|

시장보고서

상품코드

1521844

일본의 데이터센터 물리적 보안 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2024-2029년)Japan Data Center Physical Security - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

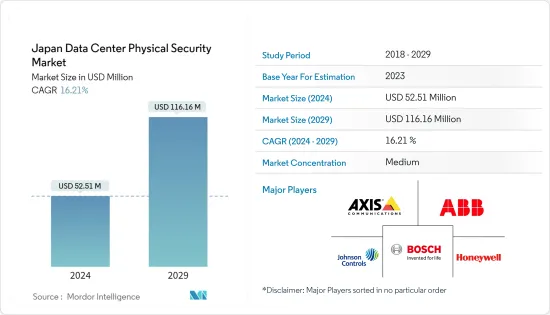

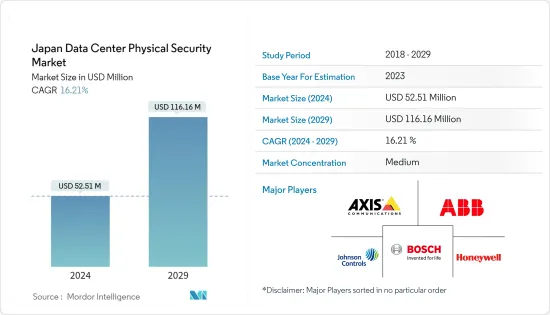

일본의 데이터센터 물리적 보안 시장 규모는 2024년 5,251만 달러로 추정되며, 2029년에는 1억 1,616만 달러에 달할 것으로 예상되며, 예측 기간(2024-2029) 동안 16.21%의 CAGR로 성장할 것으로 예상됩니다.

보안 대책은 경계 보안, 시설 관리, 전산실 관리, 캐비닛 관리 등 4단계로 분류할 수 있습니다. 데이터센터 보안의 첫 번째 층은 경계에서 인원의 무단 침입을 차단, 감지, 지연시킵니다. 경계 감시가 위반되면 두 번째 방어 계층은 접근을 거부합니다. 이는 카드 스와이프 또는 생체인식을 이용한 출입 통제 시스템입니다.

제3의 물리적 보안 계층은 모든 제한 구역의 모니터링, 회전식 개찰구와 같은 출입 제한 배치, 손가락, 지문, 홍채, 혈관 패턴 등을 확인하는 생체인식 출입 통제 장치 제공, VCA 제공, 무선 주파수 식별 사용 등 다양한 검증 방법을 통해 출입을 더욱 제한합니다. 처음 세 계층은 허가된 사람만 출입할 수 있도록 보장합니다. 출입을 제한하는 추가 보안에는 캐비닛 잠금 장치가 포함됩니다. 이 계층은 악의적 인 직원과 같은 "내부 위협"에 대한 두려움을 해결합니다.

주요 하이라이트

- 건설 중인 IT 부하 용량: 일본 데이터센터 물리적 보안 시장의 향후 IT 부하 용량은 2029년까지 2,000MW에 달할 것으로 예상됩니다.

- 건설 중인 고층 공간: 일본의 바닥 면적은 2029년까지 1,000만 평방피트까지 증가할 것으로 예상됩니다.

- 계획 중인 랙: 2029년까지 국내 설치되는 랙의 총 수는 50만 개에 달할 것으로 예상되며, 2029년에는 도쿄에 가장 많은 수의 랙이 설치될 것으로 예상됩니다.

- 계획 중인 해저 케이블: 필리핀을 연결하는 해저 케이블 시스템은 거의 30개에 달하며, 대부분 건설 중. 2023년 서비스 개시 예정인 해저 케이블 중 하나는 동남아시아-일본 케이블 2(SJC2)로, 센쿠라(일본)에서 시마(일본)까지의 지점까지 10,500km가 넘는 길이의 해저 케이블입니다.

일본 데이터센터 물리적 보안 시장 동향

비디오 감시 부문이 가장 큰 비중을 차지

- 데이터센터에는 기밀성이 높은 중요한 데이터가 저장되어 있기 때문에 보안이 최우선 과제입니다. 데이터센터 사업자들은 보안 기준과 규제를 준수하기 위해 비디오 감시 시스템을 활용하고 있습니다. 이를 통해 액세스를 모니터링하고, 무단 액세스를 감지하고, 규정 준수를 유지할 수 있습니다.

