|

시장보고서

상품코드

1939665

소형 풍력 터빈 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Small Wind Turbine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

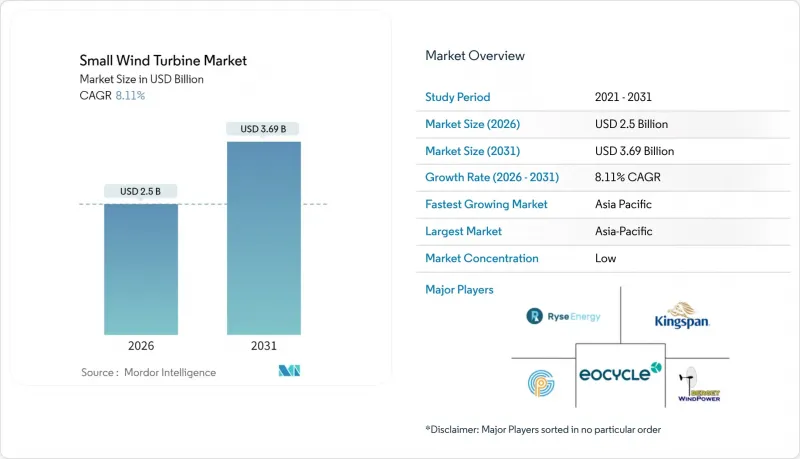

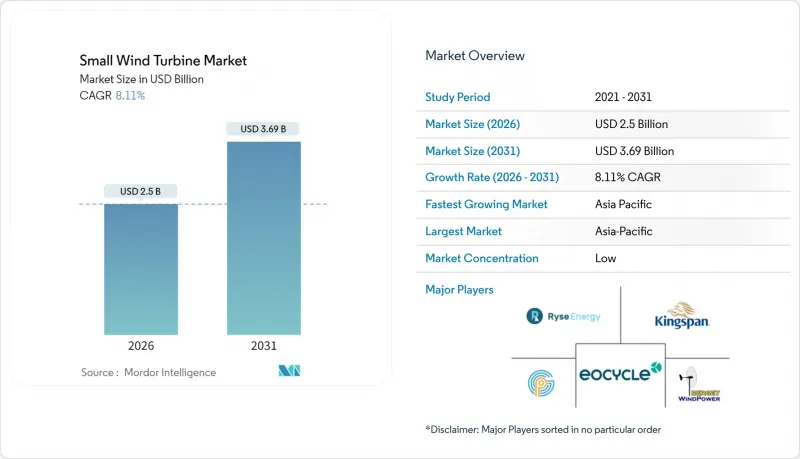

소형 풍력 터빈 시장은 2025년에 23억 1,000만 달러로 평가되며, 2026년 25억 달러에서 2031년까지 36억 9,000만 달러에 달할 것으로 예측됩니다. 예측 기간(2026-2031년) 동안 CAGR은 8.11%로 예상됩니다.

정책적 인센티브, 수직축 기술 발전, 통신, 농업, 분산형 에너지 시스템에서의 활용 확대가 성장의 원동력이 되고 있습니다. 북미, 유럽 연합, 아시아에서 공공 자금 프로그램이 도입에 박차를 가하고 있으며, 머신러닝을 활용한 터빈 최적화를 통해 평생 에너지 비용을 절감하고 신뢰성을 향상시키고 있습니다. 기업의 전력구매계약(PPA)은 계통연계 프로젝트에 대한 수요를 확대하고, 풍력과 태양광을 결합한 하이브리드 시스템은 풍력 자원이 변동하는 지역에서 대상 시장을 확대하고 있습니다. 10kW 미만 부문에서는 지붕형 태양광과의 비용 경쟁이 여전히 제약요인으로 작용하고 있지만, 효율 향상과 새로운 설치 규제로 인해 그 격차가 줄어들고 있습니다.

