|

시장보고서

상품코드

1521778

요골동맥 압박 기기 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2024-2029년)Radial Artery Compression Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

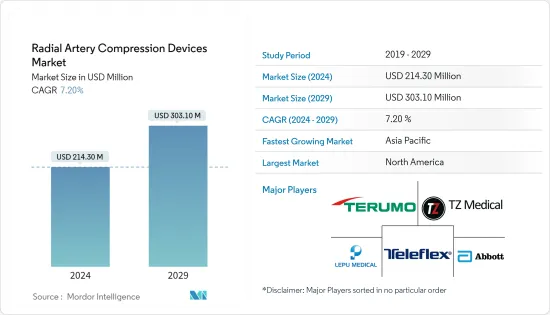

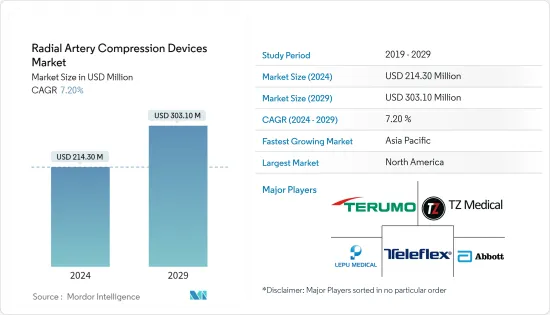

요골동맥 압박 기기 시장 규모는 2024년 2억 1,430만 달러로 추정되며, 2029년에는 3억 310만 달러에 달할 것으로 예상되며, 예측 기간(2024-2029) 동안 7.20%의 CAGR로 성장할 것으로 예상됩니다.

요골동맥 압박 기기는 요골동맥 접근을 통한 진단 또는 중재적 시술 후 지혈(출혈을 멈추는 것)을 달성하고 요골동맥 천자 부위의 압력을 유지하기 위해 사용됩니다. 이 기구는 제어된 압박을 가하고 요골 동맥의 밀봉을 보장하기 위해 특별히 설계되었습니다. 수술 건수 증가와 혁신적인 제품 출시가 시장을 이끄는 요인 중 하나입니다.

주요 하이라이트

- 말초동맥질환과 같은 심혈관계 질환은 전 세계적인 건강 문제입니다. 예를 들어, 2023년 11월 National Center for Chronic Disease Prevention and Health Promotion이 발표한 자료에 따르면, 2022년 전 세계적으로 약 5억 2,300만 명이 심혈관 질환(CVD)을 앓고 있는 것으로 추정되며, 흡연, 음주 등 다양한 생활습관 변화로 인해 향후 몇 년 동안 증가할 것으로 예상됩니다. 이처럼 심혈관 질환 환자의 증가는 심혈관 중재시 요골동맥 접근 시술에 따른 출혈성 합병증 감소에 도움이 되는 요골동맥 압박 기기에 대한 수요를 촉진할 것으로 예상됩니다.

- 또한, 요골동맥 압박 기기에 대한 수요가 지속적으로 증가함에 따라 기업들은 전 세계 환자들의 증가하는 수요를 충족시키기 위해 제조 시설을 설립하여 신제품 개발 및 지리적 확장과 같은 다양한 전략을 채택하고 있습니다. 예를 들어, 2024년 2월 푸에르토리코 카구아스에 새로운 제조 시설을 개설한 테르모 메디컬 코퍼레이션(Telmo Medical Corporation)은 혈관 폐쇄 장치 Angio-Seal에 대한 수요 증가에 대응하기 위해 생산량을 확대했습니다. 제조 시설의 확장은 제품 생산량을 늘리고 시장에서 사용할 수 있는 장치의 수를 증가시킬 것입니다. 이는 장치 수요 증가에 대응하고 시장을 주도할 것으로 예상됩니다.

- 따라서 심혈관 질환 환자의 지속적인 증가와 시장 제품의 다양한 제조 시설의 확장은 향후 몇 년 동안 시장 성장을 촉진할 것으로 예상됩니다. 그러나 국가별로 상이한 상환 정책과 혈종과 같은 신체 접근 부위의 잠재적 합병증은 예측 기간 동안 시장 성장을 저해할 것으로 예상되는 몇 가지 요인으로 꼽힙니다.

