|

시장보고서

상품코드

1521651

화물 운송 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2024-2029년)Cargo Shipping - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

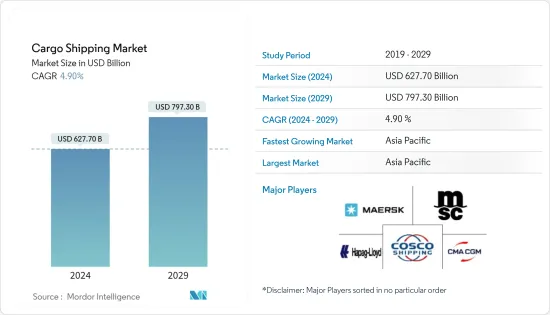

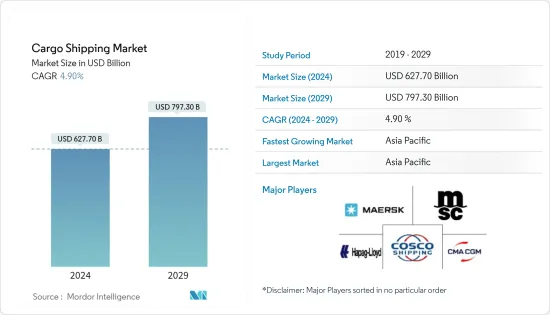

화물 운송 시장 규모는 2024년 6,277억 달러로 추정 및 예측되며, 2029년에는 7,973억 달러에 달할 것으로 예상되며, 예측 기간(2024-2029년) 동안 4.90%의 CAGR로 성장할 것으로 예상됩니다.

해상 화물 활동의 증가로 인해 컨테이너선, 벌크 화물 운송 및 기타 화물 운송에 대한 수요가 증가함에 따라 화물 운송 시장을 주도하고 있습니다.

선박을 통한 화물 운송 수요 증가, 무역 관련 협정 체결 급증 등의 요인이 화물 운송 시장의 성장을 보완하고 있습니다. 운송 비용과 재고 비용의 변동은 화물 운송 시장의 성장을 저해합니다. 그러나 해상 운송의 자동화, 해상 안전 기준 강화 등의 요인은 예측 기간 동안 화물 운송 시장의 성장에 기회를 제공할 것으로 예상됩니다.

주요 하이라이트

- 2022년 일본 연안선박의 국내 수송 물동량은 2021년 3억 2,466만 톤에 비해 3억 2,093만 톤을 기록할 것으로 예상된다.

- 인도 항만해운수로부에 따르면, 2022년 인도 전역 항구의 화물 처리량은 13억 2,300만 톤으로 2021년 대비 6.0% 증가했다고 합니다.

화물 운송 시장 동향

시장 확대를 뒷받침하는 크로스보더 거래의 증가

해상을 통한 국경 간 거래 증가, E-Commerce 산업 성장에 따른 해상 물동량 증가, 국가 간 다양한 자유무역협정의 시행은 해상 무역 활동의 확대에 기여하고 있으며, 이는 화물 운송 시장의 성장에 긍정적인 영향을 미치고 있습니다.

- 2022년 현재 세계 상선대의 일반 화물 운송은 17,784척, 벌크 화물 운송은 12,941척에 달합니다.

세계 상선대의 선복량은 최근 수십 년 동안 꾸준히 증가하고 있는데, 이는 해상 무역의 수요 증가로 인해 한 번의 항해에서 더 많은 양을 운송하기 위해 더 큰 선박이 필요하기 때문입니다.

- 2022년 컨테이너선 용량은 2억 9,300만 톤에 달해 2018년부터 2022년까지 3.1%의 CAGR을 기록할 것으로 예상됩니다.

해상 무역 활동이 증가함에 따라 이러한 선박이 다양한 상품을 운송하기 때문에 이러한 화물 운송에 대한 더 큰 수요가 존재하여 시장의 급격한 성장에 긍정적인 영향을 미쳤습니다.

전 세계 주요 해상 화물 운송업체들은 최근 몇 년 동안 국경 간 E-Commerce 활동의 성장으로 인해 운송 물동량이 급증하는 것을 목격했습니다. 해상 운송은 여전히 장거리 운송의 주류로 화물 운송 업체의 수요가 크게 증가하고 있습니다.