세계 소형 풍력 터빈 시장 동향과 전망

카리브해 섬의 급속한 원격지 전기화

도서 지역의 전력 사업자들은 디젤 발전 시스템을 소형 풍력 터빈을 포함한 하이브리드 재생에너지 마이크로그리드로 대체하고 있습니다. 정부 및 다자간 금융기관은 프로젝트 초기비용을 절감하고 개발사업자의 진입을 촉진하는 우대융자를 배정하고 있습니다. 내식성 코팅과 모듈식 물류 패키지를 제공하는 터빈 공급업체는 이러한 시장에서 경쟁 우위를 점하고 있습니다. 사이트당 평균 설치 용량은 50kW 미만이며, 0-20kW의 제품 라인과 일치합니다. 안정적인 무역풍으로 가동률이 35% 이상 유지되며, 태양광 단독 설계에 비해 투자 회수 기간이 단축됩니다. 도서지역 전력화 프로그램에서는 높은 가동률을 평가하는 성과 연동형 요금제를 채택하고 있으며, 신형 터빈에 통합된 디지털 모니터링 플랫폼의 가치가 더욱 높아지고 있습니다.

미국 농무부(USDA) 농촌 에너지 보조금으로 5kW 미만 터빈 수요 급증

2025년도에 배정된 1억 8,000만 달러 규모의 '미국 농촌 에너지 프로그램'은 농장 및 농촌 지역 중소기업을 위한 마이크로 풍력 시스템을 우선적으로 지원할 예정입니다. 보조금은 자본 비용의 최대 50%를 지원하며, 평균 풍속 6m/s 이상의 지역에서는 6년 미만의 회수 기간을 허용합니다. 국립재생에너지연구원의 경쟁력 강화 프로젝트는 시제품 인증에 필요한 자금을 지원하고, 제3자 대출의 길을 열어줌으로써 기존 은행 대출의 장벽을 해소합니다. 400개 이상의 농장을 대상으로 2027년까지 누적 25MW 규모의 마이크로급 설비 증설을 추진합니다. 풍력 터빈과 헛간 지붕의 태양전지판을 결합하여 생산자는 낮의 피크 부하와 저녁의 관개 수요를 상쇄할 수 있습니다. 이 프로그램을 통해 UL 6141 인증을 획득한 제조업체는 연방정부 조달에서 우선권을 부여받게 됩니다.

유럽 도시 지역의 높이 규제

많은 역사지구에서는 지자체의 높이 제한으로 인해 터빈 허브의 높이가 10m 이하로 제한되어 발전량이 억제되고 있습니다. 예외허가 신청 시에는 그림자 드리움이나 경관 평가가 요구되는 경우가 많아 사업기간이 연장되는 경우가 많습니다. 소음 측정 규정은 실측 데이터가 아닌 모델 데이터에 의존하고 있으며, 설계 비용을 증가시키고 있습니다. 관할구역이 분절되어 있으며, 같은 프로젝트라도 인접한 지자체 간 서로 다른 규정이 적용되어 개발업자의 도시전개에 걸림돌로 작용하고 있습니다. EU 풍력발전 패키지의 지침은 조화를 이루고 있지만, 지역 문화유산 보호 단체는 거부권을 가지고 있습니다. 이에 반해, 공급업체는 난간 하부에 맞는 짧은 기둥 수직축 설계로 대응하고 있지만, 스위핑 면적 감소로 인해 연간 발전량이 감소합니다.

부문 분석

수평축형은 공기역학적 특성과 성숙한 공급망으로 인해 2025년 매출의 67.40%를 유지했습니다. 이 부문은 대규모 풍력발전소 갱신 및 농촌지역 가정용 풍력발전기 교체를 주도하고 있습니다. 제조업체는 미국 농무부(USDA)와 인도의 통신 입찰 사양을 충족하기 위해 2-20kW 모델을 표준화하여 규모의 경제를 활용하고 있습니다. 소형 풍력터빈 시장에서 수직축 유닛은 낮은 수준에서 빠르게 성장하여 13.4%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측되며, 수평축 유닛을 능가할 것으로 전망됩니다. 수직축 터빈은 지붕이나 가로등 기둥 근처의 난기류 환경에서 진가를 발휘하며, 전방향 블레이드가 다방향에서 불어오는 돌풍을 포착합니다. 회전마다 피치를 조정하는 유전적 학습 알고리즘으로 출력 계수가 최대 0.45까지 향상되어 베츠 한계 기준값에 근접하고 있습니다. 움직이는 부품의 감소로 지상 설치형 기어박스를 실현하여 유지보수 작업 차량의 출동 횟수를 30% 감소시킴. 이를 통해 상업용 차량 도입이 촉진되고 있습니다.