요골동맥 압박 기기 시장 동향

외과 수술에 대한 응용이 크게 성장할 것으로 예상

- 요골 동맥 압박 장치는 주로 심장 카테터 치료와 관련이 있습니다. 심장 카테터 삽입이 증가함에 따라 요골 동맥 압박 장치의 사용은 외과 적 개입으로 증가할 것으로 예상되며 예측 기간 동안이 분야의 성장을 촉진 할 가능성이 높습니다.

- 심장병과 같은 만성질환은 전 세계적으로 이환율의 중요한 원인 중 하나입니다. 예를 들어, 영국 심장 재단이 2024년 3월에 발표한 데이터에 따르면, 2022년 영국에서 약 760만 명이 심장병을 앓고 있습니다. 이는 심장 질환의 부담이 크다는 것을 나타내며, 심장 카테터 검사에 대한 수요를 증가시켜 요골 동맥 압박 장치에 대한 수요를 증가시키고 있습니다.

- 외과 적 개입 부문의 성장은 심장병에 걸리기 쉽고 외과 적 개입이 필요한 노인 인구가 전 세계적으로 증가함에 따라 주도 될 것으로 예상됩니다. United Nations World Population Prospects 2022가 발표한 데이터에 따르면 전 세계 노인 인구는 빠르게 증가하고 있으며, 2022년에는 65세 이상의 노인 인구가 전 세계적으로 7억 7100만 명에 달할 것으로 예상됩니다. 7억 7,100만 명 이상으로 세계 인구의 약 9.3%를 차지할 것입니다. 또한 2050년에는 65세 이상 인구가 약 15억 명에 달해 세계 인구의 약 16.0%를 차지할 것으로 예측하고 있습니다. 이처럼 심혈관 질환을 앓고 있는 고령화 인구의 증가는 향후 몇 년 동안 외과적 개입 분야에서 큰 성장이 예상되는 주요 요인 중 하나입니다.

북미가 큰 시장 점유율을 차지할 것으로 예상

- 북미는 심혈관 수술 건수 증가, 헬스케어 인프라 개발, 신제품 출시, 기존 기업의 존재 등으로 인해 시장에서 큰 비중을 차지할 것으로 예상됩니다.

- 미국은 전국적으로 심혈관 수술 건수가 증가함에 따라 이 지역 시장을 독점할 것으로 예상됩니다. 예를 들어, Current Cardiology Reviews가 2023년 5월에 발표한 논문에 따르면, 미국에서는 지난 몇 년 동안 경피적 방사선 심장 카테터 치료(TRA)가 크게 증가했다고 합니다.

- 미국에서는 심장 이식 건수도 증가하고 있습니다. 예를 들어, 로체스터 대학 메디컬 센터 로체스터는 2024년 1월, 스트롱 메모리얼 병원에서 2023년 40건의 심장 이식 수술이 실시되어 전년(2022년) 대비 82% 증가했다고 발표했습니다. 또한 Cedars-Sinai가 2022년 1월에 발표한 데이터에 따르면 관상동맥 우회술 또는 우회술이라고도 불리는 관상동맥 우회술(CABG)은 여전히 미국에서 가장 흔한 심장 수술로 밝혀졌습니다. 또한 미국에서는 매년 30만 명 이상이 우회 수술을 받고 있습니다. 따라서 요골 압박 장치는 효과적인 심장 수술에서 중요한 역할을 합니다.

- 또한, 이 지역의 주요 기업들의 신제품 출시가 시장을 견인할 것으로 예상됩니다. 예를 들어, 2022년 3월 Medical Ingenuities는 미국 Lakewood Ranch Medical Center에서 특허 지혈을 달성하기 위해 혁신적인 요골 지혈 밴드 시스템인 PH Band를 사용하여 상업적 사례를 수행했습니다. 모든 사례는 성공적이었으며, 다른 요골 밴드와 비교하여 PH 밴드의 고유한 장점을 입증했습니다. 따라서 외과적 개입이 필요한 심혈관 질환의 부담이 증가하고 첨단 요골 동맥 압박 장치의 채택이 증가함에 따라 조사 대상 시장은 북미에서 크게 성장할 것으로 예상됩니다.

