|

시장보고서

상품코드

1521641

우주용 센서 및 액추에이터 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2024-2029년)Space Sensors And Actuators - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

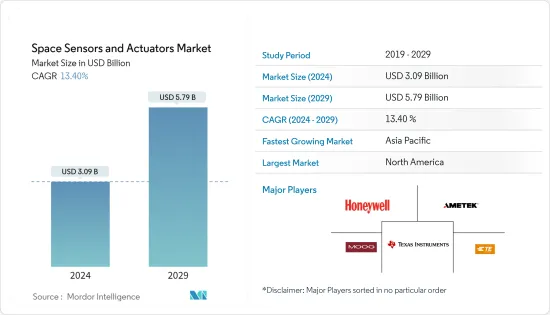

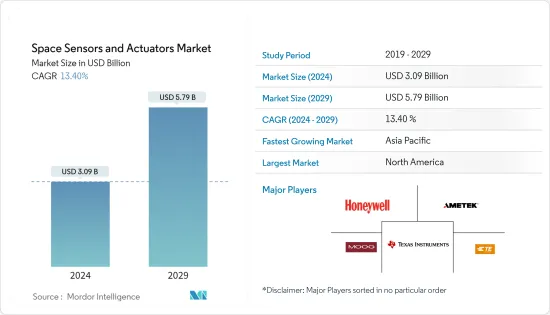

우주 센서 및 액추에이터 시장 규모는 2024년 30억 9,000만 달러로 추정되며, 2029년에는 57억 9,000만 달러에 달할 것으로 예상되며, 예측 기간(2024-2029) 동안 13.40%의 CAGR로 성장할 것으로 예상됩니다.

우주 산업은 비상장 기업의 진입과 투자로 큰 변화를 겪고 있으며, SpaceX와 Blue Origin과 같은 선구자들은 우주선 설계, 추진력 및 임무 수행에 대한 혁신적인 접근 방식으로 전망을 재구성하고 있습니다. 상용 부품은 우주 기술을 민주화하여 보다 친숙하고 비용 효율적으로 만들고 있습니다. 여기에 로봇 공학 및 적층 제조 기술의 발전이 더해져 우주 탐사에 대한 경제적 장벽이 낮아지고 있습니다.

신흥국들도 우주 예산을 늘리면서 시장 성장을 더욱 촉진하고 있습니다. 이러한 시장 개척은 우주 센서 및 액추에이터 시장을 발전시킬 뿐만 아니라, 우주가 더 많은 탐험가와 기업가들의 손이 닿을 수 있는 새로운 행성 탐사 시대로 나아가는 길을 열어주고 있습니다. 기술 발전과 투자 확대의 시너지 효과로 인해 과거에는 도달할 수 없을 것 같았던 미래의 혁신과 임무를 위한 비옥한 토양이 만들어지고 있습니다.

우주용 센서 및 액추에이터 시장은 성장을 저해할 수 있는 심각한 도전에 직면해 있습니다. 지상 임무용 센서 및 액추에이터 기술의 성숙도, 방사선 및 부식성 대기와 같은 우주의 가혹한 조건을 견딜 수 있는 시스템 설계의 복잡성 등이 주요 관심사입니다. 우주선 개발 및 배치와 관련된 정부 정책도 장애물이 될 수 있습니다. 이러한 문제에도 불구하고, 기술 발전과 비상장 기업의 투자 증가로 인해 시장 성장이 예상됩니다.

우주용 센서 및 액추에이터 시장 동향

예측 기간 동안 센서 부문이 시장 성장을 견인할 것으로 예상

우주용 센서와 액추에이터는 현대의 우주 임무에 필수적인 구성요소로, 각 응용 분야의 고유한 요구 사항을 충족하도록 맞춤화되어 있습니다. 이 정교한 장치들은 우주의 혹독한 조건에서 작동하도록 설계되어 환경 모니터링, 우주선 조종 및 데이터 수집과 같은 중요한 기능을 수행합니다. 예를 들어, 첨단 센서가 장착된 기상 관측 위성은 대기 상태를 정확하게 측정할 수 있으며, 액추에이터는 최적의 이미지 촬영과 태양광발전을 위해 위성의 정확한 위치를 보장합니다.

