|

시장보고서

상품코드

1521791

전자 데이터 캡처 시스템 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2024-2029년)Electronic Data Capture Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

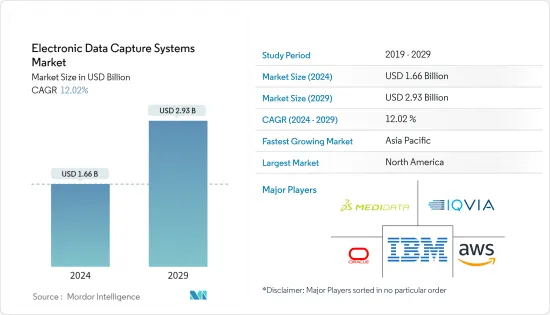

전자 데이터 캡처 시스템 시장 규모는 2024년 16억 6,000만 달러로 추정되며, 2029년에는 29억 3,000만 달러에 달할 것으로 예상되며, 예측 기간(2024-2029년) 동안 12.02%의 CAGR로 성장할 것으로 예상됩니다.

분산형 임상시험의 증가는 EDC 시스템이 의학 연구에서 추진력을 얻게 될 것으로 보입니다. 2023년 4월에 발표된 논문에 따르면, COVID-19 사태로 인해 임상시험의 약 68%가 중단된 것이 가상 임상시험 모델과 하이브리드 임상시험 모델의 채택이 급증한 원인으로 분석됐습니다. 분산형 임상시험에서는 적절한 데이터 관리가 매우 중요하기 때문에 EDC 시스템이 중요한 역할을 합니다. 임상시험 서비스 기업들은 제휴와 인수를 통해 서비스 제공을 확대하고 있습니다. 예를 들어, 2023년 7월 시그넌트 헬스(Signant Health)는 분산형 임상시험 및 시설 기반 임상시험을 위한 직접 데이터 캡처 및 전자 데이터 캡처 기술을 제공하는 DSG의 인수를 발표했습니다. 이번 인수를 통해 회사는 임상시험의 규모와 종류에 관계없이 종합적인 디지털 솔루션을 제공할 수 있게 됐습니다. 이러한 새로운 시장 진입은 기존의 경쟁력과 효율성을 가속화 할 가능성이 높습니다.

미국 FDA와 같은 규제 기관은 임상시험 데이터 기록에 EDC 시스템을 채택하는 최종사용자에게 권고하고 있습니다. 임상시험 계획서에 따라 임상시험 의뢰자는 시스템에 대한 자세한 설명과 시스템 관리, 시스템 사용에 대한 직원 교육 및 액세스 제어에 대한 정보를 제공해야 합니다. 규제 당국의 개입을 통해 기업은 철저한 품질 검사를 수행하고 데이터를 보호하기 위한 보안 보호 수단을 제공함으로써 제품 결함의 위험을 최소화할 수 있습니다. 따라서 규제 준수 및 권장 사항은 최종사용자의 EDC 시스템 사용을 촉진하고 전체 시장의 성장을 촉진하고 있습니다.

그러나 시스템 라이선스 및 호스팅 비용이 높아 시장 성장에 걸림돌로 작용할 것으로 예상됩니다. 또한, 신흥 경제국에서는 사이버 인프라가 미비하여 최종사용자가 시스템을 사용하는 것을 억제하고 있습니다.

전자 데이터 캡쳐 시스템 시장 동향

예측 기간 동안 웹 및 클라우드 기반 부문이 큰 시장 점유율을 차지할 것으로 전망

예측 기간 동안 웹 및 클라우드 기반 부문이 큰 시장 점유율을 차지할 것으로 예상됩니다. 클라우드 기반 시스템은 중앙 집중식 데이터베이스이며, 전문가들은 지역 데이터 공유 규정을 준수하기 위해 클라우드 데이터베이스를 지역 또는 지역별로 맞춤화할 수 있습니다. 이러한 장점으로 인해 연구자들은 웹 및 클라우드 기반 접근 방식을 선호하고 있습니다.

