|

시장보고서

상품코드

1937338

양극재 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Cathode Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

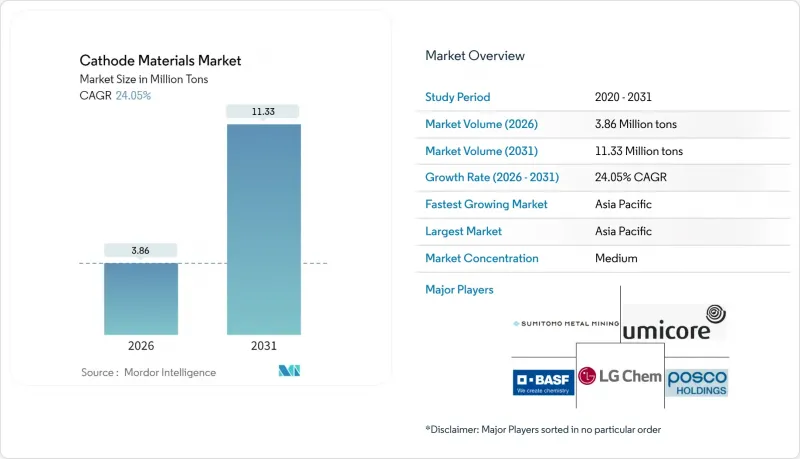

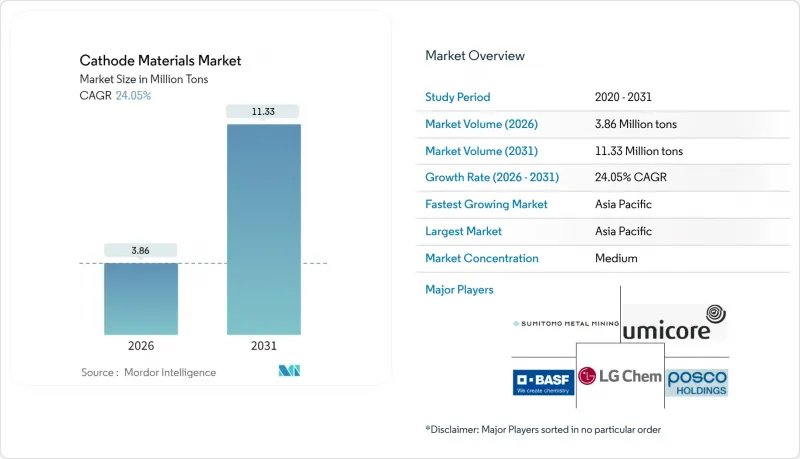

양극재 시장은 2025년 311만 톤에서 2026년에는 386만 톤으로 성장하여 2026년부터 2031년까지 CAGR 24.05%를 기록하며 2031년까지 1,133만 톤에 달할 것으로 예측됩니다.

전기자동차(EV) 생산 증가, 배출가스 규제 강화, 지역 기반 공급망 투자가 양극재 시장의 견조한 성장세를 뒷받침하고 있습니다. 한편, 전구체 불필요 합성 등 제조 공정의 발전으로 단위 비용은 점차 낮아지고 있습니다. 아시아태평양은 여전히 세계 생산량의 대부분을 차지하고 있지만, 북미와 유럽의 정책적 인센티브로 인해 공급 안보 위험을 줄이기 위해 지역 생산능력 확대가 가속화되고 있습니다. 리튬인산철(LFP)의 빠른 상용화와 니켈-망간-코발트(NMC) 혼합 재료의 적용 범위가 확대되고 있는 가운데, 고체 배터리 프로토타입은 미래의 배합 변화를 예고하고 있습니다. 재활용 인프라의 병행 정비와 재활용 함량 의무화는 양극재 원료의 경제성을 재구축하여 양극재 산업의 새로운 수익원을 창출하고 있습니다.