- 데이터 보호법은 데이터센터 사업자에게 엄격한 요구 사항을 규정하고 있습니다. 비디오 모니터링은 물리적 보안 조치를 개선하여 컴플라이언스를 준수하는 데 도움이 됩니다.

- 2021년 일본 가정의 스마트폰 보급률은 89%에 육박했습니다. 최근 몇 년 동안 사람들이 모바일 인터넷을 사용하는 평균 시간이 증가하여 E-Commerce와 같은 관련 산업에 비즈니스 기회를 가져 왔습니다. 온라인 쇼핑 플랫폼의 등장으로 중소기업들도 온라인 결제 방식으로 전환하여 E-Commerce 세계에서 디지털 존재감을 드러내고 있습니다. 전통 있는 대기업들조차도 E-Commerce 플랫폼을 기존 비즈니스 형태에 통합하고 있습니다. 그 결과 데이터 트래픽이 증가하고, 데이터센터가 증가하고, 비디오 모니터링에 대한 수요가 증가하게 됩니다. 이는 사용자의 데이터센터에 대한 악의적인 조작이나 오작동을 방지하고, 사고 발생 시 책임자를 식별할 수 있는 증거가 될 수 있습니다.

- 일본의 인터넷 사용자는 2021년에서 2022년까지 84만 4,000명 증가(0.7% 증가)했습니다. COVID-19로 인해 가정 내 화상회의, 원격 학습, 비디오 스트리밍이 급증하면서 2020년 인터넷 트래픽은 2019년 COVID-19 이전 수준 대비 1.6배 증가했습니다. 또한, 커넥티드 디바이스와 스마트홈의 사용 증가로 디지털 데이터에 대한 수요가 증가하면서 네트워크 트래픽이 개선되었습니다. 이로 인해 중국은 이 지역에서 모바일 상거래의 선구자 중 하나가 되었습니다. 이는 전체 데이터센터의 데이터 소비 증가를 의미하며, 이는 데이터센터 물리적 보안 시장을 촉진할 것입니다.

- 2021년 초부터 일본 이동통신사들은 5G의 보급에 박차를 가하고 있습니다. 국제통신부는 일본의 5G 경험을 더욱 발전시키고자 했습니다. 그 목표는 2024년 3월 말까지 5G 인구 커버리지 98%를 달성하는 것이었습니다. 전반적으로 일본은 5G 서비스에 사용할 수 있는 주파수의 수를 늘리고자 합니다. 통신 산업의 성장은 데이터센터의 규모를 확대하여 비디오 감시의 필요성을 증가시켰습니다. 영상 감시는 강력한 억제 효과가 있어 물리적 공격과 중요한 데이터에 대한 무단 액세스 가능성을 줄여줍니다.

IT 및 통신 부문이 주요 점유율을 차지

- 일본에는 소니, 파나소닉, 후지쯔, NEC, 도시바 등 주요 ICT 기업이 있으며, ICT의 주요 거점으로서 일본의 확장에 중요한 역할을 하고 있습니다. 또한, 일본 내 수많은 현대화 및 확장 프로젝트와 고품질 및 첨단 인프라를 유지하기 위한 정부 지출 증가도 시장 성장에 기여하고 있습니다.

- 일본 정부는 민간 부문의 디지털 전환을 가속화하고 신흥 중소기업을 지원하기 위해 노력하고 있으며, 2021년 일본 경제산업성과 총무성이 주도하는 일본 정부는 특히 중소기업을 대상으로 한 조직 내 디지털 전환 추진을 위한 가이드라인을 발표했습니다. 가이드라인을 발표했습니다. 같은 해 AI, 사이버 보안, 안전한 클라우드 서비스 도입에 관한 가이드라인도 발표됐습니다.

