|

시장보고서

상품코드

1521709

바이오아세톤 시장 : 시장 점유율 분석, 산업 동향, 성장 예측(2024-2029년)Bio-Acetone - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

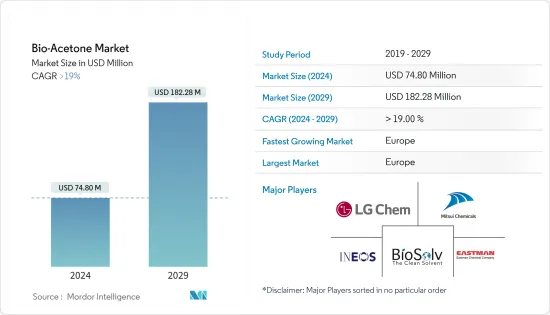

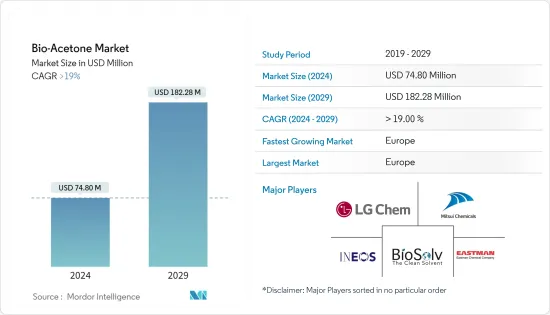

바이오아세톤 시장 규모는 2024년에 7,480만 달러로 추정되고, 2029년에는 1억 8,228만 달러에 이를 전망이며, 예측 기간 중(2024-2029년)의 CAGR은 19% 이상으로 성장할 것으로 예측됩니다.

COVID-19 팬데믹은 각국의 폐쇄 및 제한으로 인해 시장 수요에 부정적인 영향을 미쳤습니다. 그러나 시장은 2021년에 회복되었고, 2022년과 2023년에는 다양한 산업에서의 용도 증가로 유통 이전 수준으로 돌아갔습니다.

단기적으로, 바이오아세톤 수요는 페인트 및 코팅제와 같은 다양한 산업으로부터의 바이오 제품 수요에 의해 촉진됩니다.

반대로 다양한 대체품을 사용할 수 있다는 것은 향후 시장 성장을 방해할 것으로 예상됩니다.

바이오 제품을 생산하는 기술 증가는 예측 기간 동안 바이오아세톤 시장에 기회를 창출할 것으로 예상됩니다.

바이오아세톤 시장 동향

바이오 페인트 및 코팅 수요 증가

- 바이오아세톤은 일반적인 아세톤의 신재생 버전이며 아세톤과 동일한 화학적 특성을 가지고 있습니다.

바이오아세톤의 장점은 다음과 같습니다.

- 안전하고 발암성이 없습니다. 고성능 용제이며, 다양한 도료나 코팅제에 사용할 수 있습니다.

- 신재생 자원으로 만들어졌으며 생물 분해성이 있습니다. 폴리 우레탄 페인트, UV 경화 페인트, 에나멜, 바니시에 효과적입니다.

- 페인트 및 코팅제의 제조에서 시너로 사용됩니다. 페인트 및 코팅은 자동차, 건축, 포장, 가구, 섬유 등 다양한 용도로 사용됩니다.

- 많은 산업이 휘발성 유기 화합물(VOC)이 낮은 제품을 사용하기 시작했으며, VOC 규제 강화가 최근 시장 수요 증가로 이어지고 있습니다. 바이오아세톤은 옥수수와 같은 식물 유래의 원료로 제조되기 때문에 바이오용제는 주로 낮은 VOC 기반 페인트 및 코팅 제품에 사용됩니다.

- 자동차 산업에서는 다양한 VOC 규제로 인해 바이오 페인트에 대한 수요가 증가하고 있습니다. 바이오아세톤은 바이오 코팅용 용매로 사용되며 대시보드, 스티어링 휠, 도어 트림 및 기타 자동차 등 다양한 용도에 적용됩니다.

OICA(International Organization Of Motor Vehicle Manufacturers : 국제 자동차 공업회)가 발표한 최신 데이터에 따르면, 2021년에 8,000만 대였던 자동차의 총 생산 대수는 2022년에는 약 8,500만 대가 되었습니다.