세계 양극재 시장 동향과 인사이트

급증하는 전기자동차 생산량

2024년 세계 전기자동차 배터리 설치 용량은 1,170GWh를 넘어 리튬이온 배터리 총 생산량의 약 76%를 차지하며, NMC, LMFP, 고급 LFP 변종 등 고에너지 양극재에 대한 수요를 직접적으로 견인하고 있습니다. 자동차 제조업체의 다년간의 배터리 공급 계약은 차량 생산 일정을 예측 가능한 양극재 주문 패턴으로 전환하여 양극재 시장에 대한 예측 가시성을 높이고 있습니다. 업스트림로의 파급효과는 KoBold Metals가 마노노리튬 광산에 10억 달러를 투자한 것에서 알 수 있듯이, 원자재 확장에 대한 새로운 자본 유입이 이루어지고 있습니다. 승용차를 넘어 버스, 배송 차량, 고정형 에너지 저장 시스템까지 채용 범위가 확대되어 대상 양극재 시장이 크게 확대되고 있습니다. 향후 모멘텀은 지속적인 소비자 수용과 전국적인 충전 인프라 구축에 달려있지만, 이는 지역에 따라 크게 달라질 수 있습니다.

정부 인센티브와 배출 규제

미국의 인플레이션 억제법, EU의 중요 원자재법 등의 입법은 OEM이 재정적 인센티브를 받기 위해 충족해야 하는 국내 조달 비율과 재활용 소재 비율을 규정함으로써 조달 전략을 재구성하고 있습니다. 외국 우려 기업(FOC) 조항과 연계된 세액 공제는 2025년 이후 미국 바이어가 중국 공급업체를 회피하도록 효과적으로 유도하고, 양극재 산업에서 미국 - 캐나다의 신규 양극재 공장에 단기적인 기회를 가져다 줄 것입니다. 유럽은 2030년까지 리튬-코발트의 완전한 가공 자급자족을 달성할 계획이며, 채굴 및 정제 프로젝트에 225억 유로를 투자하여 지역 조달 양극재 원료의 프리미엄 시장을 형성하고 있습니다. 캐나다의 1억 캐나다 달러 규모의 코발트 정련소 투자는 유럽과 미국 국가들이 업스트림 공정의 핵심 인프라를 어떻게 지원하고 있는지를 보여줍니다. 컴플라이언스 비용으로 인해 지역 조달 양극재에 20-30%의 가격 프리미엄이 발생하는 것으로 추정되지만, 동시에 장기적인 공급 리스크를 줄일 수 있는 장점이 있습니다.

주요 광물 가격 변동성(Ni, Co, Li)

상품 가격의 급격한 변동은 수익률을 압박하고 장기 계약을 복잡하게 만듭니다. 2024년 코발트 가격 급락으로 인해 BASF와 엘라멧의 26억 달러 규모의 니켈 사업 중단을 포함한 주요 프로젝트가 연기되었습니다. 탄산리튬에서도 비슷한 경향을 보이며 조달 헤지를 강요받고 있으며, MIT가 개발하고 람보르기니가 라이센스를 취득한 TAQ 유기 음극 등 코발트 무사용 화학 기술에 대한 관심이 가속화되고 있습니다. 가격의 불확실성은 재활용의 매력을 증가시키지만, 현재의 2차 재료 생산능력은 1차 공급의 변동을 상쇄하기에 충분하지 않습니다.

부문 분석

2025년 기준 리튬이온 배터리는 양극재 시장 점유율 88.20%를 차지하며 2031년까지 CAGR 25.62%를 기록할 것으로 예상됩니다. 이를 통해 EV, 가전, 축전 분야에서의 플랫폼으로서의 우위를 강화하고, 예측 기간 동안 리튬이온이 양극재 시장을 주도할 것으로 보입니다. 납축배터리는 자동차 스타터 분야에서 틈새시장을 유지하고 있지만, 리튬이온 배터리가 비용 측면에서 균형에 가까워지면서 점유율을 내주고 있습니다. 설치형 축전지 분야에서 나트륨 이온 배터리의 초기 도입이 상용화될 조짐을 보이고 있지만, 아직 전체 시장에서 차지하는 비중은 미미합니다. 플로우 배터리는 높은 초기 비용으로 인해 특수 전력망 프로젝트에 국한되어 있지만, 에너지 밀도의 지속적인 향상으로 인해 금세기 말까지 새로운 기회 계층을 개척할 수 있습니다.

