|

시장보고서

상품코드

1522844

자동차용 차선 경보 시스템 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2024-2029년)Automotive Lane Warning Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

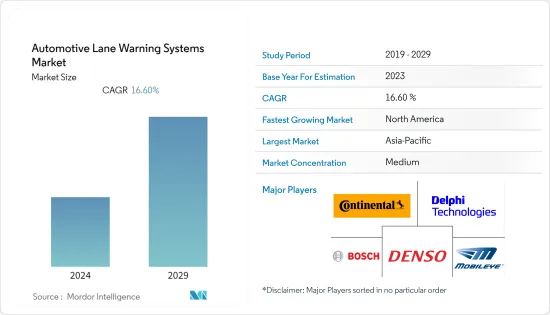

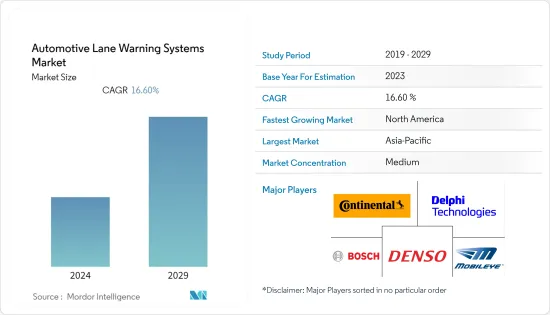

자동차용 차선 경보 시스템 시장 규모는 2024년 59억 4,000만 달러로 추정되며, 2029년에는 147억 9,000만 달러에 달할 것으로 예상되며, 예측 기간(2024-2029년) 동안 16.60%의 CAGR을 기록할 것으로 예상됩니다.

자동차용 차선 경보 시스템 시장은 교통 안전에 대한 인식이 높아지고 자동차의 첨단 안전 기능에 대한 세계 각국 정부의 지침이 증가함에 따라 괄목할 만한 성장세를 보이고 있습니다. 이 시장은 ADAS(첨단 운전자 보조 시스템) 시장의 한 분야로, 자동차 산업의 지능화, 자율주행차로의 전환을 반영하고 있습니다.

승용차 생산량이 증가하고 자동차 제조업체들이 첨단 안전 기능을 표준으로 장착함에 따라 차선 경고 시스템에 대한 수요가 증가하고 있습니다. 교통 안전 문제에 대한 인식이 높아지고 이러한 기술이 탑재된 자동차의 가치를 높이 평가하면서 소비자의 선호도는 첨단 안전 기술이 탑재된 자동차에 점점 더 기울어지고 있습니다.

기술의 발전은 이 시장에서 중요한 역할을 했습니다. 카메라, 센서, 인공지능 기술의 혁신으로 차선 경고 시스템의 정확성과 신뢰성이 향상되고 있습니다. 이러한 시스템을 적응형 크루즈 컨트롤, 사각지대감지 등 다른 안전 기능과 통합하여 보다 종합적인 안전 솔루션을 만들어 시장 성장을 더욱 촉진하고 있습니다.

지역별로 보면 유럽과 북미 시장이 첨단 안전 시스템 장착을 의무화하는 엄격한 정부 규제가 주요 요인으로 작용하면서 유럽과 북미 시장이 채택 측면에서 선두를 달리고 있습니다. 그러나 중국, 일본과 같은 국가들이 자동차 기술 및 인프라 개발에 많은 투자를 하고 있기 때문에 아시아태평양이 급성장하는 시장으로 부상하고 있습니다.

차선 경고 시스템 시장의 미래는 유망하며, 자율주행차 및 반자율주행차 확대에 이러한 시스템이 통합되면서 잠재적인 성장 기회가 있을 것으로 예상됩니다.

자동차용 차선 경보 시스템 시장 동향

승용차 부문이 시장 성장을 주도

승용차 부문이 자동차용 차선 경보 시스템 시장을 주도하고 있으며, 전 세계 승용차 생산 및 판매량 증가가 큰 역할을 하고 있습니다. 특히 신흥국에서 승용차 가격이 저렴해지고 접근성이 높아지면서 차선 경고 시스템과 같은 첨단 안전 기능에 대한 수요도 증가하고 있습니다. 처음에는 사치품이나 고급 옵션으로 여겨졌던 이러한 시스템은 소비자의 안전에 대한 요구와 규제 당국의 압력으로 인해 주류로 진입하고 있습니다.

