|

시장보고서

상품코드

1536875

핫멜트 접착제 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2024-2029년)Hot-melt Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

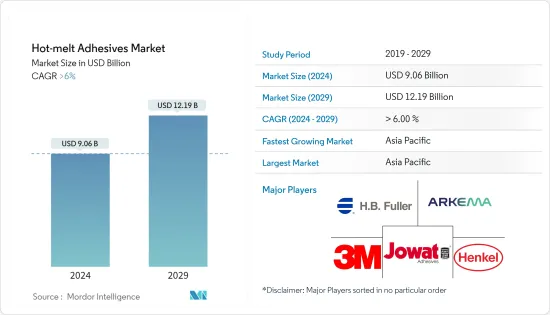

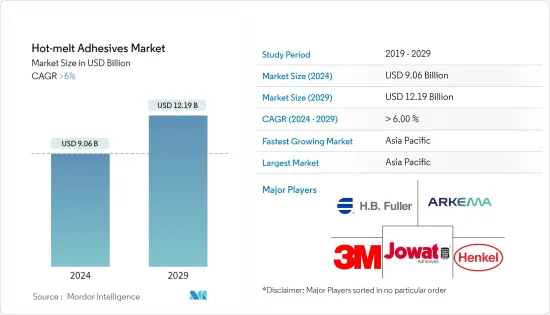

세계의 핫멜트 접착제(Hot-melt Adhesives) 시장 규모는 2024년 90억 6,000만 달러에 달할 것으로 예상되며, 2024-2029년의 예측 기간 동안 CAGR 6% 이상으로 추이하며 성장 할 것으로 예상되며, 2029년에는 121억 9,000만 달러에 달할 것으로 예측됩니다.

COVID-19는 핫멜트 접착제 시장을 방해했습니다. 자동차 제조, 건설, 부직포 위생 제품 등 핫멜트 접착제의 다양한 최종 용도 산업은 정부 규제, 소비자 수요 감소, 공급망 혼란으로 인해 생산 감속과 정지를 경험했습니다. 폐쇄 및 규제 완화로 인해 많은 산업이 운영을 재개하고 핫멜트 접착제 수요 증가로 이어지고 있습니다.

포장 산업에서 핫멜트 접착제 수요 증가, 건설 부문 수요 증가, 부직포 위생 제품의 핫멜트 접착제 채택 증가가 시장을 견인할 것으로 예상됩니다.

그러나 원재료 가격 변동이 핫멜트 접착제 시장 성장을 방해할 것으로 예상됩니다.

자동차 제조의 확대와 건설 기술 진보는 향후 기간에 기회를 제공할 것으로 예상됩니다.

인도, 일본, 중국 등 경제가 급성장하고 있기 때문에 아시아 태평양은 향후 수년간 지배적인 시장이 될 것으로 예상됩니다.

핫멜트 접착제 시장 동향

종이, 판지, 포장 분야가 시장을 독점

포장 산업은 핫멜트 접착제의 최대 소비자 중 하나입니다. 이러한 접착제는 케이스 및 카톤 씰, 트레이 성형, 라벨링, 라미네이트 등 용도로 판지, 골판지, 플라스틱 필름, 호일 등 포장 재료를 접착하는 데 널리 사용됩니다. 산업용 핫멜트 접착제의 대규모 사용은 큰 수요와 시장 우위를 견인하고 있습니다.

포장 분야에서 핫멜트 접착제 수요는 식품 소비 증가와 다양한 용도로 증가하고 있습니다. 예를 들어, 인도에서는 포장이 가장 빠르게 성장하는 산업 중 하나입니다. 이 분야는 지난 몇 년동안 꾸준한 성장을 이루고 있으며, 특히 수출 분야에서 급속한 확대가 예상되고 있습니다.

예를 들어 인도에서는 인도제지공업협회(IPMA)가 보고한 데이터에 의하면 2023년 4월-12월까지 종이 수입량은 37% 증가한 147만톤으로 되어 있습니다.

또한 독일 연방 통계국이 2023년 3월에 발표한 추계에 따르면 2022년 독일 포장 산업 수익의 약 46%는 종이 포장으로 인한 것이었습니다. 거의 34%는 플라스틱 포장입니다.

또한 독일 연방 통계국이 2023년에 발표한 추계에 따르면 독일 포장 산업은 약 350억 유로(379억 4,000만 달러) 매출을 올렸습니다. 이는 전년도 296억 유로(320억 9,000만 달러)에 비해 증가했습니다.

식품 및 음료 부문은 포장의 주요 소비자 중 하나입니다. 세계 증가 추세에 대응하기 위해 베이커리 부문이 성장하고 있으며, 이는 포장 제품의 판매를 견인하고 있습니다.

이와 같이, 상기와 같은 요인으로부터, 종이 및 판지·포장 산업의 핫멜트 접착제 수요가 성장할 것으로 예상됩니다.