자원이 부족한 지역의 기업들은 아마존웹서비스(AWS)나 Oracle과 같은 클라우드 제공업체와 협력하고 있습니다. 예를 들어, 독일에 본사를 둔 헬스 테크 기업 Climedo Health는 AWS를 활용하여 병원, 제약회사, 의료기기 제조업체 및 150개 공공 보건소를 위한 클라우드 기반의 확장 가능한 전자 데이터 캡처 시스템을 개발하고 있습니다. 이 회사는 또한 유럽 전자 데이터 캡처 시스템 시장에서의 입지를 강화하고 미국에서의 입지를 확대하기 위해 2022년 2월에 570만 달러의 투자를 유치한 바 있습니다. 클라우드 기반 솔루션은 제품 개발에 추가 비용을 들이지 않고도 기업의 지역 확장을 용이하게 합니다.

전자 데이터 캡처 시스템 제공을 확대하기 위한 제휴, 출시, 승인 등 시장 기업의 활동은 예측 기간 동안 이 분야의 성장을 촉진할 것으로 예상되며, 2022년 10월 Medidata는 베링거인겔하임과 5년간의 파트너십 갱신을 발표했습니다. 이 계약에 따라 메디데이터는 베링거인겔하임의 임상시험을 위해 Rave EDC 시스템을 전 세계에 공급할 예정입니다.

따라서 데이터의 자유로운 흐름과 데이터 보호를 위한 프로토콜 강화가 결합되어 웹 및 클라우드 기반 전자 데이터 캡처 시스템의 채택률이 높아지면서 이 부문의 성장을 견인할 것으로 보입니다.

예측 기간 동안 북미가 큰 시장 점유율을 차지할 것으로 예상

예측 기간 동안 북미가 가장 큰 시장 점유율을 차지할 것으로 예상됩니다. 이는 시장에서의 입지를 강화하기 위한 전략적 이니셔티브의 증가와 이 지역에서의 임상시험의 증가와 같은 요인에 기인합니다.

북미는 제품 개발에 있어 디지털화와 실험적 연구 채택률이 높은 지역입니다. 예를 들어, 2023년 7월 아스트라제네카, 이그나이트데이터(IgniteData), University College London Hospitals NHS Foundation Trust(UCLH)는 임상시험 환경에서 전자 의료 기록(EHR)에서 전자 데이터 수집(EDC)으로의 데이터 전송을 평가하기 위해 협력했습니다. 데이터 전송을 평가했습니다. 이 공동 연구의 목적 중 하나는 EHR에서 EDC로의 기술 활용을 여러 영역으로 확대하는 것이었습니다. 또한, 이 지역의 신흥 업체들은 다른 지역보다 상대적으로 자금 조달이 용이합니다. 예를 들어, 2022년 11월 미국의 임상시험 소프트웨어 제공업체인 요나링크(YonaLink)는 EHR-EDC 통합 플랫폼을 확장하고 CRO의 채택률을 높이기 위해 600만 달러의 자금 조달을 발표하였습니다. 자금 조달과 공동 연구를 통한 투자 유입은 예측 기간 동안 이 지역의 시장 성장을 촉진할 것으로 예상됩니다.

또한, 이 지역의 EDC 시스템 이용 확대에 대한 헬스케어 기업들의 적극적인 참여도 이 시장의 중요한 성장 결정 요인으로 꼽히고 있습니다. 예를 들어, 2022년 6월 국립의학도서관(National Library of Medicine)에 게재된 논문에 따르면, Discovery Critical Care Research Network Program for Resilience and Emergency Preparedness(Discovery PREP)는 기술 공급업체와 협력하여 미국 내 응급상황에서 다기관 데이터 수집 문제를 해결할 수 있는 EDC 툴을 개발했습니다. 이 연구는 EDC 도구가 다기관 데이터 수집 및 계절성 독감 치료 프로토콜을 평가하기 위해 실행 가능하다는 결론을 내렸습니다. 이러한 연구는 다양한 응용 분야에서 EDC의 사용을 촉진하고 시장 범위를 확대할 것입니다.

따라서, 제품 개발 및 시장 개척을 통한 각 플레이어의 투자 확대 등 위의 요인으로 인해 북미 전자 데이터 캡처 시스템 시장은 예측 기간 동안 지배적인 위치를 유지할 것으로 예상됩니다.