- 2022년 온라인 쇼핑을 이용하는 인도 소비자 중 미국이 전체 국경 간 E-Commerce 시장의 21%를 차지할 것으로 예상되며, 호주가 그 뒤를 이을 것으로 보입니다.

이러한 E-Commerce의 급속한 발전은 해상 운송 활동의 활성화와 함께 향후 몇 년 동안 화물 운송 시장의 급격한 성장에 기여할 수 있습니다.

유럽이 시장에서 큰 점유율을 차지

해상 무역의 증가와 경제 성장에 따라 화물 운송에 대한 수요는 유럽 시장에서 눈에 띄게 성장할 것으로 예상됩니다.

해운 부문은 독일 경제에서 가장 중요한 부문 중 하나입니다. 연간 매출액은 500억 유로(532억 2,000만 달러)에 달하며, 해운업에 직간접적으로 의존하는 고용자 수는 2022년 40만 명에 달할 것으로 예상됩니다.

독일에는 360개 이상의 해운회사가 약 2,700척의 선박을 운항하고 있습니다. 선주 국적별로 보면 독일은 그리스, 일본, 중국(4위)에 이어 가장 큰 상선대를 보유한 해운국입니다.

- 독일은 전 세계 컨테이너 운송 능력의 약 29%를 차지하는 컨테이너 선박을 보유하고 있으며, 선주 국적별로는 여전히 국제적인 선두주자입니다.

약 9개의 조선소가 독일 해군 조선 산업을 뒷받침하고 있으며, 약 2,800개의 기업이 조선 및 해양 산업에서 활약하고 있습니다. 이들 기업은 독일 조선소로부터의 납품으로 약 85%의 국내 부가가치를 창출하고 있습니다.

마찬가지로 영국 수출입의 거의 95%가 400개 이상의 영국 항구를 통해 해상으로 이루어지고 있습니다.

- 2022년 스페인은 미국, 중국, 일본에 이어 세계 4위의 해산물 수입국이 되었습니다.

- 2022년 스페인의 전체 수산물 수입액은 96억 달러로 2021년 대비 7.6% 증가했고, 2022년 스페인의 총 수출액은 전년 대비 3.4% 증가한 59억 달러에 달했습니다.

스페인은 유럽의 해운과 물류에 있어 필수적인 국가입니다. 스페인의 해운 산업은 도로, 철도, 항공 등 모든 부문에 걸쳐 잘 구축된 인프라 네트워크에 힘입어 유럽 내외의 효율적이고 유능한 공급 경로를 자랑합니다. 스페인에는 100개 이상의 해운회사가 있으며, 거대한 선단을 형성하고 있습니다. 스페인은 삼면이 바다로 둘러싸여 있어 항구 및 기타 해운 허브를 설치하기에 이상적인 국가입니다. 잘 연결된 시설은 이 지역의 여러 국제 공항과 연결되어 있습니다.

상기의 요인으로 인해 시장의 유럽 부문은 예측 기간 동안 성장할 것으로 예상됩니다.

화물 운송 산업 개요

화물 운송 시장은 세분화되어 있으며 많은 국제 기업들이 진출하고 있습니다. 이 부문의 주요 기업은 Maersk, MSC, CMA, COSCO, Hapag Lloyd 등입니다. 높은 진입장벽은 차량 비용의 상승과 규모의 경제의 증가로 인해 시장을 억제하고 있으며, 이는 업계의 경쟁에 영향을 미치고 있습니다. 그러나 주요 기업들은 향후 몇 년 동안 시장 점유율을 확보하기 위해 전략적 파트너십과 인수합병에 참여하고 있습니다.

- 2023년 1월, A.P. Moller-Maersk는 덴마크의 프로젝트 물류 전문가이자 비컨테이너 운송 외 프로젝트 물류 및 세계 운영 역량을 갖춘 Martin Bencher Group의 인수 완료를 발표했습니다. 인수 완료를 발표했습니다. 이번 인수로 양사는 전 세계 고객에게 프로젝트 물류 서비스를 제공할 수 있는 역량을 강화하는 한편, 다양한 산업 분야에 보다 종합적인 서비스를 제공할 수 있게 됐습니다.