규제의 영향은 정말 컸습니다. 유럽과 북미를 포함한 많은 지역에서는 신차에 첨단 안전 시스템을 장착하도록 의무화하거나 강력하게 장려하는 엄격한 안전 규제를 시행하고 있습니다. 이러한 규제 강화는 승용차 부문에서 차선 경고 시스템 시장을 효과적으로 확대했습니다.

고급 센서, 카메라 및 소프트웨어의 통합은 차선 경고 시스템의 효율성을 향상시켰을 뿐만 아니라 시간이 지남에 따라 비용 효율성도 향상시켰습니다. 기술의 접근성이 향상되고 제조 비용이 낮아지면서 자동차 제조업체들은 중급 차량을 포함한 다양한 모델에 이러한 시스템을 장착하고 있습니다.

교통 안전 문제와 ADAS(첨단 운전자 보조 시스템)의 장점에 대한 일반 소비자의 인식이 높아지면서 구매 의사결정에 영향을 미치고 있습니다. 소비자들은 차선 이탈 경고와 같은 안전 기능이 탑재된 자동차를 선택하고 있으며, 이는 안전 운전에 필수적인 것으로 여겨지고 있습니다.

또한, 커넥티드카와 자율주행차의 등장은 승용차 부문에서 차선 경고 시스템 시장에 더 많은 성장 기회를 가져왔습니다. 자동차 제조업체들이 반자율주행차 및 자율주행차 개발에 투자함에 따라 첨단 차선 경고 시스템 및 기타 ADAS 기술의 통합이 매우 중요해졌습니다.

이러한 추세는 ADAS의 혁신으로 승용차의 안전성과 매력을 더욱 높여주는 ADAS의 혁신으로 지속될 것으로 예상됩니다.

북미는 자동차용 차선 경보 시스템의 주요 시장

북미는 자동차용 차선 경보 시스템의 주요 시장으로 부상하고 있으며, 이러한 추세는 여러 가지 요인이 복합적으로 작용하고 있습니다. 이 지역, 특히 미국과 캐나다는 세계에서 1인당 자동차 보유율이 가장 높은 지역 중 하나이며, 차선 경고 시스템을 포함한 첨단 자동차 기술의 거대한 시장을 형성하고 있습니다.

이러한 국가들의 규제 노력은 매우 중요하며, 적극적인 조치를 통해 자동차에 안전 기술 적용을 장려하거나 의무화하고 있습니다. 이러한 규제적 지원은 이 지역의 강력한 기술 혁신에 의해 보완되고 있으며, 이 지역에 기반을 둔 많은 주요 자동차 및 기술 기업들이 최첨단 운전 지원 시스템을 지속적으로 개발하고 있습니다.

또한, 북미에서는 자동차 안전에 대한 소비자의 인식과 우선순위가 높습니다. 이러한 인식은 안전 기술에 대한 투자 의지와 함께 차선 경고 시스템 시장을 더욱 촉진하고 있습니다. 또한, 정부 및 단체의 다양한 교통 안전에 대한 노력은 자동차의 첨단 안전 기능의 중요성을 강조하고 있습니다.

북미 국가들의 경제가 호조를 보이면서 개인 소비자와 차량 운영사 모두 이러한 첨단 기술이 탑재된 새롭고 안전한 차량에 투자할 수 있게 되었고, 경제적인 요인도 한몫을 하고 있습니다. 이러한 모든 측면이 시너지 효과를 발휘하여 북미는 자동차용 차선 경보 시스템 분야에서 중요한 시장으로 부상했습니다.

캐나다 정부는 운전 보조 기술에 대한 인식을 확산하는 한편, 모든 차량에 대한 안전 테스트와 자율주행차 및 커넥티드카의 배치를 발표했습니다.

- 지난 5월, GM은 INRIX Inc.와의 건설적인 파트너십을 발표하고, Safety View by GM Future Roads &Inrix 이니셔티브에 따라 분석 지원 클라우드 기반 애플리케이션을 통해 미국 교통부에 안전 솔루션 데이터를 직접 제공하기로 했습니다.

- 2022년 5월, 도요타 자동차는 텍사스 오스틴의 스타트업 Invisible AI에서 조달한 컴퓨터 기반 비전 기술을 북미 조립 공장에서 사용할 것이라고 발표했습니다. 이 기술은 신체 움직임 데이터를 처리하여 품질, 안전 및 효율성을 향상시킬 수 있습니다.

