|

시장보고서

상품코드

1521717

펩타이드 및 올리고뉴클레오티드 CDMO : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2024-2029년)Peptide And Oligonucleotide CDMO - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

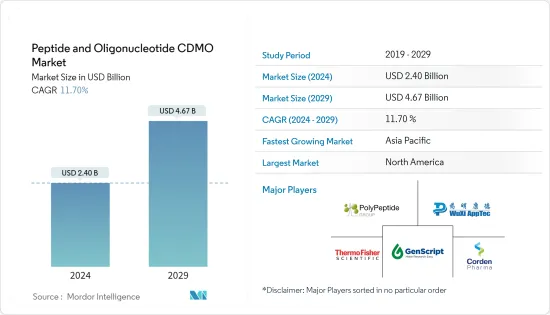

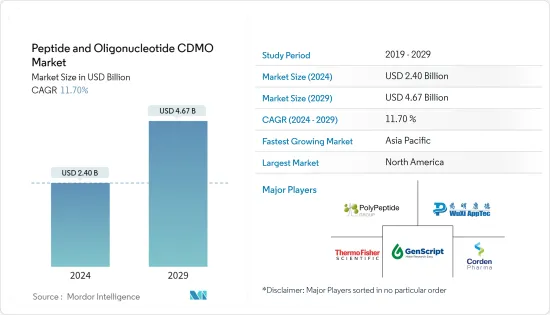

펩타이드 및 올리고뉴클레오티드 CDMO 시장 규모는 2024년 24억 달러로 추정 및 예측되며, 2029년에는 46억 7,000만 달러에 달할 것으로 예상되며, 예측 기간(2024-2029) 동안 11.70%의 CAGR로 성장할 것으로 예상됩니다.

펩타이드 및 올리고뉴클레오타이드 기반 치료제에 대한 수요 증가, 펩타이드 합성 및 올리고뉴클레오타이드 제조 기술의 발전, 제약 업계의 아웃소싱 추세로 인해 시장 동향은 더욱 가속화되고 있습니다. 펩타이드와 올리고뉴클레오타이드는 질병 치료에 대한 보다 타겟화된 개별화 접근법을 제공합니다. 펩타이드와 올리고뉴클레오티드는 특정 분자 표적과 상호 작용하도록 설계되어 치료 개입의 정확성을 높입니다. 이러한 분자는 암, 유전성 질환, 대사성 질환 등 다양한 치료 분야에서 연구되고 있습니다. 예를 들어, 올리고뉴클레오티드는 유전자 돌연변이를 치료할 수 있는 잠재력으로 주목을 받고 있으며, CDMO는 종종 펩타이드와 올리고뉴클레오티드를 포함한 특정 유형의 분자를 합성하고 제조하는 데 특화되어 있습니다. 그들의 전문성은 효율적이고 고품질의 생산을 보장하고 치료용 분자가 요구되는 기준을 충족할 수 있도록 보장합니다.

제약 업계 내 협업과 파트너십은 펩타이드 및 올리고뉴클레오티드 CDMO 시장을 크게 성장시킬 수 있습니다. 예를 들어, 2023년 5월 PolyPeptide와 Numaferm은 펩타이드 개발 및 생산에 대한 Preferred Partner Collaboration Agreement를 체결하여 PolyPeptide의 cGMP 제조 능력, 규제 관련 노하우, 시장 접근성, Numaferm의 생화학 생산 플랫폼과 지속가능한 펩타이드 제조에 대한 전문성을 활용했습니다.

또한, 2023년 8월 EUROAPI와 CDMO인 BianoGMP의 주주들은 EUROAPI가 Biano의 지분 100%를 인수하는 주식 매매 및 양도 계약을 체결하였습니다. 이 계약은 초기 단계(전임상 및 1상) 올리고뉴클레오티드 프로젝트에서 EUROAPI의 매력을 강화할 것입니다.

따라서 펩타이드 및 올리고뉴클레오티드 기반 치료제에 대한 수요 증가와 전략적 제휴는 예측 기간 동안 시장 성장에 기여할 것으로 예상됩니다. 그러나 엄격한 규제 정책과 치료에 따른 높은 비용은 예측 기간 동안 시장을 억제할 것으로 예상됩니다.

