|

시장보고서

상품코드

1523308

자동차용 엔진 관리 시스템 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2024-2029년)Automotive Engine Management System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

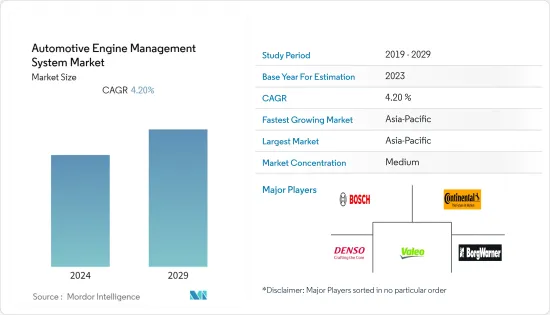

자동차용 엔진 관리 시스템 시장 규모는 2024년에 662억 달러로 추정되고, 2029년에는 848억 달러에 이를 것으로 예측되며, 예측 기간 중(2024-2029년) CAGR은 4.20%로 성장할 것으로 예측됩니다.

장기적으로는 저연비 차량을 요구하는 소비자 동향 증가가 엔진 동작을 제어하는 선진 컴포넌트의 개발을 제조업체에 촉구하고 있습니다. 세계의 온실가스 농도 상승으로 엄격한 배기가스 규제 제정이 크게 증가할 가능성이 높습니다.

승용차 판매와 생산 증가에 따라 세계 자동차 부문은 해마다 급격한 성장을 이루고 있습니다. 예를 들어 인도의 2022-23년도 승용차 판매 대수는 전년도 대비 14,67,039대에서 17,47,376대로, 유틸리티 차량는 14,89,219대에서 20,03,718대로, 밴은 1,13,265대에서 1, 39,020대로 증가했습니다.

자동차 수요가 증가함에 따라 엔진 관리 기업은 높은 수요에 대응하기 위해 제품 투입, 생산 능력 확대, 합병 등의 전략적 움직임을 채택하고 있습니다.

주요 하이라이트

- 2023년 7월, 발레오는 Sanand 공장에서 초음파 센서의 생산 능력을 700만 유닛으로 확대했습니다. Sanand의 첫 생산 라인은 2021년 11월에 시작되었습니다. 이 추가 라인으로 총 생산 능력은 연간 300만 유닛에서 700만 유닛으로 증가했습니다.

- 2023년 1월 센서타는 자동차 및 대형 차량 오프로드(HVOR) 용도을 위한 광범위한 미션 크리티컬 센서 및 전기 보호 솔루션을 전시했습니다.

북미는 세계에서 가장 빠르게 성장하는 자동차용 엔진 관리 시스템 시장입니다. 그러나 특히 중국과 인도에서 자동차 판매량이 많기 때문에 아시아태평양의 자동차용 엔진 관리 시스템이 큰 시장 점유율을 차지하고 있습니다. 인도와 중국의 고객은 자동차 성능 향상에 대한 인식이 높아지고 있으며, 이는 자동차용 엔진 관리 시스템 시장을 밀어 올릴 것으로 예상됩니다.

자동차용 엔진 관리 시스템 시장 동향

승용차가 가장 높은 시장 점유율을 차지

승용차는 세련되고 컴팩트한 디자인과 경제적 가치와 같은 특징으로 소비자들 사이에서 매우 인기가 있습니다. 승용차 수요 증가는 중류 계급의 인구 증가와 신흥국의 생활 수준의 향상도 영향을 미치고 있습니다.

스포츠용 다목적 차량(SUV) 수요 증가는 인도에서 승용차 판매의 50% 이상을 스포츠용 다목적 차량 판매가 차지하고 있기 때문에 시장 기업에게 수익 기회를 창출하고 있습니다. 인도나 중국과 같은 나라에서는 지상고가 높은 대형차를 선호하는 등 다양한 요인들로부터 스포츠용 다목적차 수요가 급증했습니다.

게다가 세제 보조금과 충전기 인프라의 확충에 의한 전기자동차 수요 증가도 시장의 성장을 가져왔습니다. 인도의 2023년 1분기 전기차 판매량은 2022년 동시기의 2배에 달했습니다.