상기 요인으로 인해 차량 안전 솔루션에 대한 수요가 증가할 것으로 예상됩니다. 이는 2024년부터 2029년까지 조사 대상 시장의 성장을 촉진할 것으로 예상됩니다.

자동차용 차선 경보 시스템 산업 개요

자동차용 차선 경보 시스템 시장은 다음과 같은 업체들이 주도하고 있습니다. Continental AG, Delphi Technologies, Mobileye, Robert Bosch GmbH, Hitachi Ltd, ZF Friedrichshafen AG, DENSO Corporation, and Magna International Inc. .

기타 혜택

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 소개

- 조사 가정

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 성장 촉진요인

- 안전 인식 확산이 시장 성장을 촉진

- 시장 성장 억제요인

- 사이버 보안에 대한 우려가 시장 성장을 억제할 것으로 예측

- Porter's Five Forces 분석

- 신규 참여업체의 위협

- 구매자/소비자의 협상력

- 공급 기업의 교섭력

- 대체품의 위협

- 경쟁 기업 간의 경쟁 강도

제5장 시장 세분화

- 기능 유형

- 차선 이탈 경고 시스템

- 차선 유지 시스템

- 센서 유형

- 비디오 센서

- 레이저 센서

- 적외선 센서

- 판매 채널

- OEM

- 애프터마켓

- 차종

- 승용차

- 소형 상용차

- 대형 상용차

- 지역

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 러시아

- 스페인

- 기타 유럽

- 아시아태평양

- 인도

- 중국

- 일본

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 아랍에미리트

- 사우디아라비아

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 상황

- 벤더 시장 점유율

- 기업 개요

- Continental AG

- Delphi Technologies

- Mobileye

- DENSO Corporation

- Robert Bosch GmbH

- The Bendix Corporation

- Hitachi Ltd

- Iteris Inc.

- Nissan Motor Co. Ltd

- Volkswagen AG

- ZF TRW

제7장 시장 기회와 향후 동향

ksm 24.08.02The Automotive Lane Warning Systems Market size is estimated at USD 5.94 billion in 2024, and is expected to reach USD 14.79 billion by 2029, growing at a CAGR of 16.60% during the forecast period (2024-2029).

The market for automotive lane warning systems was experiencing significant growth driven by heightened awareness of road safety and increasing mandates from governments worldwide for advanced safety features in vehicles. This market is a segment of the broader advanced driver assistance systems (ADAS) market, reflecting the automotive industry's shift toward more intelligent and autonomous vehicles.

The demand for lane warning systems was being bolstered by the rising production of passenger vehicles and the integration of advanced safety features as standard offerings by automobile manufacturers. Consumer preferences were increasingly leaning toward vehicles equipped with advanced safety technologies, partly due to a growing awareness of road safety issues and partly due to the higher perceived value of these technologically-equipped vehicles.

Technological advancements played a crucial role in this market. Innovations in camera, sensor, and artificial intelligence technologies were making lane warning systems more accurate and reliable. The integration of these systems with other safety features, like adaptive cruise control and blind spot detection, creates more comprehensive safety solutions, further driving the market growth.

Regionally, markets in Europe and North America were leading in terms of adoption largely due to stringent government regulations requiring the incorporation of advanced safety systems in vehicles. However, Asia-Pacific was emerging as a rapidly growing market, with countries like China and Japan investing heavily in automotive technology and infrastructure development.

The future of the lane warning systems market appeared promising, with potential growth opportunities in the integration of these systems into the expansion of autonomous and semi-autonomous vehicles.

Automotive Lane Warning Systems Market Trends

The Passenger Cars Segment is Driving the Market Growth

The passenger car segment is leading the automotive lane warning system market, with the global rise in passenger car production and sales playing a significant role. With the increasing affordability and availability of passenger cars, particularly in emerging economies, the demand for advanced safety features like lane warning systems has also escalated. These systems, initially seen as luxury or high-end options, were becoming more mainstream, driven both by consumer demand for safer vehicles and by regulatory pressures.

Regulatory influences were indeed significant. Many regions, including Europe and North America, have been implementing stringent safety regulations mandating or strongly encouraging the inclusion of advanced safety systems in new vehicles. This regulatory push effectively broadened the market for lane warning systems in the passenger car segment.

The integration of sophisticated sensors, cameras, and software not only improved the effectiveness of lane warning systems but also made them more cost-effective over time. As technology became more accessible and less expensive to produce, automakers started incorporating these systems across a wider range of models, including mid-range vehicles.