요골동맥 압박 기기 산업 개요

요골동맥 압박 기기 시장은 전 세계 및 지역적으로 활동하는 여러 기업이 존재하기 때문에 시장이 세분화되어 있습니다. 경쟁 상황에는 시장 점유율을 차지하고 있는 국제 및 지역 기업들에 대한 분석이 포함됩니다.

기타 혜택

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 소개

- 조사 가정과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- 심혈관질환 증가

- 요골동맥 액세스에 대한 기호 상승

- 시장 성장 억제요인

- 상환 정책 격차

- 액세스 부위에서의 합병증의 가능성

- Porter's Five Forces 분석

- 신규 참여업체의 위협

- 구매자·소비자의 협상력

- 공급 기업의 교섭력

- 대체품의 위협

- 경쟁 기업 간의 경쟁 강도

제5장 시장 세분화(시장 규모 - 금액)

- 제품별

- 밴드/스트랩형

- 노브 기반

- 플레이트 기반

- 용도별

- 교환 가능 기기

- 재사용 가능 기기

- 용도별

- 수술 개입

- 진단

- 최종사용자별

- 병원

- 외래 수술 센터

- 기타 최종사용자

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카공화국

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 상황

- 기업 개요

- Terumo Corporation

- Abbott

- Teleflex Incorporated

- Semler Technologies Inc.

- VYGON

- Merit Medical Systems

- Beijing Demax Medical Technology

- Forge Medical

- TZ Medical, Inc.

- Lepu Medical Technology(Beijing) Co. Ltd

- Advin Health Care

제7장 시장 기회와 향후 동향

ksm 24.08.01The Radial Artery Compression Devices Market size is estimated at USD 214.30 million in 2024, and is expected to reach USD 303.10 million by 2029, growing at a CAGR of 7.20% during the forecast period (2024-2029).

Radial artery compression devices achieve hemostasis (stop bleeding) and maintain pressure at the radial artery puncture site following diagnostic or interventional procedures performed through radial artery access. These devices are specifically designed to provide controlled compression and ensure the seal of the radial artery. An increase in the number of surgeries and innovative product launches are some factors that drive the market.

Key Highlights

- Cardiovascular diseases, like peripheral artery disease, are global health concerns. For instance, as per the data published by the National Center for Chronic Disease Prevention and Health Promotion in November 2023, globally, an estimated 523 million were living with cardiovascular diseases (CVD) in 2022, and this is expected to increase over the coming years due to the various lifestyle changes such as smoking, alcohol consumption, etc. Thus, the rising burden of cardiovascular disease cases is expected to drive the demand for radial artery compression devices as the device helps reduce bleeding complications associated with radial artery access procedures during cardiovascular interventions.

- Furthermore, as the demand for radial artery compression devices continues to rise, companies are adopting different strategies, such as new product development and geographical expansion, by setting up manufacturing facilities to cater to the increasing requirements of patients worldwide. For instance, in February 2024, Terumo Medical Corporation opened a new manufacturing facility in Caguas, Puerto Rico, to expand production to meet the growing demand for the company's Angio-Seal vascular closure device. The expansion of the manufacturing facility boosts product volume, increasing the number of devices available in the market. This is expected to meet the growing requirement of the devices and drive the market.

- Therefore, the continuous increase in cardiovascular disease cases and the expansion of various manufacturing facilities of market products are projected to drive the market's growth over the coming years. However, variability in reimbursement policies across countries and potential complications at the body's access site, like hematoma, are some factors expected to hinder the market's growth during the forecast period.

Radial Artery Compression Devices Market Trends

Surgical Intervention Application is Expected to Have Significant Growth

- Radial artery compression devices are primarily associated with cardiac catheterization procedures. As the procedures of cardiac catheterization increase, the utilization of radial artery compression devices is expected to increase in surgical intervention, which is likely to boost the segment's growth over the forecast period.

