|

시장보고서

상품코드

1641987

의료기기 보안 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Medical Device Security - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

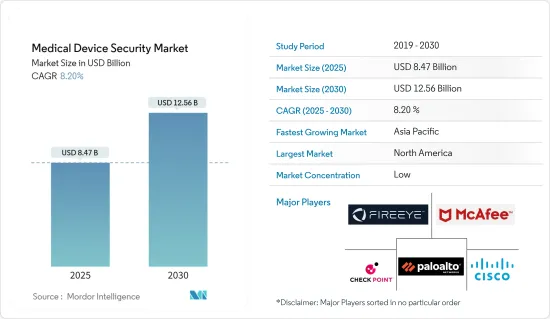

의료기기 보안 시장 규모는 2025년에 84억 7,000만 달러로 추정되고, 2030년에는 125억 6,000만 달러에 이를 것으로 예측되며, 시장 추정 및 예측 기간(2025-2030년)의 CAGR은 8.2%로 전망됩니다.

의료 산업은 IoT 기술의 변혁적 성질과 컴퓨팅 능력, 무선 기술, 빅 데이터 등의 데이터 분석 기술의 진보에 도움을 받아 지난 몇 년동안 큰 변화를 확인해 왔습니다. 빅데이터는 현재 단백질체학, 유전체학, 약물유전체학를 포함한 복잡한 이종 의료 데이터를 분석하기 위해 의료 시설 및 의료 연구 부문에서 전 세계적으로 도입되고 있습니다.

주요 하이라이트

- 의료 종사자가 예측, 예방, 개인화, 참여형 의약품 제공에 대한 인사이트를 높이고 이를 촉진하는 데 도움이 되는 의료 데이터 및 데이터 분석 서비스를 캡처하고 전송할 수 있는 커넥티드 의료기기의 수가 증가하고 소프트웨어가 진보하고 있습니다. 커넥티드 의료기기를 안전하게 보호할 필요성은 의료 부문에서 데이터 유출 사건이 증가함에 따라 증가하고 있습니다.

- 의료 부문의 직원이 사용하는 연결 디바이스 증가는 정보 공유 증가로 이어집니다. 또한 엔드포인트는 이전보다 더 높은 위험에 노출되어 있습니다.

- 의료 산업에서는 컴플라이언스 및 HIPAA(Health Insurance Portability and Accountability Act : 의료 보험 상호 운용성 및 책임 법률) 중심 접근 방식에서부터 종합적이고 보안 중심 접근 방식으로 사이버 보안 전략의 변화가 진행되고 있습니다. 정부는 IoMT 장비의 안전과 보안과 관련하여 더 엄격한 규정을 부과할 것으로 예상됩니다. 의료 제공업체는 사이버 내성을 강화해야 합니다.

- 의료기기나 시스템의 취약성을 악용하려는 사이버 범죄자가 의료 부문을 표적으로 하는 경우가 늘고 있습니다. 병원에 대한 랜섬웨어 공격과 같은 유명한 사건은 견고한 사이버 보안 대책의 긴급한 필요성을 돋보이게합니다. 의료 조직은 제한된 예산을 당분간 보안 위협에 대처하는 것에 우선적으로 할당할 수 있습니다.

- 의료 모니터링 장비에 대한 인식 부족과 저개발 국가에서의 의료 보안을 위한 금전적 자금 부족은 의료기기 보안 시장의 성장을 방해할 것으로 예상됩니다.

- 의료 제공 기관은 원격 의료 플랫폼, 새로운 의료기기 그룹 및 기타 환자 지원 기술 등 COVID-19에 대한 대응을 지원하도록 설계된 기술의 도입을 신속하게 확대했습니다. 여기에는 임시 케어 사이트, 실험실, 연결된 디바이스의 더미, 환자 케어를 지원하는 데 필요한 원격 의료 플랫폼 등이 포함되었습니다.

의료기기 보안 시장 동향

커넥티드 의료기기에 대한 수요 증가가 시장 성장을 견인할 전망

- 의료 부문은 IoT 대응 기술을 통합한 스마트 웨어러블이나 원격 모니터링 장치 등의 신기술을 채용하여 생명과 관련된 서비스와 치료를 제공합니다. 의료 서비스는 더 나은 의료 서비스를 위해 환자 데이터를 얻기 위해 온라인화가 진행되고 있습니다. 이러한 웨어러블 의료기기는 기술 향상과 스마트폰과 같은 상용 기기와의 호환성으로 엄청난 인기를 얻고 있습니다. 건강 의식은 건강과 피트니스 상태를 모니터링하기 위해 이러한 스마트 웨어러블의 성장과 사용을 촉진합니다.