마찬가지로, 우주 관측 위성은 미세한 움직임을 위해 MEMS 기반 액추에이터를 사용하고, 강렬한 우주 방사선을 견디기 위해 방사선 경화 센서를 사용합니다. 이러한 기술은 우주선 및 탐사선의 성능과 신뢰성을 향상시켜 우주 임무의 비용 효율성에 기여합니다. 텔레다인 e2v의 고해상도 센서를 사용하는 ESA의 코페르니쿠스(Copernicus)와 같은 프로그램은 지구 관측 및 기타 과학적 시도를 지원하는 데 있어 이러한 구성요소의 중요성을 보여줍니다.

우주 탐사가 계속 발전함에 따라, 센서와 액추에이터의 역할은 우주 기술의 한계를 뛰어넘는 데 있어 점점 더 중요해지고 있습니다. 우주 영역 인식의 발전은 궤도상의 안보와 감시 능력 강화에 대한 중요한 약속을 반영합니다. 미국 우주군의 센서 및 감시 시스템에 대한 투자는 점점 더 경쟁이 치열해지고 있는 우주 공간에서 상황 인식을 유지하기 위한 전략적 움직임입니다.

광학 망원경과 감시 위성 개발은 우주 활동 감시 능력을 강화하고 잠재적 위협에 대한 신속한 대응을 보장하기 위한 것입니다. 이러한 적극적인 접근 방식은 우주가 국방과 세계 안보에 있어 중요한 프론티어로서 우주의 중요성을 강조하고 있습니다.

예측 기간 동안 북미가 시장을 독점할 것으로 예상

예측 기간 동안 북미가 우주용 센서 및 액추에이터 시장을 주도할 것으로 예상됩니다. 북미 우주 센서 및 액추에이터 시장에서 미국이 큰 비중을 차지하고 있습니다. 미국 시장의 성장은 주요 우주 센서 및 액추에이터 시스템 제조업체의 존재에 기인합니다. 미국에 기반을 둔 주요 우주 센서 및 액추에이터 제조업체로는 Texas Instruments Incorporated, Sierra Nevada Corporation, Honeywell International Inc, NASA의 발사 횟수 증가도 예측 기간 동안 행성 탐사 측면에서 미국 우주 센서 및 액추에이터 시장을 견인할 것으로 예상됩니다. 예를 들어, SpaceX는 Falcon 시리즈 로켓으로 96번의 성공적인 임무를 수행했습니다.

우주 센서 및 액추에이터의 사용은 방사선 내성 전기 광학 우주 센서의 개발 증가와 위성, 캡슐 화물, 행성 간 우주선 및 탐사선, 로버/우주선 착륙선, 로켓, 우주 정거장용 우주 센서 및 액추에이터의 소형화로 인해 성장할 것으로 예상됩니다. 또한, 2023년 6월 미국 우주군은 L3Harris Technologies Inc.에 2,900만 달러 규모의 탄성 미사일 경보 및 추적 위성 별자리용 센서 설계 계약을 발주했습니다. 이러한 신흥국 시장 개척은 예측 기간 동안 시장 성장을 촉진할 것으로 보입니다.

우주용 센서 및 액추에이터 산업 개요

저명한 우주용 센서 및 액추에이터 제조업체들의 존재감이 커지면서 예측 기간 동안 경쟁 업체들 간의 적대적 관계가 심화될 것으로 예상됩니다. 시장은 다음과 같은 주요 기업의 존재로 인해 반쯤 고정되어 있습니다. Honeywell International Inc., Moog Inc., Texas Instruments Incorporated, TE Connectivity Ltd., and Ametek Inc. These players have continuously expanded their operations by focusing on market expansions and acquisitions.