수직축 터빈 제조업체는 파사드 기술자와 협력하여 커튼월에 내장하는 것을 실현했습니다. EU의 혁신 기술 도입 의무를 충족합니다. 사보니우스와 다리우스의 하이브리드 방식은 역회전 로터로 토크 리플을 최소화하여 5m 거리에서 소음을 35dB 이내로 억제합니다. 도쿄대학교의 현지 시험에서 태풍급 돌풍에도 15년의 베어링 수명을 확인하여 내구성에 대한 우려를 불식시켰습니다. 개발업체는 서비스와 재활용 의무를 결합한 임대 계약을 구축하여 중국과 EU의 순환 경제 규칙을 충족합니다. 이러한 접근 방식은 수직축 터빈을 파괴적이지 않고 보완적인 존재로 인식하고, 혼합 배열을 통해 현장 에너지 출력을 평활화할 수 있습니다.

마이크로급(0-5kW) 시스템은 농장, 산장, 도로변 센서에 대한 보조금 설치로 인해 2025년 소형 풍력 터빈 시장의 45.30%를 차지할 것으로 예측됩니다. 전자부품의 상품화로 인해 평균 판매가격은 전년 대비 6% 하락했으나, 설치 후 서비스 매출은 증가했습니다. 중형 21-100kW 유닛은 2031년까지 연평균 복합 성장률(CAGR) 10.83%로 확대될 것이며, 통신 타워, 산업단지, 데이터센터 캠퍼스에 공급될 것입니다. 개발업체들은 고장시 연속운전 기능과 무효전력 지원이 통합된 IEC 61400-2 인증 모델을 선호하고 있으며, 이를 통해 별도의 컨버터 없이 계통연계가 가능합니다. 60kW 규모에서는 kW당 단가가 2,300달러 이하로 내려가면서 지붕형 태양광발전+축전 시스템과의 가격 차이가 줄어들고 있습니다.

6-20kW급 소형 풍력터빈 시장은 전력요금에 수요 요금이 포함된 도시 근교 상업지역에서 꾸준히 확대되고 있습니다. 냉장 부하가 높은 농가는 저녁 피크 전력을 상쇄하기 위해 15kW 터빈을 선택했습니다. 설치업체의 축적된 기술력으로 프로젝트 리드타임이 단축되어 도입 실적 확대에 기여하고 있습니다. 중견 공급업체는 97%의 기술 가동률을 보장하는 연장 보증을 패키지로 제공하고, 그린뱅크의 저비용 융자를 받을 수 있도록 하고 있습니다. 상호 운용 가능한 SCADA 시스템을 통해 풍력발전 출력을 현지 축전지 제어에 연동하여 자가 소비를 최적화하고 계통 연계의 출력 억제를 방지합니다.

소형 풍력터빈 시장 보고서는 축 유형(수평축 풍력터빈과 수직축 풍력터빈), 정격용량(0-5kW, 6-20kW, 21-100kW), 연결방식(Off-grid, 온그리드, 하이브리드), 설치장소(옥상/건물일체형, 독립형 타워), 용도(주거용, 상업용, 기타), 지역(북미, 유럽, 아시아태평양, 중동, 아프리카, 유럽, 중동 및 아프리카, 기타) 기타), 지역(북미, 유럽, 아시아태평양, 남미, 기타)으로 분류되어 있습니다.

지역별 분석

아시아태평양은 2025년 47.30%의 점유율로 소형 풍력 터빈 시장을 주도할 것이며, 중국의 산업 탈탄소화와 인도의 통신 전기화를 배경으로 CAGR 9.84%로 확대될 것으로 예측됩니다. 중국에서는 2030년까지 공장의 40%를 친환경 공장으로 인증하는 정책을 제시하고 있으며, 경제특구에서는 옥상이나 안마당에 터빈 설치를 의무화하고 있습니다. 또한 장쑤성의 재활용 기준은 순환형 공급망을 촉진하고 있습니다. 인도의 타워 운영사는 백업 전원으로 재생에너지를 채택하고 있으며, 하이브리드 입찰에서는 태양광발전 및 리튬 배터리 팩과 함께 5kW 마이크로터빈을 도입하도록 지정되어 있습니다. 일본은 엄격한 소음 규제를 유지하면서 철도 연선 부근에서 수직축 터빈의 실증 시험을 지원하고 있습니다. 아세안 섬나라들은 지역 마이크로그리드를 도입하고 있으며, 베트남 제조업체는 10kW급 터빈을 지역 어선단에 수출하고 있습니다.