펩타이드 및 올리고뉴클레오타이드 CDMO 시장 동향

치료제 부문이 큰 시장 점유율을 차지하고 있으며, 예측 기간 동안에도 비슷한 상황이 지속될 것으로 예상

펩타이드 및 올리고뉴클레오타이드 치료제는 다양한 용도로 사용되며, 제조 및 규제 측면에서 공통점이 있고, 제형의 발전으로 인해 제품의 복잡성이 증가하여 혁신적인 솔루션이 필요합니다. 숙련된 개발 및 제조 위탁 기관과의 협력은 의약품 개발자의 제조 요건을 용이하게 하고 개발 노력의 우선순위를 정할 수 있게 해줍니다.

펩타이드와 올리고뉴클레오타이드의 치료 응용은 의약품 개발 활동을 활성화하고 시장 성장에 기여할 것으로 예상됩니다. 펩타이드는 표적화된 암 치료 및 당뇨병과 같은 질병 관리를 위해 연구되고 있습니다. 이러한 질병으로 인한 부담 증가는 이 분야의 성장을 촉진할 것으로 예상됩니다. 예를 들어, 미국암협회(ACS)가 발표한 2024년 통계에 따르면 암 발병률은 2021년 193만 건에서 2023년 200만 건으로 증가할 것으로 추정되며, 이는 2년 만에 6만 건 이상 증가한 것으로 국내 암 발병률이 빠르게 증가하고 있음을 보여줍니다. 펩타이드와 올리고뉴클레오티드는 암 표적 치료제로 연구되고 있으며, CDMO는 펩타이드 기반 항암제 개발 및 생산에 기여하고 있습니다.

또한, 펩타이드 및 올리고뉴클레오타이드 생산능력의 증가는 예측 기간 동안 시장을 견인할 것으로 예상됩니다. 예를 들어, 2023년 9월 CordenPharma는 세계 최대 규모의 고체상 펩타이드 합성(SPPS) 제조 시설인 CordenPharma Colorado에서 새롭게 업그레이드된 설비를 통해 상업용 펩타이드 생산능력을 강화할 것이라고 발표했습니다.

따라서 펩타이드 및 올리고뉴클레오타이드의 치료적 응용과 시장 기업의 전략적 이니셔티브가 예측 기간 동안 이 부문의 성장을 촉진할 것으로 예상됩니다.

북미가 예측 기간 동안 큰 시장 점유율을 차지할 것으로 예상

북미에서 펩타이드 및 올리고뉴클레오타이드 CDMO 시장은 잘 구축된 연구 시설, 펩타이드 및 올리고뉴클레오타이드 기반 치료제의 연구개발에 대한 높은 투자, 만성질환의 부담 증가로 인해 성장할 것으로 예상됩니다. 펩타이드와 올리고뉴클레오티드를 포함한 바이오의약품에 대한 수요가 증가하고 있습니다. 북미 CDMO는 이러한 복잡한 분자의 개발 및 제조에 특화된 서비스를 제공함으로써 이러한 수요에 대응할 수 있는 체제를 갖추고 있습니다.

제약사 및 생명공학 기업들의 R&D 활동에 대한 지속적인 투자는 펩타이드 및 올리고뉴클레오타이드 CDMO 시장 확대에 기여하고 있습니다. 이러한 투자는 전문 지식과 인프라를 활용하기 위해 CDMO와 제휴를 맺는 경우가 많습니다. 예를 들어, 2023년 1월 애질런트 테크놀러지(Agilent Technology)는 급격한 시장 성장에 따라 치료용 핵산 생산능력을 두 배로 늘리기 위해 약 7억 2,500만 달러를 투자했습니다. 이 투자는 치료용 올리고뉴클레오타이드에 대한 수요와 치료용 올리고뉴클레오타이드 위탁 개발 및 제조 조직의 독보적인 품질과 서비스를 반영하고 있습니다.

또한 2022년 12월, CDMO의 Asimchem Laboratories(천진)는 매사추세츠 주 워번(Woburn)에 새로운 지점을 개설할 것이라고 발표했습니다. 보스턴에 위치한 최신 시설은 저분자, 펩타이드, 올리고뉴클레오티드를 포함한 초기 단계의 연구 개발 서비스를 제공할 예정입니다.

따라서 북미 펩타이드 및 올리고뉴클레오티드 CDMO 시장은 수요 증가, 치료제의 발전, 아웃소싱 동향, 규제 지원, R&D 투자로 인해 활기를 띌 것으로 예상됩니다.