전자 데이터 캡쳐 시스템 산업 개요

전자 데이터 캡처 시스템 시장은 몇몇 대형 업체들에 의해 반쯤은 고정화되어 있습니다. 이들 주요 기업들은 대부분 전 세계적으로 존재감을 드러내고 있으며, 인수 및 제휴와 같은 전략적인 노력을 아끼지 않고 있습니다. 신흥국은 분산형 임상시험 프로그램의 증가로 인해 시장이 급성장하고 있어 경쟁이 치열하게 전개되고 있습니다. 시장 진입 기업으로는 Calyx, Castor, OpenClinica, LLC, Oracle, IQVIA Inc., Medidata Solutions Inc., IBM, Amazon Web Services Inc., Veeva Systems, Wemedoo 등이 있습니다.

기타 혜택:

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 소개

- 조사 가정과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- 임상시험 분산화 진전

- 임상시험중인 데이터 복잡화

- 시장 성장 억제요인

- 높은 도입 비용

- Porter's Five Forces 분석

- 공급 기업의 교섭력

- 구매자/소비자의 협상력

- 신규 참여업체의 위협

- 대체품의 위협

- 경쟁 기업 간의 경쟁 강도

제5장 시장 세분화(시장 규모 - 금액)

- 제공 형태별

- 웹 및 클라우드 기반

- 온프레미스

- 개발 단계별

- 단계 l

- 단계 ll

- 단계 ll

- 단계 lV

- 최종사용자별

- 제약·바이오테크놀러지 기업

- 병원 프로바이더

- 계약 연구기관

- 기타 최종사용자

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카공화국

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 상황

- 기업 개요

- Calyx

- Castor

- OpenClinica LLC

- Oracle

- IQVIA Inc

- Medidata Solutions Inc.

- IBM

- Amazon Web Services Inc.

- Veeva Systems

- Wemedoo

제7장 시장 기회와 향후 동향

ksm 24.08.01The Electronic Data Capture Systems Market size is estimated at USD 1.66 billion in 2024, and is expected to reach USD 2.93 billion by 2029, growing at a CAGR of 12.02% during the forecast period (2024-2029).

An increase in decentralized clinical trials will likely assist EDC systems in gaining momentum in medical research. According to an article published in April 2023, the disruption of around 68% of clinical trials during the pandemic caused the surge in the adoption of virtual and hybrid trial models. Good data management is crucial in decentralized trials; therefore, the EDC system plays a vital role. Companies in clinical trial services are expanding their offerings through collaboration and acquisitions. For instance, in July 2023, Signant Health announced the acquisition of DSG, a direct data capture and electronic data capture technology provider in the eClinical suite for decentralized and site-based clinical trials. This acquisition enabled the company to offer comprehensive digital solutions to any size and type of clinical trial. Thus, new entrants in the market are likely to accelerate the existing competitiveness and efficiency.

Regulatory bodies, such as the US FDA, offer recommendations to end users who employ the EDC system to record data in clinical investigations. As per the clinical investigation protocol, the sponsor must provide an in-detailed description of the system and information on system management, staff training on the use of the system, and access control. The regulatory intervention minimizes the risk of product failure as companies ensure thorough quality checks and offer security safeguards in order to protect the data. Hence, regulatory compliance and recommendations encourage the use of EDC systems among end users, boosting overall market growth.

However, the high cost of licensing and hosting the system is anticipated to hamper market growth. Additionally, under-developed cyberinfrastructure in emerging economies restrains end users from utilizing the system.

Electronic Data Capture Systems Market Trends

The Web and Cloud-Based Segment is Expected to Hold a Significant Market Share Over the Forecast Period

The web and cloud-based segment is estimated to have a substantial market share during the forecast period. A cloud-based system is a centralized database that enables professionals to tailor the cloud database to the region or local specific to adhere to local data sharing regulations. Such advantages increase the preference for the web and cloud-based approach amongst researchers.