- Chronic diseases like heart disease continue to be some of the significant causes of morbidity globally. For instance, as per the data published by the British Heart Foundation in March 2024, in the United Kingdom, around 7.6 million individuals suffered from heart disease in 2022. This shows the high burden of heart disease, which increases the demand for cardiac catheterization, thereby increasing the demand for radial artery compression devices.

- The surgical intervention segment's growth is expected to be driven by the rising number of elderly individuals worldwide, who are more susceptible to cardiac diseases and need surgical intervention. This increases the use of radial artery compression devices in the surgical intervention. According to the data published by the United Nations World Population Prospects 2022, the global geriatric population is rapidly increasing. In 2022, over 771.0 million individuals aged 65 years or older lived worldwide, accounting for approximately 9.3% of the global population. The report also predicts that by 2050, the population aged 65 years or older is likely to reach approximately 1.5 billion, representing around 16.0% of the global population. Thus, the increasing aging population with cardiovascular disease is one of the major factors that is expected to witness significant growth in the surgical intervention segment in the upcoming years.

North America is Expected to Hold Significant Market Share

- North America is expected to have a significant share of the market owing to factors such as increasing cases of cardiovascular surgeries, developed healthcare infrastructure, new product launches, and the presence of established players in the region.

- The United States is projected to dominate the market in the region due to the increasing number of cardiovascular surgeries nationwide. For instance, an article published by the Current Cardiology Reviews in May 2023 stated that trans-radial cardiac catheterization (TRA) witnessed a significant rise in the United States during the last few years.

- The number of heart transplants in the United States is also increasing. For instance, the University of Rochester Medical Center Rochester stated in January 2024 that the Strong Memorial Hospital had 40 life-saving heart transplantation surgeries in 2023, an 82% increase over the previous year (2022). Additionally, the data released by Cedars-Sinai in January 2022 revealed that coronary artery bypass graft surgery (CABG), alternatively referred to as coronary artery bypass or bypass surgery, remains the prevailing cardiac surgical procedure in the United States. Additionally, over 300,000 individuals in the United States undergo successful bypass surgery annually. Hence, radial compression devices play an important role in effective cardiac surgeries.

- Furthermore, new product launches by the key companies from the region are expected to boost the market. For instance, in March 2022, Medical Ingenuities conducted commercial cases with a transformational radial hemostasis band system, PH Band, to achieve patent hemostasis at Lakewood Ranch Medical Center, United States. All cases were successful and demonstrated the unique benefits of the PH Band compared to other radial bands. Hence, owing to the increasing burden of cardiovascular disease that requires surgical intervention and the adoption of advanced radial compression devices, the market studied is anticipated to grow significantly in North America.

Radial Artery Compression Devices Industry Overview

The radial artery compression devices market is fragmented due to the presence of several companies operating globally and regionally. The competitive landscape includes an analysis of a few international and local companies holding market shares. Some of the key market players include Terumo Corporation, Abbott, Teleflex Incorporated, Lepu Medical Technology (Beijing) Co. Ltd, and TZ Medical Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Prevelance of Cardiovascular Diseases

- 4.2.2 Growing Preference for Radial Artery Access

- 4.3 Market Restraints

- 4.3.1 Variability in Reimbursement Policies

- 4.3.2 Potential Complications at the Access Site

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1 By Product

- 5.1.1 Band/Strap Based

- 5.1.2 Knob-based

- 5.1.3 Plate-based

- 5.2 By Usage

- 5.2.1 Replaceable Device

- 5.2.2 Resuable Device

- 5.3 By Application

- 5.3.1 Surgical Intervention

- 5.3.2 Diagnostics

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Ambulatory Surgical Centers

- 5.4.3 Other End Users

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Terumo Corporation

- 6.1.2 Abbott

- 6.1.3 Teleflex Incorporated

- 6.1.4 Semler Technologies Inc.

- 6.1.5 VYGON

- 6.1.6 Merit Medical Systems

- 6.1.7 Beijing Demax Medical Technology

- 6.1.8 Forge Medical

- 6.1.9 TZ Medical, Inc.

- 6.1.10 Lepu Medical Technology (Beijing) Co. Ltd

- 6.1.11 Advin Health Care