국제청정교통평의회에 따르면 미국의 전기차 판매량은 100만대를 넘어섰습니다. 특히 2023년 1-3분기까지 판매량은 2022년 동기 대비 약 58% 증가했습니다.

승용차 부문의 성장에 따라 전자제어유닛과 엔진센서 등 각종 엔진관리시스템 수요는 앞으로도 비약적으로 성장할 것으로 예상됩니다. 안전성과 편의성과 관련된 고급 기능의 동향이 진행됨에 따라 자동차의 기능 탑재가 진행되고 있습니다. 게다가 자율주행차와 전기자동차에 대한 수요 증가는 엔진 관리 시스템에 새로운 기회를 가져올 것으로 예상됩니다.

기업은 또한 시장의 높은 수요에 대응하기 위해 기술적으로 고급 제품을 생산하고 생산 능력을 확대하는 데 주력하고 있습니다. 예를 들어, 2023년 6월 MEMS 기반 솔리드 스테이트 자동차 라이더와 ADAS(선진 운전 지원 시스템) 솔루션의 리더인 MicroVision Inc.는 솔리드 스테이트 플래시 기반 MOVIA 라이더 센서를 출시했습니다. MOVIA 센서는 작고 가볍기 때문에 다양한 용도에 적합합니다.

아시아태평양이 가장 높은 시장 점유율을 차지

예측 기간 동안 아시아태평양이 주요 시장 점유율을 차지할 것으로 예상됩니다. 이 지역의 성장은 주로 인도, 중국, 일본 등 자동차 생산 상위 국가가 견인하고 있습니다.

기타 촉진요인으로는 운전 체험의 향상, 쾌적성, 안전성을 제공하는 자동차에 대한 수요 증가, 저연비 엔진에 대한 수요 증가 등을 들 수 있습니다. 인도와 같은 국가에서는 엄격한 규제, 보조금, 세액 공제 및 기타 우대 조치를 통해 엔진 관리 시스템의 채택을 추진하고 있기 때문에 전기자동차 판매가 증가하고 있음이 엔진 관리 시스템의 사용을 더욱 밀어줍니다.

- 인도의 도로 교통 고속도로성(MoRTH)은 자동차의 연비 효율을 높이기 위해 2023년부터 연비 기준에의 적합을 의무화했습니다. 플렉스 연료차에 관한 새로운 가이드라인은 내연 기관차의 성장에 기여하고 있습니다.

- 중국은 연료 펌프와 인젝터를 공급하는 엔진 관리 시스템(EMS) 분야에서 세계 시장 점유율을 선도하고 있습니다. 디젤 엔진의 새로운 배기가스 규제는 중국의 엔진 관리 회사에 대한 추가적인 비즈니스 기회를 의미할 수 있습니다.

전통적인 IC 엔진 차량과는 별도로 전기자동차 수요가 시장 성장을 뒷받침할 것으로 예상됩니다. 각 지역에서 배기가스 규제가 엄격해져 예측기간 동안 전기차 수요가 증가할 가능성이 높습니다. International Council of Clean Transportation에 따르면, 중국은 세계 최대의 EV 시장으로 계속 2023년 상반기에 약 300만대의 EV가 판매되었습니다.

- 2024년 1월 현재 중국 제조업체는 자율주행 기술의 라이더 혁신으로 주도권을 잡고 있으며, 2000년 이후 라이더 관련 특허 출원 건수는 25,957건으로 경이적이며 미국 기업과 일본 기업을 웃돌고 있습니다.

자동차용 엔진 관리 시스템 산업 개요

자동차용 엔진 관리 시스템 시장은 세계적으로 그리고 지역적으로 확립된 선수에 의해 통합되고 주도되고 있습니다. 각 회사는 신제품 투입, 제휴, 합병 등의 전략을 채용하여 시장에서의 지위를 유지하고 있습니다.