- 정부는 5G와 현재 LTE(Long Term Evolution)보다 더 빠른 데이터 전송이 가능한 다른 첨단 기술의 보급을 지속적으로 추진하고 있으며, NTT도코모, KDDI, 소프트뱅크, 라쿠텐 모바일은 2019년 4월 총무성으로부터 5G 주파수 대역을 각각 할당받았습니다. 를 할당받았습니다. 이들 4개 통신사는 2020년에 5G 통신 서비스를 시작했습니다. 이 시나리오는 데이터 소비와 데이터센터 이용을 증가시켜 조사 대상 시장의 성장을 촉진할 수 있습니다.

- 일본 정부 디지털청은 중앙 관공서와 지방 관공서 모두에서 클라우드 서비스 이용을 추진하고 있습니다. 예를 들어, 디지털청은 2022년 10월에 정부 기관이 연내 '정부 클라우드' 서비스를 도입할 것이라고 발표했습니다.

- 일본 경제산업성은 2017년도부터 클라우드 서비스를 포함한 IT 투자를 하는 조직에 'IT 도입 보조금'을 지급하고 있습니다. 후생노동성은 2021년 COVID-19의 영향을 받은 조직에 '일하는 방식 개혁 추진' 보조금을 지급하여 원격 근무로의 전환을 지원했습니다. 후생노동성은 중소기업이 클라우드 서비스 및 기타 IT 장비와 계약할 때 계약금과 장비 비용을 지원합니다.

일본의 데이터센터 물리적 보안 산업 개요

Axis Communications AB, ABB Ltd, Bosch Sicherheitssysteme GmbH와 같은 플레이어가 기업의 역량 향상에 중요한 역할을 하기 때문에 시장은 매우 세분화되어 있습니다. 시장 지향성은 고도의 경쟁 환경으로 이어집니다. 소매 및 도매 데이터센터 시장의 가장 큰 기업들은 도난으로부터 시스템을 보호하고 보안을 강화하기 위해 노력하고 있습니다. 중소기업은 경쟁에서 이기기 위해 생산 규모를 확대하려 하고, 대기업은 시장 지위를 유지하기 위해 제품 혁신과 출시에 중점을 두기 때문에 시장에 통합의 물결이 밀려오고 있습니다. 예를 들어

2023년 4월, 슈나이더일렉트릭은 모듈형 데이터센터 에코케어(EcoCare for Modular Data Centers)라는 새로운 서비스를 출시했습니다. 이 혁신적인 서비스 플랜의 회원은 모듈형 데이터센터의 가동 시간을 최대화하기 위해 24시간 365일 사전 예방적 원격 모니터링과 상태 기반 유지보수를 통해 슈나이더 일렉트릭의 전문지식을 활용할 수 있습니다. 회원 전용 지원에는 전담 고객 성공 관리팀이 포함되며, 원격 서비스 팀과 현장 서비스 팀을 지휘하여 문제 발생 시 각 자산에 대한 단편적인 접근 방식이 아닌 시스템 차원의 인프라 및 유지보수 요구사항을 시스템 수준에서 인프라 및 유지보수 요구사항에 대응합니다.

기타 혜택:

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 소개

- 조사 가정과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- 데이터 트래픽 증가와 안전한 연결성에 대한 요구가 데이터센터 물리적 보안 시장 성장을 촉진

- 사이버 위협 증가가 데이터센터 물리적 보안 시장 성장을 촉진

- 시장 성장 억제요인

- 한정된 IT 예산, 저비용 대체품의 입수 가능성, 불법 복제가 데이터센터 물리적 보안 시장 잠재적 성장을 저해하고 있습니다.

- 밸류체인/공급망 분석

- 업계의 매력 - Porter's Five Forces 분석

- 신규 참여업체의 위협

- 구매자/소비자의 협상력

- 공급 기업의 교섭력

- 대체품의 위협

- 경쟁 기업 간의 경쟁 강도

- COVID-19의 영향 평가

제5장 시장 세분화

- 솔루션 유형별

- 비디오 감시

- 입퇴실 관리 솔루션

- 기타(맨트랩, 펜스, 모니터링 솔루션)

- 서비스 유형별

- 컨설팅 서비스

- 전문 서비스

- 기타(시스템 통합 서비스)

- 최종사용자

- IT·통신

- BFSI

- 정부기관

- 헬스케어

- 기타 최종사용자

제6장 경쟁 상황

- 기업 개요

- Axis Communications AB

- ABB Ltd

- Bosch Sicherheitssysteme GmbH

- Honeywell International Inc.