펩타이드 및 올리고뉴클레오타이드 CDMO 산업 개요

펩타이드 및 올리고뉴클레오타이드 위탁 개발 및 제조 시장의 경쟁은 완만하며, 크고 작은 업체들이 서비스 확장, 제휴, 공동 연구, 합병, 인수 등의 전략적 활동을 펼치고 있습니다. 주요 업체로는 Thermo Fisher Scientific Inc., Polypeptide Group, Wuxi Apptec, Genscript Biotech Corporation, CordenPharma International 등이 있습니다.

기타 혜택:

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

목차

제1장 소개

- 조사 가정과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- 펩타이드 및 올리고뉴클레오티드 기반 치료제에 대한 수요 증가

- 펩타이드 합성 및 올리고뉴클레오티드 제조 기술의 진보

- 제약 업계의 아웃소싱 동향 상승

- 시장 성장 억제요인

- 규제상 과제

- 제조능력 제약과 지적재산에 관한 우려

- Porter's Five Forces 분석

- 공급 기업의 교섭력

- 구매자·소비자의 협상력

- 신규 참여업체의 위협

- 대체품의 위협

- 경쟁 기업 간의 경쟁 강도

제5장 시장 세분화(시장 규모 - 금액)

- 제품별

- 펩타이드 CDMO

- 올리고뉴클레오티드 CDMO

- 용도별

- 치료

- 연구 용도

- 진단

- 기타 용도

- 최종사용자별

- 제약·바이오테크놀러지 기업

- 연구기관

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 영국

- 독일

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 인도

- 일본

- 중국

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카공화국

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 상황

- 기업 개요

- Thermo Fisher Scientific Inc.

- Merck KGaA

- Catalent, Inc.

- Genscript Biotech Corporation

- Polypeptide Group

- Bachem Holding AG

- Ajinomoto Co. Inc.

- Wuxi Apptec Co. Ltd

- Rentschler Biopharma SE

- CordenPharma International

- Senn Chemicals AG

- PolyPeptide Group

- Almac Group

- Lonza

제7장 시장 기회와 향후 동향

ksm 24.08.01The Peptide And Oligonucleotide CDMO Market size is estimated at USD 2.40 billion in 2024, and is expected to reach USD 4.67 billion by 2029, growing at a CAGR of 11.70% during the forecast period (2024-2029).

The market increases due to the rising demand for peptide and oligonucleotide-based therapeutics, advancements in peptide synthesis and oligonucleotide manufacturing technologies, and the growing outsourcing trend in the pharmaceutical industry. Peptides and oligonucleotides offer a more targeted and personalized approach to treating diseases. They are designed to interact with specific molecular targets, providing precision in therapeutic interventions. These molecules are being explored for various therapeutic areas, including cancer, genetic disorders, and metabolic diseases. Oligonucleotides, for instance, are gaining attention for their potential in addressing genetic mutations. CDMOs often specialize in synthesizing and manufacturing specific types of molecules, including peptides and oligonucleotides. Their expertise ensures efficient and high-quality production, ensuring the therapeutic molecules meet the required standards.

Collaboration and partnerships within the pharmaceutical industry can significantly boost the peptide and oligonucleotide CDMO market. For instance, in May 2023, PolyPeptide and Numaferm signed a Preferred Partner Collaboration Agreement for peptide development and production, leveraging PolyPeptide's cGMP manufacturing capacities, regulatory know-how, and market access and Numaferm's biochemical production platform and expertise in sustainable peptide manufacturing.

Similarly, in August 2023, EUROAPI and the shareholders of BianoGMP, a CDMO, signed a share purchase and transfer agreement under which EUROAPI will acquire 100% of Biano shares. The deal enhances EUROAPI's attractiveness for early-phase (preclinical and Phase 1) oligonucleotide projects.

Hence, increasing demand for peptide and oligonucleotide-based therapeutics and strategic partnerships is expected to contribute to the market growth during the forecast period. However, stringent regulatory policies and the high cost associated with the therapy are expected to restrain the market during the forecast period.

Peptide And Oligonucleotide CDMO Market Trends

The Therapeutics Segment Holds a Significant Market Share and is Expected to Continue the Same During the Forecast Period

Peptide and oligonucleotide therapeutics possess multifaceted applications and share manufacturing and regulatory similarities, with advancements in formulation increasing product complexity and necessitating innovative solutions. Collaboration with a proficient contract development and manufacturing organization facilitates drug developers' manufacturing requirements, enabling them to prioritize their development efforts.