유럽은 성숙한 시장으로서 명확한 규제가 점진적인 성장을 지원하고 있습니다. 재생에너지 지침 개정으로 50kW 미만 프로젝트의 허가 지연이 해소되어 도시지역에서의 도입이 촉진되고 있습니다. 독일에서는 특정 주에서 10m 미만의 터빈을 계획 승인 대상에서 제외하여 간접비용을 25% 절감했습니다. 북유럽의 데이터센터용 전력구매계약(PPA)이 탄탄한 계통연계 파이프라인을 지원하고 있습니다. 노스크 하이드로의 29년 235MW 풍력 PPA는 장기수용계약에 대한 신뢰를 보여주는 좋은 예입니다. 덴마크의 39dB의 엄격한 소음 규제는 전 세계로 수출되는 제품의 음향 설계에 영향을 미치고 있습니다. 영국은 섬 지역의 육상 풍력발전 확대를 지원하고, 지역 이익 분배를 위한 마이크로터빈 도입도 포함하고 있습니다.

북미의 정책적 환경이 수요를 활성화합니다. 미국 농무부(USDA)의 1억 8,000만 달러의 보조금 풀은 농장 도입을 가속화하고, NREL의 3억 2,000만 달러의 경쟁력 기금은 인증 과정을 촉진합니다. 캐나다에서 노덱스의 대규모 풍력터빈 247MW 수주 급증은 부품 현지화를 촉진하고, 운송망 공유를 통해 소형 풍력 공급업체에도 이익을 가져다 줄 것입니다. 다만, 지붕형 태양광발전의 가격 우위 때문에 주택 도입이 늦어지고 있습니다. 미국 등에서는 소형풍력 전용 고정가격임베디드제도(FIT)를 시범 도입하고, 캘리포니아 주에서는 여러 기술 시스템을 평가하는 마이크로그리드 요금을 시범 운영 중입니다. 멕시코의 농촌 전기화 기관은 오프 그리드 진료소를 위한 1.5kW 풍력발전기를 포함한 하이브리드 키트 입찰을 재개했습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 개요

제4장 시장 구도

- 시장 개요

- 시장 성장 촉진요인

- 카리브해 외딴 섬들의 신속한 전력 공급

- 미국 농무부(USDA)의 "미국 농촌 에너지 지원" 보조금으로 인한 5kW 미만 터빈 수요 급증

- 중국의 "탄소 제로 산업 단지", 현장 재생 에너지 의무화

- EU 옥상 재생에너지 지침, 건물 일체형 풍력 발전 촉진

- 인도 및 아세안의 통신탑 하이브리드화 계획

- 북유럽 데이터센터 클러스터에서 마이크로 풍력 발전을 위한 기업 PPA 증가

- 시장 성장 억제요인

- 유럽 도시 높이 기반 구역 설정 제한

- 일본의 음향 방출 기준 강화

- 북미 높은 LCOE와 옥상형 태양광 발전 비교(10kW 미만)

- 아프리카 생태계: 장기적인 O&M 부재로 인한 대출 가능성의 격차

- 산업가치/공급망 분석

- 규제와 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 축 유형별

- 수평축 풍력 터빈(HAWT)

- 수직축 풍력 터빈(VAWT)

- 용량별(kW)

- 0-5kW(마이크로)

- 6-20kW (소형)

- 21-100kW (중형)

- 연결성별

- 오프 그리드

- 온 그리드

- 하이브리드(풍력 + 배터리/태양광)

- 설치 위치별

- 옥상/건물 일체형

- 독립형 타워(지면 설치형)

- 용도별

- 주거용

- 상업용 (소매점, 사무실, 호텔)

- 산업 및 창고

- 농업 및 양식업

- 통신탑 및 원격 모니터링 사이트

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- 아랍에미리트

- 사우디아라비아

- 남아프리카공화국

- 이집트

- 기타 중동

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Aeolos Wind Energy Ltd

- Bergey Windpower Co.

- City Windmills Holdings PLC

- D-Link Corporation

- Wind Energy Solutions BV

- SD Wind Energy Ltd

- UNITRON Energy Systems Pvt Ltd

- Northern Power Systems Inc.