- Johnson Controls

- Schneider Electric

- ASSA ABLOY

- Cisco Systems Inc.

- Boon Edam

- Dahua Technology

제7장 투자 분석

제8장 시장 기회와 향후 동향

ksm 24.08.01The Japan Data Center Physical Security Market size is estimated at USD 52.51 million in 2024, and is expected to reach USD 116.16 million by 2029, growing at a CAGR of 16.21% during the forecast period (2024-2029).

Security measures can be categorized into four layers, i.e., perimeter security, facility controls, computer room controls, and cabinet controls. The first layer of data center security discourages, detects, and delays any unauthorized entry of personnel at the perimeter. In case of any infringement in the perimeter monitoring, the second layer of defense denies access. It is an access control system utilizing card swipes or biometrics.

The third layer of physical security further restricts access through various verification methods, including monitoring all restricted areas, deploying entry restrictions such as turnstiles, providing biometric access control devices to verify finger and thumbprints, irises, or vascular patterns, providing VCA, and using radio frequency identification. The first three layers ensure the entry of only authorized people. Further security to restrict admission includes cabinet locking mechanisms. This layer addresses the fear of an 'insider threat,' such as a malicious employee.

Key Highlights

- Under Construction IT Load Capacity: The upcoming IT load capacity of the Japanese data center physical security market is expected to reach 2,000 MW by 2029.

- Under Construction Raised Floor Space: The country's construction of raised floor area is expected to increase to 10 million sq. ft by 2029.

- Planned Racks: The country's total number of racks to be installed is expected to reach 500 K units by 2029. Tokyo is expected to house the maximum number of racks by 2029.

- Planned Submarine Cables: There are close to 30 submarine cable systems connecting the Philippines, and many are under construction. One such submarine cable that is estimated to start service in 2023 was the Southeast Asia-Japan Cable 2 (SJC2), which stretches over 10,500 kilometers with landing points from Chikura, Japan, to Shima, Japan.

Japan Data Center Physical Security Market Trends

The Video Surveillance Segment Holds Significant Share

- Sensitive and important data are stored in data centers, so security is a top priority. Data center operators use video surveillance systems to ensure that security standards and regulations are met. This allows one to monitor access, detect unauthorized access, and maintain compliance.

- Data protection laws set strict requirements for data center operators. Video surveillance can help maintain compliance by improving physical security measures.

- In 2021, the smartphone penetration rate in Japanese households was nearly 89%. In recent years, the average amount of time people spend using mobile internet has increased, creating business opportunities for related industries such as e-commerce. With the advent of online shopping platforms, small and medium-sized businesses are also switching to online payment methods and a digital presence in the world of e-commerce. Even large, well-established companies are integrating e-commerce platforms with traditional forms of business. This leads to an increase in data traffic and, thus, an increase in data centers and, in turn, an increase in the demand for video surveillance. This helps prevent malicious or erroneous operations in the user's data center and provides evidence to identify those responsible in the event of an incident.

- Internet users in Japan increased by 844 thousand (+0.7%) between 2021 and 2022. Internet traffic increased 1.6x in 2020 compared to pre-COVID-19 levels in 2019 as the pandemic led to a surge in home video conferencing, distance learning, and video streaming. In addition, the increased use of connected devices and smart homes increased the demand for digital data and improved network traffic. This makes the country one of the pioneers of mobile commerce in the region. This means an increase in data consumption across data centers, thereby boosting the data center physical security market.

- Since the beginning of 2021, Japanese mobile phone companies have been accelerating the rollout of 5G. The Ministry of International Communications wanted to advance Japan's 5G experience further. The goal was to achieve 98% 5G population coverage by the end of March 2024. Overall, Japan wants to increase the number of frequencies available for its 5G services. The growth of the telecommunications industry is increasing the size of data centers, thereby increasing the need for video surveillance. Video surveillance has a powerful deterrent effect, reducing the likelihood of physical attacks and unauthorized access to critical data.

The IT and Telecommunication Segment Holds the Major Share

- Japan is home to major ICT organizations such as Sony, Panasonic, Fujitsu, NEC, and Toshiba, which continue to play a key role in the country's expansion as a major center for ICT. In addition, the orderly development of numerous modernization and expansion projects in the country, along with increasing government spending on maintaining high-quality and advanced infrastructure, are also driving the growth of the market.

