|

시장보고서

상품코드

1521873

방사성의약품 테라노스틱스 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2024-2029년)Radiopharmaceutical Theranostics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

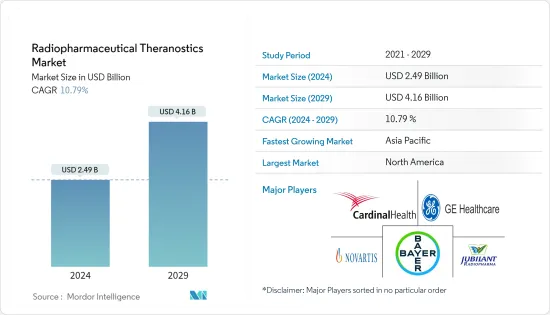

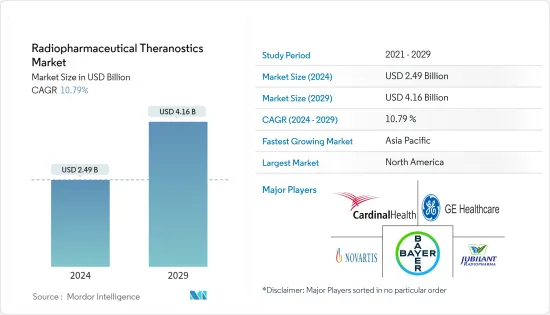

방사성의약품 테라노스틱스 시장 규모는 2024년 24억 9,000만 달러로 추정되며, 2029년에는 41억 6,000만 달러에 달할 것으로 예상되며, 예측 기간(2024-2029) 동안 10.79%의 CAGR로 성장할 것으로 예상됩니다.

COVID-19 팬데믹은 초기에 방사성의약품 세라믹 시장에 큰 영향을 미쳤습니다. 팬데믹은 진행 중이거나 계획 중인 방사성의약품 임상시험에 지연과 혼란을 초래했습니다. 운송 제한과 인력 문제 등 공급망 혼란은 생산 및 공급 능력에 영향을 미쳤습니다. 연구소와 연구 시설은 폐쇄 기간 동안 폐쇄 및 용량 감소에 직면하여 진행중인 의약품 관련 연구 개발 활동에 영향을 미쳤습니다. 따라서 COVID-19는 다른 많은 치료제와 마찬가지로 테라노스틱스의 임상 개발에도 악영향을 미쳤습니다. 그러나 COVID-19 이후 방사성의약품을 이용한 필수적인 영상 진단을 기다리는 많은 수술 대기 환자가 발생하여 수술 건수에 영향을 미쳤습니다. 또한, 질병의 조기 발견과 개인 맞춤형 의료에 대한 역할로 인해 전염병은 예방 건강 관리의 중요성을 강조하여 적극적인 건강 관리로 이어졌습니다. 영상 진단 및 방사성의약품 개발의 기술 혁신은 진단의 정확성을 높이고 이후 보다 효과적인 치료에 기여했습니다.

암 표적 치료의 발전은 진단과 치료의 정확성을 높여 방사성의약품 테라노스틱스 시장을 크게 견인하고 있습니다. 종양학에서 방사성의약품의 적용은 SSTR2 양성 또는 NET 양성 신경내분비 종양, NIS 양성 분화 갑상선 종양, PSMA 양성 전립선암과 같은 암종 특이적 바이오마커를 이용한 잔존 종양 관리에서 그 중요성이 커지고 있습니다. 예를 들어, 177Lu-PSMA-617과 같은 방사성 표지 PSMA 표적 약물은 이미징과 치료 모두에 적용할 수 있습니다. 68Ga-HER2 표적 PET 약물과 같은 방사성 표지 HER2 표적 추적자는 정확한 진단을 위한 비침습적 이미징을 가능하게 하고, 68Ga-HER2 표적 PET 약물과 같은 방사성 표지 HER2 표적 추적자는 정확한 진단을 위한 비침습적 이미징을 가능하게 합니다. 이러한 사례는 표적 암 치료가 방사성의약품과 결합하여 정확한 진단과 개별화된 표적 치료 전략을 가능하게 하는 테라노스틱스의 적용이 가능하다는 것을 보여줍니다.

또한 68Ga/177Lu와 같은 일부 방사성의약품은 임상에서 일상적으로 사용되고 있으며, 수십 종류의 방사성의약품이 임상 개발(전) 단계에 있습니다. 표적 암 치료의 진화하는 상황은 방사성의약품 테라노스틱스 산업의 기술 혁신에 계속 박차를 가하고 있습니다. 예를 들어, 2022년 9월 텍사스대학교 MD Anderson Cancer Center와 Radiopharm Theranostics는 암을 위한 새로운 방사성의약품 치료 제품을 혁신하기 위해 설립된 조인트벤처인 Radiopharm Ventures LLC를 설립했습니다.