- 또한 각국에서 전기자동차의 제조가 증가하고 있어 자동차산업에 있어서의 바이오 베이스 코팅 수요를 더욱 밀어 올리고 있습니다.

- 각국의 VOC 규제가 증가함에 따라 바이오의 페인트 및 코팅제에 대한 수요가 증가하는 경향이 있으며, 예측 기간 동안 시장 수요에 긍정적인 영향을 미칠 것으로 예상됩니다.

유럽이 가장 큰 소비자에게

- 유럽은 신재생 기반 제품에 대한 다양한 규정에 따라 바이오 아세톤의 최대 소비국 중 하나가 될 것으로 예상됩니다.

- 페인트 산업에서 배출되는 VOC는 다양한 환경 문제와 인체 건강 문제를 일으키고 있습니다. 이 때문에 다양한 국가가 코팅산업에서 유럽연합이 정한 지령에 따릅니다.

- 유럽연합(EU)은 페인트 및 코팅산업을 포함한 산업활동에서 배출되는 VOC를 삭감하기 위해 VOC용제 배출지령(SED)의 실시를 시작했습니다.

- SED는 VOC의 배출 규제치를 정하고, 도료나 코팅제 제조 등의 업계에 대해 제조 공정에서 낮은 VOC 또는 제로 VOC계 용매를 사용하도록 요구하고 있습니다.

- 화장품 산업에서 바이오아세톤은 아세톤에 비해 우수한 특성을 가지며 독성이 낮기 때문에 매니큐어의 제광액으로 사용되고 있습니다.

- 퍼스널케어 협회의 코스메틱스 유럽에 의하면, 화장품 업계의 2022년 시장 규모는 880억 유로(약 949억 달러)입니다.

- 이 지역에서 가장 큰 화장품 시장은 독일, 프랑스, 이탈리아, 영국, 폴란드입니다. 이 모든 국가는 이 지역의 화장품 시장 전체의 67% 이상을 차지합니다.

- 이러한 모든 요인은 예측 기간 동안 유럽 각국에서 바이오 아세톤 수요를 촉진할 것으로 예상됩니다.

바이오아세톤 산업 개요

세계의 바이오아세톤 시장은 통합되어 있습니다. 주요 진입기업(순부동)으로는 LG Chem, Mitsui Chemicals, INEOS, Bio Brands LLC, Eastman Chemical Company 등이 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 성장 촉진요인

- 다양한 산업용도에 있어서의 바이오 베이스 원료 수요 증가

- VOC 규제 증가

- 기타 촉진요인

- 억제요인

- 대체품의 이용가능성

- 기타 억제요인

- 산업 밸류체인 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 진입업자의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 세분화(시장 규모 금액 기준)

- 유형별

- 순도 99% 이하

- 순도 99 이상

- 용도별

- 플라스틱

- 고무

- 도장

- 기타(제광액, 세정제, 화학 중간체 등)

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 말레이시아

- 태국

- 인도네시아

- 베트남

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 터키

- 러시아

- 북유럽 국가

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 콜롬비아

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 나이지리아

- 카타르

- 이집트

- 아랍에미리트(UAE)

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- M&A, 합작사업, 제휴 및 협정

- 시장 점유율** 및 랭킹 분석

- Stratergies Adopted by Leading players

- 기업 프로파일

- INEOS

- Bio Brands LLC

- Celtic Renewables

- Circular Industries

- Eastman Chemcial Company

- LanzaTech

- LG Chem

- Mitsui Chemcials

- Sigma Aldrich(Merck KGaA)

- Vertec BioSolvents Inc.

제7장 시장 기회 및 향후 동향

- 바이오아세톤 제조 기술 증가

- 기타 기회

The Bio-Acetone Market size is estimated at USD 74.80 million in 2024, and is expected to reach USD 182.28 million by 2029, growing at a CAGR of greater than 19% during the forecast period (2024-2029).

The COVID-19 pandemic negatively impacted demand in the market due to lockdowns and restrictions imposed by various countries. However, the market recovered in 2021 and returned to pre-pandemic levels in 2022 and 2023 with the rise in applications in various industries.

Over the short term, the demand for bio-acetones is propelled by the demand for bio-based products from various industries, such as paints and coatings.

Conversely, the availability of various alternatives is expected to hinder the market's growth in the future.

The increasing technology for producing bio-based products is expected to create opportunities for the bio-acetone market during the forecast period.