지속적인 제품 출시와 기술 업그레이드는 우주 분야의 전체 시장 성장과 관련하여 효과적으로 공을 굴릴 수 있습니다. 예를 들어, 2023년 6월 허니웰과 양자 네트워킹 및 컴퓨팅 회사인 Aegiq는 우주 페이로드 및 관련 지상 자산의 설계 및 배치를 보다 정확하고 비용 효율적으로 만들기 위한 종합적인 솔루션 구축을 검토하는 MoU를 체결하였습니다. 이번 협력은 소형 위성에 사용되는 광통신 기술의 링크 성능을 위해 허니웰의 대기 감지 기술과 Aegiq의 에뮬레이션 툴킷을 결합하기 위한 것입니다.

기타 혜택:

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

목차

제1장 소개

- 조사 가정

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- 시장 성장 억제요인

- Porter's Five Forces 분석

- 구매자/소비자의 협상력

- 공급 기업의 교섭력

- 신규 참여업체의 위협

- 대체품의 위협

- 경쟁 기업 간의 경쟁 강도

제5장 시장 세분화

- 제품 유형

- 센서

- 액추에이터

- 플랫폼

- 위성

- 캡슐/카고 모듈

- 혹성간 탐사기

- 로버/우주선 착륙선

- 발사체

- 최종사용자

- 상업

- 정부·방위

- 지역

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 프랑스

- 독일

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 세계 기타 지역

- 북미

제6장 경쟁 상황

- 벤더 시장 점유율

- 기업 개요

- Honeywell International Inc.

- TE Connectivity Ltd.

- Moog Inc.

- Ametek Inc.

- Texas Instruments Incorporated

- RUAG Group

- STMicroelectronics NV

- RTX Corporation

- Cobham Advanced Electronics Solutions(Cobham Limited)

- Maxar Technologies Inc.

- Bradford Space(Bradford Engineering BV)

The Space Sensors And Actuators Market size is estimated at USD 3.09 billion in 2024, and is expected to reach USD 5.79 billion by 2029, growing at a CAGR of 13.40% during the forecast period (2024-2029).

The space industry is witnessing a significant transformation fueled by the entry and investments of private companies. Pioneers like SpaceX and Blue Origin are reshaping the landscape with their innovative approaches to spacecraft design, propulsion, and mission execution. Commercial-off-the-shelf components have democratized space technology, making it more accessible and cost-effective. This, coupled with robotics and additive manufacturing advancements, has reduced the financial barriers to space exploration.

Emerging countries are also increasing their space budgets, further stimulating the market's growth. These developments are not only propelling the space sensors and actuators market forward but are also paving the way for a new era of planetary exploration, where space is within reach of a broader range of explorers and entrepreneurs. The synergy of technological progress and increased investment is creating a fertile ground for future innovations and missions that once seemed beyond our grasp.

The space sensors and actuators market faces significant challenges that could impede growth. The maturity of sensor and actuator technologies for surface missions is a critical concern, as is the complexity of designing systems that can withstand the harsh conditions of space, such as radiation and corrosive atmospheres. Government policies related to spacecraft development and deployment can also pose obstacles. Despite these challenges, the market is expected to grow, driven by technological advancements and increased investments from private companies.

Space Sensors And Actuators Market Trends

The Sensors Segment is Anticipated to Drive the Growth of the Market During the Forecast Period

Space sensors and actuators are integral components of modern space missions, each tailored to meet the unique demands of their respective applications. These sophisticated devices are designed to operate in the harsh conditions of space, performing critical functions such as environmental monitoring, spacecraft maneuvering, and data collection. For instance, weather monitoring satellites with advanced sensors can accurately measure atmospheric conditions, while actuators ensure precise satellite positioning for optimal image capture or solar power generation.