- 사이버 공격의 사례가 늘어나고 있는 가운데, 커넥티드 의료기기의 보안은 과제가 되고 있습니다. 더 많은 의료기기가 임상 네트워크에 통합되어 실시간으로 커넥티드 의료기기의 이용 데이터는 병원 및 의료 시스템 전체의 긴급 상황에 대비하고 자본 계획의 이니셔티브에 더 높은 정확성을 추가합니다.

- 2023년 8월 의료기기 제조업체(MDM)를 위한 프로액티브 사이버 보안 솔루션 제공업체인 Medcrypt Inc.는 의료 산업에서 중요한 사이버 보안 문제를 해결하기 위해 세계 XIoT 보안 문제의 세분화된 시각화를 제공하는 네트라이즈와 제휴했습니다. 이 제휴를 통해 의료기기 제조업체가 잠재적인 보안 위험을 적극적으로 식별하고 해결하고 의료기기의 안전과 무결성을 보장할 수 있는 소프트웨어 BOM(라이프사이클 관리 솔루션)을 MDM에 제공할 수 있습니다.

- 의료 부문에서 사물 인터넷(IoT) 장비의 보급이 진행되고 있는 것은 의료기기 보안 시장의 성장을 뒷받침하고 있습니다. Ericsson에 따르면 2022년 근거리 사물 인터넷(IoT) 디바이스의 수는 전 세계 103억 대에 달했습니다. 이 수는 2027년까지 250억 대까지 증가할 것으로 예상됩니다. 광역 IoT 디바이스는 2021년에는 약 29억 대로, 2027년에는 54억 대에 이를 것으로 예측됩니다.

북미가 큰 시장 점유율을 차지할 전망

- 의료는 디지털 환자 기록과 관련된 프라이버시와 보안 문제로 인해 북미에서 가장 엄격한 산업 중 하나입니다. 의료보험의 상호운용성과 책임에 관한 법률(HIPAA)과 경제적 및 임상적 건강을 위한 의료정보기술(HITECH)법 등의 규제에 의해 이 나라의 의료부문에 있어서 사이버 보안 솔루션의 보급률은 꾸준히 성장하고 있습니다.

- 미국과 캐나다는 신흥 경제 국가이며 연구 개발에 많은 투자를 할 수 있습니다. 산업 중점 부문 전체에서 디지털화의 진전, 꾸준한 기술 진보, 스마트 커넥티드 디바이스의 보급률의 상승이 북미의 IoT 디바이스 시장의 성장에 기여하고 있습니다. 커넥티드 디바이스와 관련 네트워크 인프라 이용 증가, 네트워크, 하드웨어, 소프트웨어 프로바이더의 연계 강화는 북미의 IoT 시장 확대를 뒷받침하는 주요 요인입니다.

- IoT 의료기기의 보급에 따라 위협 방지 방법이 요구되고 있습니다. 2023년 6월 미국 의료기기 사이버 보안 조직인 MedCrypt는 보안 평가 및 침입 테스트를 제공하기 위해 Stratigos Security와 제휴하여 일련의 제3자 평가 및 권고 서비스를 제공합니다.

- 2023년 11월, NYU 랑곤헬스는 Philips와 제휴하여 환자의 안전, 품질, 결과에 대한 새로운 의료 기술 솔루션을 도입했습니다. 정밀 진단 및 치료를 위해 환자 데이터를 확보하기 위한 새로운 협력 관계에는 디지털 병리학, 임상 정보학, 혁신적인 AI 대응 진단 및 서비스 모델로서의 기업 모니터링이 포함됩니다.

의료기기 보안 산업 개요

의료기기 보안 시장은 매우 세분화되어 있으며 Check Point Software Technologies, Cisco Systems Inc., FireEye Inc., McAfee Corp, Palo Alto Networks와 같은 대기업이 있습니다. 이 시장 진출 기업은 제품 라인업을 강화하고 지속 가능한 경쟁 우위를 얻기 위해 제휴 및 인수와 같은 전략을 채택하고 있습니다.

- 2023년 12월-엔터프라이즈 네트워킹 및 보안 리더 중 하나인 Cisco는 Cisco AI Assistant for Security를 발표했습니다. 이는 시스코의 통합 AI 주도 크로스 도메인 보안 플랫폼인 Security Cloud에 인공지능(AI)을 침투시키는 큰 단계입니다. AI 어시스턴트는 고객이 정보를 기반으로 의사 결정을 내리고, 도구 기능을 향상시키고, 복잡한 작업을 자동화하는 데 도움이 될 수 있습니다.