- Shanghai Ghrepower Green Energy Co. Ltd

- TUGE Energia OU

- Ryse Energy

- Kingspan Group Plc (Wind Division)

- Eocycle Technologies Inc.

- XZERES Wind Corp.

- Fortis Wind Energy BV

- HY Energy Co. Ltd

- Endurance Wind Power Inc.

- Kliux Energies International

- Pika Energy (Generac)

- Envergate Energy AG

- Suzlon Energy Ltd

제7장 시장 기회와 향후 전망

KSA 26.03.06The Small Wind Turbine Market was valued at USD 2.31 billion in 2025 and estimated to grow from USD 2.5 billion in 2026 to reach USD 3.69 billion by 2031, at a CAGR of 8.11% during the forecast period (2026-2031).

Growth is driven by policy incentives, vertical-axis technology advances, and rising use in telecom, agricultural, and distributed energy systems. Public funding programs in North America, the European Union, and Asia accelerate deployments, while machine-learning-enabled turbine optimization reduces lifetime energy costs and improves reliability. Corporate power purchase agreements expand demand for on-grid projects, and hybrid wind-solar systems extend the addressable market in regions with variable wind resources. Cost rivalry with rooftop solar remains a restraint in the sub-10 kW segment, but efficiency gains and new siting rules narrow the gap.

Global Small Wind Turbine Market Trends and Insights

Rapid Electrification of Remote Islands across the Caribbean

Remote island utilities are replacing diesel systems with hybrid renewable microgrids, including small wind turbines. Governments and multilateral lenders have earmarked concessional finance that reduces upfront project costs and broadens developer participation. Turbine suppliers that offer corrosion-resistant coatings and modular logistics packages gain a competitive advantage in these markets. The average installed capacity per site remains below 50 kW, aligning with 0-20 kW product lines. Steady trade winds support capacity factors above 35%, improving payback periods relative to solar-only designs. Island electrification programs adopt performance-based tariffs that reward high availability, reinforcing the value of digital monitoring platforms integrated into new turbine models.

Sub-5 kW Turbine Demand Surge from USDA Rural Energy Grants

The USD 180 million Rural Energy for America Program allocation in 2025 prioritizes micro wind systems for farms and rural small businesses. Grants cover up to 50% of capital costs, enabling paybacks under six years in regions with mean wind speeds above 6 m/s. The National Renewable Energy Laboratory's Competitiveness Improvement Project funds prototype certification that unlocks third-party financing, addressing historical bankability gaps. More than 400 farms are targeted, driving an incremental 25 MW of cumulative micro-class installations by 2027. Coupling turbines with barn-roof solar arrays allows producers to offset peak daytime loads and evening irrigation demand. Manufacturers that complete UL 6141 certification under the program qualify for preference in federal procurement.

Height-Based Zoning Restrictions in Urban Europe

Municipal height limits constrain turbine hub height to 10 m or less in many historic districts, curbing energy yield. Variance requests often require shadow-flicker and visual assessments that lengthen project timelines. Noise measurement rules rely on modeled rather than empirical data, adding engineering costs. Fragmented jurisdiction means identical projects face divergent rules between adjacent municipalities, discouraging developers from citywide rollouts. EU Wind Power Package guidance seeks harmonization, but local cultural heritage bodies retain veto power. Suppliers respond with stub-mast vertical-axis designs that fit below parapets, though lower swept area reduces annual output.

Other drivers and restraints analyzed in the detailed report include:

- China's Zero-Carbon Industrial Parks Mandating On-Site Renewables

- EU Rooftop-Renewables Directive Boosting Building-Integrated Wind

- High Levelized Cost of Energy versus Rooftop Solar in Sub-10 kW Segment

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Horizontal configurations retained 67.40% of 2025 revenue on proven aerodynamics and supply chain maturity. The segment dominated large-farm repowering and rural household replacements. Manufacturers standardize 2-20 kW models to meet USDA and Indian telecom bid specifications, leveraging volume economies. The small wind turbine market size for vertical axis units grew quickly from a lower base and is forecast to post 13.4% CAGR, outpacing horizontal units. Vertical turbines thrive in disrupted wind flows near rooftops and street-level poles, where omnidirectional blades capture multidirectional gusts. Genetic learning algorithms that modulate pitch through each rotation improve power coefficients by up to 0.45, close to Betz-limit benchmarks. Reduced moving parts allow ground-level gearboxes, cutting maintenance truck rolls by 30% and encouraging commercial fleet adopters.

