|

시장보고서

상품코드

1537608

슬립 첨가제 시장 : 점유율 분석, 산업 동향·통계, 성장 예측(2024-2029년)Slip Additives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

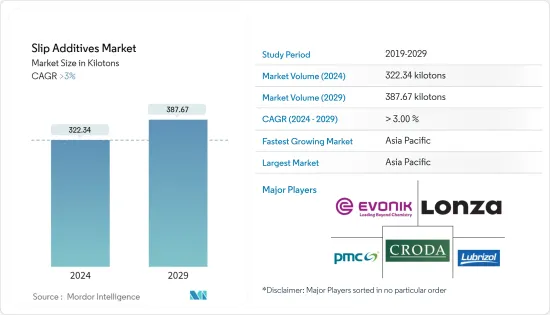

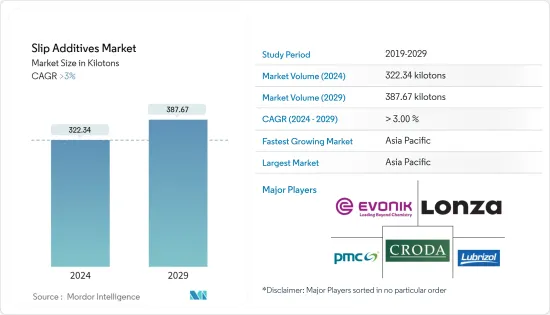

세계 슬립 첨가제 시장 규모는 2024년 322.34킬로톤에 달하고, 2024-2029년 예측기간 동안 CAGR 3% 이상의 성장률로 추이하고, 2029년에는 387.67킬로톤에 달할 것으로 예측되고 있습니다.

COVID-19 팬데믹은 슬립 첨가제 시장에 긍정적인 영향을 미쳤습니다. 봉쇄 기간 중 소비재, 의약품, 식품 및 음료 등의 온라인 판매가 포장 제품 수요를 증가시켰기 때문에 슬립 첨가제 시장 전망은 밝아졌습니다. COVID-19의 유행 이후, 포장 및 비포장 용도에 대한 수요 증가로 시장은 성장률을 더욱 기록했습니다.

식품 및 음료 포장 산업에서의 수요 증가와, 대체품에 비해 저가격으로 입수할 수 있는 것이, 실리콘 코팅 시장을 견인할 것으로 예상됩니다.

플라스틱 사용에 대한 엄격한 환경 규제는 시장 성장을 방해할 것으로 예상됩니다.

바이오 슬립 첨가제 시장 개척과 의료 용도에서 플라스틱 필름 수요 증가는 예측 기간 동안 시장에 기회를 가져올 것으로 예상됩니다.

아시아태평양이 시장을 독점할 것으로 예상됩니다. 또한 포장 및 비포장 용도에서 슬립 첨가제 수요 증가로 인해 예측 기간 동안 가장 높은 CAGR을 나타낼 것으로 예상됩니다.

슬립 첨가제 시장 동향

포장 용도가 시장을 독점

- 슬립 첨가제 수요가 증가하고 있는 주요 요인은 식품 및 음료 산업에 있어서의 사용량 증가입니다. 플라스틱 포장은 포장된 제품의 저장 수명을 연장하고 식품 누출을 줄이는 데 도움이 됩니다.

- 포장 산업의 중요한 동향 중 하나는 제품의 안전과 위생을 손상시키지 않고 포장 폐기물을 줄이기 위해 일회용 플라스틱의 사용을 금지하는 것입니다. 이러한 요인으로 인해 폴리올레핀 플라스틱 포장용 필름에 대한 수요가 증가할 것으로 보입니다. 슬립 첨가제는 마찰을 줄이는 데 사용되며 포장 재료에 원하는 특성을 부여하는 데 도움이 될 것입니다.

- 포장 분야는 슬립 첨가제의 가장 광범위한 용도가 될 것으로 예상됩니다. 중합체 필름은 주로 포장 및 라벨링에 사용됩니다. 폴리에틸렌 필름 및 캐스트 필름의 제조에서 슬립 첨가제의 중요한 역할은 필름 표면에 슬립 특성을 부여하는 것입니다.

- 식품포장시장은 향후 수년간 큰 성장률을 기록할 가능성이 높습니다. Foodservice Packaging Association에 따르면 세계 식품 포장 시장의 매출은 2022년에 3억 6,380만 달러를 기록했으며, 2026년에는 4억 5,830만 달러에 이를 것으로 예상됩니다. 따라서 식품 포장 시장의 성장은 현재의 연구 시장을 견인하는 것으로 보입니다.

- 제약 산업에서 폴리에틸렌과 폴리프로필렌 포장은 1차 포장 재료로 널리 사용됩니다. 이 포장재는 다목적이며 고성능이며 의료 및 제약 용도로 사용됩니다. 플라스틱 필름은 산소와 냄새, 습기, 수증기 투과, 오염, 박테리아로부터 의약품을 보호합니다. 플라스틱 필름은 스포이드, 주사기 등 다양한 플라스틱 포장 제품에 사용됩니다. 세계 의약품 시장은 최근 몇 년동안 크게 성장하고 있습니다. 2022년 세계 의약품 시장은 전년 대비 4.2%의 성장률로 1조 4,800억 달러를 기록했습니다.