Bio-Acetone Market Trends

Growing Demand For Bio-Based Paints and Coatings

- Bio-acetone is a renewable version of regular acetone and has the same characteristics as acetone with identical chemical properties.

Some of the advantages of bio-acetones include:

- They are safe and non-carcinogenic. They are high-performance solvents and can be used in various paints and coatings.

- They are made of renewable sources and are bio-degradable. They are effective in polyurethane paints, UV-curable coatings, enamels, and varnishes.

- They are used as thinners in paints and coatings manufacturing. Paints and coatings are used in various applications, including automotive, construction, packaging, furniture, textiles, and other applications.

- Many industries have started using products with low volatile organic compounds (VOC), and the increase in VOC regulations has led to a rise in demand in the market in recent times. Since bio-acetones are manufactured from plant-based raw materials such as corn, bio-solvents are used mainly in lower VOC-based paints and coating products.

- In the automotive industry, the demand for bio-based coatings is increasing owing to various VOC regulations. Bio acetone is used as a solvent in bio-based coatings and is applied to various applications such as dashboards, steering wheels, door trims, and other automotive vehicles.

According to the latest data released by the International Organization Of Motor Vehicle Manufacturers (OICA), the total number of vehicles manufactured in 2022 was around 85 million units compared to 80 million in 2021.

- In addition, there has been a rise in electric vehicle manufacturing in various countries, further propelling the demand for bio-based coatings in the automotive industry.

- Due to the rise in VOC regulations in various countries, the demand for bio-based paints and coatings is on the rise, which is expected to positively impact the demand in the market during the forecast period.

Europe To Become the Largest Consumer

- Europe is expected to be one of the largest consumers of bio-acetone due to various regulations set up for renewable-based products.

- The VOC emission from the coatings industry has raised various environmental and human health issues. This has led various countries to follow the directives laid by the European Union in the coatings industry.

- The European Union has started the implementation of the VOC solvents emission directive (SED) to reduce VOC emissions from industrial activities, including the paints and coatings industry.

- The SED has set up emission limits for VOCs and requires industries such as paints and coatings manufacturing to use low-VOC or zero-VOC-based solvents in the manufacturing process.

- In the cosmetics industry, bio-acetone is used as a nail polish remover owing to its superior characteristics and low toxicity compared to acetones.

- According to Cosmetics Europe, the personal care association, the cosmetics industry was valued at EUR 88 billion (~USD 94.9 billion) in 2022.

- The largest cosmetics markets in the region are Germany, France, Italy, the United Kingdom, and Poland. All these countries account for more than 67% of the total cosmetics market in the region.

- All these factors are expected to drive the demand for bio-acetones in various European countries during the forecast period.

Bio-Acetone Industry Overview

The global bio-acetone market is consolidated. Some major players (not in any particular order) include LG Chem, Mitsui Chemicals, INEOS, Bio Brands LLC, and Eastman Chemical Company.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand for Bio Based Raw Materials in Various Industrial Applications

- 4.1.2 Increase in VOC Regulations

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Availability of Alternatives

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size In Value)

- 5.1 Type

- 5.1.1 Purity <99%

- 5.1.2 Purity >99%

- 5.2 Application

- 5.2.1 Plastics

- 5.2.2 Rubber

- 5.2.3 Painting

- 5.2.4 Other Applications (Nail Polish Remover, Cleaning Agent, Chemicals Intermediaries, etc.)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Turkey

- 5.3.3.7 Russia

- 5.3.3.8 NORDIC Countries

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 Nigeria

- 5.3.5.3 Qatar

- 5.3.5.4 Egypt

- 5.3.5.5 United Arab Emirates

- 5.3.5.6 South Africa

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market share**/Ranking Analysis

- 6.3 Stratergies Adopted by Leading players

- 6.4 Company Profiles

- 6.4.1 INEOS

- 6.4.2 Bio Brands LLC

- 6.4.3 Celtic Renewables

- 6.4.4 Circular Industries

- 6.4.5 Eastman Chemcial Company

- 6.4.6 LanzaTech

- 6.4.7 LG Chem

- 6.4.8 Mitsui Chemcials

- 6.4.9 Sigma Aldrich (Merck KGaA)

- 6.4.10 Vertec BioSolvents Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Technologies for Bio Based Acetone Production

- 7.2 Other Opportunities