|

시장보고서

상품코드

1521846

바이오의약품 CMO 및 CRO : 시장 점유율 분석, 업계 동향, 성장 예측(2024-2029년)Biopharmaceutical CMO And CRO - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

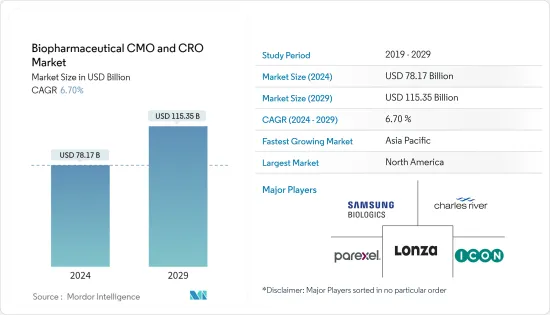

바이오의약품 CMO 및 CRO(Biopharmaceutical CMO And CRO) 시장 규모는 2024년에 781억 7,000만 달러로 추정되며, 2029년에는 1,153억 5,000만 달러에 이를 것으로 예측되며, 예측기간 중(2024-2029년) CAGR은 6.70%로 추이하며 성장할 것으로 예상됩니다.

시장을 견인하고 있는 것은 바이오의약품 CMO시설 확대를 위한 시장 진출기업에 의한 투자의 확대, 견고한 의약품 파이프라인의 성장, 제휴나 파트너십 등 시장 진출기업에 의한 전략적 활동의 활성화등이 요인입니다.

바이오 의약품 업계에서 아웃소싱 동향이 증가함에 따라 세계 CMO 및 CRO 시장은 큰 성장을 이루고 있습니다. 예를 들어, 2022년 11월, Baxter International Inc.는 독일의 할레(할레 베스트팔렌)에 있는 무균 충전 및 마감 제조 시설의 대폭적인 1억 달러의 확대를 발표했습니다. 할레의 시설은 유명한 제약회사 및 생명공학기업과 협력하여 주사용 의약품(비경구제)의 의약품을 제조·위탁 생산하는 Baxter 지사, BioPharma Solutions(BPS)가 운영하고 있습니다.

마찬가지로 2022년 6월 퀘벡 정부는 Jubilant Pharma Limited에 대해 몬트리올의 수탁 제조 시설의 확대를 촉진하기 위해 1,800만 달러의 대출을 실시했습니다. 게다가 2022년 10월, Evonik은 미국과 유럽의 수탁 제조 시설의 3,600만 유로(3,812만 달러) 상당한 확대 공사의 완료를 발표했습니다. Evonik의 각 제조 기지에서 고역가 원료, 발효, mPEG, 연속 처리와 같은 첨단 기술이 통합되거나 개선되었습니다. 따라서 이러한 위탁제조 서비스의 확대는 제약회사나 의료기기회사에 의한 채택을 증가시켜 시장 성장을 밀어올릴 것으로 예상됩니다.

게다가 시장 진출기업은 합병, 인수, 협업 등 몇 가지 전략도 채택하고 있으며, 예측 기간 중 바이오 의약품 CMO&CRO 시장 성장을 뒷받침할 것으로 예상됩니다. 예를 들어, 2023년 11월, CRO와 장수 생명 공학 회사인 Ichor Life Sciences는 Ichor Clinical Trial Services의 출시를 발표했습니다. Ichor Clinical의 설립을 통해 이 회사는 초기 전임상시험부터 후기 임상시험, FA 승인에 이르기까지 생명공학 및 제약 기업 고객에게 서비스를 제공할 수 있게 되었습니다.

또한 2023년 7월 인간화 마우스 모델을 전문으로 하는 CRO인 TransCure bioServices는 자가면역 질환 및 염증성 질환을 전문으로 하는 한국의 Precl na Inc.와 전략적 파트너십을 체결했습니다. 이 제휴는 TransCure bioServices에 있어서 아시아 태평양에 대한 입지 확대, 서비스 포트폴리오 강화, 연구 성과의 질 향상 등 중요한 이정표가 됩니다.

따라서 CRO 및 CMO 기업의 제조시설 확대를 위한 자금 조달 및 전략적 이니셔티브 증가는 예측 기간 동안 시장을 밀어올릴 것으로 예상됩니다. 그러나 전통적인 바이오 의약품 제조업체의 아웃소싱은 제한적이며 규제 문제가 있기 때문에 예측 기간 동안 시장 성장 억제요인이 될 것으로 예상됩니다.