또한, 방사성의약품 테라노스틱스에 대한 수요 증가로 이 분야의 기술 혁신이 촉진되고 연구개발에 투자하는 기업이 늘어나면서 파이프라인 선택의 폭이 넓어졌습니다. 예를 들어, 2022년 9월 차세대 핵융합 기술 기업인 샤인 테크놀러지스(Shine Technologies)는 동위원소 비담체 첨가 루테튬 177(Lu-177)을 방사성의약품 테라노스틱스에 공급하는 임상 계약을 체결했으며, 2021년 6월에는 바이엘이 노리아 테라퓨틱스(Noria Therapeutics Inc.(Noria Therapeutics Inc.)와 PSMA Therapeutics Inc.)를 인수하여 액티늄225와 전립선 특이적 막 항원(PSMA)을 표적으로 하는 저분자 기반 분화형 알파 방사성 핵종 치료제에 대한 독점권을 획득했습니다. 이번 인수로 바이엘은 기존 표적 알파 치료(TAT)의 종양학 포트폴리오를 확장할 수 있게 됐습니다.

따라서 방사성의약품 테라노스틱스 시장은 암 유병률 증가, 개인 맞춤형 의료에 대한 수요 증가, 다양한 종양학적 적응증에 대한 세라믹스 적용 확대, 진단 및 치료의 정확성을 높이는 표적 치료의 발전에 대한 수요 증가 등 다양한 요인의 수렴에 의해 주도되고 있습니다. 방사성의약품 테라노스틱스 시장이 크게 성장하고 있는 반면, 규제의 복잡성, 공급망의 혼란, 세라믹스 접근법 개발 및 도입의 복잡성 등이 시장 성장의 걸림돌로 작용하고 있습니다. 방사성의약품 테라노스틱스가 암 진단과 치료에 변화를 가져올 수 있는 잠재력을 최대한 발휘하기 위해서는 이러한 장애물을 극복하는 것이 중요합니다.

방사성의약품 테라노스틱스 시장 동향

예측 기간 동안 동반진단용 방사성의약품 부문이 방사성의약품 테라노스틱스 시장을 장악할 것으로 전망

동반진단용 방사성의약품은 방사성의약품 테라노스틱스 시장에서 다양한 질환, 특히 암의 정확한 영상 진단과 정확한 진단을 위한 필수적인 도구를 제공하는 데 있어 매우 중요한 역할을 하고 있습니다. 진단용 방사성의약품은 종양학, 순환기학, 신경학 등에서 광범위하게 사용되고 있습니다. 질병의 조기 발견, 병기 결정 및 모니터링에 도움을 주며, 치료 계획에 중요한 정보를 제공합니다.

지속적인 연구 개발 노력으로 특이성과 민감도가 향상된 새로운 방사성의약품 추적자가 지속적으로 도입되고 있습니다. 예를 들어, 전립선암 이미징을 위한 전립선 특이적 막 항원(PSMA) 표적 추적자의 개발은 진단용 방사성의약품 시장의 역동적인 성격을 보여줍니다. 또한, 2023년 5월 Radiopharm Theranostics는 미국 식품의약국(FDA)이 췌관 선암(PDAC) 환자의 영상 진단을 위한 Ga68-Trivehexin(RAD 301) 방사성의약품 기술을 희귀질환 치료제로 지정했다고 발표했습니다.

진단용 방사성의약품은 암의 병기 분류, 치료 효과 모니터링, 재발 감지 등 종양학에서 광범위하게 사용되고 있습니다. 대사 영상용 18F-FDG, 신경내분비 종양용 68Ga-DOTATATE와 같은 추적자는 종양학 영역의 다양한 용도의 일례로, 이 분야의 다재다능함을 보여줍니다. 따라서 진단용 방사성의약품은 조기에 정확한 진단, 치료적 의사결정의 기초, 다양한 임상적 응용을 통해 방사성의약품 테라노스틱스 시장을 선도하고 있습니다.

북미, 방사성의약품 테라노스틱스 시장 독주 전망

북미의 방사성의약품 테라노스틱스 시장에서의 리더십은 첨단 의료 인프라, 뛰어난 연구, 높은 질병 유병률, 규제 당국의 지원, 전략적 제휴, 의료 분야의 첨단 기술 도입에 대한 헌신 등이 결합되어 이루어지고 있습니다. 이러한 요소들이 복합적으로 작용하여 이 지역은 정밀 의료를 위한 세라믹 솔루션의 미래를 주도하는 선두주자로 자리매김하고 있습니다.