지속적인 규모의 경제 효과, 6배의 수명 향상, CATL의 6C 초급속 충전 LFP 아키텍처와 같은 셀-투-팩 혁신으로 리튬이온 배터리의 성능과 비용 우위는 유지될 것입니다. 재활용 함량 규제 추진은 순환형 원료 루프를 확보하여 리튬이온 배터리의 설치 기반을 더욱 강화할 것입니다. 그 결과, 리튬이온 배터리는 앞으로도 양극재 산업의 가격 책정, 제조 기준, 연구개발 방향을 주도해 나갈 것입니다.

양극재 시장 보고서는 배터리 종류별(납축배터리, 리튬이온 배터리, 리튬이온, 나트륨이온, 플로우전지), 재료별(리튬인산철, 리튬코발트산염, 리튬니켈망간코발트산염, 리튬망간산리튬 등), 최종사용자 산업별(자동차, 가전, 전기전자, 전동 공구 등), 지역별(아시아, 북미, 유럽, 중동, 아프리카, 아시아태평양) 등으로 분류되어 있습니다. 공구 등), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)으로 분류되어 있습니다.

지역별 분석

아시아태평양은 2025년 시장 점유율의 79.10%를 차지하며 2031년까지 CAGR 26.34%를 기록할 것으로 예상됩니다. 이는 채굴, 가공, 셀 제조에 걸친 깊은 통합을 반영합니다. 중국은 비용 우위와 고유한 공정 전문성을 통해 이 생태계를 지원하고 지속적인 혁신의 속도를 가능하게 합니다. 한국과 일본은 상호보완적인 고정밀 제조와 첨단 소재 배합을 제공하여 지역적 우위를 강화하고 있습니다.

북미는 중요한 지역 부문이며, 인플레이션 억제법과 국내 조달 요건이 새로운 음극 공장에 대한 자본 유입을 촉진하고 있습니다. 미국 정부가 제안한 사커패스 광산 10% 투자 및 캐나다 코발트 제련소 증설은 공급 리스크 감소를 위한 업스트림 자산의 가속화를 상징합니다. 그러나 높은 투입비용과 긴 허가 취득 주기가 단기적인 경쟁력을 억제하고 있습니다.

유럽 핵심원료법은 2030년까지 리튬과 코발트의 자급자족을 달성하기 위해 47개 프로젝트에 총 225억 유로를 보장하고, 원료 조달을 재구성하는 엄격한 재활용 함량 의무를 규정하고 있습니다. 이 지역의 지속가능성 중심의 접근 방식은 순환형 공급망을 촉진하지만, 아시아 수입품과의 비용 경쟁력에 대한 도전이 있습니다. 중동 및 아프리카는 신흥 시장임에도 불구하고 풍부한 기회를 가지고 있으며, 진행 중인 재생에너지 사업이 지역적 수요 기반을 창출하고 있어 향후 투자 핫스팟으로 발전할 가능성이 있습니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSM 26.03.09The Cathode Materials Market is expected to grow from 3.11 Million tons in 2025 to 3.86 Million tons in 2026 and is forecast to reach 11.33 Million tons by 2031 at 24.05% CAGR over 2026-2031.

Rising electric-vehicle (EV) production, aggressive emissions regulations, and localized supply-chain investments anchor the robust growth trajectory of the cathode materials market, while advances in manufacturing processes, such as precursor-free synthesis, are gradually lowering unit costs. Asia-Pacific continues to contribute the bulk of global output, yet North American and European policy incentives are accelerating regional capacity additions to mitigate supply-security risks. Rapid commercialization of lithium-iron-phosphate (LFP) and evolving lithium-nickel-manganese-cobalt (NMC) blends broadens application windows, even as solid-state prototypes foreshadow future formulation shifts. Parallel development of recycling infrastructure and mandatory recycled-content quotas is recasting cathode feedstock economics and fostering new revenue pools in the cathode materials industry.

