|

시장보고서

상품코드

1939103

자동차 코팅 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Automotive Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

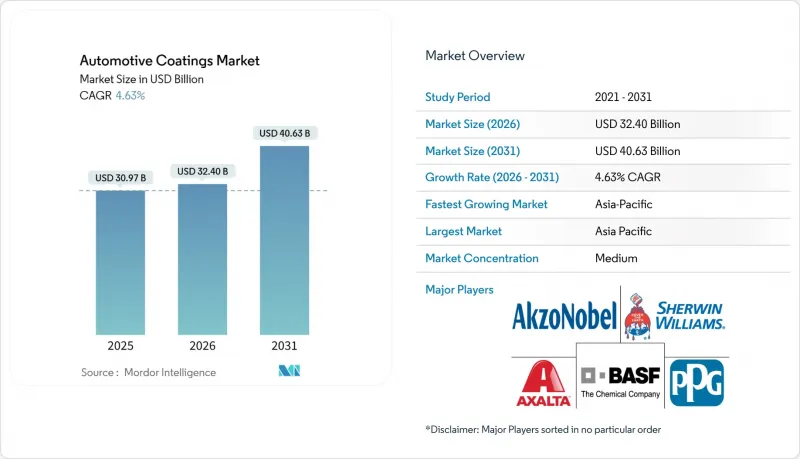

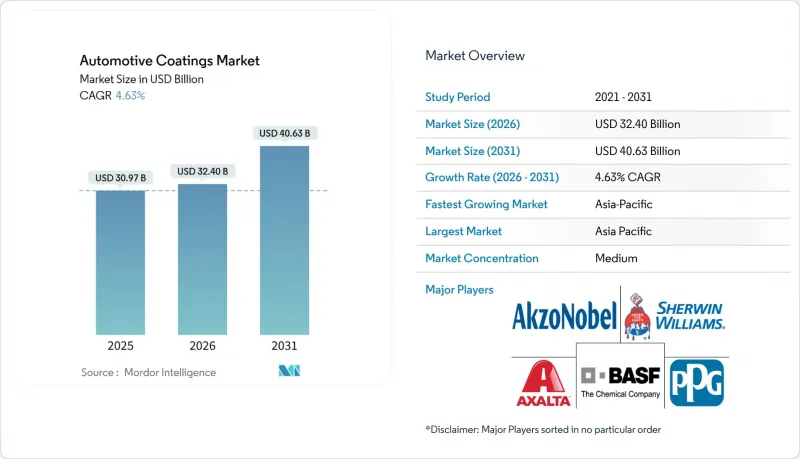

자동차 코팅 시장은 2025년에 296억 달러로 평가되었으며, 2026년 309억 7,000만 달러에서 2031년까지 388억 2,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년) 동안 CAGR은 4.62%로 예상됩니다.

세계 자동차 생산의 회복, 저휘발성 유기화합물(VOC) 배합으로의 전환, 전기자동차(EV) 생산의 급격한 증가가 수요 확대를 뒷받침하고 있습니다. 한편, 원재료 가격 변동과 용제 규제 강화는 수익률을 압박하는 요인으로 작용하고 있습니다. 공급업체들은 곧 시행될 배출가스 규제에 대응하면서 OEM 수준의 내구성을 유지하는 수성 도료 및 분체 도장 시스템 도입에 박차를 가하고 있습니다. 인라인 경화, 로봇 검사, 클라우드 기반 컬러 매칭을 아우르는 OEM 도장 공장의 디지털화는 생산성을 향상시키는 동시에 진입 장벽을 기술적으로 높이고 있습니다. 한편, 대규모 지속가능성 및 자동화 프로그램에 투자할 수 있는 다국적 기업들에 맞서 지역 중견 공급업체들이 시장 점유율 경쟁을 벌이면서 시장 세분화는 계속되고 있습니다.