바이오 의약품 CMO 및 CRO 시장 동향

예측 기간 동안 종양 영역이 큰 점유율을 차지할 전망

CRO(의약품 개발 업무 수탁기관)는 암 연구 및 의약품 개발에 있어서 중요한 역할을 하고 있습니다. CRO는 종종 암 치료의 임상시험의 다양한 단계의 관리에 관여하고 있습니다. 여기에는 시험 설계 및 계획, 환자 모집, 데이터 관리, 규제 기준 준수를 보장하기 위한 시험 진행 상황 모니터링 등이 포함됩니다. 또한 CRO는 제약 회사가 전임상시험을 설계할 수 있도록 지원하고, 데이터 분석 및 해석을 제공하며, 규제 당국을 지원합니다.

암 유병률 증가는 선진적이고 효과적인 치료에 대한 수요를 높일 것으로 예상되며, 신규 암 치료의 동정, 시험, 개발을 위한 기업이나 정부 등 이해관계자에 의한 새로운 투자로 이어지고 있습니다. 예를 들어 Canadian Cancer Statistics 2023 보고서에 따르면 캐나다에서는 2022년 23만 3,900건에 대해 2023년에는 약 23만 9,200건의 새로운 암 증례가 보고되었습니다. 이와 같이 암에 대한 부담 증가는 의약품 연구·제조 서비스에 대한 수요를 만들어낼 것으로 예상되며, 이것이 같은 부문의 성장에 기여할 가능성이 높습니다.

연구개발 활동 증가나 암의 약제 연구 방법을 효율적으로 완료하기 위한 CRO 제공업체와의 제휴가 부문 성장에 기여할 것으로 예상됩니다. 예를 들어 ITOCHU Corporation과 그 자회사인 A2 Healthcare Corporation은 2023년 6월 국립암 연구센터의 관련회사로서 일본 내 다기관 공동 임상연구를 추진하기 위해 CRO로서 NRG Oncology와 제휴 계약을 체결 했다고 발표했습니다. 본 계약에 따라 A2 의료는 일본 미승인 약의 임상시험 지원 사업을 계속합니다. 또한 2023년 5월에는 CRO의 George Clinical이 폐암을 포함한 바이오마커에서 선택된 환자 집단을 대상으로 종양 증식과 항암제 내성의 강력한 드라이버인 HER3를 표적으로 한 Hummingbird Bioscience의 정밀 치료 프로그램을 검토하는 두 개의 암 영역 1b 단계 시험 준비를 호주에서 시작했습니다.

따라서 항암제의 연구개발 활동 증가는 예측기간 중에 CRO 서비스에 대한 수요를 창출할 것으로 예상됩니다.

예측기간 중 북미가 큰 시장 점유율을 차지할 전망

북미는 만성질환의 이환율 증가, 제네릭 의약품 및 생물제제 수요 증가, 바이오시밀러 의약품 수요 증가, 바이오 의약품 업계에 의한 R&D 투자 증가로 예측 기간 동안 시장에서 가장 큰 점유율을 획득 예상됩니다. 또한 제조시설의 확대와 시장 진출기업의 전략적 활동 증가가 시장 성장에 기여할 것으로 예상됩니다.

또한 이 지역의 의약품 지출 증가도 시장 성장을 뒷받침하고 있습니다. 예를 들어, 연방연구개발(R&D) 기금(Federal Research and Development(R&D) Funding)에 따르면 2022년에는 연구개발에 대한 자금이 증가할 것으로 예상됩니다. FY2022에 따르면 연구개발을 위한 자금은 소수의 연방부처에 집중되어 있습니다. 2021년도에는 연방 정부의 연구 개발 자금 총액의 93.0%를 5개 기관이 획득하고 있으며, 그 중 보건 복지성은 27.6%를 획득하고 있습니다. 연구개발 자금의 가장 큰 가격 인상은 보건복지성으로 최대 77억 달러(17.8%)가 됩니다. 이러한 이니셔티브는 R&D 활동에 인센티브를 제공하고 이해관계자간의 협력을 촉진하며 과학적 발견의 임상적 응용으로의 전환을 촉진합니다. 바이오의약품 CMO를 전문으로 하는 수탁 제조업자는 이러한 협력적인 대처로부터 혜택을 받는 입장에 있으며, 최첨단 연구를 구체적인 의료 솔루션으로 전환하는 지원을 실시했습니다.