Vertical axis suppliers partner with facade engineers to embed turbines into curtain walls, meeting EU innovative-technology quotas. Savonius and Darrieus hybrids with contra-rotating rotors minimize torque ripple, lowering the acoustic signature to within 35 dB at a 5 m distance. University of Tokyo field tests verify 15-year bearing life even under typhoon gusts, addressing durability perceptions. Developers structure leasing deals that bundle services and recycle obligations, satisfying circular economy rules in China and the EU. The narrative positions vertical turbines as complementary rather than disruptive, allowing mixed arrays that smooth site energy output.

Micro class 0-5 kW systems delivered 45.30% of the small wind turbine market share in 2025, supported by grant-funded installations on farms, cabins, and roadside sensors. Average selling price fell 6% year-on-year as electronics commoditized, yet post-installation service revenues rose. Medium 21-100 kW units expand at 10.83% CAGR through 2031, serving telecom towers, industrial parks, and data-center campuses. Developers favor IEC 61400-2-certified models that integrate fault ride-through and reactive power support, enabling grid connection without separate converters. At 60 kW size, unit cost per kW drops below USD 2,300, closing the gap to rooftop solar plus storage stacks.

The small wind turbine market size for 6-20 kW equipment grows steadily in peri-urban business estates where grid tariffs include demand charges. Farmers with high refrigeration loads choose 15 kW turbines to offset evening peaks. Historical adoption benefits from accumulated installer skillsets that shorten project lead times. Medium-class suppliers bundle extended warranties that guarantee 97% technical availability, unlocking low-cost debt from green banks. Interoperable SCADA links wind output to onsite battery dispatch, optimizing self-consumption and avoiding interconnection curtailments.

The Small Wind Turbine Market Report is Segmented by Axis Type (Horizontal Axis Wind Turbines and Vertical Axis Wind Turbines), Capacity Rating (0 To 5 KW, 6 To 20 KW, and 21-100 KW), Connectivity (Off-Grid, On-Grid, and Hybrid), Installation Location (Rooftop/Building-Integrated and Freestanding Tower), Application (Residential, Commercial, and More), and Geography (North America, Europe, Asia-Pacific, South America, and More).

Geography Analysis

Asia-Pacific dominated the small wind turbine market with a 47.30% share in 2025 and is growing at a 9.84% CAGR on the back of Chinese industrial decarbonization and Indian telecom electrification. China's mandate for 40% certified green factory output by 2030 compels economic zones to install rooftop and courtyard turbines, while Jiangsu's recycling standards promote circular supply chains. India's tower operators commit to renewable energy for backup power, and hybrid tenders specify 5 kW microturbines alongside PV and lithium packs. Japan maintains stringent acoustic rules yet supports vertical-axis demonstrations near rail corridors. ASEAN island states deploy community microgrids, and Vietnamese manufacturers export 10 kW turbines to regional fishing fleets.

Europe remains a mature base where regulatory clarity supports incremental growth. The Renewables Directive revision cuts permitting delays for projects below 50 kW, boosting urban adoption. Germany exempts sub-10 m turbines from planning approval in selected Lander, cutting soft costs by 25%. Nordic data-center PPAs underpin a robust on-grid pipeline; Norsk Hydro's 29-year 235 MW wind PPA exemplifies confidence in long-dated offtake. Denmark's stringent 39 dB noise cap influences product acoustics exported worldwide. The United Kingdom supports island onshore wind expansions, including micro-turbines for community benefit shares.

North America's policy landscape rejuvenates demand. The USDA's USD 180 million grant pool accelerates farm deployments, and NREL's USD 3.2 million competitiveness fund advances certification pathways. Canada's 247 MW order boom for Nordex utility-scale turbines raises component localization that benefits small wind suppliers through shared transport links. However, residential adoption lags due to rooftop solar price advantage. States such as New York pilot feed-in tariffs specific to small wind, while California trials microgrid tariffs that reward multi-technology systems. Mexico's rural electrification agency reopens tenders for a hybrid kit, including 1.5 kW wind units for off-grid clinics.

- Aeolos Wind Energy Ltd

- Bergey Windpower Co.