- 예를 들어 TTTech Auto는 2023년 4월 고급 네트워크 기능을 갖춘 고성능 ECU, N4 Network Controller를 출시했습니다. N4는 최신 자동차 E/E 아키텍처에서 중심적인 역할을 하도록 설계되어 있어 소프트웨어 정의의 자동차로 가는 길을 열었습니다.

이 시장의 주요 기업으로는 콘티넨탈 AG, 주식회사 덴소, 주식회사 발레오, 로버트 보쉬 GmbH 등이 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 성장 촉진요인

- 승용차 판매 증가

- 시장 성장 억제요인

- 안전 장비 추가로 차량 비용 상승

- 업계의 매력도-Porter's Five Forces 분석

- 신규 진입업자의 위협

- 구매자 및 소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화

- 자동차 유형별

- 승용차

- 상용차

- 컴포넌트 유형별

- 엔진 제어 유닛(ECU)

- 엔진 센서

- 연료 펌프

- 기타 컴포넌트 유형

- 지역별

- 북미

- 미국

- 캐나다

- 기타 북미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 인도

- 중국

- 일본

- 한국

- 기타 아시아태평양

- 세계 기타 지역

- 남미

- 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 벤더의 시장 점유율

- 기업 프로파일

- Robert Bosch GmbH

- Continental AG

- BorgWarner Inc.

- DENSO Corporation

- Hella KGaA Hueck & Co.

- Infineon Technologies AG

- Sensata Technologies

- Mobiletron Electronics Co. Ltd

- NGK Spark Plugs Pvt Ltd.

- Hitachi Automotive Systems Ltd

- Dover Corporation

제7장 시장 기회 및 향후 동향

AJY 24.08.08The Automotive Engine Management System Market size is estimated at USD 66.20 billion in 2024, and is expected to reach USD 84.80 billion by 2029, growing at a CAGR of 4.20% during the forecast period (2024-2029).

Over the long term, the growing consumer trend toward fuel-efficient vehicles has encouraged manufacturers to develop advanced components that control engine operation. The enactment of stringent emission norms is likely to increase significantly due to the rise in greenhouse gas levels globally.

With the growth in sales and production of passenger cars, the global automotive sector has been witnessing exponential growth year on year. For instance, the sales of passenger cars in India increased from 14,67,039 to 17,47,376, utility vehicles from 14,89,219 to 20,03,718, and vans from 1,13,265 to 1,39,020 units in FY 2022-23, compared to the previous year.

With the growth in demand for vehicles, engine management companies are adopting strategic moves such as product launches, capacity expansion, and mergers to cater to the high demand.

Key Highlights

- In July 2023, Valeo expanded its ultrasonic sensor manufacturing capacity to 7 million units at the Sanand plant. The first production line at Sanand was started in November 2021. With this additional line, the total production capacity increased from 3 million to 7 million units annually.

- In January 2023, Sensata showcased its broad range of mission-critical sensors and electrical protection solutions for automotive and heavy vehicle off-road (HVOR) applications.

North America is the fastest automotive engine management systems market in the world. However, due to the more significant automotive sales, especially in China and India, the automotive engine management systems in Asia-Pacific hold the major market share. Customers in India and China are becoming more aware of enhancing their vehicles' performance, which is expected to boost the automotive engine management system market.

Automotive Engine Management System Market Trends

Passenger Cars Holds Highest Market Share

Passenger cars have become exceptionally popular among consumers due to features like their stylish and compact design and economic value. The rise in the demand for passenger cars is also influenced by the increasing middle-class population and the enhanced standard of living in emerging countries.

The rise in demand for sports utility vehicles (SUVs) creates profitable opportunities for market players as the sale of sports utility vehicles accounts for more than 50% of passenger car sales in India. The demand for sports utility vehicles in countries like India and China surged due to various factors, such as buying preference for bigger cars with high ground clearance.

Furthermore, the increase in demand for electric vehicles due to tax subsidies and expansion in charger infrastructure also resulted in the growth of the market. Electric car sales in India in the first quarter of 2023 were double what they were in the same period in 2022.