기타 혜택

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 소개

- 조사 성과

- 조사 가정

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- 국가 간의 무역 협정 증가

- 국제 무역량 증가

- 시장 성장 억제요인

- 연료비 급등이 시장에 영향

- 밸류체인/공급망 분석

- 업계 규제와 정책

- Porter's Five Forces 분석

- 신규 참여업체의 위협

- 구매자/소비자의 협상력

- 공급 기업의 교섭력

- 대체품의 위협

- 경쟁 기업 간의 경쟁 강도

제5장 시장 세분화

- 선종

- 벌크 캐리어

- 일반화물 운송

- 컨테이너선

- 탱커

- 리퍼선

- 업종

- 식품 및 음료

- 제조업

- 석유 및 가스

- 제약

- 전기·전자

- 기타

- 화물 유형

- 액체화물

- 건화물

- 일반화물

- 지역

- 북미

- 미국

- 캐나다

- 기타 북미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 인도

- 중국

- 일본

- 한국

- 기타 아시아태평양

- 세계 기타 지역

- 남미

- 중동 및 아프리카

- 북미

제6장 경쟁 상황

- 벤더 시장 점유율

- 기업 개요

- A. P. Moller-Maersk AS

- MSC Mediterranean Shipping Company SA

- CMA CGM

- China COSCO Holdings Company Limited

- Hapag-Lloyd

- ONE(Ocean Network Express)

- Evergreen Line

- Wan Hai Lines

- Zim

- SITC

- Zhonggu Logistics Corp.

- Antong Holdings(QASC)

제7장 시장 기회와 향후 동향

- 물류 분야의 기술 개발

The Cargo Shipping Market size is estimated at USD 627.70 billion in 2024, and is expected to reach USD 797.30 billion by 2029, growing at a CAGR of 4.90% during the forecast period (2024-2029).

The rising demand for cargo vessels such as container ships, bulk carriers, and others due to the growth in sea freight activity is driving the cargo shipping market.

Factors such as the increasing demand for cargo transportation through ships and the surge in trade-related agreements supplement the growth of the cargo shipping market. Fluctuations in transportation and inventory costs hamper the growth of the cargo shipping market. However, factors such as the anticipated trend of automation in marine transportation and an increase in marine safety norms are expected to provide opportunities for the growth of the cargo shipping market during the forecast period.

Key Highlights

- In 2022, the freight volume transported domestically via coastwise vessels in Japan stood at 320.93 million metric ton, compared to 324.66 million metric ton in 2021.

- According to the Indian Ministry of Ports, Shipping, and Waterways, the total volume of cargo handled at seaports across India touched 1,323 million metric ton in FY 2022, witnessing a Y-o-Y increase of 6.0% compared to FY 2021.

Cargo Shipping Market Trends

Increasing Cross-border Trading to Support Market Expansion

The increasing cross-border trading activity via sea, rising sea freight volumes due to the growth of the e-commerce industry, and the implementation of various free-trade agreements across nations are contributing to expanding sea trade activity, which, in turn, is positively contributing to the growth of the cargo shipping market.

- The number of general cargo ships in the global merchant fleet stood at 17,784 units as of 2022, while the number of bulk cargo carriers reached 12,941 units.

The capacity of the global merchant fleet has increased steadily in recent decades, attributed to the rising demand for more seaborne trade, which calls for larger vessels to transport more volume in one trip.

- In 2022, the capacity of container ships touched 293 million dwt, registering a CAGR of 3.1% between 2018 and 2022.

With the rising seaborne trade activity, there exists a greater demand for these cargo carriers as these ships transport various goods, thereby positively impacting the surging growth of the market.

Leading ocean freight forwarders across the world are witnessing a rapid surge in the volume of freight they are transporting in recent years, owing to the growth in cross-border e-commerce activity. Since sea freight remains the dominant transportation medium to ship goods across long distances, the demand for cargo carriers shoots up extensively.

- In 2022, the United States was the leading market among Indian consumers who shop online, capturing 21% of the cross-border e-commerce market out of the overall cross-border e-commerce share, followed by Australia.

Thus, the rapid advancement in e-commerce, coupled with rising sea freight activity, may contribute to the surging growth of the cargo shipping market in the coming years.

