|

시장보고서

상품코드

1523356

무산소 구리 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2024-2029년)Oxygen Free Copper - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

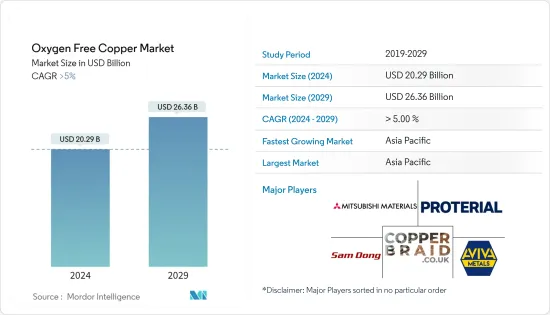

무산소 구리 시장 규모는 2024년 202억 9,000만 달러로 추정되고, 2029년 263억 6,000만 달러에 이를 것으로 예측되며, 예측 기간 동안 복합 연간 성장률(CAGR)은 5% 이상으로 성장할 전망입니다.

COVID-19 팬데믹은 생산과 이동이 둔화되고 반도체가 부족하여 무산소 구리 시장에 부정적인 영향을 미쳤습니다. 또한 전자 및 자동차 등의 산업도 봉쇄 대책과 경제적 혼란으로 인해 생산 지연을 강요했습니다. 현재 시장은 유행에서 회복하고 있습니다. 시장은 2022년에는 유행 이전 수준에 이르렀으며 앞으로도 안정적인 성장이 예상됩니다.

반도체의 무산소 구리 수요 증가는 예측 기간 동안 시장 성장을 견인하고 있습니다.

그러나 구리 비용이 높은 것은 조사된 시장의 성장을 방해할 것으로 예상됩니다.

무산소 구리의 폭넓은 전자 기기에의 응용이 성장할 전망이며 있어 향후 5년간의 무산소 구리 시장에 기회를 가져올 것으로 보입니다.

아시아태평양은 중국과 인도와 같은 국가의 소비가 증가하고 있으며 세계에서 우위를 차지하고 있습니다.

무산소 구리 시장 동향

시장을 독점하는 것은 전기 및 전자산업

- 전기 및 전자산업은 반도체나 초전도체의 제조에 널리 사용되고 있기 때문에 시장을 독점하는 부문이 될 것입니다.

- 무산소 구리는 반도체나 초전도체의 제조, 플라즈마 증착이 필요한 입자 가속기와 같은 고진공 시스템 등의 제조 용도로 자주 사용됩니다.

- 산소나 기타 불순물이 있으면 시스템에서 사용되는 재료와 바람직하지 않은 화학 반응을 일으키기 때문입니다.

- 무산소 구리은 인쇄회로기판, 마이크로파관, 진공커패시터, 진공차단기, 진공씰, 도파관, 라디오나 텔레비전의 송신기나 마그네트론용 진공관 등 폭넓은 용도로 사용되기 때문에 소비량이 성장할 전망이며 있습니다.

- 휴대전화, 스마트 기기, 태블릿, TV 세트 등 세계에서 전자 기기의 수가 급격히 늘어나고 있는 것이 예측 기간 동안 무산소 구리 수요를 끌어올릴 것으로 보입니다. 이처럼 전기 및 전자산업에서의 사용량이 늘어나 응용범위도 넓어지고 있기 때문에 시장 성장의 원동력이 될 것으로 예상됩니다.

- 일본전자정보기술산업협회(JEITA)에 따르면 세계 전자,IT산업의 생산고는 2021년 3조 4,159억 달러에 비해 2022년 3조 4,368억 달러로 추정되고 전년대비 1%의 성장률을 기록했습니다. 게다가 2023년에는 전년 대비 3%의 성장률로 3조 5,266억 달러에 달할 것으로 예상되고 있습니다.

- 또한 전자정보기술부에 따르면 인도 전역의 가전(TV, 액세서리, 오디오)의 생산액은 2022년도에 7,450억 루피(94억 6,000만 달러)를 넘어 시장 성장을 지원하고 있다.

- 이상과 같은 요인이 예측 기간 중 무산소 동 시장을 견인해 갈 것으로 보입니다.

아시아태평양이 시장을 독점

- 중국, 일본, 인도 등 아시아태평양의 신흥 국가에서는 전자 반도체 장치에 대한 수요가 증가하고 있으며, 아시아태평양 시장은 예측 기간 동안 가장 크고 가장 빠르게 성장하는 시장이 될 것으로 예상됩니다.

- 스마트폰, PC, 노트북, 기타 의료용 전자제품 등 소비자용 장비에 대한 수요는 아시아태평양을 통해 빠르게 성장할 전망이며 있으며 인도, 일본, 중국이 시장 성장에 크게 기여하고 있습니다.