세계 자동차 코팅 시장 동향 및 인사이트

세계 자동차 생산 회복세 확대

북미 소형차 생산량은 2024년 1,550만 대에 달할 것으로 예상되며, 이는 외장 및 언더바디 도료에 대한 공장 수요를 뒷받침하고 있습니다. 경트럭이월 판매량의 84%를 차지하며, 프리미엄급 스크래치 방지 클리어 코트(상도) 소비를 촉진하고 있습니다. 중국에서는 생산능력 증설과 수출 모멘텀이 안정적인 도료 수요를 뒷받침하고 있지만, 지역적 과잉 생산능력에 대한 우려도 제기되고 있습니다. 팬데믹으로 인한 혼란 이후, 전 세계 자동차 제조업체들이 예측 가능한 조달 일정을 재개함에 따라 공급업체들은 일괄 생산 및 물류 최적화를 할 수 있게 되었습니다. OEM 업체들이 내구성 기준을 충족시키면서 브랜드 고유의 미학을 추구하는 가운데, 첨단 도장 공정의 자동화와 차별화된 마감재에 대한 투자가 병행되고 있습니다.

VOC 규제 대응을 위한 수성 및 분체 도장 시스템으로의 전환

캘리포니아 주에서 2025년 시행되는 엄격한 VOC 상한 규제와 EU 그린딜 대책의 진전에 따라 용제계 도료의 배합 재검토가 가속화되고 있습니다. 주요 바디샵에서 수성 베이스코트는 이미 64%의 보급률을 달성하여 상업적 타당성을 입증했습니다. BASF의 글라스릿 100 라인은 1,000개 이상의 충돌 수리 센터에서 채택된 고효율, 저VOC 제품의 대표적인 예입니다. 분말도장은 에너지 사용량을 50% 절감하는 레이저 경화로 보급으로 휠, 엔진룸 부품, EV 배터리 케이스 분야에서 점유율을 확대하고 있습니다. 광범위한 수지 및 안료 포트폴리오를 보유한 공급업체는 규제가 더욱 강화되기 전에 고객 전환을 빠르게 진행하여 선구자적 우위를 확보할 수 있습니다.

용매 및 이소시아네이트 노출의 엄격한 제한

미국 산업안전보건국(OSHA)의 중점 감시 프로그램에 따라 도장 부스에 대한 검사가 강화되고, 이소시아네이트에 의한 천식 및 피부염의 위험을 줄이기 위해 환기 시설 강화 및 개인보호구 착용이 의무화되었습니다. 소규모 재도장 사업자는 규제 대응 스프레이 부스 도입에 따른 막대한 자본 비용에 직면하거나, 성능을 희생할 수 있는 저 이소시아네이트 화학제품으로 전환해야 하는 상황에 직면해 있습니다. 프라이머 및 클리어 코트 제제 제조사들은 폴리우레아 프리 대체품을 상품화하고 있지만, 내구성 기준의 검증이 진행 중인 가운데, 채용에 신중을 기하고 있습니다.

부문 분석

2025년, 아크릴계 도료는 자동차 코팅 시장 수요의 48.10%를 차지할 것으로 예상되며, 비용 효율성과 균형 잡힌 내후성으로 그 입지를 확고히 할 것입니다. 폴리우레탄계 도료는 2031년까지 CAGR 5.00%로 확대될 것이며, 특히 고급 스포츠유틸리티차량(SUV)과 우수한 내스크래치성이 요구되는 전기자동차(EV)를 위한 프리미엄 클리어코팅 및 유연한 기판에 대한 수요를 충족시킬 것으로 예상됩니다. 폴리우레탄계 자동차 도료 시장 규모는 새로운 지방족 디이소시아네이트 화학 기술이 엄격한 황변 시험 기준을 충족시킴에 따라 북미 OEM 라인에서 눈에 띄게 확대될 것으로 예상됩니다. 부식 방지가 중요한 음극전착도장 분야에서는 에폭시 수지가 틈새 시장을 계속 독점하고 있는 반면, 유럽 OEM이 주도하는 컨셉 프로그램에서는 바이오 기반 하이브리드 기술이 부상하고 있습니다.