- 2023년 7월-Cynerio와 Check Point Software Technologies(Check Point Software Technologies)는 의료용 IoT 장비의 종합적인 보안을 의료 기관에 제공하기 위한 제휴를 발표했습니다. Cynerio의 360 플랫폼은 장치 감지, 패치 적용 지침, 마이크로 세분화, 공격 감지 등 의료용 IoT 장치의 보안을 보장하는 데 필수적인 기능을 제공합니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 산업의 매력-Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 진입업자의 위협

- 경쟁 기업간 경쟁 관계

- 대체품의 위협

- COVID-19의 산업에 대한 영향 평가

제5장 시장 역학

- 시장 성장 촉진요인

- 커넥티드 의료기기에 대한 수요 증가

- 정부 규제와 컴플라이언스의 필요성

- 시장 성장 억제요인 및 과제

- 제한된 의료 보안 예산

제6장 시장 세분화

- 솔루션

- 데이터 유출 방지 솔루션

- 안티바이러스 및 안티멀웨어 솔루션

- 암호화 솔루션

- 네트워크 및 엔드포인트 보안

- ID 확인 및 액세스 관리 솔루션

- 침입 감지 시스템 및 침입 방어 시스템

- 리스크 및 컴플라이언스 관리

- 기타 솔루션

- 디바이스 유형

- 병원용 의료기기

- 내장형 의료기기

- 웨어러블 의료기기

- 지역

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

제7장 경쟁 구도

- 기업 프로파일

- Check Point Software Technologies

- Cisco Systems Inc.

- FireEye Inc.

- McAfee LLC

- Palo Alto Networks Inc.

- IBM Corporation

- Imperva Inc.

- Fortinet Inc.

- General Electric Company

- ClearDATA

제8장 투자 분석

제9장 시장의 미래

AJY 25.02.20The Medical Device Security Market size is estimated at USD 8.47 billion in 2025, and is expected to reach USD 12.56 billion by 2030, at a CAGR of 8.2% during the forecast period (2025-2030).

The healthcare industry has been witnessing a significant transformation throughout the past few years, aided by the transformative nature of IoT technologies and advancements in computing power, wireless technologies, and data analytics techniques, such as Big Data. Big Data is currently being deployed in medical facilities and the medical research sector to analyze complex heterogeneous medical data that involves proteomics, genomics, and pharmacogenomics worldwide.

Key Highlights

- There is a rise in the number of connected medical devices and advancements in software that may capture and transmit medical data and data analytics services that help medical practitioners drive insights into and promote the delivery of predictive, preventive, personalized, and participatory medicines. The need to secure connected medical devices is rising owing to the increasing number of data breach incidents in the healthcare sector.

- The growing number of connected devices used by employees in the healthcare sector leads to more information sharing. It also places the endpoint at higher risk than ever.

- The healthcare industry is experiencing a transformation in cyber security strategy from a compliance and Health Insurance Portability and Accountability Act (HIPAA)-focused approach to a more comprehensive and security-centric approach. The governments are expected to impose stricter regulations about the safety and security of IoMT devices. Healthcare providers need to step up the game on cyber resilience.

- Cybercriminals seeking to exploit medical device and system vulnerabilities increasingly target the healthcare sector. High-profile incidents, such as ransomware attacks on hospitals, highlight the urgent need for robust cybersecurity measures. Healthcare organizations may prioritize allocating limited budgets to address immediate security threats.

- Lack of awareness about medical surveillance equipment and scarcity of monetary funds for healthcare security in underdeveloped countries are expected to hamper the growth of the medical device security market.

- Healthcare delivery organizations quickly scaled the implementations of technologies designed to support the response to COVID-19, including telehealth platforms, new fleets of medical devices, and other patient support technologies. This included temporary care sites, labs, troves of connected devices, and telehealth platforms desperately needed to support patient care.

Medical Device Security Market Trends

Increasing Demand for Connected Medical Devices is Expected to Drive the Market Growth

- The healthcare sector has adopted new technologies, such as smart wearables and remote monitoring equipment embedded with IoT-enabled technologies, to offer life-critical services and treatments. Healthcare services are moving online to capture patient data for better health services. These wearable medical devices are gaining immense popularity due to improved technologies and their compatibility with regularly used instruments, such as smartphones. Health awareness promotes the growth and use of these smart wearables to monitor health and fitness conditions.