- 산업정보화성(MIIT)에 따르면 중국은 세계 최대의 가전생산국이며 세계 점유율은 60%를 넘고 있습니다.

- 일본전자정보기술산업협회(JEITA)에 따르면 일본 일렉트로닉스산업의 국내 생산액은 2022년 11조 1,243억엔(-851억 9,000만 달러)으로 추정되고 전년대비 2%의 성장률을 보였습니다. 있습니다. 일본의 일렉트로닉스 산업에 의한 국내 생산은 2023년에는 11조 4,029억엔(-873억 2,000만 달러)에 이를 전망이며 전년대비 3%의 성장률을 나타낼 것으로 예상됩니다.

- 아시아태평양의 에너지 부문도 높은 에너지 수요에 힘입어 활황을 보이고 있습니다. 급성장하는 산업 부문은 이 지역의 에너지 수요를 촉진하는 주요 요인 중 하나이며, 이는 예측 기간 동안 시장 성장을 지원합니다.

- 아시아태평양의 화력발전부문은 성장을 기록하고 있으며, 주로 중국이 이 부문의 성장을 견인하고 있습니다. 중국은 세계 어느 나라와 지역보다 석탄 화력 발전소가 많습니다. 중국 본토에서는 2022년 7월 현재 1,118기의 석탄화력발전소가 가동되고 있습니다. 이것은 2위 인도의 약 4배입니다. 중국은 세계 석탄 발전의 절반 이상을 차지합니다.

- 앞서 언급한 요인은 예측 기간 동안 이 지역에서 무산소 구리 소비 수요 증가에 기여할 것으로 예상됩니다.

무산소 구리 산업 개요

무산소 구리 시장은 세분화되어 있습니다. 조사된 시장의 주요 기업(순부동)에는 Copper Braid Products, 미쓰비시 머티리얼, Aviva Metals, PROTERIAL Ltd, Sam Dong 등이 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트,지원

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 성장 촉진요인

- 반도체로부터 수요 증가

- 자동차 분야로부터 수요 증가

- 기타 촉진요인

- 억제요인

- 구리의 비용 고

- 기타 억제요인

- 산업 밸류체인 분석

- Porter's Five Forces 분석

- 신규 진입업자의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁도

제5장 시장 세분화(금액 베이스 시장 규모)

- 등급

- CU-OF

- CU-OFE

- 제품

- 와이어

- 스트립

- 버스바, 로드

- 기타(튜브, 파이프 등)

- 최종 사용자 산업

- 전기 및 전자

- 자동차

- 산업

- 기타(발전, 항공우주 등)

- 지역

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 말레이시아

- 태국의

- 인도세이아의

- 베트남

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 북유럽 국가

- 터키

- 러시아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 콜롬비아

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 나이지리아

- 카타르

- 이집트

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- M&A, 합작사업, 제휴, 협정

- 시장 점유율(%)/랭킹 분석

- 주요 기업의 전략

- 기업 프로파일

- Aviva Metals

- Citizen Metalloys Ltd

- Copper Braid Products

- Cupori

- Farmers Copper LTD

- FURUKAWA ELECTRIC CO. LTD

- KGHM

- KME GERMANY GMBH

- Metrod Holdings Berhad

- Sam Dong

- Lacroix Kress GmbH

- Mitsubishi Materials Corporation

- PROTERIAL Ltd

제7장 시장 기회와 앞으로의 동향

BJH 24.08.09The Oxygen Free Copper Market size is estimated at USD 20.29 billion in 2024, and is expected to reach USD 26.36 billion by 2029, growing at a CAGR of greater than 5% during the forecast period (2024-2029).

The market was negatively impacted by the COVID-19 pandemic as there was a slowdown in production and mobility, which caused a shortage of semiconductors, which negatively impacted the market for oxygen-free copper. Also, industries such as electronics, automotive, etc., were forced to delay their production due to containment measures and economic disruptions. Currently, the market has recovered from the pandemic. The market reached pre-pandemic levels in 2022, and it is expected to grow steadily in the future.

Increasing demand for oxygen-free copper from semiconductors has been driving the market growth during the forecast period.

However, the high cost of copper is anticipated to hinder the growth of the studied market.

Growing oxygen-free copper applications in a wide range of electronics are likely to provide opportunities for the oxygen-free copper market over the next five years.

The Asia-Pacific region is dominated across the world, with increasing consumption from countries like China and India.

Oxygen Free Copper Market Trends

Electrical and Electronics Industry to Dominate the Market

- The electrical and electronics industry stands to be the dominating segment owing to wide consumption in the manufacturing of semiconductors and superconductors.

- Oxygen-free copper is commonly used in manufacturing applications such as the manufacture of semiconductors and superconductors and high-vacuum systems such as particle accelerators requiring plasma deposition.