폴리우레탄 추진 움직임은 내구성 수요를 견인하는 소유주기가 길어짐에 따라 가속화되고 있습니다. 그러나 이소시아네이트 취급에 대한 미국 산업안전보건청(OSHA)의 감시가 강화됨에 따라 밀폐형 혼합 셀과 로봇 분무용 인클로저에 대한 투자를 장려하고 있습니다. 코베스트로와 같은 공급업체는 현재 33% 재생 탄소 폴리우레탄을 제공하고 있어 OEM의 지속가능성 목표에 부합하는 모습을 보여주고 있습니다. 아크릴계 화학업체들은 VOC 수준을 증가시키지 않으면서 내마모성을 향상시키는 차세대 가교제로 대응하고 있습니다. 경쟁 우위는 에너지 사용 규제와 경량화 요구 사항을 모두 충족하는 기계적 강인성과 저온 경화 특성을 결합한 특허 포트폴리오에 점점 더 의존하고 있습니다.

2025년에도 솔벤트계 도료는 메탈릭과 펄톤에 요구되는 우수한 유동성과 발색성으로 인해 매출의 70.20%를 차지했습니다. 그러나 전 세계 VOC 배출 제한이 강화됨에 따라 자동차 도료 시장은 분명히 대체 기술로 전환하고 있습니다. 수성 시스템은 현재 EU의 OEM 베이스 코트 라인에서 주류가 되고 있으며, 마쓰다와 같은 일본 OEM은 업계 최저 수준의 VOC 배출량인 15g/m2를 달성했습니다. 분말 코팅은 현재 소수이지만, 에너지 효율이 높은 레이저 경화 터널이 EV 부품 라인의 표준 장비가 됨에 따라 가장 높은 복합 성장률을 보이고 있습니다.

규제 지역에서는 차체 공장이 환경 허가를 준수하는 가운데, 자동차 코팅 시장에서 수성 수리 라인의 점유율이 60%를 넘어섰습니다. 수지 유화 기술과 플래시 오프 제어의 기술적 혁신으로 솔벤트 기반 프라이머와의 성능 차이가 해소되었습니다. Tier 1 공급업체는 모듈형 수지 구조를 활용하여 VOC 및 HAPS(유해대기오염물질) 허용치 인하로 인한 규제 강화 시 신속한 재배합이 가능하여, 규제 사이클 중 규제 준수에 따른 불의의 사태로부터 고객을 보호하고 있습니다.

지역별 분석

아시아태평양은 중국의 순수출국으로서의 부상과 EV 생산의 선도적 위치에 힘입어 2025년 세계 매출의 58.40%를 차지할 것으로 예상됩니다. 인도네시아의 백만 톤급 페인트 공장과 베트남의 급성장하는 공급업체 단지 등의 생산능력 증설이 이 지역의 CAGR 6.05% 예측을 뒷받침하고 있습니다. 국내 OEM 업체는 다국적 배합업체와 협력하여 용제계 기준과 외관 균일성을 유지하면서 수성수지의 국산화를 추진하고 있습니다. 정부의 신에너지 자동차에 대한 지원책은 배터리 전용 기능성 코팅에 대한 수요를 더욱 확대시키고 있습니다.

북미에서는 2024년 소형차 생산량이 9.6% 증가할 것으로 예상되며, 생산능력이 부족한 공장에서는 정격 처리량을 초과하는 가동이 일상화되어 도료 가격에 유리한 상황이 발생하고 있습니다. 미국 농무부(USDA)의 바이오프리퍼드 규제와 환경보호청(EPA)의 과불화알킬물질(PFAS) 규제 강화로 인해 불소 프리 탑코트의 신속한 인증이 촉진되고 있으며, 공급업체들은 연구개발을 가속화해야 하는 상황에 처해 있습니다. 캐나다와 멕시코의 사업장이 미국 규정을 준수함에 따라 저 VOC 시스템에서 자동차 코팅의 시장 점유율이 확대될 것으로 예상됩니다.