북미 방사성의약품 업계 기업들은 연구기관 및 헬스케어 기관과 전략적 제휴를 맺어 세라믹스 제품의 개발, 생산 및 상용화를 촉진하고 시장 리더십을 확보하는 데 기여하고 있습니다. 예를 들어, 2023년 5월 NUCLIDIUM과 PharmaLogic Holdings는 NUCLIDIUM의 방사성의약품 파이프라인 개발을 가속화하기 위해 미국 내 61Cu의 생산 및 임상 공급을 위한 전략적 제휴를 발표했습니다. NUCLIDIUM의 세라노시스 접근법은 구리 방사성 금속과 특이성이 높은 암 표적 분자를 결합하여 다양한 고형암 환자에게 혁신적인 진단 및 치료법을 제공하는 것을 목표로 하고 있습니다.에서 61Cu를 지속적으로 공급받아 계획 중인 임상시험과 향후 상용화 제품 모두에 사용할 수 있게 됐습니다.

미국 FDA는 방사성의약품을 포함한 의료 제품의 규제 및 승인에 있어 매우 중요한 역할을 하고 있으며, 2023년 5월 FDA는 Posluma를 전이가 의심되는 전립선암 환자의 PSMA 양성 병변을 식별하기 위해 PET 촬영에 사용할 수 있는 약물로 승인했습니다. 2023년 9월, Bracco Imaging의 자회사인 Blue Earth Diagnostics는 미국 메디케어 및 메디케이드 서비스 센터(CMS)로부터 전립선 특이적 막 항원(PSMA) 양성 전립선암 전이 검출을 위한 Posluma에 대한 경과적 지불 지위를 획득했습니다. 지불 자격을 획득했습니다.

결론적으로, 북미의 기업과 연구기관은 첨단 기술 개발의 최전선에 있습니다. 주요 제품 출시, 시장 기업의 집중, 미국 내 제조업체의 존재 등이 미국 방사성의약품 테라노스틱스 시장의 성장을 촉진하는 요인으로 작용하고 있습니다. 따라서 앞서 언급한 요인들로 인해 북미 시장은 확대될 것으로 예상됩니다.

기타 혜택:

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

목차

제1장 소개

- 조사 가정과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- 암표적 치료의 진보

- 맞춤형 의료에 대한 주목 상승

- 영상 진단에 대한 응용 확대

- 시장 성장 억제요인

- 공급망의 복잡성과 생산능력의 한계

- 규제상 과제와 승인 프로세스

- Porter's Five Forces 분석

- 신규 참여업체의 위협

- 구매자·소비자의 협상력

- 공급 기업의 교섭력

- 대체품의 위협

- 경쟁 기업 간의 경쟁 강도

제5장 시장 세분화(시장 규모)

- 유형별

- 동반진단용 방사성의약품

- 표적 치료용 방사성의약품

- 방사성 동위원소별

- 테크네튬-99

- 갈륨-68

- 요오드 131

- 루테튬(Lu)-177

- 구리(Cu)-67 & 64

- 기타 방사성 동위원소

- 공급원별

- 원자로

- 사이클로트론

- 용도별

- 종양학

- 심장병학

- 신경학

- 기타 용도

- 최종사용자별

- 병원

- 영상 진단 센터

- 연구기관

- 기타 최종사용자

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카공화국

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 상황

- 기업 개요

- Bayer AG

- Cardinal Health

- GE HealthCare

- Jubilant Radiopharma

- Novartis AG

- Curium

- Telix Pharmaceuticals Limited

- Lantheus

- ARICEUM THERAPEUTICS

- NuView Life Sciences

- Clarity Pharmaceuticals

제7장 시장 기회와 향후 동향

ksm 24.08.01The Radiopharmaceutical Theranostics Market size is estimated at USD 2.49 billion in 2024, and is expected to reach USD 4.16 billion by 2029, growing at a CAGR of 10.79% during the forecast period (2024-2029).

The COVID-19 pandemic initially had a substantial impact on the radiopharmaceutical theranostics market. The pandemic caused delays and disruptions in ongoing and planned clinical trials of radiopharmaceuticals. Disruptions in the supply chain, including transportation restrictions and workforce challenges, affected production and availability. Laboratories and research facilities faced closure or reduced capacity during lockdowns, impacting ongoing research and development activities related to pharmaceuticals. Therefore, the pandemic negatively affected the clinical development of theranostics, as with many other therapies. However, post-COVID-19, there was a backlog of many elective surgery patients awaiting essential diagnostic imaging using radiopharmaceuticals, impacting the volume of procedures. Furthermore, with its role in early disease detection and personalized medicine, the pandemic emphasized the importance of preventive healthcare, leading to proactive health management. Innovations in imaging modalities and radiopharmaceutical development enhanced diagnostic accuracy and later contributed to more targeted and effective treatments.

Advancements in targeted cancer therapies significantly drive the radiopharmaceuticals theranostics market by enhancing precision in diagnosis and treatment. Theranostics applications in oncology gained importance in the management of remnant tumors using cancer-type specific biomarkers, such as SSTR2-positive or NET-positive neuroendocrine tumors, NIS-positive differentiated thyroid tumors, and PSMA-positive prostate cancer. For instance, radiolabeled PSMA-targeted agents, such as 177Lu-PSMA-617, enable both imaging and therapeutic applications. They help visualize prostate cancer lesions and deliver targeted radiation for therapeutic purposes. Radiolabeled HER2-targeted tracers, like 68Ga-HER2-targeted PET agents, allow non-invasive imaging for accurate diagnosis. These examples demonstrate how targeted cancer therapies, when combined with radiopharmaceuticals, enable theranostics applications, allowing for accurate diagnosis and personalized targeted treatment strategies.

Furthermore, several radiopharmaceuticals are routinely used in clinical practice, such as 68Ga/177Lu, and dozens are under (pre)clinical development. The evolving landscape of targeted cancer therapies continues to fuel innovation in the radiopharmaceuticals theranostics industry. For instance, in September 2022, the University of Texas MD Anderson Cancer Center and Radiopharm Theranostics launched Radiopharm Ventures LLC, a joint venture developed to innovate novel radiopharmaceutical therapeutic products for cancer.

In addition, the increasing demand for radiopharmaceutical theranostics drove innovation in the field, leading to more companies investing in research and development, resulting in a wider range of options under pipelines. For instance, in September 2022, SHINE Technologies, a next-generation fusion technology company, entered a clinical agreement to supply Radiopharm Theranostics with isotope non-carrier-added lutetium-177 (Lu-177). In June 2021, Bayer acquired Noria Therapeutics Inc. (Noria) and PSMA Therapeutics Inc. to obtain exclusive rights to a differentiated alpha radionuclide therapy based on actinium-225 and a small molecule targeting prostate-specific membrane antigen (PSMA). The acquisition broadens Bayer's existing oncology portfolio of targeted alpha therapies (TAT).

Therefore, the radiopharmaceutical theranostics market is propelled by a convergence of factors, including the rising prevalence of cancer leading to demand for advancements in targeted therapies providing precision in diagnosis and treatment, the growing demand for personalized medicine, and the expanding applications of theranostics across various oncological indications. While the radiopharmaceuticals theranostics market is poised for significant growth, challenges such as regulatory complexities, supply chain disruptions, and the intricate nature of developing and implementing theranostics approaches pose restraints. Navigating these hurdles will be crucial for realizing the full potential of radiopharmaceuticals theranostics in transforming cancer diagnosis and treatment.

Radiopharmaceutical Theranostics Market Trends

The Companion Diagnostic Radiopharmaceuticals Segment is Expected to Dominate the Radiopharmaceutical Theranostics Market During the Forecast Period

Companion diagnostic radiopharmaceuticals play a pivotal role in providing essential tools for precise imaging and accurate diagnosis of various medical conditions, particularly cancer, in the radiopharmaceutical theranostics market. Diagnostic radiopharmaceuticals find extensive use in oncology, cardiology, neurology, and beyond. They aid in early detection, staging, and monitoring of diseases, providing critical information for treatment planning.

Ongoing research and development efforts continually introduce new radiopharmaceutical tracers with enhanced specificity and sensitivity. For instance, the development of prostate-specific membrane antigen (PSMA) targeted tracers for prostate cancer imaging demonstrates the dynamic nature of the diagnostic radiopharmaceutical market. Furthermore, in May 2023, Radiopharm Theranostics announced that the US Food and Drug Administration (FDA) granted orphan drug designation to Ga68-Trivehexin (RAD 301) radiopharmaceutical technology for imaging of patients with pancreatic ductal adenocarcinoma (PDAC).