Europe Holds a Significant Share in the Market

With the increasing seaborne trade and economic growth, the demand for cargo shipping is anticipated to witness evident growth in the European market.

The marine sector is one of the most important sectors of the German economy. The annual turnover is up to EUR 50 billion (USD 53.22 billion), and the number of jobs directly or indirectly dependent on the maritime industry was up to 400,000 in 2022.

In Germany, more than 360 shipping companies operate around 2,700 seagoing vessels. According to owner nationality, Germany is the largest shipping nation after Greece, Japan, and China (ranked 4th) with its merchant fleet.

- Germany holds around 29% of all container-carrying capacities worldwide in container shipping and is still positioned as an international leader according to owner nationality.

About nine shipyards support the German naval shipbuilding industry, and about 2,800 companies are active in the shipbuilding and ocean industries. The companies generate a domestic value added of approximately 85% on deliveries from German shipyards.

Likewise, almost 95% of all UK imports and exports move by sea through over 400 British ports.

- In 2022, Spain was the world's fourth largest importer of fish and seafood after the United States, China, and Japan.

- In 2022, Spain's seafood imports from all origins were USD 9.6 billion, up 7.6% from 2021. Total Spanish exports in 2022 reached USD 5.9 billion, up 3.4% compared to the previous year.

Spain is vital to the shipping and logistics in Europe. Spain's shipping industry is supported by its network of maintained infrastructure across all sectors (road, rail, and air), allowing it to boast efficient and capable supply routes through Europe and beyond. Over a hundred different shipping companies in Spain make up its massive fleet. Spain is covered by water on three sides, making it ideal for establishing ports and other shipping hubs. Well-connected facilities are linked to several international airports in the region.

Owing to the abovementioned factors, the European segment of the market is expected to grow during the forecast period.

Cargo Shipping Industry Overview

The cargo shipping market is fragmented in nature, with the presence of many international companies in the market. The top players in the segment include Maersk, MSC, CMA, COSCO, and Hapag Lloyd. High barriers to entry restrain the market due to the high cost of vehicles and increasing economies of scale, which affect competition in the industry. However, key players are involved in strategic partnerships and acquisitions to capture market share in the coming years.

- In January 2023, A.P. Moller-Maersk (Maersk) announced the completion of its acquisition of Martin Bencher Group, a Danish project logistics expert with premium capabilities within non-containerized project logistics and global operations. With the addition of Martin Bencher, these companies are strengthening their ability to offer project logistics services to their global clients while providing a more comprehensive offering to a wide array of industries.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 The Rise of Trade Agreements Between Nations

- 4.2.2 Increasing Volume of International Trade

- 4.3 Market Restraints

- 4.3.1 Surge in Fuel Costs Affecting the Market

- 4.4 Value Chain/Supply Chain Analysis

- 4.5 Industry Policies and Regulations

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Ship Type

- 5.1.1 Bulk Carriers

- 5.1.2 General Cargo Ships

- 5.1.3 Container Ships

- 5.1.4 Tankers

- 5.1.5 Reefer Ships

- 5.2 Industry Type

- 5.2.1 Food and Beverages

- 5.2.2 Manufacturing

- 5.2.3 Oil and Gas

- 5.2.4 Pharmaceutical

- 5.2.5 Electrical and Electronics

- 5.2.6 Others

- 5.3 Cargo Type

- 5.3.1 Liquid Cargo

- 5.3.2 Dry Cargo

- 5.3.3 General Cargo

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 India

- 5.4.3.2 China

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Rest of the World

- 5.4.4.1 South Ameria

- 5.4.4.2 Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 A. P. Moller-Maersk AS

- 6.2.2 MSC Mediterranean Shipping Company SA

- 6.2.3 CMA CGM

- 6.2.4 China COSCO Holdings Company Limited

- 6.2.5 Hapag-Lloyd

- 6.2.6 ONE (Ocean Network Express)

- 6.2.7 Evergreen Line

- 6.2.8 Wan Hai Lines

- 6.2.9 Zim

- 6.2.10 SITC

- 6.2.11 Zhonggu Logistics Corp.

- 6.2.12 Antong Holdings (QASC)

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Technological Developments in the Logistics Sector