유럽의 탄소 중립에 대한 관심은 OEM 업체들이 100% 재생 가능 전력을 사용하는 도장 공장과 용제 회수 소각로를 도입하도록 유도하고 있습니다. 이산화티타늄 반덤핑 관세로 인해 비용 구조가 상승했지만, 드라이 스크러버 부스 및 폐쇄 루프 슬러지 재활용을 광범위하게 채택하여 비용 지출의 일부를 상쇄했습니다. 폴란드와 헝가리를 포함한 동유럽 클러스터의 성장은 저임금 조립을 제공하지만, 공급업체는 Tier 1 도장 모듈을 위한 저스트 인 시퀀스 허브 설치를 요구하고 있습니다.

남미에서는 메르코수르 관세 인하로 인해 자동차 제조업체들이 신형 SUV 플랫폼을 브라질과 아르헨티나에 배분하는 움직임이 가속화되면서 OEM용 도료 소비가 증가하고 있습니다. 그러나 환율 변동으로 인해 페인트 제조업체들은 달러 페그 계약을 도입할 수밖에 없는 상황에 처해 있습니다. 중동 및 아프리카는 아직 개발도상국이지만 사우디의 '비전 2030'이 국내 자동차 생산을 촉진하고, 수출 시장을 위한 코팅 설비 확충이 진행되는 등 미래성이 기대되는 지역입니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSM 26.03.09The Automotive Coatings Market was valued at USD 29.60 billion in 2025 and estimated to grow from USD 30.97 billion in 2026 to reach USD 38.82 billion by 2031, at a CAGR of 4.62% during the forecast period (2026-2031).

The rebound in global vehicle production, the pivot toward low-Volatile Organic Compound (VOC) formulations, and surging electric-vehicle (EV) output underpin demand expansion, even as raw-material price swings and tightening solvent regulations constrain margins. Suppliers are accelerating launches of water-borne and powder systems that comply with imminent emissions caps while still delivering Original Equipment Manufacturer (OEM)-level durability. OEM paint-shop digitalization spanning inline curing, robotic inspection, and cloud-based color matching is raising throughput and widening technical barriers to entry. Meanwhile, fragmentation persists as regional midsized suppliers vie for share against multinationals that can fund large-scale sustainability and automation programs.

Global Automotive Coatings Market Trends and Insights

Growing Global Vehicle Production Rebound

North American light-vehicle output reached 15.5 Million units in 2024 and continues rising, sustaining factory demand for exterior and under-body coatings. Light trucks now represent 84% of monthly sales, propelling the consumption of premium, scratch-resistant clear coats. In China, capacity additions and export momentum reinforce steady coating volumes, even as localized overcapacity looms. Automakers worldwide reinstate predictable sourcing schedules after pandemic disruptions, enabling suppliers to optimize batch production and logistics. Parallel investments in advanced paint-shop automation and differentiated finishes surfaced as OEMs seek brand-distinctive aesthetics while meeting durability standards .

Shift Toward Water-borne & Powder Systems to Meet VOC Caps

The 2025 enforcement of stricter VOC ceilings in California and forthcoming EU Green Deal measures are accelerating reformulation of solvent-borne systems. Leading body shops already report 64% penetration of water-borne basecoats, validating commercial viability. BASF's Glasurit 100 Line exemplifies high-efficiency, low-VOC products now used by more than 1,000 collision centers. Powder coatings are gaining share in wheels, under-hood parts, and EV battery casings, helped by laser-curing ovens that cut energy use by 50%. Suppliers with broad resin and pigment portfolios are fastest to convert customers, establishing early-mover advantages before regulations tighten further.