Diagnostic radiopharmaceuticals are extensively used in oncology for staging, monitoring treatment responses, and detecting cancer recurrence. Tracers such as 18F-FDG for metabolic imaging and 68Ga-DOTATATE for neuroendocrine tumors exemplify the diverse applications within the oncology domain, showcasing the versatility of this segment. Therefore, early and accurate diagnosis, foundation for therapeutic decision-making, and diverse clinical applications help diagnostic radiopharmaceuticals to lead in the radiopharmaceutical theranostics market.

North America is Expected to Dominate the Radiopharmaceutical Theranostics Market

North America's leadership in the radiopharmaceutical theranostics market is driven by a combination of advanced healthcare infrastructure, research excellence, high disease prevalence, regulatory support, strategic collaborations, and a commitment to adopting cutting-edge technologies in the healthcare sector. These factors collectively position the region as a frontrunner in shaping the future of theranostics solutions for precision medicine.

The companies in the radiopharmaceutical industry of North America often engage in strategic collaborations with research institutions and healthcare organizations to facilitate the development, production, and commercialization of theranostics products, contributing to market leadership. For instance, in May 2023, NUCLIDIUM and PharmaLogic Holdings announced a strategic collaboration aimed at the production and clinical supply of 61Cu in the United States to accelerate the development of NUCLIDIUM's theranostic pipeline. By combining copper radiometals with highly specific cancer-targeting molecules, NUCLIDIUM's theranostic approach aims to offer innovative diagnostic and therapeutic treatments for patients suffering from a range of solid tumors. The partnership with PharmaLogic will provide NUCLIDIUM with a sustainable supply of 61Cu in the United States for both its planned clinical trials and future commercialized products.

The US FDA plays a pivotal role in regulating and approving medical products, including radiopharmaceuticals. In May 2023, the FDA approved Posluma as an agent that can be used with PET imaging to identify PSMA-positive lesions in prostate cancer patients with suspected metastasis. In September 2023, Bracco Imaging's subsidiary Blue Earth Diagnostics received transitional pass-through payment status to Posluma for detecting prostate-specific membrane antigen (PSMA)-positive prostate cancer metastases from the US Centers for Medicare & Medicaid Services (CMS).

In conclusion, North American companies and research institutions have been at the forefront of developing advanced technology. Key product launches, a high concentration of market players, and manufacturers' presence in the United States are some of the factors driving the growth of the radiopharmaceutical theranostics market in the country. Therefore, owing to the aforementioned factors, the market is anticipated to expand in North America.

Radiopharmaceutical Theranostics Industry Overview

The radiopharmaceutical theranostics market is consolidated due to the presence of 4-5 major companies dominating it. Ongoing advancement efforts by major players such as Bayer AG, Cardinal Health, GE HealthCare, Jubilant Radiopharma, and Novartis AG for development, including the discovery of new tracers, ligands, and targeting agents, contribute to the market's consolidation. These companies continually explore novel approaches, resulting in a diverse array of radiopharmaceutical products.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Advancements in Targeted Cancer Therapies

- 4.2.2 Growing Emphasis on Personalized Medicine

- 4.2.3 Expanding Applications in Diagnostic Imaging

- 4.3 Market Restraints

- 4.3.1 Supply Chain Complexities and Limited Production Capacity

- 4.3.2 Regulatory Challenges and Approval Processes

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1 By Type

- 5.1.1 Companion Diagnostic Radiopharmaceuticals

- 5.1.2 Targeted Therapeutic Radiopharmaceuticals

- 5.2 By Radioisotopes

- 5.2.1 Technetium-99

- 5.2.2 Gallium-68

- 5.2.3 Iodine-131

- 5.2.4 Lutetium (Lu)- 177

- 5.2.5 Copper (Cu)- 67 & 64

- 5.2.6 Other Radioisotopes

- 5.3 By Source

- 5.3.1 Nuclear Reactors

- 5.3.2 Cyclotrons

- 5.4 By Application

- 5.4.1 Oncology

- 5.4.2 Cardiology

- 5.4.3 Neurology

- 5.4.4 Other Applications

- 5.5 By End User

- 5.5.1 Hospitals

- 5.5.2 Diagnostic Imaging Centers

- 5.5.3 Research Institutes

- 5.5.4 Other End Users

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Bayer AG

- 6.1.2 Cardinal Health

- 6.1.3 GE HealthCare

- 6.1.4 Jubilant Radiopharma

- 6.1.5 Novartis AG

- 6.1.6 Curium

- 6.1.7 Telix Pharmaceuticals Limited

- 6.1.8 Lantheus

- 6.1.9 ARICEUM THERAPEUTICS

- 6.1.10 NuView Life Sciences

- 6.1.11 Clarity Pharmaceuticals