제조 수탁 시설의 개발·확대에 대한 투자 증가는 예측 기간 중 시장 성장에 기여할 것으로 예상됩니다. CMO는 FDA의 승인을 받아 생물 제제 제조에 연속 제조를 채택하는 경우가 늘고 있습니다. 예를 들어, 2022년 6월, 애질런트 테크놀로지스와 압제나는 연속 생산 능력을 확대했습니다. 또한, 백신의 제조와 개발을 간소화하기 위해 CDMO에 의한 제약회사와의 제휴 및 파트너십 계약은 시장 성장에 기여할 것으로 예상됩니다. 예를 들어, 2023년 5월, Modernna Inc.는 온타리오 주를 기반으로 하는 CMO인 Novocol Pharma와 캐나다에서 제조가 예상되는 mRNA 호흡기 백신의 무균 충전 마무리, 라벨링, 포장을 실시하는 장기 계약을 체결했다 라고 발표했습니다.

이와 같이 높은 R&D 투자와 주요 기업에 의한 제품 포트폴리오의 확대에 대한 대처가 신약의 개발을 뒷받침하고, CMO나 CRO 등 아웃소싱 서비스 수요를 높여 시장 성장을 높일 것으로 예상됩니다.

바이오 의약품 CMO 및 CRO 산업 개요

바이오 의약품 CMO 및 CRO 시장은 적당한 경쟁이 있으며 여러 선도 기업으로 구성되어 있습니다. 시장 점유율에서는 소수의 대기업이 시장을 독점하고 있습니다. 일부 유력 참가 기업은 세계 시장에서 지위를 굳히기 위해 타사의 인수를 정력적으로 실시했습니다. 주요 시장 진출기업으로는 Lonza Group AG, ICON PLC, Parexel International Corporation, Samsung Biologics, Charles River Laboratories International Inc. 등이 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사 전제 조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- CMO에 의한 생산 능력 확대를 위한 투자 증가

- 견조한 바이오 의약품 파이프라인

- 수탁 서비스에 의한 비용과 시간의 절약

- 시장 성장 억제요인

- 확립된 바이오 의약품 제조업체에 있어서 아웃소싱의 제한

- 규제상의 과제

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자/소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계 강도

제5장 시장 세분화(시장 규모-달러)

- 공급원별

- 포유류

- 비포유류

- 서비스 유형별

- 수탁 제조

- 프로세스 개발

- 충전·마무리 작업

- 분석·QC 시험

- 포장

- 수탁조사

- 종양학

- 염증·면역학

- 심장병학

- 신경과학

- 기타

- 수탁 제조

- 제품별

- 생물제제

- 단클론항체(MAbs)

- 재조합 단백질

- 백신

- 안티센스, RNAi, 분자요법

- 기타

- 바이오시밀러

- 생물제제

- 지역

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 영국

- 독일

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아 태평양

- 인도

- 일본

- 중국

- 호주

- 한국

- 기타 아시아 태평양

- 중동 및 아프리카

- GCC 국가

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 기업 프로파일

- Boehringer Ingelheim GmbH

- Lonza Group AG

- Inno Biologics Sdn Bhd

- Fujifilm Diosynth Biotechnologies USA Inc.

- Toyobo Co. Ltd

- Samsung Biologics

- Thermo Fisher Scientific Inc(Patheon & PPD)

- WuXi Biologics

- Charles River Laboratories International Inc.

- ICON PLC

- Parexel International Corporation

- Laboratory Corporation of America Holdings

제7장 시장 기회 및 향후 동향

LYJThe Biopharmaceutical CMO And CRO Market size is estimated at USD 78.17 billion in 2024, and is expected to reach USD 115.35 billion by 2029, growing at a CAGR of 6.70% during the forecast period (2024-2029).

The market is driven by factors such as growing investment by market players to expand the biopharmaceutical CMO facility, growing robust pharmaceutical pipeline, and increasing strategic activities by the market players such as collaboration and partnership.

