효율적이고 확장 가능하며 비용 효율적인 위성 설계를 위한 추세를 반영하고 있습니다. 을 반영하고 있습니다.

예를 들어, 2023년 1월 에어버스는 벨기에 국방부와 15년간 군에 전술 위성 통신 서비스를 제공하는 계약을 체결했습니다. 에어버스는 2024년까지 다른 유럽 국가와 NATO 동맹국 군대를 위한 새로운 초고주파(UHF) 통신 서비스를 시작할 계획입니다. 이러한 신흥국 시장 개척이 시장 성장을 견인하고 있습니다.

아시아태평양이 예측 기간 동안 가장 높은 CAGR을 기록할 것으로 예상

아시아태평양은 우주 산업, 특히 우주용 파워 일렉트로닉스 분야에서 괄목할 만한 발전을 거듭하고 있습니다. 주요 동향으로는 우주가 국가 안보의 중요한 부분이라는 인식의 증가, 소규모 민간 상업용 우주 스타트업의 부상, 우주 자원 개발에 대한 관심의 전환 등이 있습니다. 중국, 인도, 일본과 같은 국가들은 달 탐사 및 소행성 채굴 기술을 개발하여 우주에서의 입지를 구축하기 위한 야심찬 우주 프로그램을 주도하고 있습니다.

아시아 지역의 위성 통신 장비 시장은 고속 인터넷 연결에 대한 수요 증가로 인해 성장세를 보이고 있습니다. 이러한 성장을 뒷받침하는 것은 싱텔(Singtel)과 타이콤(Thaicom)과 같은 대형 위성 통신 사업자로, 아시아 지역의 유료 위성 TV 가입자가 1억 명을 넘어서는 데 기여하고 있습니다. 예를 들어, 중국은 2023년 12월 지구 저궤도를 이용한 위성 인터넷 콘스텔레이션 '스타링크'의 자국 버전을 구축한다고 발표했으며, 국영기업을 중심으로 전 세계를 커버하는 약 2만 6,000개의 위성을 발사할 계획입니다.

이러한 우주 파워 일렉트로닉스의 발전은 장기 임무와 심우주 탐사에 필수적인 인공위성의 전력 관리에서 보다 효율적이고 신뢰할 수 있는 시스템을 구축할 수 있기 때문에 이러한 발전에 매우 중요합니다.

우주용 파워 일렉트로닉스 산업 개요

우주용 파워 일렉트로닉스 시장은 통합되어 있으며, 주요 기업들이 큰 시장 점유율을 차지하고 있습니다. 이 시장의 주요 업체는 다음과 같습니다. BAE Systems PLC, Cobham Limited, Infineon Technologies AG, Texas Instruments Incorporated, STMicroelectronics NV 등이 있습니다. 극한의 온도와 방사선과 같은 우주에서의 가혹한 조건을 견딜 수 있는 강력한 전자 장치 개발의 선두에 서 있습니다.

시장을 선도하는 업체들은 시장 지위를 유지하기 위해 계약 체결에 더욱 집중하고 있습니다. 이러한 접근 방식은 종종 최첨단 기술을 탑재한 혁신적인 제품 출시로 보완되는 경우가 많습니다. 예를 들어, 2023년 4월 ZF는 STMicroelectronics와 다년간의 실리콘 카바이드 장치 공급 계약을 체결한 바 있습니다. 이 협력은 우주용 전력 및 전자기기 개발에 특화된 R&D 센터를 설립하는 데 도움이 되었으며, 이는 이 첨단 기술 분야의 혁신과 성장에 대한 강한 의지를 보여줍니다.

기타 혜택:

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 소개

- 조사 가정

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- 시장 성장 억제요인

- Porter's Five Forces 분석

- 구매자/소비자의 협상력

- 공급 기업의 교섭력

- 신규 참여업체의 위협

- 대체품의 위협

- 경쟁 기업 간의 경쟁 강도

제5장 시장 세분화

- 플랫폼

- 인공위성

- 우주선과 로켓

- 기타

- 유형

- 내방사선

- 방사선 내성

- 용도

- 통신

- 지구 관측

- 내비게이션, 범지구 위치결정 시스템(GPS), 감시

- 기술 개발·교육

- 기타

- 지역

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 프랑스

- 독일

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 상황

- 벤더 시장 점유율

- 기업 개요

- BAE Systems PLC

- Cobham Limited

- Microchip Technology Inc.

- RUAG Group

- STMicroelectronics NV

- Teledyne Technologies Incorporated

- Texas Instruments Incorporated

- Honeywell International Inc.

- Microsemi Conduction

- ON Semiconductor

- Analog Devices Inc.

- Renesas Electronics Corporation

- Infineon Technologies AG

The Space Power Electronics Market size is estimated at USD 320.35 million in 2024, and is expected to reach USD 635.21 million by 2029, growing at a CAGR of 14.68% during the forecast period (2024-2029).