Global Cathode Materials Market Trends and Insights

Surging EV Production Volumes

Global EV battery installations surpassed 1,170 GWh in 2024, equaling roughly 76% of all lithium-ion battery output and directly driving demand for higher-energy cathodes such as NMC, LMFP, and advanced LFP variants. Automakers' multiyear battery-supply contracts are translating vehicle production schedules into predictable cathode ordering patterns, strengthening forecasting visibility in the cathode materials market. The upstream ripple is evident in KoBold Metals' USD 1 billion commitment to the Manono lithium deposit, signaling fresh capital flows into raw-material expansion. Adoption extends beyond passenger cars into buses, delivery fleets, and stationary energy-storage systems, substantially enlarging the addressable cathode materials market. Future momentum rests on sustained consumer acceptance and nationwide charging-infrastructure build-outs, which vary widely by region.

Government Incentives and Emissions Regulations

Legislation such as the U.S. Inflation Reduction Act and the EU Critical Raw Materials Act reshapes procurement strategies by imposing domestic-content and recycled-content thresholds that OEMs must meet to unlock financial incentives. Tax credits linked to Foreign Entity of Concern provisions effectively steer American buyers away from Chinese suppliers starting in 2025, opening near-term opportunities for new U.S. and Canadian cathode plants in the cathode materials industry. Europe's plan to achieve full processing self-sufficiency in lithium and cobalt by 2030 channels EUR 22.5 billion into extraction and refining projects, providing a premium market for regionally sourced cathode feedstock. Canada's CAD 100 million cobalt refinery investment demonstrates how Western governments are underwriting critical upstream infrastructure. Compliance costs are driving a price premium-estimated at 20-30%-for regionally sourced cathode materials but simultaneously de-risking long-term supply.

Critical Mineral Price Volatility (Ni, Co, Li)

Sharp commodity-price swings erode margins and complicate long-term contracts. Cobalt prices sank in 2024, prompting major project deferrals, including BASF-Eramet's USD 2.6 billion nickel venture cancellation. Similar patterns in lithium carbonate have forced procurement hedges and accelerated interest in cobalt-free chemistries like MIT's TAQ organic cathode licensed by Lamborghini. Price unpredictability amplifies the appeal of recycling, yet current secondary-material capacity is insufficient to offset primary-supply volatility.

Other drivers and restraints analyzed in the detailed report include:

- Battery-Pack Cost Decline from Scale Learning

- Localization of Cathode Supply Chains in US and EU

- Supply-Chain Concentration in China

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Lithium-ion batteries comprised 88.20% of the cathode materials market share in 2025 and are tracking a 25.62% CAGR to 2031, reinforcing the platform's primacy across EV, consumer electronics, and storage sectors. This dominance positions lithium-ion as the engine of the cathode materials through the forecast horizon. Lead-acid retains an automotive-starter niche but surrenders volume as lithium-ion approaches cost parity. Nascent sodium-ion deployments in stationary storage demonstrate early commercialization yet still represent a marginal slice of overall market size. Flow batteries remain confined to specialized grid projects due to higher upfront costs, but ongoing energy-density gains could unlock new opportunity strata by decade's end.

Continuing scale benefits, six-fold life-cycle improvements, and cell-to-pack innovations such as CATL's 6C ultra-fast-charging LFP architecture sustain lithium-ion's performance-cost momentum. Regulatory push for recycling content further cements lithium-ion's installed base by ensuring a circular raw-material loop. Consequently, lithium-ion will continue dictating pricing, manufacturing standards, and R&D direction within the cathode materials industry.

The Cathode Materials Market Report is Segmented by Battery Type (Lead-Acid, Lithium-Ion, Sodium-Ion, Flow Batteries), Materials (Lithium Iron Phosphate, Lithium Cobalt Oxide, Lithium-Nickel Manganese Cobalt, Lithium Manganese Oxide, and More), End-User Industry (Automotive, Consumer Electronics, Power Tools, and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle-East and Africa).

Geography Analysis

Asia-Pacific commanded 79.10% of the market share in 2025 and is on a 26.34% CAGR trajectory to 2031, reflecting deep integration across mining, processing, and cell manufacturing. China anchors this ecosystem through cost advantages and proprietary process expertise, enabling sustained innovation velocity. South Korea and Japan provide complementary high-precision manufacturing and advanced material formulations, reinforcing regional dominance.

North America is a significant regional segment, catalyzed by the Inflation Reduction Act and domestic-content requirements funneling capital into new cathode plants. The U.S. government's proposed 10% stake in Thacker Pass and Canada's cobalt refinery build-out exemplify upstream asset acceleration aimed at de-risking supply. Nevertheless, higher input costs and lengthy permitting cycles temper short-term competitiveness.