- The Japanese government is making efforts to accelerate the digital transformation of the private sector and support emerging SMEs. In 2021, the Japanese government, led by the Ministry of Economy, Trade and Industry and the Ministry of Internal Affairs and Communications, published guidelines for promoting digital transformation within organizations, especially targeting small and medium-sized enterprises. Similarly, guidelines on implementing AI, cybersecurity, and secure cloud services were also published in the same year.

- The government is continuing to push the rollout of 5G and other cutting-edge technologies capable of transferring data at even higher rates than currently possible with long-term evolution (LTE). NTT DOCOMO, KDDI, Softbank, and Rakuten Mobile were each allocated a 5G spectrum by the Ministry of Internal Affairs and Communication (MIC) in April 2019. These four mobile service providers launched 5G telecommunication services in 2020. This scenario may increase the consumption of data and use of data centers, thereby driving the growth of the market studied.

- The Government of Japan's Digital Agency promotes the utilization of cloud services for both central and local government offices. For instance, the Digital Agency announced in October 2022 that the government agencies would adopt "Government Cloud" services for the fiscal year.

- The Ministry of Economics, Trade and Industry (METI) provided an IT Adoption Subsidy to organizations investing in IT, including cloud services, from FY 2017. In 2021, the Ministry of Health, Labour and Welfare (MHLW) provided organizations affected by the COVID-19 pandemic with a "Workstyle Reform Promotion" subsidy to help them transition to remote work. MHLW supports SMEs to cover the contracting fees and equipment costs of cloud services and other IT devices.

Japan Data Center Physical Security Industry Overview

The market is highly fragmented due to players like Axis Communications AB, ABB Ltd, and Bosch Sicherheitssysteme GmbH, which play a vital role in upscaling the capabilities of enterprises. Market orientation leads to a highly competitive environment. The biggest retail and wholesale data center market companies are trying to make their system secure and safe from thefts. There has been a wave of consolidation in the market as smaller players seek to scale up their production to compete, and big companies are focusing on product innovation and launches to maintain their market position. For instance,

In April 2023, Schneider Electric launched a new service offer, EcoCare for Modular Data Centers. Members of this innovative service plan benefit from specialized expertise to maximize modular data centers' uptime with 24/7 proactive remote monitoring and condition-based maintenance. Members benefit from exclusive support, which includes a dedicated customer success management team, who become their go-to coach, orchestrating remote and on-site services teams and addressing infrastructure and maintenance needs at a system level, rather than a fragmented approach for each asset only when problems arise.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Data Traffic and Need for Secured Connectivity is Promoting the Growth of the Data Center Physical Security Market

- 4.2.2 Rise in Cyber Threats is Causing the Data Center Physical Security Market to Grow

- 4.3 Market Restraints

- 4.3.1 Limited IT Budgets, Availability of Low-Cost Substitutes, and Piracy is Discouraging the Potential Growth of Data Center Physical Security Market

- 4.4 Value Chain / Supply Chain Analysis

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Assessment of COVID-19 Impact

5 MARKET SEGMENTATION

- 5.1 By Solution Type

- 5.1.1 Video Surveillance

- 5.1.2 Access Control Solutions

- 5.1.3 Others (Mantraps and Fences and Monitoring Solutions)

- 5.2 By Service Type

- 5.2.1 Consulting Services

- 5.2.2 Professional Services

- 5.2.3 Others (System Integration Services)

- 5.3 End-User

- 5.3.1 IT and Telecommunication

- 5.3.2 BFSI

- 5.3.3 Government

- 5.3.4 Healthcare

- 5.3.5 Other End User

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Axis Communications AB

- 6.1.2 ABB Ltd

- 6.1.3 Bosch Sicherheitssysteme GmbH

- 6.1.4 Honeywell International Inc.

- 6.1.5 Johnson Controls

- 6.1.6 Schneider Electric

- 6.1.7 ASSA ABLOY

- 6.1.8 Cisco Systems Inc.

- 6.1.9 Boon Edam

- 6.1.10 Dahua Technology