Similarly, space observation satellites utilize MEMS-based actuators for fine-tuned movements and radiation-hardened sensors to withstand intense cosmic radiation. These technologies enhance the performance and reliability of spacecraft and rovers and contribute to the cost-effectiveness of space missions. Programs like ESA's Copernicus, which employs high-resolution sensors from Teledyne e2v, exemplify the importance of these components in supporting Earth observation and other scientific endeavors.

As space exploration continues to evolve, the role of sensors and actuators becomes increasingly vital in pushing the boundaries of what is possible in space technology. The advancements in space domain awareness reflect a significant commitment to enhancing security and surveillance capabilities in orbit. The US Space Force's investment in sensors and surveillance systems is a strategic move to maintain situational awareness in space, which is increasingly becoming a contested domain.

The development of optical telescopes and surveillance satellites aims to bolster the ability to monitor space activities, ensuring a rapid response to any potential threats. This proactive approach underscores the importance of space as a critical frontier for national defense and global security.

North America is Expected to Dominate the Market During the Forecast Period

North America is expected to lead the space sensors and actuators market during the forecast period. The US accounted for a major share of the space sensors and actuators market in North America. The market's growth in the US can be attributed to the presence of key manufacturers of space sensors and actuator systems. Some key US-based space sensors and actuator companies include Texas Instruments Incorporated, Sierra Nevada Corporation, Honeywell International Inc., Moog Inc., and Bradford Space. The rise in the number of launches from NASA is also anticipated to drive the US space sensors and actuators market in terms of planetary exploration during the forecast period. For instance, SpaceX launched 96 successful missions with its Falcon series of rockets.

The use of space sensors and actuators is expected to grow due to the increasing development of radiation-hardened electro-optical space sensors and the miniaturization of space sensors and actuators for satellites, capsules cargos, interplanetary spacecraft & probes, rovers/spacecraft landers, launch vehicles, and space stations. Also, in June 2023, the US Space Force awarded L3Harris Technologies Inc. a USD 29 million contract to design a sensor for the service's planned Resilient Missile Warning and Tracking satellite constellation. Thus, developments such as these will drive the market's growth during the forecast period.

Space Sensors And Actuators Industry Overview

The increasing presence of prominent space sensors and actuator manufacturers is expected to intensify competitive rivalry during the forecast period. The market is semi-consolidated with the presence of key players such as Honeywell International Inc., Moog Inc., Texas Instruments Incorporated, TE Connectivity Ltd., and Ametek Inc. These players have continuously expanded their operations by focusing on market expansions and acquisitions.

Continuous product launches and technological upgrades effectively set the ball rolling regarding overall market growth in the space sector. For instance, in June 2023, Honeywell and Aegiq, a quantum networking and computing company, signed an MoU to explore creating a comprehensive solution to enable more precise and cost-effective design and deployment of space payloads and related ground assets. This collaboration was intended to combine Honeywell's atmospheric sensing technology and Aegiq's emulation toolkit for link performance of optical communication technologies used by small satellites.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Product Type

- 5.1.1 Sensors

- 5.1.2 Actuators

- 5.2 Platform

- 5.2.1 Satellites

- 5.2.2 Capsules/Cargo Modules

- 5.2.3 Interplanetary Spacecraft & Probes

- 5.2.4 Rovers/Spacecraft Landers

- 5.2.5 Launch Vehicles

- 5.3 End User

- 5.3.1 Commercial

- 5.3.2 Government and Defense

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 France

- 5.4.2.3 Germany

- 5.4.2.4 Russia

- 5.4.2.5 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Rest of the World

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Honeywell International Inc.

- 6.2.2 TE Connectivity Ltd.

- 6.2.3 Moog Inc.

- 6.2.4 Ametek Inc.

- 6.2.5 Texas Instruments Incorporated

- 6.2.6 RUAG Group

- 6.2.7 STMicroelectronics NV

- 6.2.8 RTX Corporation

- 6.2.9 Cobham Advanced Electronics Solutions (Cobham Limited)

- 6.2.10 Maxar Technologies Inc.

- 6.2.11 Bradford Space (Bradford Engineering BV)