The therapeutic application of peptides and oligonucleotides is expected to increase drug development activities and contribute to market growth. Peptides are being explored for targeted cancer therapies and managing conditions like diabetes. The growing burden of these diseases is expected to propel the segment's growth. For instance, according to 2024 statistics published by the American Cancer Society (ACS), the incidence of cancer cases was estimated to increase from 1.93 million in 2021 to 2.00 million in 2023, a rise of more than 60 thousand cases in two years, demonstrating a rapid growth in the incidence of cancer cases in the country. Peptides and oligonucleotides are being explored for targeted cancer therapies. CDMOs contribute to the development and production of peptide-based anticancer drugs.

Moreover, the launch of peptides and oligonucleotides production capacity is expected to boost the market during the forecast period. For instance, in September 2023, CordenPharma announced the inauguration of increased commercial peptide production capacity with newly upgraded facilities at CordenPharma Colorado, the largest solid-phase peptide synthesis (SPPS) manufacturing facility worldwide.

Hence, the therapeutic applications of peptides and oligonucleotides, along with the strategic initiatives taken by market players, are expected to drive the growth of this segment during the forecast period.

North America is Expected to Hold a Significant Market Share During the Forecast Period

In North America, the peptide and oligonucleotide CDMO market is expected to grow owing to established research facilities, high investment in R&D for peptide and oligonucleotide-based therapeutics, and the growing burden of chronic diseases. The demand for biopharmaceuticals, including peptides and oligonucleotides, has been rising. CDMOs in North America are well-positioned to cater to this demand by offering specialized services in developing and manufacturing these complex molecules.

Continuous investments in research and development activities by pharmaceutical and biotech companies contribute to expanding the peptides and oligonucleotide CDMO market. These investments often involve collaborations with CDMOs to access specialized expertise and infrastructure. For instance, in January 2023, Agilent Technologies Inc. invested approximately USD 725 million to double the manufacturing capacity of therapeutic nucleic acids in response to the market's rapid growth. This investment reflects the strong demand for therapeutic oligonucleotide and the unmatched quality and service of therapeutic oligonucleotide contract development and manufacturing organization.

Additionally, in December 2022, Asymchem Laboratories (Tianjin) Co. Ltd, a CDMO, announced the opening of a new site in Woburn, Massachusetts. The latest Boston site provides early-stage R&D services, including small molecules, peptides, and oligonucleotides.

Hence, the North American peptides and oligonucleotide CDMO market is expected to boost due to increasing demand, advancements in therapeutics, outsourcing trends, regulatory support, and R&D investments.

Peptide And Oligonucleotide CDMO Industry Overview

The market for peptide and oligonucleotide contract development and manufacturing organizations is moderately competitive, with both small and large players involved in strategic activities such as the expansion of services, partnerships, collaborations, as well as mergers, and acquisitions. Key players are Thermo Fisher Scientific Inc., Polypeptide Group, Wuxi Apptec Co. Ltd, Genscript Biotech Corporation, and CordenPharma International.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definitions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand For Peptide And Oligonucleotide-Based Therapeutics

- 4.2.2 Advancements In Peptide Synthesis And Oligonucleotide Manufacturing Technologies

- 4.2.3 Increasing Outsourcing Trend In The Pharmaceutical Industry

- 4.3 Market Restraints

- 4.3.1 Regulatory Challenges

- 4.3.2 Manufacturing Capacity Constraints and Intellectual Property Concerns

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1 By Product

- 5.1.1 Peptide CDMO

- 5.1.2 Oligonucleotide CDMO

- 5.2 By Application

- 5.2.1 Therapeutics

- 5.2.2 Research Applications

- 5.2.3 Diagnostics

- 5.2.4 Other Application

- 5.3 End User

- 5.3.1 Pharmaceutical and Biotechnology Companies

- 5.3.2 Research Organization

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Spain

- 5.4.2.5 Italy

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 India

- 5.4.3.2 Japan

- 5.4.3.3 China

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of the Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Thermo Fisher Scientific Inc.

- 6.1.2 Merck KGaA

- 6.1.3 Catalent, Inc.

- 6.1.4 Genscript Biotech Corporation

- 6.1.5 Polypeptide Group

- 6.1.6 Bachem Holding AG

- 6.1.7 Ajinomoto Co. Inc.

- 6.1.8 Wuxi Apptec Co. Ltd

- 6.1.9 Rentschler Biopharma SE

- 6.1.10 CordenPharma International

- 6.1.11 Senn Chemicals AG

- 6.1.12 PolyPeptide Group

- 6.1.13 Almac Group

- 6.1.14 Lonza