- The use of oxygen-free materials is critical in these applications, as the presence of oxygen or some other impurity contributes to unwanted chemical reactions with the materials used in the system.

- Oxygen-free copper is witnessing growth in consumption due to its wide application in printed circuit boards, microwave tubes, vacuum capacitors, vacuum interrupters, vacuum seals, waveguides, and vacuum tubes for radio and TV transmitters and magnetrons.

- The exponential growth in the number of electronic gadgets across the globe, such as mobile phones, smart devices, tablets, and TV sets, is expected to drive the demand for oxygen-free copper over the forecast period. Thus, the increasing usage and widening arena of application in the electrical and electronics industry is expected to drive market growth.

- According to the Japan Electronics and Information Technology Industries Association (JEITA), the production by the global electronics and IT industry was estimated at USD 3,436.8 billion in 2022, registering a growth rate of 1% year-on-year, compared to USD 3,415.9 billion in 2021. Moreover, the industry is expected to reach USD 3,526.6 billion, with a growth rate of 3% year-on-year in 2023.

- Moreover, according to the Ministry of Electronics and Information Technology, the production value of consumer electronics (TV, accessories, and audio) across India was above INR 745 billion (USD 9.46 billion) in fiscal year 2022, thus supporting the growth of the market.

- All the aforementioned factors are expected to drive the oxygen-free copper market during the forecast period.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific market is expected to be the largest and fastest-growing market over the forecast period, owing to the increasing demand for electronic semiconductor devices in developing countries of Asia-Pacific, such as China, Japan, and India.

- Demand for consumer devices, such as smartphones, PCs, laptops, and other medical electronics products, is growing rapidly through the Asia-Pacific region, with India, Japan, and China contributing majorly to the market growth.

- According to the Ministry of Industry and Information Technology (MIIT), China is the world's largest producer of consumer electronics, with a global share of more than 60%.

- Furthermore, Japan is one of the largest producers of electronics; as per the Japan Electronics and Information Technology Industries Association (JEITA), the domestic production by the Japanese electronics industry was estimated at JPY 11,124.3 billion (~USD 85.19 billion) in 2022, witnessing a growth rate of 2% compared to the previous year. The domestic production by the Japanese electronics industry is likely to reach JPY 11,402.9 billion (~USD 87.32 billion) by 2023, registering a growth rate of 3% year-on-year.

- The Asia-Pacific energy sector is also thriving, owing to the high demand for energy. The rapidly growing industrial sector is one of the key factors driving the energy demand in the region, which in turn is supporting the market growth during the forecast period.

- The Asia-Pacific thermal sector is registering growth, with China primarily driving the growth of the sector. China has the most coal-fired power plants of any country or territory in the world. On the Chinese Mainland, as of July 2022, there were 1,118 operational coal power plants. This is approximately four times the number of such power plants in India, which came in second place. China accounts for more than half of the world's coal electricity generation.

- The aforementioned factors are anticipated to contribute to the increasing demand for oxygen-free copper consumption in the region during the forecast period.

Oxygen Free Copper Industry Overview

The oxygen-free copper market is fragmented in nature. The major players in the studied market (not in any particular order) include Copper Braid Products, Mitsubishi Materials Corporation, Aviva Metals, PROTERIAL Ltd, and Sam Dong.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand from Semiconductor

- 4.1.2 Increasing Demand from Automotive Sector

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 High Cost of Copper

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Grade

- 5.1.1 CU-OF

- 5.1.2 CU-OFE

- 5.2 Product

- 5.2.1 Wires

- 5.2.2 Strips

- 5.2.3 Busbars and Rods

- 5.2.4 Other Products (Tubes and Pipes, Etc.)

- 5.3 End-user Industry

- 5.3.1 Electrical and Electronics

- 5.3.2 Automotive

- 5.3.3 Industrial

- 5.3.4 Other End-user Industries (Power Generation, Aerospace, Etc.)

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Thailand

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 NORDIC Countries

- 5.4.3.7 Turkey

- 5.4.3.8 Russia

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Nigeria

- 5.4.5.4 Qatar

- 5.4.5.5 Egypt

- 5.4.5.6 UAE

- 5.4.5.7 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Aviva Metals

- 6.4.2 Citizen Metalloys Ltd

- 6.4.3 Copper Braid Products

- 6.4.4 Cupori

- 6.4.5 Farmers Copper LTD

- 6.4.6 FURUKAWA ELECTRIC CO. LTD

- 6.4.7 KGHM

- 6.4.8 KME GERMANY GMBH

- 6.4.9 Metrod Holdings Berhad

- 6.4.10 Sam Dong

- 6.4.11 Lacroix + Kress GmbH

- 6.4.12 Mitsubishi Materials Corporation

- 6.4.13 PROTERIAL Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Oxygen-free Copper Application in Wide Range of Electronics

- 7.2 Other Opportunities