- As cyberattack cases continue to rise, the security of connected medical devices is becoming challenging. With more medical devices integrated into clinical networks, real-time connected medical device utilization data adds greater accuracy to emergency preparedness and capital planning initiatives across hospitals and health systems.

- In August 2023, Medcrypt Inc., the proactive cybersecurity solution provider for medical device manufacturers (MDMs), partnered with Netrise, the company offering granular visibility into the world's XIoT security problem to solve critical cybersecurity challenges in the healthcare industry. This collaboration would offer the MDMs a Software Bill of Materials (SBOM) lifecycle management solution that would enable device manufacturers to proactively identify and address the potential security risks and ensure the safety and integrity of their medical devices.

- The increasing proliferation of connected Internet of Things (IoT) devices in the healthcare sector drives the growth of the medical device security market. According to Ericsson, in 2022, the number of short-range Internet of Things (IoT) devices reached 10.3 billion globally. That number is expected to increase to 25 billion by 2027. The wide-area IoT devices would be about 2.9 billion in 2021 and are forecasted to reach 5.4 billion by 2027.

North America is Expected to Hold Significant Market Share

- Healthcare is one of North America's most regulated industries due to privacy and security concerns associated with digital patient records. Regulations, such as the Health Insurance Portability and Accountability Act (HIPAA) and the Health Information Technology for Economic and Clinical Health (HITECH) Act, ensure a steady growth in the penetration rates of cyber security solutions in the country's healthcare sector.

- The United States and Canada have developed economies that enable them to invest heavily in R&D. Rising digitization throughout the industrial emphasis areas, steady technological advancements, and rising penetration of smart connected devices have all contributed to the growth of the North American IoT device market. The increased usage of connected devices and associated network infrastructure, as well as the increased collaboration of network, hardware, and software providers, are the primary drivers that assist in expanding the IoT market in North America.

- The proliferation of IoT medical devices demands threat-prevention methods. In June 2023, the US-based medical device cybersecurity organization MedCrypt partnered with Stratigos Security to provide security assessments and penetration testing, offering a suite of third-party assessment and advisory services.

- In November 2023, NYU Langone Health partnered with Philips to adopt new health technology solutions in patient safety, quality, and outcomes. The new collaboration to unlock patient data for precision diagnosis and treatment includes digital pathology, clinical informatics, and innovative AI-enabled diagnostics with enterprise monitoring as a service model.

Medical Device Security Industry Overview

The medical device security market is highly fragmented, with the presence of major players like Check Point Software Technologies, Cisco Systems Inc., FireEye Inc., McAfee LLC, and Palo Alto Networks Inc. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- December 2023 - Cisco, one of the enterprise networking and security leaders, unveiled the Cisco AI Assistant for Security. This marks a major step in making artificial intelligence (AI) pervasive in the Security Cloud, Cisco's unified, AI-driven, cross-domain security platform. The AI Assistant would help customers make informed decisions, augment their tool capabilities, and automate complex tasks.

- July 2023 - Cynerio and Check Point Software Technologies announced a partnership to offer healthcare organizations comprehensive security for their medical IoT devices. Cynerio's 360 platforms would offer functionality critical to securing healthcare IoT devices, including device discovery, patch guidance, micro-segmentation, and attack detection.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitute Products

- 4.3 Assessment of the Impact of COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand for Connected Medical Devices

- 5.1.2 Government Regulations and Need for Compliance

- 5.2 Market Restraint/Challenge

- 5.2.1 Limited Healthcare Security Budgets

6 MARKET SEGMENTATION

- 6.1 Solution

- 6.1.1 Data Loss Prevention Solutions

- 6.1.2 Antivirus/Antimalware Solutions

- 6.1.3 Encryption Solutions

- 6.1.4 Network and Endpoint Security

- 6.1.5 Identity and Access Management Solutions

- 6.1.6 Intrusion Detection Systems/Intrusion Prevention Systems

- 6.1.7 Risk and Compliance Management

- 6.1.8 Other Solutions

- 6.2 Device Type

- 6.2.1 Hospital Medical Devices

- 6.2.2 Internally Embedded Medical Devices

- 6.2.3 Wearable and External Medical Devices

- 6.3 Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia-Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East & Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Check Point Software Technologies

- 7.1.2 Cisco Systems Inc.

- 7.1.3 FireEye Inc.

- 7.1.4 McAfee LLC

- 7.1.5 Palo Alto Networks Inc.

- 7.1.6 IBM Corporation

- 7.1.7 Imperva Inc.

- 7.1.8 Fortinet Inc.

- 7.1.9 General Electric Company

- 7.1.10 ClearDATA