Growing public awareness about road safety issues and the benefits of advanced driver assistance systems (ADAS) is influencing buying decisions. Consumers were increasingly opting for vehicles equipped with safety features like lane departure warnings, which they viewed as essential for driving safety.

Moreover, the rise of connected and autonomous vehicles presented additional growth opportunities for the lane warning system market within the passenger car segment. As automakers invested in developing semi-autonomous and autonomous vehicles, the integration of sophisticated lane warning systems and other ADAS technologies became crucial.

This trend is expected to continue with innovations in ADAS that further enhance the safety and appeal of passenger vehicles.

North America is the Leading Market for Automotive Lane Warning Systems

North America has emerged as a leading market for automotive lane warning systems, a trend driven by a confluence of factors. The region, particularly the United States and Canada, boasts one of the highest rates of vehicle ownership per capita globally, creating a vast market for advanced automotive technologies, including lane warning systems.

Regulatory initiatives in these countries have been pivotal, with proactive measures encouraging or even mandating the adoption of safety technologies in vehicles. This regulatory push is complemented by the region's strong technological innovation, with many leading automotive and technology companies based here continually developing cutting-edge driver assistance systems.

Moreover, there is a significant consumer awareness and prioritization of vehicle safety in North America. This awareness, coupled with the willingness to invest in safety technologies, has further propelled the market for lane warning systems. Additionally, various road safety initiatives by governments and organizations have emphasized the importance of advanced safety features in vehicles.

Economic factors also play a role as the robust economies of North American countries enable both individual consumers and fleet operators to invest in newer, safer vehicles equipped with these advanced technologies. All these aspects synergistically contribute to North America's position as a key market in the realm of automotive lane warning systems.

The Canadian government announced the safe testing of every vehicle and deployment of automated and connected vehicles while spreading awareness regarding driver assistance technologies.

- In May 2022, GM announced its constructive partnership with INRIX Inc. to provide safety solutions data directly to the US Department of Transportation through its analytics-assisted cloud-based application under its Safety View by GM Future Roads & Inrix initiative.

- In May 2022, Toyota Motors announced that it would use computer-based vision technology sourced from Austin, Texas-based start-up company Invisible AI in its North American assembly plants. This technology shall be able to process body motion data to enhance quality, safety, and efficiency.

Due to the factors above, the demand for vehicle safety solutions is likely to increase. This is expected to propel the growth of the studied market between 2024 and 2029.

Automotive Lane Warning Systems Industry Overview

The automotive lane warning system market is dominated by players such as Continental AG, Delphi Technologies, Mobileye, Robert Bosch GmbH, Hitachi Ltd, ZF Friedrichshafen AG, DENSO Corporation, and Magna International Inc.

Companies are engaging in partnerships and acquisitions to develop new products and expand within the market. For instance,

- In November 2023, Honda Motor Co. Ltd unveiled its latest innovation, the Honda SENSING 360, an all-encompassing safety and driver-assistance system. This advanced technology is designed to eliminate blind spots surrounding the vehicle, aiding in preventing collisions and lessening the driver's workload during operation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Increased Safety Awareness is Driving the Market Growth

- 4.2 Market Restraints

- 4.2.1 Cybersecurity Concerns is Anticipated to Restrain the Market Growth

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in Value USD Billion)

- 5.1 Function Type

- 5.1.1 Lane Departure Warning System

- 5.1.2 Lane Keeping System

- 5.2 Sensor Type

- 5.2.1 Video Sensors

- 5.2.2 Laser Sensors

- 5.2.3 Infrared Sensors

- 5.3 Sales Channel

- 5.3.1 OEM

- 5.3.2 Aftermarket

- 5.4 Vehicle Type

- 5.4.1 Passenger Cars

- 5.4.2 Light Commercial Vehicles

- 5.4.3 Heavy Commercial Vehicles

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Russia

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 India

- 5.5.3.2 China

- 5.5.3.3 Japan

- 5.5.3.4 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Continental AG

- 6.2.2 Delphi Technologies

- 6.2.3 Mobileye

- 6.2.4 DENSO Corporation

- 6.2.5 Robert Bosch GmbH

- 6.2.6 The Bendix Corporation

- 6.2.7 Hitachi Ltd

- 6.2.8 Iteris Inc.

- 6.2.9 Nissan Motor Co. Ltd

- 6.2.10 Volkswagen AG

- 6.2.11 ZF TRW