- City Windmills Holdings PLC

- Wind Energy Solutions BV

- SD Wind Energy Ltd

- UNITRON Energy Systems Pvt Ltd

- Northern Power Systems Inc.

- Shanghai Ghrepower Green Energy Co. Ltd

- TUGE Energia OU

- Ryse Energy

- Kingspan Group Plc (Wind Division)

- Eocycle Technologies Inc.

- XZERES Wind Corp.

- Fortis Wind Energy BV

- HY Energy Co. Ltd

- Endurance Wind Power Inc.

- Kliux Energies International

- Pika Energy (Generac)

- Envergate Energy AG

- Suzlon Energy Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Electrification of Remote Islands across the Caribbean

- 4.2.2 Sub-5 kW Turbine Demand Surge from U.S. USDA "Rural Energy for America" Grants

- 4.2.3 China's "Zero-Carbon Industrial Parks" Mandating On-site Renewables

- 4.2.4 EU Rooftop-Renewables Directive Boosting Building-Integrated Wind

- 4.2.5 Telecom Tower Hybridization Agenda in India & ASEAN

- 4.2.6 Increasing Corporate PPAs for Micro-Wind in Nordics' Data-Center Cluster

- 4.3 Market Restraints

- 4.3.1 Height-Based Zoning Restrictions in Urban Europe

- 4.3.2 Acoustic-Emission Standards Tightening in Japan

- 4.3.3 High LCOE versus Rooftop PV in North America <10 kW segment

- 4.3.4 Bankability Gaps due to Absence of Long-Term O&M Ecosystem in Africa

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Investment Analysis

5 Market Size & Growth Forecasts

- 5.1 By Axis Type

- 5.1.1 Horizontal Axis Wind Turbines (HAWT) (Upwind, and Downwind)

- 5.1.2 Vertical Axis Wind Turbines (VAWT) (Savonius, Darrieus and Giromill)

- 5.2 By Capacity Rating (kW)

- 5.2.1 0 to 5 kW (Micro)

- 5.2.2 6 to 20 kW (Small)

- 5.2.3 21 to 100 kW (Medium)

- 5.3 By Connectivity

- 5.3.1 Off-Grid

- 5.3.2 On-Grid

- 5.3.3 Hybrid (Wind + Battery/PV)

- 5.4 By Installation Location

- 5.4.1 Rooftop/Building-Integrated

- 5.4.2 Freestanding Tower (Ground-Mounted)

- 5.5 By Application

- 5.5.1 Residential

- 5.5.2 Commercial (Retail, Offices, Hotels)

- 5.5.3 Industrial and Warehousing

- 5.5.4 Agricultural and Aquaculture

- 5.5.5 Telecom Towers and Remote Monitoring Sites

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 Germany

- 5.6.2.3 France

- 5.6.2.4 Spain

- 5.6.2.5 Nordic Countries

- 5.6.2.6 Russia

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 ASEAN Countries

- 5.6.3.6 Australia

- 5.6.3.7 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Colombia

- 5.6.4.4 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 South Africa

- 5.6.5.4 Egypt

- 5.6.5.5 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Strategic Moves (M&A, Partnerships, PPAs)

- 6.2 Market Share Analysis (Market Rank/Share for key companies)

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.3.1 Aeolos Wind Energy Ltd

- 6.3.2 Bergey Windpower Co.

- 6.3.3 City Windmills Holdings PLC

- 6.3.4 Wind Energy Solutions BV

- 6.3.5 SD Wind Energy Ltd

- 6.3.6 UNITRON Energy Systems Pvt Ltd

- 6.3.7 Northern Power Systems Inc.

- 6.3.8 Shanghai Ghrepower Green Energy Co. Ltd

- 6.3.9 TUGE Energia OU

- 6.3.10 Ryse Energy

- 6.3.11 Kingspan Group Plc (Wind Division)

- 6.3.12 Eocycle Technologies Inc.

- 6.3.13 XZERES Wind Corp.

- 6.3.14 Fortis Wind Energy BV

- 6.3.15 HY Energy Co. Ltd

- 6.3.16 Endurance Wind Power Inc.

- 6.3.17 Kliux Energies International

- 6.3.18 Pika Energy (Generac)

- 6.3.19 Envergate Energy AG

- 6.3.20 Suzlon Energy Ltd

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment