|

시장보고서

상품코드

1521787

주입 약물 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2024-2029년)Infused Drugs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

주입 약물 시장 규모는 2024년 85억 달러로 추정되고, 2029년 115억 달러에 이를 것으로 예측되며, 예측기간 중(2024-2029년) CAGR은 7.30%로 성장할 전망입니다.

주입 약물 시장의 성장을 가속하는 주요 요인은 만성 질환의 만연, 약물 전달 시스템의 진보, 노인 인구 증가입니다. 예를 들어, 2022년 아시아태평양의 60세 이상 인구는 약 6억 7,000만 명으로 약 7명 중 1명을 차지합니다. 2050년에는 그 수가 두 배로 13억 명이 될 것으로 예상됩니다. 유엔 아시아태평양경제사회위원회 보고서에 따르면 아시아 노인 인구 중 여성은 54%를 차지하며 평균 수명이 길어 연령에 따라 증가하는 경향이 있습니다. 노인 인구 증가는 예측 기간 동안 시장의 견인 역할이 될 것으로 예상됩니다.

주요 하이라이트

- 또한, 심혈관 질환, 종양 질환, 당뇨병 등 만성 질환의 유병률 증가가 시장 성장에 기여하고 있습니다. 예를 들어, 영국 심장재단(BHF)이 2023년 4월에 발표한 보고서에 따르면, 2022년에는 영국에서 760만명 이상이 심장 및 순환기 질환을 가지고 생활하고 있어, 고령화, 출생율의 감소, 다른 만성 질환에서 생존율 증가로 인해 더 증가할 것으로 예상됩니다. 따라서 만성질환의 유병률 증가는 이러한 질환을 효과적으로 관리하기 위한 주입 약물에 대한 수요를 증가시키고 결국 연구시장을 견인할 것으로 예상됩니다.

- 게다가 인수 및 제품 출시 등 전략적 활동 증가도 시장을 견인할 것으로 예상됩니다. 예를 들어, Bristol Myers Squibb는 2024년 3월 재발 또는 난치성 만성 림프성 백혈병(CLL) 성인 환자의 치료로서 CD19 지향성 키메라 항원 수용체(CAR) T 세포 요법인 생물학적 제제 'Breyanzi' 승인을 미국 식품의약국에서 취득했습니다. Breyanzi는 CAR 양성 생존 T 세포를 포함한 한 번 복용량의 드립 정주로 끝나는 치료 과정을 통해 투여됩니다. 이러한 제품의 출시는 예측 기간 동안 시장을 견인할 것으로 예상됩니다.

- 그러나 주입 약물과 관련된 부작용, 엄격한 규제, 주입 약물 제조 및 시장 개척의 고비용은 주입 약물 시장의 성장을 제한할 수 있습니다.

주입 약물 시장 동향

예측 기간 동안 암 영역이 큰 시장 점유율을 차지할 전망

- 암 유병률 증가는 암 환자에 대한 신속한 작용으로부터 주입 약물 수요를 증가시킬 것으로 예상되고 있습니다. 예를 들어, 2023년 1월에 Spanish Network Of Cancer Registries가 발표한 보고서에 따르면, 2023년 스페인에서 보고된 신규 사례는 약 29만 5,675건으로, 2022년에 비해 1.96% 증가하고 있습니다. 암 유병률 증가는 주입 약물 수요를 촉진할 것으로 예상됩니다.

- 또한 암 영역에서 신약의 연구 개발을 위한 자금도 증가하고 있습니다. 예를 들어 미국에서는 미국 국립위생연구소(NIH)가 암과 관련된 연구활동에 2022년 76억 3,500만 달러에 대해, 2023년에는 80억 7,800만 달러를 투자하고 있습니다. 이러한 암 영역에서 시장 개척 활동에 의해 동 시장에 있어서의 신규 주입형 항암제 증가가 기대됩니다.

- 또한 제품 출시 등 전략적 활동 증가는 암 영역의 성장을 가속할 것으로 예상됩니다. 예를 들어, 2022년 10월 미국 식품의약국은 재발 및 난치성 다발성 골수종의 치료로서 Teclistamab-cqvy(Tecvayli)를 승인했습니다.

- 따라서 암 유병률의 상승 및 제품 출시 증가는 예측기간 동안 같은 부문의 성장을 가속할 것으로 예상됩니다.

북미가 큰 시장 점유율을 차지

- 북미의 주입 약물 시장은 암이나 감염증 등 만성질환의 유병률 상승, 연구개발 활동 투자 증가 등의 요인으로 예측기간 동안 성장할 것으로 전망됩니다. 또한 주요 기업에 의한 제품 출시 및 인수 등 전략적 활동 증가도 이 지역 시장을 견인할 것으로 예상됩니다.

- 암 등 만성질환의 유병률 상승은 종양학에서 사용되는 특수치료 수요를 증가시킬 것으로 예상됩니다. 예를 들어, 미국 암 협회가 2023년에 갱신한 데이터에 따르면, 미국에서는 폐암의 이환율이 증가하고 있으며, 2022년에는 23만 6,740명의 폐암 환자가 보고된 반면, 2023년에 는 23만 8,340명의 폐암 환자가 보고되었습니다. 마찬가지로 캐나다암협회가 2024년 1월에 갱신한 데이터에 따르면 2023년에는 남성 약 12만 4,200명, 여성 약 11만 4,900명이 암으로 진단된 것으로 추정되고 있습니다. 전립선암은 2023년 남성의 신규암 사례의 5분의 1(20%)을 차지하고 있습니다. 따라서 북미의 암환자의 대폭적인 유병률은 주입 약물 수요에 박차를 가할 것으로 예측됩니다.

- 정부와 민간조직에 의한 연구개발 투자 증가도 북미 시장을 견인할 것으로 예상됩니다. 예를 들어, 2023년 11월, 전미 다발성 경화증 협회는 새로운 연구 프로젝트에 440만 달러를 투자해, '치료에의 길(Pathways to Cure)'의 로드맵에 개설된 유망 부문에 세계의 MS 연구를 유도하는 전략에 부합했습니다. 또한 미국에서는 2023년 3월 Bayer AG가 의약품 연구개발에 10억 달러의 투자를 계획하고 있습니다. 이러한 연구개발에 대한 막대한 투자는 신규성이 높은 제품 출시로 이어질 수 있습니다.

- 따라서 암환자의 유병률 상승과 정부와 민간조직에 의한 연구개발 투자 증가는 예측기간에 걸쳐 북미 시장을 견인할 것으로 예상됩니다.

주입 약물 산업 개요

주입 약물 시장의 경쟁은 중간 정도입니다. 주요 기업은 시장 출시를 강화하기 위해 제품 출시, 제품 서비스의 새로운 지역 확대, 합병, 인수, 새로운 파트너십 및 제휴 체결 등 다양한 전략을 채택하고 있습니다. 주요 기업에는 AstraZeneca, Sanofi SA, Teva Pharmaceutical Industries Ltd, Amgen, Inc., Bristol-Myers Squibb Company 등이 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- 만성질환의 유병률 증가

- 고령자 인구 증가

- 시장 성장 억제요인

- 투약에 따른 부작용

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자 및 소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화(시장 규모-달러)

- 의약품 유형별

- 저분자 의약품

- 생물제제

- 치료 영역별

- 암 영역

- 소화기 질환

- 류마티스 관절

- 면역 결핍

- 심장병학

- 신경학

- 당뇨병

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC 국가

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 기업 프로파일

- AstraZeneca

- Sanofi SA

- Pfizer Inc.

- Weefsel Pharma

- Parenteral Drugs(India) Limited

- Bristol-Myers Squibb Company

- Regeneron Pharmaceuticals Inc.

- Eisai Co. Ltd

- Amgen Inc.

- Teva Pharmaceutical Industries Ltd

제7장 시장 기회 및 향후 동향

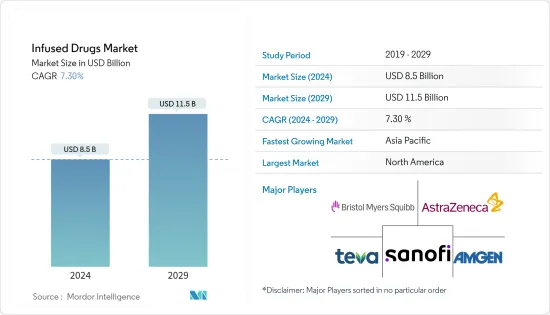

AJY 24.08.08The Infused Drugs Market size is estimated at USD 8.5 billion in 2024, and is expected to reach USD 11.5 billion by 2029, growing at a CAGR of 7.30% during the forecast period (2024-2029).

The key factors driving the growth of the infused drugs market are the growing prevalence of chronic diseases, advancements in drug delivery systems, and the rising geriatric population. For instance, in 2022, there were approximately 670 million people aged 60 years or older in Asia-Pacific, which accounted for roughly one in every seven people in the region. By 2050, the number is projected to be doubled to 1.3 billion. Among the elderly population in Asia, women comprise 54%, and this tends to increase with age due to their long life expectancy, according to a report by the United Nations Economic and Social Commission for Asia and the Pacific. The rising geriatric population is expected to drive the market over the forecast period.

Key Highlights

- Moreover, the increasing prevalence of chronic conditions such as cardiovascular diseases, oncology diseases, and diabetes contribute to the market's growth. For instance, according to the report published by the British Heart Foundation (BHF) in April 2023, more than 7.6 million people were living with heart and circulatory diseases in the United Kingdom in 2022, which is further projected to increase with the aging population, decreasing fertility rates, and increasing survivability from other chronic diseases. Hence, the rising prevalence of chronic diseases is expected to increase the demand for infused drugs to effectively manage these diseases, ultimately driving the market studied market.