Stringent Solvent & Isocyanate Exposure Limits

Occupational Safety and Health Administration (OSHA)'s National Emphasis Program intensifies inspections of paint booths, mandating enhanced ventilation and personal protective equipment to mitigate asthma and dermatitis risks from isocyanates . Small refinishing operations face steep capital costs for compliant spray booths or must migrate to low-isocyanate chemistries that may sacrifice performance. Primer and clear-coat formulators commercialize polyurea-free variants, although adoption remains cautious while durability benchmarks are validated.

Other drivers and restraints analyzed in the detailed report include:

- Rising EV-specific Coating Demand for Battery Thermal Management

- Recovery of Collision-repair Volumes in Mature Markets

- Volatile Petrochemical-based Raw-material Pricing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, acrylics supplied 48.10% of the Automotive Coatings market demand, cementing their status owing to cost-efficiency and balanced weatherability. Polyurethane formulations, advancing at a 5.00% CAGR to 2031, fulfill premium clear-coat and flexible-substrate needs, especially on luxury Sports Utility Vehicles (SUVs) and EVs requiring superior scratch resistance. The automotive coatings market size for polyurethane systems is expected to widen notably in North American OEM lines as new aliphatic diisocyanate chemistries meet stricter yellowing tests. Epoxy resins continue niche dominance in cathodic e-coats where corrosion protection is critical, while bio-based hybrids are emerging in concept programs led by European OEMs.

The polyurethane push is amplified by longer ownership cycles driving demand for durability, though OSHA scrutiny around isocyanate handling is prompting investment in closed-mixing cells and robot-spray enclosures. Suppliers such as Covestro now offer 33% renewable-carbon polyurethanes, illustrating alignment with OEM sustainability targets. Acrylic chemists are responding with next-generation crosslinkers that improve mar resistance without raising VOC levels. Competitive advantage increasingly hinges on patent portfolios that combine mechanical robustness with low-temperature cure profiles, addressing both energy-use mandates and lightweight-substrate requirements.

Solvent-borne finishes still held 70.20% revenue in 2025, propelled by superior flow and color depth demanded on metallic and pearlescent shades. Yet the automotive coatings market is unmistakably tilting toward alternatives as global VOC ceilings narrow. Water-borne systems now dominate EU OEM base-coat lines, with Japanese OEMs such as Mazda achieving industry-low emissions of 15 g VOC/m2. Powder coatings, while presently a minority, post the highest compound growth as energy-efficient laser-cure tunnels become standard on EV component lines.

The automotive coatings market share for water-borne refinish lines has surpassed 60% in regulated regions as body shops align with environmental permits. Technological breakthroughs in resin emulsification and flash-off control have closed the performance gap with solvent-borne primers. Tier-one suppliers leverage modular resin architectures, enabling fast reformulation when each new rule tightens permissible VOCs or HAPS (hazardous air pollutants), insulating customers from mid-cycle compliance surprises.

The Automotive Coatings Market Report is Segmented by Resin Type (Polyurethane, Epoxy, Acrylic, and Others), Technology (Solvent-Borne, Water-Borne, and Powder), Coating Layer (E-Coat, Primer, Base Coat, and Clear Coat), Application (OEM and Refinish), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific accounted for 58.40% of global 2025 revenue, buoyed by China's ascent as a net exporter and leadership in EV output. Capacity additions such as Indonesia's million-ton paint plant and Vietnam's fast-growing supplier parks underpin a 6.05% regional CAGR forecast. Local OEMs collaborate with multinational formulators to localize water-borne resins while preserving appearance parity with solvent benchmarks. Government stimulus on new-energy vehicles further amplifies demand for battery-specific functional coatings.

North America, with light-vehicle builds rising 9.6% in 2024, exhibits that constrained capacity plants regularly exceed rated throughput, creating favorable pricing for coatings. Stringent United States Department of Agriculture (USDA) BioPreferred and upcoming Environmental Protection Agency (EPA) per- and polyfluoroalkyl substances (PFAS) rules spur rapid qualification of fluorine-free top coats, compelling suppliers to accelerate R&D. The automotive coatings market share of low-VOC systems is poised to expand as Canadian and Mexican operations align with United States regulations.