아시아 태평양이 시장을 독점

아시아 태평양에서는 특히 신흥 경제 국가에서 급속한 산업화, 도시화 및 인프라 정비가 진행되고 있습니다. 이러한 성장은 건축, 포장, 자동차 및 기타 산업에서 핫멜트 접착제에 대한 수요를 촉진하고 있습니다.

아시아 태평양 정부 및 민간 부문은 교통, 유틸리티, 주택 및 상업시설 건설 등 다양한 인프라 프로젝트에 투자하고 있습니다. 핫멜트 접착제는 날개판, 바닥재 시공, 단열재 접착, 지붕 교체 등 다양한 건설 용도로 사용되고 있으며, 이 지역 건설 산업 수요를 견인하고 있습니다.

Indian Brand Equity Foundation에 따르면 인프라에 대한 설비투자는 2023-2024년 예산으로 33% 증가한 약 1,220억 달러에 달하며 GDP의 3%를 차지합니다.

또한 민간투자를 유치하기 위해 인도 정부는 특히 도로·고속도로, 공항, 비즈니스파크, 고등교육·기능개발부문에 대해 많은 방법을 개발하고 있습니다. 비공개 회사와 벤처 캐피탈은 2023년 5월까지 인도 기업에 35억 달러를 투자하여 71건의 거래를 했습니다.

중국은 2008년 이후 종이 포장재와 판지 생산량이 가장 많은 나라가 되고 있습니다. 중국지업협회의 조사에 따르면 2023년 중국 종이 및 판지 제조 기업의 총수는 2,500개사, 전국 종이 및 판지 생산량은 1억 2,965만 톤으로 전년대비 4.35% 증가했습니다.

이런 식으로 위의 요인은 예측 기간 동안이 지역의 핫멜트 접착제 시장을 견인할 것으로 예상됩니다.

핫멜트 접착제 산업 개요

세계의 핫멜트 접착제 시장은 세분화되어 있습니다. 이 시장의 주요 기업에는 3M, Jowat SE, Henkel Corporation, Arkema, HB Fuller 등이 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 성장 촉진요인

- 포장 산업에서 수요 증가

- 건설 산업에서 수요 증가

- 기타 촉진요인

- 억제요인

- 원재료 가격 변동

- 산업 밸류체인 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 세분화(시장 규모 : 금액)

- 수지 유형

- 에틸렌 비닐 아세테이트

- 스티렌계 블록 공중합체

- 열가소성 폴리우레탄

- 기타 수지 유형

- 최종 사용자 산업

- 건축 및 건설

- 종이·판지·포장

- 목공·건구

- 자동차·운수

- 양말·가죽

- 헬스케어

- 전기 및 전자 기기

- 기타 최종 사용자 산업

- 지역

- 아시아 태평양

- 중국

- 인도

- 일본

- 한국

- 말레이시아

- 태국

- 인도네시아

- 베트남

- ASEAN 국가

- 기타 아시아 태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 터키

- 스페인

- 러시아

- 북유럽

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 콜롬비아

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카공화국

- 나이지리아

- 이집트

- 카타르

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

- 아시아 태평양

제6장 경쟁 구도

- M&A, 합작사업, 제휴, 협정

- 시장 점유율(%)**/랭킹 분석

- 주요 기업의 전략

- 기업 프로파일

- 3M

- Alfa International

- Arkema

- Ashland

- AVERY DENNISON CORPORATION

- Beardow Adams

- Dow

- DRYTAC

- Franklin International

- HB Fuller Company

- Henkel Corporation

- Hexcel Corporation

- Huntsman International LLC

- Jowat SE

- Mactac

- Master Bond Inc.

- Paramelt RMC BV

- Pidilite Industries Limited

- Sika AG

제7장 시장 기회 및 향후 동향

- 자동차 제조 확대

- 건설기술 진보

The Hot-melt Adhesives Market size is estimated at USD 9.06 billion in 2024, and is expected to reach USD 12.19 billion by 2029, growing at a CAGR of greater than 6% during the forecast period (2024-2029).

COVID-19 hampered the hot melt adhesive market. Various end-use industries for hot melt adhesives, such as automotive manufacturing, construction, and nonwoven hygiene products, experienced slowdowns or shutdowns in production due to government-mandated restrictions, reduced consumer demand, and supply chain disruptions. With the easing of lockdown measures and restrictions, many industries have resumed operations, leading to increased demand for hot melt adhesives.

* Increasing demand for hot melt adhesives from the packaging industry, rising demand from the construction sector, and increased adoption of hot melt adhesives in nonwoven hygiene products are expected to drive the market.

* However, volatility in raw material prices is expected to hamper the growth of the hot melt adhesive market.

* Expansion in automotive manufacturing and the advancements in construction technologies are expected to provide opportunities in the upcoming period.

* Due to rapidly growing economies like India, Japan, and China, Asia-Pacific is expected to emerge as a dominant market in the coming years.

Hot Melt Adhesives Market Trends

Paper, Board, and Packaging Segment to Dominate the Market

* The packaging industry is one of the largest consumers of hot melt adhesives. These adhesives are widely used for bonding packaging materials such as paperboard, corrugated cardboard, plastic films, and foils in applications such as case and carton sealing, tray forming, labeling, and lamination. The industry's large-scale use of hot melt adhesives drives significant demand and market dominance.

* The demand for hot melt adhesives in the packaging sector is increasing due to increased food consumption and various applications. For instance, in India, packaging is one of the fastest-growing industries. The sector has witnessed steady growth over the past several years and is expected to expand rapidly, particularly in the export sector.

* For instance, in India, paper imports rose by 37% to 1.47 million tonnes from April to December 2023, according to data reported by The Indian Paper Manufacturers Association (IPMA).

* Further, according to the estimate published by the Statistisches Bundesamt in March 2023, in 2022, around 46 percent of the packaging industry revenue in Germany was generated by paper packaging. Almost 34 percent was made up of plastic packaging.

* Moreover, according to the estimate published by the Statistisches Bundesamt in 2023, the German packaging industry generated around EUR 35 billion (USD 37.94 billion) in revenue. This was an increase compared to the previous year at EUR 29.6 billion (USD 32.09 billion).

* The food and beverage sector is one of the major consumers of packaging. In order to cope with the increasing trend around the world, the bakery sector is growing, and this is driving sales of packaging products.

* Thus, the factors mentioned above are expected to grow the demand for hot melt adhesives from the paper, board, and packaging industries.

Asia-Pacific to Dominate the Market

* Asia-Pacific is experiencing rapid industrialization, urbanization, and infrastructure development, particularly in emerging economies in the region. This growth fuels the demand for hot melt adhesives in construction, packaging, automotive, and other industries, as these adhesives are essential for bonding materials and components in manufacturing and construction processes.

* Governments and private sectors in the Asia Pacific are investing in various infrastructure projects such as transportation, utilities, and residential and commercial construction. Hot melt adhesives are used in various construction applications, including paneling, flooring installation, insulation bonding, and roofing, driving the demand for these adhesives in the region's construction industry.

* According to the Indian Brand Equity Foundation, the capital investment in infrastructure is set to increase by 33%, amounting to about USD 122 billion, for the budget of 2023-24, and this accounts for 3% of GDP.

* Further, in order to attract private investment, the government of India has developed a number of ways, particularly for roads and highways, airports, business parks, and higher education and skills development sectors. Private Equity and Venture Capital Firms invested USD 3.5 billion in Indian companies between May 2023 with 71 deals.

* China has been the most extensive paper packaging and paperboard producer since 2008. According to a survey conducted by the China Paper Association, in 2023, the total number of paper and paperboard manufacturing enterprises in China stood at 2,500, with a nationwide paper and paperboard output of 129.65 Million tons, a 4.35% increase from the previous year.

* Thus, the above factors are expected to drive the hot-melt adhesives market in the region during the forecast period.

Hot-melt Adhesives Industry Overview

The global hot-melt adhesives market is fragmented in nature. Some of the major players in the market (not in any particular order) include 3M, Jowat SE, Henkel Corporation, Arkema, and H.B. Fuller, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand from Packaging Industry

- 4.1.2 Rising Demand from Construction Sector

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Volatility in Raw Material Prices

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size by Value)

- 5.1 Resin Type

- 5.1.1 Ethylene Vinyl Acetate

- 5.1.2 Styrenic Block Co-polymers

- 5.1.3 Thermoplastic Polyurethane

- 5.1.4 Other Resin Types (Polyolefin, polyamide)

- 5.2 End-user Industry

- 5.2.1 Building and Construction

- 5.2.2 Paper, Board, and Packaging

- 5.2.3 Woodworking and Joinery

- 5.2.4 Automotive and Transportation

- 5.2.5 Footwear and Leather

- 5.2.6 Healthcare

- 5.2.7 Electrical and Electronic Appliances

- 5.2.8 Other End-user Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 ASEAN Countries

- 5.3.1.10 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Turkey

- 5.3.3.6 Spain

- 5.3.3.7 Russia

- 5.3.3.8 NORDIC

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Nigeria

- 5.3.5.4 Egypt

- 5.3.5.5 Qatar

- 5.3.5.6 UAE

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Alfa International

- 6.4.3 Arkema

- 6.4.4 Ashland

- 6.4.5 AVERY DENNISON CORPORATION

- 6.4.6 Beardow Adams

- 6.4.7 Dow

- 6.4.8 DRYTAC

- 6.4.9 Franklin International

- 6.4.10 H.B. Fuller Company

- 6.4.11 Henkel Corporation

- 6.4.12 Hexcel Corporation

- 6.4.13 Huntsman International LLC

- 6.4.14 Jowat SE

- 6.4.15 Mactac

- 6.4.16 Master Bond Inc.

- 6.4.17 Paramelt RMC B.V.

- 6.4.18 Pidilite Industries Limited

- 6.4.19 Sika AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Expansion in Automotive Manufacturing

- 7.2 Advancements in Construction Technologies