- 이와 같이 식품 및 음료 포장과 의약품 포장 용도 수요 증가가 슬립 첨가제 수요를 견인하게 됩니다.

아시아태평양이 시장을 독점

- 아시아태평양은 세계에서 가장 큰 슬립 첨가제 시장입니다. 중국, 인도 및 일본은이 지역의 슬립 첨가제의 최대 시장입니다.

- 아시아태평양에서는 중간층 인구 증가, 급속한 산업화, 포장 제품 사용량 증가 등의 요인이 포장 산업을 견인해 슬립 첨가제 시장에 다양한 성장 전망을 가져올 것으로 예상됩니다.

- 중국과 인도는 이 지역에서 가장 큰 식품 및 음료 시장입니다. 중국국가경공업위원회에 따르면 연간 매출액이 280만 달러를 넘는 주요 식품제조기업은 2022년 1조 5,300억 달러를 넘는 수익을 보고했습니다. 2021년에 비해 총수입은 전년 대비 5.6% 증가했으며 식품산업의 강력한 성장을 보여주고 있습니다. 따라서 식품 및 음료 산업의 성장으로 식품 및 음료 포장 용도에 사용되는 슬립 첨가제 수요가 증가할 것으로 예상됩니다.

- 마찬가지로 의약품 포장 응용에서도 슬립 첨가제에 대한 수요가 증가하고 있습니다. 인도는 세계 의약품 허브이며 200여 개국에 의약품을 수출하고 있습니다. 2023년 상반기에는 의약품 산업에 대한 외국 직접 투자 유입액이 25% 증가했습니다. IBEF에 따르면 제약산업의 수익은 2024년까지 650억 달러에 달할 것으로 예상됩니다. 따라서 의약품 시장의 확대는 현재의 연구 시장을 견인하게 됩니다.

- 일본은 현재 세계에서 세 번째로 유명한 전자상거래 시장입니다. 일본 전자상거래 시장의 수익은 2023년까지 2,322억 달러를 창출하고, 2027년까지 3,554억 달러에 이를 것으로 예상됩니다. 또한 일본의 화장품 시장에서 상품을 구입하는 소비자는 보다 선택적이 되어 가치에 대한 의식이 높아지고 있습니다. 그러므로 전자상거래 시장의 확대는 일본에서의 포장 용도를 촉진하고 슬립 첨가제 시장을 견인하게 됩니다.

- 위의 요인들로부터 아시아태평양의 슬립 첨가제 시장은 예측 기간 동안 크게 성장할 것으로 예측됩니다.

슬립 첨가제 산업 개요

슬립 첨가제 시장은 그 특성상 부분적으로 단편화됩니다. 이 시장의 주요 기업으로는 Croda International Plc, Evonik Industries AG, Lonza, PMC Group, Inc., The Lubrizol Corporation 등이 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 성장 촉진요인

- 식품 및 음료 포장 산업에서의 수요 증가

- 대체품에 비해 저렴한 가격으로 이용가능성

- 기타 촉진요인

- 억제요인

- 플라스틱 사용에 관한 엄격한 환경 규제

- 기타 억제요인

- 산업 밸류체인 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 세분화(시장 규모 : 수량 기준)

- 캐리어 수지

- 폴리에틸렌

- 폴리프로필렌

- 기타 캐리어 수지

- 유형

- 지방 아미드

- 왁스 및 폴리실록산

- 기타 유형

- 용도

- 포장

- 식품 및 음료

- 소비재

- 헬스케어

- 비포장

- 포장

- 지역

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 이탈리아

- 프랑스

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 합병·인수, 합작 사업, 제휴, 협정

- 시장 점유율(%)/랭킹 분석

- 주요 기업의 전략

- 기업 프로파일

- Afron

- ALTANA

- BASF SE

- Croda International Inc.

- Emery Oleochemicals

- Evonik Industries AG

- Fine Organics

- Honeywell International

- Lonza

- The Lubrizol Corporation

- PMC Group, Inc.

제7장 시장 기회와 앞으로의 동향

- 바이오 슬립 첨가제 개발

- 의료 용도에 있어서의 플라스틱 필름 수요 증가

The Slip Additives Market size is estimated at 322.34 kilotons in 2024, and is expected to reach 387.67 kilotons by 2029, growing at a CAGR of greater than 3% during the forecast period (2024-2029).

The COVID-19 pandemic had a positive impact on the slip additives market. During the lockdown, the online sales of consumer goods, pharmaceuticals, food, and beverage products increased the demand for packaged products, thus creating a positive market outlook for slip additives. Post-COVID-19 pandemic, the market further registered a growth rate due to rising demand from packaging and non-packaging applications.

Increasing demand from the food and beverage packaging industry and the availability at low prices compared to substitutes are expected to drive the market for silicone coatings.

The stringent environmental regulations on the use of plastics are expected to hinder the market's growth.

The development of bio-based slip additives and the increasing demand for plastic films in medical applications are expected to create opportunities for the market during the forecast period.