According to the International Council of Clean Transportation, the sales of electric vehicles in the United States crossed 1 million. Notably, the sales through the first three quarters of 2023 were about 58% higher than the same period in 2022.

With the growth in the passenger car segment, demand for various engine management systems, such as electronic control units and engine sensors, is expected to continue to grow exponentially in the future. With the ongoing trend of advanced features related to safety and convenience, cars are becoming more feature-loaded. Moreover, the rise in demand for autonomous and electric vehicles is anticipated to create new opportunities for engine management systems.

Companies are also focusing on creating technologically advanced products and expanding their capacity to cater to the high demand in the market. For example, in June 2023, MicroVision Inc., a leader in MEMS-based solid-state automotive lidar and advanced driver-assistance systems (ADAS) solutions, launched its solid-state flash-based MOVIA lidar sensor. The small form factor and light weight of the MOVIA sensor make it appealing for a wide variety of applications.

Asia-Pacific Holds the Highest Market Share

Asia-Pacific is expected to hold a major market share during the forecast period. The regional growth is mainly driven by the top-producing automotive countries like India, China, and Japan.

Other driving factors include the increase in demand for automobiles that provide enhanced driving experiences, comfort, and safety and an increase in demand for fuel-efficient engines. The rise in the sale of electric vehicles has further boosted the use of engine management systems, as countries like India are promoting their adoption through strict regulations, subsidies, tax credits, and other incentives.

- The Ministry of Road Transport and Highways (MoRTH) in India made it mandatory for vehicles to comply with fuel consumption standards from 2023 to make vehicles fuel efficient. The new guidelines on flex-fuel vehicles contribute to the growth of ICE engines.

- China is leading the global market share in the engine management system (EMS) segment, supplying fuel pumps and injectors. New emission norms for diesel engines could mean additional opportunities for Chinese engine management companies.

Apart from conventional IC engine vehicles, the demand for electric vehicles is anticipated to boost the growth of the market. With stringent emission regulations across every region, the demand for electric vehicles is likely to increase during the forecast period. According to the International Council of Clean Transportation, China remained the world's largest EV market, with approximately 3 million EVs sold in 2023 H1.

- As of January 2024, Chinese manufacturers continue to lead the charge in lidar innovation of autonomous driving technology and have filed a staggering 25,957 patent applications related to lidar since 2000, surpassing American and Japanese companies.

Automotive Engine Management System Industry Overview

The automotive engine management system market is consolidated and led by globally and regionally established players. The companies adopt strategies such as new product launches, collaborations, and mergers to sustain their market positions.

- For instance, in April 2023, TTTech Auto launched the N4 Network Controller, a high-performance ECU with advanced networking capabilities. The N4 is designed to play a central role in modern automotive E/E architectures, paving the way to software-defined vehicles.

Some of the major players in the market include Continental AG, DENSO Corporation, DENSO Corporation, Valeo, and Robert Bosch GmbH.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Increase in Sales of Passenger Cars

- 4.3 Market Restraints

- 4.4 Increased Cost of Vehicles Due to Additional Safety Features

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD Billion)

- 5.1 By Vehicle Type

- 5.1.1 Passenger Car

- 5.1.2 Commercial Vehicle

- 5.2 By Component Type

- 5.2.1 Engine Control Unit (ECU)

- 5.2.2 Engine Sensors

- 5.2.3 Fuel Pump

- 5.2.4 Other Component Types

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia Pacific

- 5.3.3.1 India

- 5.3.3.2 China

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Rest of the World

- 5.3.4.1 South America

- 5.3.4.2 Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles*

- 6.2.1 Robert Bosch GmbH

- 6.2.2 Continental AG

- 6.2.3 BorgWarner Inc.

- 6.2.4 DENSO Corporation

- 6.2.5 Hella KGaA Hueck & Co.

- 6.2.6 Infineon Technologies AG

- 6.2.7 Sensata Technologies

- 6.2.8 Mobiletron Electronics Co. Ltd

- 6.2.9 NGK Spark Plugs Pvt Ltd.

- 6.2.10 Hitachi Automotive Systems Ltd

- 6.2.11 Dover Corporation