- Furthermore, increasing strategic activities such as acquisitions and product launches are also expected to drive the market. For instance, in March 2024, Bristol Myers Squibb received approval from the United States Food and Drug Administration for a biological product, Breyanzi, a CD19-directed chimeric antigen receptor (CAR) T cell therapy, for the treatment of adult patients with relapsed or refractory chronic lymphocytic leukemia (CLL). Breyanzi is delivered through a treatment process that culminates in a one-time infusion with a single dose containing CAR-positive viable T cells. Such product launches are expected to drive the market over the forecast period.

- However, the side effects associated with infusion drugs, strict regulations, and the high cost of manufacturing and developing infusion drugs may restrict the growth of the infused drugs market.

Infused Drugs Market Trends

Oncology is Expected to Have Significant Market Share During the Forecast Period

- The rising prevalence of cancer is expected to increase the demand for infused drugs because of their rapid action in cancer patients. For instance, according to the report published by the Spanish Network Of Cancer Registries in January 2023, about 295,675 new cases were reported in Spain in 2023, which represented 1.96% more compared to 2022. The increasing prevalence of cancer is expected to drive the demand for infused drugs.

- Moreover, the funding for research and development of novel medicines in oncology is increasing. For instance, in the United States, the National Institute of Health (NIH) invested USD 8,078 million in 2023 compared to 7,635 million in 2022 for its research activities associated with cancer. Such development activities in oncology are expected to increase the novel infused anti-cancer medicines in the market.

- Furthermore, the increasing strategic activities, such as product launches, are expected to drive the growth of the oncology segment. For instance, in October 2022, the United States Food and Drug Administration approved the Teclistamab-cqvy (Tecvayli), for the treatment of relapsed/refractory multiple myeloma.

- Therefore, the rising prevalence of cancer and increasing product launches are expected to drive the growth of the segment over the forecast period.

North America Holds Significant Market Share

- The North American infused drugs market is expected to grow over the forecast period owing to factors such as the rising prevalence of chronic diseases, such as cancer and infectious diseases, coupled with the increasing investment in research and development activities. Increasing strategic activities such as product launches and acquisitions by key players are also expected to drive the market in the region.

- The rising prevalence of chronic diseases such as cancer is expected to increase the demand for specialty therapeutics that are used in oncology. For instance, according to the American Cancer Society's updated data in 2023, the incidence of lung cancer is increasing in the United States, and the country reported 238,340 lung cancer cases in 2023 compared to 236,740 in 2022. Similarly, as per the Canadian Cancer Society's updated data from January 2024, it was estimated that in 2023, around 124,200 males and 114,900 females were diagnosed with cancer. Prostate cancer accounts for one-fifth (20%) of all new cancer cases in males in 2023. Hence, the significant prevalence of cancer cases in North America is projected to spur the demand for infused drugs.

- The increasing investments in research and development by governments and private organizations are also expected to drive the market in North America. For instance, in November 2023, the National Multiple Sclerosis Society invested USD 4.4 million in new research projects, aligning with the strategy to guide global MS research toward promising areas outlined in the Pathways to Cure's roadmap. Furthermore, in March 2023, in the United States, Bayer AG planned to invest USD 1.0 billion in the research and development of drugs. Such huge investments in research and development can lead to novel infusing product launches.

- Hence, the rising prevalence of cancer cases and increasing investments in research and development investments by governments and private organizations are expected to drive the market in North America over the forecast period.

Infused Drugs Industry Overview

The infused drugs market is moderately competitive. The key players are adopting various strategies such as product launches, expansion of the products and services into new regions, mergers, acquisitions, and entering new partnerships and collaborations to strengthen their position in the market. The key players include AstraZeneca, Sanofi SA, Teva Pharmaceutical Industries Ltd, Amgen, Inc., and Bristol-Myers Squibb Company.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increase in the Prevalence of Chronic Diseases

- 4.2.2 Increasing Geriatric Population

- 4.3 Market Restraints

- 4.3.1 Side Effects Associated with the Medications

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1 By Drug Type

- 5.1.1 Small Molecules

- 5.1.2 Biologics

- 5.2 By Therapeutic Area

- 5.2.1 Oncology

- 5.2.2 Gastrointestinal Diseases

- 5.2.3 Rheumatoid Arthritis

- 5.2.4 Immune Deficiencies

- 5.2.5 Cardiology

- 5.2.6 Neurology

- 5.2.7 Diabetes

- 5.2.8 Other Therapeutic Areas

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 AstraZeneca

- 6.1.2 Sanofi SA

- 6.1.3 Pfizer Inc.

- 6.1.4 Weefsel Pharma

- 6.1.5 Parenteral Drugs (India) Limited

- 6.1.6 Bristol-Myers Squibb Company

- 6.1.7 Regeneron Pharmaceuticals Inc.

- 6.1.8 Eisai Co. Ltd

- 6.1.9 Amgen Inc.

- 6.1.10 Teva Pharmaceutical Industries Ltd