Due to the rising trend of outsourcing in the biopharmaceutical industry, the global CMO/CRO market is experiencing significant growth. For instance, in November 2022, Baxter International Inc. unveiled a substantial USD 100 million expansion for its sterile fill and finish manufacturing facility in Halle (Halle Westfalen), Germany. The Halle facility is operated by BioPharma Solutions (BPS), a branch of Baxter that collaborates with renowned pharmaceutical and biotech companies to create and contract-manufacture drug products for injectable pharmaceuticals (parenteral).

Similarly, in June 2022, the Government of Quebec bestowed a loan of USD 18 million upon Jubilant Pharma Limited to facilitate the expansion of the contract manufacturing facility in Montreal. Moreover, in October 2022, Evonik unveiled the completion of an expansion worth EUR 36 million (USD 38.12 million) for its contract manufacturing facilities in the United States and Europe. At various Evonik production sites, cutting-edge technologies encompassing high-potency APIs, fermentation, mPEGs, and continuous processing were either integrated or improved. Thus, expanding these contract manufacturing services is likely to increase their adoption by pharmaceutical and medical device companies and is anticipated to boost market growth.

Moreover, market players are also adopting several strategies, such as mergers, acquisitions, and collaboration, which are expected to boost the biopharmaceutical CMO & CRO market growth over the forecast period. For instance, in November 2023, Ichor Life Sciences, a CRO and longevity biotechnology company, announced the launch of Ichor Clinical Trial Services. With the founding of Ichor Clinical, the company can now serve biotechnology and pharmaceutical clients from early preclinical studies through late-stage clinical trials and F-A approval.

Additionally, in July 2023, TransCure bioServices, a CRO specializing in humanized mouse models, formed a strategic partnership with Precl na Inc., based in South Korea, specializing in autoimmune and inflammatory diseases. This partnership is a significant milestone for TransCure as it expands its presence into the APAC region, strengthens its service portfolio, and enhances the quality of its research outcomes.

Hence, increasing funding for expanding manufacturing facilities and strategic initiatives taken by the CRO and CMO companies is expected to boost the market over the forecast period. However, limited outsourcing among well-established biopharmaceutical manufacturers and regulatory challenges are expected to restrain the market over the forecast period.

Biopharmaceutical CMO And CRO Market Trends

The Oncology Segment is Expected to Hold a Significant Share During the Forecast Period

CROs (contract research organizations) play a significant role in cancer research and drug development. CROs are often involved in managing various phases of clinical trials for cancer therapies. This includes designing and planning trials, patient recruitment, data management, and monitoring trial progress to ensure adherence to regulatory standards. In addition, CRO helps pharmaceutical companies design preclinical studies, providing data analytics and interpretation and regulatory support.

The increasing prevalence of cancer is anticipated to boost the demand for advanced and effective therapeutics, leading to new investments by companies and other stakeholders, like governments, for the identification, testing, and development of novel cancer therapeutics. For instance, as per the Canadian Cancer Statistics 2023 report, about 239.2 thousand new cancer cases were reported in 2023 in Canada, compared to 233.9 thousand in 2022. Thus, the growing burden of cancer is expected to create the demand for drug research and manufacturing services, which will likely contribute to segment growth.

The increasing research & development activities and collaboration with CRO providers to effectively complete the drug research process for cancer are expected to contribute to segment growth. For instance, in June 2023, ITOCHU Corporation and its subsidiary A2 Healthcare Corporation announced a partnership agreement with NRG Oncology as a CRO to promote multicentre joint clinical research within Japan as an affiliate of the National Cancer Institutes. Based on the agreement, A2 Healthcare will continue to engage in the clinical trial support business for drugs that have yet to be approved in Japan. Additionally, in May 2023, George Clinical, a CRO, initiated preparations in Australia for two oncology Phase 1b trials that will examine a Hummingbird Bioscience precision therapy program targeting HER3, a potent driver of tumor growth and resistance against cancer drugs, in biomarker-selected patient populations, including lung cancer.

Hence, increasing research and development activities for cancer drugs will create demand for CRO services over the forecast period.

North America is Expected to Hold a Significant Market Share During the Forecast Period

North America is expected to gain the largest share in the market during the forecast period owing to the increasing incidence of chronic diseases, increasing demand for generics and biologics, rise in demand for biosimilars, and growing investments in R&D by the biopharmaceutical industry. In addition, increasing expansion of manufacturing facilities and strategic activities by the market players are expected to contribute to the market growth.