Regional players with limited resources collaborate with cloud providers, including Amazon Web Services (AWS) and Oracle. For instance, Climedo Health, a Germany-based health tech company, uses AWS to develop cloud-based and scalable electronic data capture systems for hospitals, pharmaceutical companies, medical device manufacturers, and 150 public health offices. The company also raised USD 5.7 million in February 2022 in order to strengthen its position in the European electronic data capture system market and expand its presence in the United States. Cloud-based solutions ease regional expansion for companies without incurring extra costs for product development.

The activities of market players, such as partnerships, launches, and approvals, to expand their electronic data capture system offerings are expected to boost the segment's growth over the forecast period. In October 2022, Medidata announced the renewal of the partnership with Boehringer Ingelheim for five years. Under this agreement, Medidata is expected to offer its Rave EDC system for Boehringer Ingelheim's clinical trials globally.

Hence, the free flow of data, coupled with strengthening the protocols for data protection, is likely to increase the adoption rate of web and cloud-based electronic data capture systems, resulting in the growth of the segment.

North America is Expected to Hold a Significant Market Share Over the Forecast Period

North America is anticipated to hold a substantial market share during the forecast period. This can be attributed to factors such as increasing strategic initiatives to enhance the market presence and the growing number of clinical trials in the region.

North America has a high adoption rate of digitalization and experimental studies in product development. For instance, in July 2023, AstraZeneca, IgniteData, and University College London Hospitals NHS Foundation Trust (UCLH) collaborated to evaluate data transfer from Electronic Health Records (EHR) to Electronic Data Capture (EDC) in a clinical trial setting. One of the purposes of this collaboration was to expand the usage of EHR-to-EDC technology across multiple domains. Additionally, funding accessibility for emerging players in the region is relatively easier than in other regions. For instance, in November 2022, YonaLink, a US clinical trial software provider, announced that it would raise USD 6 million in funding to expand its integration platform of EHR-to-EDC and increase its adoption rate amongst the CROs. The inflow of investments through funding and collaborative studies is expected to propel market growth in the region during the forecast period.

The active participation of healthcare professionals in scaling up the use of EDC systems in the region is also considered an important growth determinant of the market. For instance, in June 2022, an article published in the National Library of Medicine stated that the Discovery Critical Care Research Network Program for Resilience and Emergency Preparedness (Discovery PREP) collaborated with technology vendors to develop an EDC tool that can address multisite data collection challenges during the emergencies in the United States. The study concluded that the EDC tool is feasible for collecting multisite data and assessing treatment protocols for seasonal influenza. Such studies boost the use of EDC in various applications and enlarge the market scope.

Therefore, owing to the above-mentioned factors, such as the players' growing investments via product development and market expansion, the North American electronic data capture systems market is expected to maintain its dominant position during the forecast period.

Electronic Data Capture Systems Industry Overview

The electronic data capture systems market is semi-consolidated with several major players. Most of these major players enjoy a global presence and indulge in strategic initiatives such as acquisitions and collaborations. Emerging countries are becoming hotspots for significant competition due to the rapidly expanding market fueled by growing decentralized clinical trial programs. Some of the market players include Calyx, Castor, OpenClinica, LLC, Oracle, IQVIA Inc., Medidata Solutions Inc., IBM, Amazon Web Services Inc., Veeva Systems, and Wemedoo.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Decentralized Clinical Trials

- 4.2.2 Increasing Complexity of Data during the Clinical Study

- 4.3 Market Restraints

- 4.3.1 High Implementation Cost

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1 By Delivery Mode

- 5.1.1 Web and Cloud-based

- 5.1.2 On-Premise

- 5.2 By Development Stage

- 5.2.1 Phase l

- 5.2.2 Phase ll

- 5.2.3 Phase lll

- 5.2.4 Phase lV

- 5.3 By End User

- 5.3.1 Pharmaceutical and Biotechnology Firms

- 5.3.2 Hospitals Providers

- 5.3.3 Contract Research Organisations

- 5.3.4 Other End Users

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Calyx

- 6.1.2 Castor

- 6.1.3 OpenClinica LLC

- 6.1.4 Oracle

- 6.1.5 IQVIA Inc

- 6.1.6 Medidata Solutions Inc.

- 6.1.7 IBM

- 6.1.8 Amazon Web Services Inc.

- 6.1.9 Veeva Systems

- 6.1.10 Wemedoo