Europe's focus on carbon neutrality pushes OEMs toward 100% renewable-electric paint shops and solvent-capture incinerators. Anti-dumping duties on titanium dioxide elevate cost structures, but wide adoption of dry-scrubber booths and closed-loop sludge recycling partially offsets outlays. Eastern European cluster growth, including Poland and Hungary offers lower-wage assembly yet requires suppliers to establish just-in-sequence hubs for tier-one paint modules.

South America benefits from Mercosur tariff reductions that encourage automakers to allocate new SUV platforms to Brazil and Argentina, lifting OEM-paint consumption. Nonetheless, currency volatility prompts formulators to adopt US-dollar-pegged contracts. Middle East & Africa remains nascent but shows promise as Saudi Arabia's Vision 2030 sparks domestic vehicle production and related coating capacity build-outs targeting export markets.

- Akzo Nobel N.V.

- Asian Paints PPG Pvt., Ltd.

- Axalta Coating Systems, LLC

- BASF

- Beckers Group

- Cabot Corporation

- Eastman Chemical Company

- Hempel A/S

- HMG Paints Limited

- Jotun

- Kansai Nerolac Paints Limited

- KCC Corporation

- Nippon Paint Holdings Co., Ltd.

- Parker Hannifin Corp

- PPG Industries Inc.

- RPM International Inc.

- Shanghai Kinlita Chemical Co., Ltd.

- The Sherwin-Williams Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Global Vehicle Production Rebound

- 4.2.2 Shift Toward Water-borne & Powder Systems to Meet VOC Caps

- 4.2.3 Rising EV-specific Coating Demand for Battery Thermal Management

- 4.2.4 Recovery of Collision-repair Volumes in Mature Markets

- 4.2.5 OEM Adoption of Digital Color-matching & Inline Curing

- 4.3 Market Restraints

- 4.3.1 Stringent Solvent & Isocyanate Exposure Limits

- 4.3.2 Volatile Petrochemical-based Raw-material Pricing

- 4.3.3 EV Skateboard Platforms Reducing Painted Surface Area

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products & Services

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Value)

- 5.1 By Resin Type

- 5.1.1 Polyurethane

- 5.1.2 Epoxy

- 5.1.3 Acrylic

- 5.1.4 Others

- 5.2 By Technology

- 5.2.1 Solvent-borne

- 5.2.2 Water-borne

- 5.2.3 Powder

- 5.3 By Coating Layer

- 5.3.1 E-coat

- 5.3.2 Primer

- 5.3.3 Base Coat

- 5.3.4 Clear Coat

- 5.4 By Application

- 5.4.1 OEM

- 5.4.2 Refinish

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Australia and New Zealand

- 5.5.1.6 Indonesia

- 5.5.1.7 Malaysia

- 5.5.1.8 Thailand

- 5.5.1.9 Rest of ASEAN

- 5.5.1.10 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 France

- 5.5.3.3 United Kingdom

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Egypt

- 5.5.5.4 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Akzo Nobel N.V.

- 6.4.2 Asian Paints PPG Pvt., Ltd.

- 6.4.3 Axalta Coating Systems, LLC

- 6.4.4 BASF

- 6.4.5 Beckers Group

- 6.4.6 Cabot Corporation

- 6.4.7 Eastman Chemical Company

- 6.4.8 Hempel A/S

- 6.4.9 HMG Paints Limited

- 6.4.10 Jotun

- 6.4.11 Kansai Nerolac Paints Limited

- 6.4.12 KCC Corporation

- 6.4.13 Nippon Paint Holdings Co., Ltd.

- 6.4.14 Parker Hannifin Corp

- 6.4.15 PPG Industries Inc.

- 6.4.16 RPM International Inc.

- 6.4.17 Shanghai Kinlita Chemical Co., Ltd.

- 6.4.18 The Sherwin-Williams Company

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

- 7.2 Self-Cleaning Coating Technology