The increasing pharmaceutical expenditure in the region is also bolstering the market's growth. For instance, according to Federal Research and Development (R&D) Funding: FY2022, funding for R&D is concentrated in a few federal departments and agencies. In FY 2021, five agencies received 93.0% of total federal R&D funding, with the Department of Health and Human Services receiving 27.6%. The most significant price increases in R&D funding would be made to Health and Human Services, up to USD 7.7 billion (17.8%). These initiatives incentivize research and development activities, promote collaboration among stakeholders, and facilitate the translation of scientific discoveries into clinical applications. Contract manufacturers specializing in biopharmaceutical CMO are well-positioned to benefit from these collaborative efforts, supporting the translation of cutting-edge research into tangible healthcare solutions.

Increasing investment in developing and expanding the contract manufacturing facilities is expected to contribute to the market growth during the forecast period. CMOs have increasingly adopted continuous manufacturing for biologics production following FDA approval. For instance, in June 2022, Agilent Technologies and Abzena expanded their continuous manufacturing capabilities. Furthermore, the collaboration and partnership agreement by CDMO with the pharmaceutical company to streamline vaccine manufacturing and development are expected to contribute to market growth. For instance, in May 2023, Moderna Inc. announced a long-term agreement with Ontario-based Novocol Pharma, a CMO to perform aseptic fill-finish, labeling, and packaging of mRNA respiratory vaccines expected to be produced in Canada.

Thus, the high R&D investment and initiatives by key players in the product portfolio expansion are expected to boost the development of new drugs, increasing the demand for outsourcing services such as CMO and CRO, thereby raising the market growth.

Biopharmaceutical CMO And CRO Industry Overview

The biopharmaceutical CMO and CRO market is moderately competitive and consists of several significant players. In terms of market share, a few major players dominate the market. Some prominent players are vigorously making acquisitions of other companies to consolidate their global market positions. Some of the major market players are Lonza Group AG, ICON PLC, Parexel International Corporation, Samsung Biologics, and Charles River Laboratories International Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definitions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Investment by CMOs For Capacity Expansion

- 4.2.2 Robust Biopharmaceuticals Pipeline

- 4.2.3 Cost And Time Saving Benefits Offered By Contract Services

- 4.3 Market Restraints

- 4.3.1 Limited Outsourcing Amongst Well-Stablished Biopharmaceutical Manufacturer

- 4.3.2 Regulatory Challenges

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1 By Source

- 5.1.1 Mammalian

- 5.1.2 Non-mammalian

- 5.2 By Services Type

- 5.2.1 Contract Manufacturing

- 5.2.1.1 Process Development

- 5.2.1.2 Fill & Finish Operations

- 5.2.1.3 Analytical & QC Studies

- 5.2.1.4 Packaging

- 5.2.2 Contract Research

- 5.2.2.1 Oncology

- 5.2.2.2 Inflammation & Immunology

- 5.2.2.3 Cardiology

- 5.2.2.4 Neuroscience

- 5.2.2.5 Others

- 5.2.1 Contract Manufacturing

- 5.3 By Product

- 5.3.1 Biologics

- 5.3.1.1 Monoclonal antibodies (MAbs)

- 5.3.1.2 Recombinant Proteins

- 5.3.1.3 Vaccines

- 5.3.1.4 Antisense, RNAi, & Molecular Therapy

- 5.3.1.5 Others

- 5.3.2 Biosimilars

- 5.3.1 Biologics

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Spain

- 5.4.2.5 Italy

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 India

- 5.4.3.2 Japan

- 5.4.3.3 China

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of the Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Boehringer Ingelheim GmbH

- 6.1.2 Lonza Group AG

- 6.1.3 Inno Biologics Sdn Bhd

- 6.1.4 Fujifilm Diosynth Biotechnologies U.S.A. Inc.

- 6.1.5 Toyobo Co. Ltd

- 6.1.6 Samsung Biologics

- 6.1.7 Thermo Fisher Scientific Inc (Patheon & PPD)

- 6.1.8 WuXi Biologics

- 6.1.9 Charles River Laboratories International Inc.

- 6.1.10 ICON PLC

- 6.1.11 Parexel International Corporation

- 6.1.12 Laboratory Corporation of America Holdings