The Asia-Pacific region is expected to dominate the market. It is also expected to register the highest CAGR during the forecast period due to rising demand for slip additives in packaging and non-packaging applications.

Slip Additives Market Trends

Packaging Application to Dominate the Market

- The increasing demand for slip additives is majorly attributed to the growing usage in the food & beverage industry. Plastic packaging helps increase the shelf life of the products packed and reduces leakages of food products.

- One of the significant trends in the packaging industry is the ban on the usage of single-use plastic to reduce packaging waste without compromising the safety and hygiene of the products. These factors will increase the demand for polyolefin plastic packaging films. The slip additives are used to decrease friction and will likely help to get the desired properties in the packaging material.

- The packaging segment is anticipated to be the most extensive application of slip additives. Polymer films are mainly preferred in the packaging industry for packing and labeling. The critical function of slip additives in the production of polyethylene and cast film is to deliver slip properties to the film surface.

- The food packaging market is likely to register a significant growth rate in the coming years. According to the Foodservice Packaging Association, the global food packaging market revenue is recorded at USD 363.8 million in 2022, and it is projected to reach USD 458.3 million by 2026. Thus, the growth in the food packaging market will drive the current studied market.

- In the pharmaceutical industry, polyethylene and polypropylene packaging are widely used as primary packaging materials. These packaging materials are versatile, high-performance, and used in medical and pharmaceutical applications. The plastic films protect the pharmaceutical product against oxygen and odor, moisture, water vapor transmission, contamination, and bacteria. They are used in various plastic packaging products, including eyedroppers, syringes, and others. The global pharmaceutical market has grown significantly in recent years. In 2022, the global pharmaceutical market registered at USD 1.48 trillion, at a growth rate of 4.2% compared to the previous year.

- Thus, the growing demand for food and beverage packaging and pharmaceutical packaging applications will drive the demand for slip additives.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific is the largest market for slip additives in the world. China, India, and Japan are the largest markets for slip additives in the region.

- In the Asia-Pacific region, factors such as the growing middle-class population, rapid industrialization, and the increasing usage of packed products are expected to drive the packaging industry, providing various growth prospects to the slip additives market.

- China and India are the largest food and beverage markets in the region. According to the China National Light Industry Council, major food manufacturing companies with an annual turnover of over USD 2.8 million reported revenues of over USD 1.53 trillion in 2022. Compared to 2021, the total revenue registered a year-on-year growth of 5.6%, indicating strong growth in the food industry. Thus, the growth of the food and beverage industries is expected to increase the demand for slip additives used in food and beverage packaging applications.

- Similarly, the demand for slip additives is increasing in pharmaceutical packaging applications. India is a global pharmaceutical hub, exporting pharmaceuticals to over 200 countries. In the first half of FY 2023, foreign direct investment inflows into the pharmaceutical industry increased by 25%. According to IBEF, the pharmaceutical industry revenue is expected to reach USD 65 billion by 2024. Thus, the increasing market for pharmaceuticals will drive the current studied market.

- Japan is currently the world's third most prominent e-commerce market in the world. Revenue in the e-commerce market in Japan was expected to generate USD 232.20 billion by 2023 and is further expected to reach USD 355.40 billion by 2027. Also, consumers purchasing goods within the cosmetics market in Japan are becoming more selective and value-conscious. Thus, the increasing e-commerce market will drive the packaging application in the country, thereby driving the market for slip additives.

- Owing to the factors mentioned above, the slip additives market in the Asia-Pacific is projected to grow significantly during the forecast period.

Slip Additives Industry Overview

The slip additives market is partially fragmented in nature. Some of the major players in the market include (not in any particular order) Croda International Plc, Evonik Industries AG, Lonza, PMC Group, Inc., and The Lubrizol Corporation, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand from Food & Beverage Packaging Industry

- 4.1.2 Availability at Low Price Compared to Substitutes

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Stringent Environmental Regulations on The Use of Plastics

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Carrier Resin

- 5.1.1 Polyethylene

- 5.1.2 Polypropylene

- 5.1.3 Other Carrier Resins (Polyvinyl Chloride, Polyamide,etc.)

- 5.2 Type

- 5.2.1 Fatty Amides

- 5.2.2 Waxes and Polysiloxanes

- 5.2.3 Other Types (Esters, Salts, etc.)

- 5.3 Application

- 5.3.1 Packaging

- 5.3.1.1 Food and Beverage

- 5.3.1.2 Consumer Goods

- 5.3.1.3 Healthcare

- 5.3.2 Non-Packaging

- 5.3.1 Packaging

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Afron

- 6.4.2 ALTANA

- 6.4.3 BASF SE

- 6.4.4 Croda International Inc.

- 6.4.5 Emery Oleochemicals

- 6.4.6 Evonik Industries AG

- 6.4.7 Fine Organics

- 6.4.8 Honeywell International

- 6.4.9 Lonza

- 6.4.10 The Lubrizol Corporation

- 6.4.11 PMC Group, Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Development of Bio-based Slip Additives

- 7.2 The Increasing Demand for Plastic Films in Medical Applications