The development of power electronics for space applications has been driven by advancements in semiconductor technologies and the need for efficient power management systems. Wide bandgap semiconductors, for instance, have emerged as a significant innovation, offering improved performance over traditional materials. Power electronics systems in space also include modular power electronic subsystems (PESS) that connect to a source and load at their input and output power ports. These systems are integral to operating satellites, spacecraft, launch vehicles, and rovers, ensuring they have the necessary power to perform their functions.

The space power electronics market is experiencing growth due to the increasing development of low-Earth orbit (LEO) satellites and reusable launch vehicles. These advancements drive the demand for more sophisticated power management devices, batteries, and power converters, which are essential for the long-term sustainability and efficiency of space missions.

However, the market faces significant challenges, such as the high costs associated with designing and developing these complex systems and the rigorous integration and quality inspection process required for space applications. Despite these challenges, the industry's commitment to research and development is expected to overcome these restraining factors, leading to considerable growth over the forecast period.

Space Power Electronics Market Trends

Satellites are Expected to Dominate the Market During the Forecast Period

The satellite segment is expected to dominate the market during the forecast period owing to the increasing demand for satellites for various applications such as communication, navigation, earth observation, and others. A surge in the small satellite sector was witnessed in the last decade, fueled by significant technological advancements, the commercialization of the industry, and an influx of private capital. This momentum was propelled by increased interest in space exploration and the need for small satellites to perform complex tasks such as attitude and orbit control, orbital transfers, and responsible end-of-life deorbiting strategies.

The miniaturization of power electronics has been particularly beneficial for CubeSats, enhancing their performance and reliability. Concurrently, the burgeoning NewSpace industry is embracing modularization, with components like miniaturized radiation-hardened MOSFETs, gate drivers, DC-DC converters, and solid-state relays becoming standard, reflecting a trend toward more efficient, scalable, and cost-effective satellite designs.

For instance, in January 2023, Airbus signed a contract with the Belgian Ministry of Defense to provide tactical satellite communications services to the armed forces for 15 years. Airbus plans to launch a new ultra-high frequency (UHF) communications service by 2024 for the armed forces of other European nations and NATO allies. Developments such as these are driving the growth of the market.

Asia-Pacific is Expected to Register the Highest CAGR During the Forecast Period

The Asia-Pacific region is witnessing a significant evolution in the space industry, particularly in space power electronics. Key trends include the increasing recognition of space as a vital part of national security, the rise of small private commercial space startups, and a shift in focus toward exploiting space resources. Countries like China, India, and Japan are leading the way with ambitious space programs to establish their presence in space by developing technologies for lunar exploration and asteroid mining.

The satellite communication equipment market in the region is experiencing growth due to the rising demand for high-speed internet connectivity. This growth is supported by major satellite operators such as Singtel and Thaicom, which contribute to the more than 100 million active pay satellite TV subscribers in Asia. For instance, in December 2023, China announced that it would be building its version of StarLink, a satellite internet constellation using low-Earth orbit, with plans to launch around 26,000 satellites to cover the entire world, led by state-run companies.

Thus, the advancements in space power electronics are crucial for these developments, as they enable the creation of more efficient and reliable systems for power management in satellites, which is essential for long-term missions and deep space exploration.

Space Power Electronics Industry Overview

The space power electronics market is consolidated, with key players occupying a significant market share. The major players in this market are BAE Systems PLC, Cobham Limited, Infineon Technologies AG, Texas Instruments Incorporated, and STMicroelectronics NV. These companies are at the forefront of developing powerful electronic devices that can withstand harsh conditions in space, such as extreme temperatures and radiation.

The leading market players are focusing more on acquiring contracts to maintain their market position. This approach is often complemented by introducing innovative products featuring cutting-edge technologies. For instance, in April 2023, ZF signed a multi-year supply agreement with STMicroelectronics for silicon carbide devices. Collaborations have become instrumental in establishing specialized research and development centers dedicated to advancing space power electronics equipment, signifying a robust commitment to innovation and growth in this high-tech field.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Platform

- 5.1.1 Satellites

- 5.1.2 Spacecraft and Launch Vehicles

- 5.1.3 Others

- 5.2 Type

- 5.2.1 Radiation-Hardened

- 5.2.2 Radiation-Tolerant

- 5.3 Application

- 5.3.1 Communication

- 5.3.2 Earth Observation

- 5.3.3 Navigation, Global Positioning System (GPS) and Surveillance

- 5.3.4 Technology Development and Education

- 5.3.5 Others

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 France

- 5.4.2.3 Germany

- 5.4.2.4 Russia

- 5.4.2.5 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Latin America

- 5.4.4.1 Brazil

- 5.4.4.2 Rest of Latin America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 BAE Systems PLC

- 6.2.2 Cobham Limited

- 6.2.3 Microchip Technology Inc.

- 6.2.4 RUAG Group

- 6.2.5 STMicroelectronics NV

- 6.2.6 Teledyne Technologies Incorporated

- 6.2.7 Texas Instruments Incorporated

- 6.2.8 Honeywell International Inc.

- 6.2.9 Microsemi Conduction

- 6.2.10 ON Semiconductor

- 6.2.11 Analog Devices Inc.

- 6.2.12 Renesas Electronics Corporation

- 6.2.13 Infineon Technologies AG