Europe's Critical Raw Materials Act underwrites EUR 22.5 billion across 47 projects to achieve lithium and cobalt self-sufficiency by 2030, paired with stringent recycled-content mandates that reshape feedstock sourcing. The region's sustainability-centric approach fosters closed-loop supply chains but challenges cost parity with Asian imports. The Middle East and Africa remain emerging yet opportunity-rich, with ongoing renewable-energy initiatives creating localized demand nodes that could evolve into future investment hotspots.

- BASF

- Contemporary Amperex Technology Co., Limited.

- Ecopro BM

- Eramet (Sandouville)

- Guangxi CNGR Advanced Material

- Himadri Speciality Chemical Ltd

- Huayou Cobalt Co., Ltd.

- IBU-tec

- LANDF CORP

- LG Chem

- MITSUI MINING & SMELTING CO.,LTD.

- NICHIA CORPORATION

- Nippon Chemical Industrial Co., Ltd.

- POSCO HOLDINGS. (POSCO FUTURE M)

- Shenzhen Dynanonic Co., Ltd.

- Showa Denko Materials

- Sumitomo Metal Mining Co., Ltd.

- Targray

- Umicore

- XTC New Energy Materials

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging EV production volumes

- 4.2.2 Government incentives and emissions regulations

- 4.2.3 Battery-pack cost decline from scale learning

- 4.2.4 Localization of cathode supply chains in US and EU

- 4.2.5 Sodium-ion and LMFP commercialisation expanding cathode demand

- 4.3 Market Restraints

- 4.3.1 Critical mineral price volatility (Ni, Co, Li)

- 4.3.2 Supply-chain concentration in China

- 4.3.3 Solid-state batteries reducing cathode mass/kWh

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Battery Type

- 5.1.1 Lead-acid

- 5.1.2 Lithium-ion

- 5.1.3 Sodium-ion

- 5.1.4 Flow batteries

- 5.2 By Materials

- 5.2.1 Lithium Iron Phosphate

- 5.2.2 Lithium Cobalt Oxide

- 5.2.3 Lithium-Nickel Manganese Cobalt

- 5.2.4 Lithium Manganese Oxide

- 5.2.5 Lithium Nickel Cobalt Aluminium Oxide

- 5.2.6 Lead Dioxide

- 5.2.7 Other Materials (Sodium Iron Phosphate, Oxyhydroxide, and Graphite)

- 5.3 By End-user Industry

- 5.3.1 Automotive

- 5.3.2 Consumer Electronics

- 5.3.3 Power Tools

- 5.3.4 Energy Storage

- 5.3.5 Other Applications (Medical Devices, Aerospace Components, etc)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 South Korea

- 5.4.1.4 India

- 5.4.1.5 Indonesia

- 5.4.1.6 Vietnam

- 5.4.1.7 Thailand

- 5.4.1.8 Malaysia

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Nordic Countries

- 5.4.3.7 Turkey

- 5.4.3.8 Russia

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share**/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 BASF

- 6.4.2 Contemporary Amperex Technology Co., Limited.

- 6.4.3 Ecopro BM

- 6.4.4 Eramet (Sandouville)

- 6.4.5 Guangxi CNGR Advanced Material

- 6.4.6 Himadri Speciality Chemical Ltd

- 6.4.7 Huayou Cobalt Co., Ltd.

- 6.4.8 IBU-tec

- 6.4.9 LANDF CORP

- 6.4.10 LG Chem

- 6.4.11 MITSUI MINING & SMELTING CO.,LTD.

- 6.4.12 NICHIA CORPORATION

- 6.4.13 Nippon Chemical Industrial Co., Ltd.

- 6.4.14 POSCO HOLDINGS. (POSCO FUTURE M)

- 6.4.15 Shenzhen Dynanonic Co., Ltd.

- 6.4.16 Showa Denko Materials

- 6.4.17 Sumitomo Metal Mining Co., Ltd.

- 6.4.18 Targray

- 6.4.19 Umicore

- 6.4.20 XTC New Energy Materials

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment