|

시장보고서

상품코드

1911827

마이크로디스플레이 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)Microdisplay - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

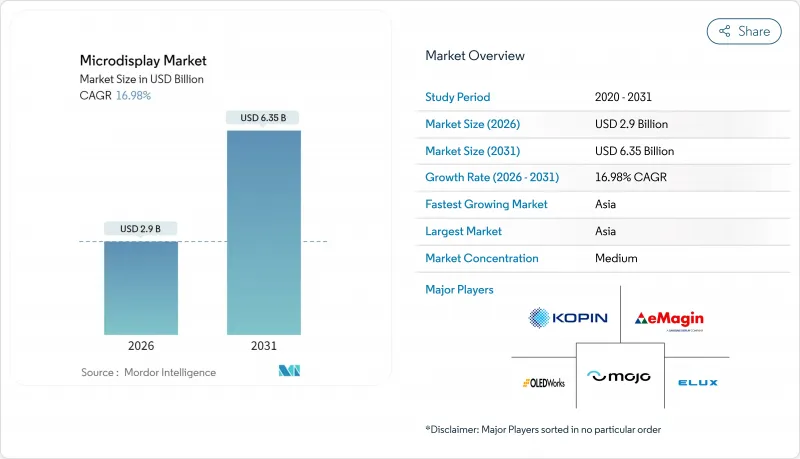

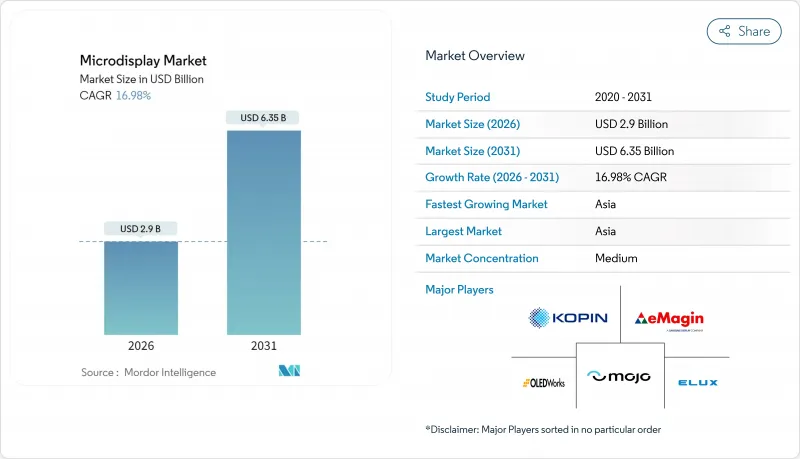

마이크로디스플레이 시장 규모는 2026년에 29억 달러로 추정되고, 2025년 24억 8,000만 달러에서 성장이 예상됩니다.

2031년까지 63억 5,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 16.98%로 성장할 것으로 전망되고 있습니다.

여러 혁신 사이클이 동시에 수렴하고 있습니다. 마이크로 LED의 대량 전사 수율이 드디어 안정화해, AR/VR 에코시스템이 스케일업 단계에 들어가, 레벨 3 이상의 운전 지원 시스템이 투명 헤드업 디스플레이를 프로토타입으로부터 양산으로 추진하고 있습니다. 제조 기술의 비약적 진보, 특히 5마이크로미터의 MicroLED 칩에 대해 99.7%의 배치 정밀도를 달성하는 레이저 유도 포워드 전사(LIFT) 기술에 의해 오랫동안 보급을 막아 온 비용 장벽이 해소되었습니다. 가전 대기업이 전문 공급업체와 제휴하는 경쟁 격화에 의해 실험실에서의 실증부터 소비자용 발매까지의 기간이 단축되고 있습니다. 지속적인 방위 지출과 자동차 안전 규제는 경기 변동을 완화하는 견조한 최종 시장 수요를 초래합니다. 사파이어 기판과 실리콘 백플레인 공급 제약이 주요 사업 리스크로 계속되고 있지만, 계속적인 생산 능력 증강에 의해 이러한 역풍은 2026년 이후 완화될 전망입니다.

세계의 마이크로디스플레이 시장 동향 및 인사이트

아시아 전역에서 AR/VR 웨어러블용 초소형 디스플레이 수요 급증

가처분 소득 증가 및 확립된 가전 공급망으로 동아시아는 차세대 스마트 글라스 발사대가 되었습니다. 상하이 거점의 JBD는 2021년 이후 100만 대 이상의 MicroLED 엔진을 출하해 연간 50%의 출하 대수 성장을 계속하고 있으며, 이 지역의 양산 잠재력을 실증하고 있습니다. 중국 SidTek사는 2024년 8억 2,630만 달러를 투자한 12인치 OLED-on-silicon 생산 라인의 시운전을 시작하여 수요 급증에 대응하는 현지 생산 능력을 확보했습니다. 지역 통합으로 물류 비용과 설계 사이클 타임이 단축되어 OEM 업체는 경쟁사보다 신속하게 광학계, 도파관, 구동 IC의 개량을 거듭할 수 있게 되었습니다. 이 제조 집적을 배경으로 부품 가격이 하락하는 가운데, 마이크로디스플레이 시장은 보다 폭넓은 소비자층에 대한 전개 기반을 획득하고 있습니다. 규모, 비용 및 보급의 호순환에 의해 이 지역은 향후도 세계 마이크로디스플레이 시장의 성장 엔진으로서의 지위를 유지할 전망입니다.

자동차 제조업체, 레벨 3 ADAS용 투명 마이크로 LED HUD로 전환

자동차 제조업체 각사는 앞 유리에 운전자 정보와 실경을 융합시키는 기술 개발을 겨루고 있습니다. 마이크로 LED 기술은 직사광선에서도 시인성을 유지하면서 전력 소비를 억제하기 위해 필요한 휘도 여력을 제공하여 기존의 프로젝터식 HUD에 비해 20-50배의 효율성을 실현합니다. 2025년 CES에서 발표된 AUO의 '버추얼 스카이 캐노피' 조종석 등의 실증은 곡면 및 베젤리스의 시각 표면이 양산 단계에 도달하고 있음을 증명하고 있습니다. 투명 HUD는 시선의 높이에 경고를 표시하여 교통사고의 1/4의 원인이 되는 주의 산만도 경감합니다. 이 안전의 장점은 특히 유럽에서 레벨 3 자동 운전의 규제 추진과 함께 마이크로 LED HUD를 미래의 표준 장비로 이끌 것입니다. 2026년 이후, 고급차로의 도입이 시작됨에 따라, 마이크로디스플레이 시장 전체에의 파급 효과는 현저해질 전망입니다.

RGB 마이크로 LED 양산 공정에서 수율 손실

개발에 120억 달러, 인수에 24억 달러를 투자했음에도 불구하고, 양산 전사의 수율은 풀 컬러 MicroLED 디스플레이 비용의 필요성을 계속하고 있습니다. 서브 미크론 단위의 배치 오차조차 눈에 보이는 불량 화소가 되어, 고비용의 재작업 작업을 강요합니다. 코히런트의 LIFT 프로세스는 중요한 전진이지만, 헤드셋에 필요한 수백만 개의 칩으로 단일 패널의 정확성을 확장하는 것은 인라인 검사 및 복구 워크플로우에 여전히 어려움이 있습니다. 오스람의 말레이시아 공장 확장 및 에노스타의 대만 공장 확장은 모두 수율의 두드림을 해소하기 위해 기술자가 임하는 가운데, 완성 시기가 2026년에서 2027년으로 늦춰졌습니다. 따라서 향후 2년간이 소비자용 마이크로 LED의 보급 페이스를 결정하게 될 것입니다.

부문 분석

2025년 시점에서 기존의 LCoS, LCD, DLP 모듈이 마이크로디스플레이 시장의 48.62%를 차지했습니다. 그러나 전사 수율 향상 및 경쟁사를 능가하는 전력 효율로 인해 MicroLED 디바이스는 2031년까지 연평균 복합 성장률(CAGR) 20.85%로 확대될 것으로 전망됩니다. Q-Pixel은 6,800 PPI의 MicroLED 어레이를 시연했으며, Apple Vision Pro의 3,380 PPI 기준치를 뛰어넘어 시각적 정확도 향상의 여지를 증명했습니다. 따라서 MicroLED의 마이크로디스플레이 시장 규모는 비용 곡선이 OLED-on-Si를 능가할 때 급성장할 전망입니다. 유럽에서는 Aledia의 2억 달러 규모 GaN-on-silicon 생산 라인이 아시아 이외 공급 기반 다양화를 실현하는 대체 공급원을 제공합니다. Applied Materials사의 프로토타입이 90% 이상의 DCI-P3 색역을 실현한 양자 도트 온 실리콘 기술은 절대적인 휘도보다 색 균일성을 중시하는 브랜드를 위한 하이브리드 솔루션으로 주목받고 있습니다.

OLED-on-Si는 종래 기술 및 신흥 솔루션의 중간에 위치해, 성숙한 증착 기술의 노하우를 활용하면서 휘도 한계에 대한 대응을 진행하고 있습니다. 폭스콘과 폴로텍의 제휴(2025년 말까지 MicroLED 웨이퍼 라인을 시작할 계획)는 수탁 제조 기업이 OLED와 MicroLED 양진영을 동시에 다리려고 하는 자세를 보여줍니다. 이 2개 세팅 전략은 마이크로디스플레이 시장에서 비용, 휘도, 수명의 균형을 추구하는 브랜드가 이용할 수 있는 기술 툴킷의 다양화가 진행되고 있는 것을 부각하고 있습니다.

지역별 분석

아시아태평양은 2025년 매출액의 46.62%를 차지하였고, 2031년까지 연평균 복합 성장률(CAGR) 17.42%로 성장할 전망입니다. 이것은 중국 본토의 적극적인 공장 건설 및 대만의 견조한 기판 생태계에 견인되고 있습니다. 시드텍사의 12인치 OLED-on-Si 양산화와 JBD사의 누계 100만대 이상의 MicroLED 엔진 출하 실적은 이 지역 생산 규모의 우위성을 나타내고 있습니다. 마이크로디스플레이 시장은 도파로 광학계, 구동 IC, 마무리 서비스가 긴밀하게 집적되어 있는 혜택을 받아 이 지역을 설계에서 조립까지의 일괄 대응 거점으로 바꾸고 있습니다. 정부 인센티브(도시 수준 디스플레이 파크 보조금 포함)는 자본 회수 기간을 더욱 단축하고 있습니다.

북미는 중요한 시스템 통합을 담당하며 방위 조달을 주도하고 있습니다. 코핀의 미국 육군 계약은 국내 설계 노하우를 입증하고 있지만, 실제 웨이퍼 생산은 해외에서 이루어지는 경우가 많습니다. 실리콘 밸리의 공간 컴퓨팅 소프트웨어에 대한 투자로 이용 사례의 혁신은 이 지역에 정착하고 있습니다. 캐나다와 멕시코는 고급 광학 연마와 최종 조립에서 생태계를 지원하지만, 규모는 미국 수요에 비해 여전히 작습니다.

유럽의 기여는 기술적 차별화에 집중되어 있습니다. 아레디아의 그르노블 공장은 유럽을 대표하는 마이크로 LED 프로젝트로, 풀 가동 시에는 주 5,000장의 웨이퍼 생산을 약속하고 있습니다. 프라운호퍼 IPMS 연구소는 경량 AR 뷰어용 투명 OLED 마이크로디스플레이를 추진하여 산업 유지보수 및 수술 지원 시나리오를 목표로 하고 있습니다. 독일과 스웨덴의 자동차 Tier 1 공급업체는 엄격한 안전 기준을 충족하는 HUD 모듈에 대한 현지 수요를 지원합니다. 유럽은 아시아 생산량에 미치지 못하는 것, 그 연구 개발 자산 및 고급 자동차 시장에 의해 세계의 마이크로디스플레이 시장에 영향력을 유지하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트에 의한 3개월간의 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 아시아 전역에서의 AR/VR 웨어러블용 초소형 디스플레이 수요 급증

- 자동차 제조업체의 레벨 3 이상 ADAS용 투명 마이크로 LED 헤드업 디스플레이로의 이행

- 낮은 SWaP 바이저 디스플레이를 지정하는 방위 현대화 프로그램(미국 및 NATO)

- 빅텍 기업 제휴에 의한 메타버스 대응 스마트 글라스의 대두

- 미니팹 위탁 생산에 의한 소비자용 카메라용 비용 효율적인 OLED-on-Si의 실현

- 시네마틱 드론 및 마이크로 프로젝터가 하이닛츠 LCoS의 채용 견인

- 시장 성장 억제요인

- RGB 마이크로 LED의 질량 이동 공정에서 수율 손실

- 고휘도 OLED-on-Si에 있어서의 한정적인 웨이퍼 관통 방열

- 고순도 사파이어 및 실리콘 백플레인 공급망에서 병목

- 미국과 중국의 패널 제조업체 사이의 지적 재산 소송 위험

- 업계 생태계 분석

- 기술 개요

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자 및 소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 기술 유형별

- 기존(LCoS, LCD, DLP)

- OLED-on-Si

- 마이크로 LED

- 양자점 온 실리콘

- 해상도별

- 1024 x 768 미만

- 1024 x 768-1920 x 1080

- 1920 x 1080 이상

- 용도별

- 소비자용 및 자동차용

- 증강현실 및 가상현실 헤드셋

- 자동차용 헤드업 디스플레이

- 기존 용도(프로젝션 및 카메라, 기타)

- 방위

- 기타

- 소비자용 및 자동차용

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 북유럽 국가

- 기타 유럽

- 남미

- 브라질

- 기타 남미

- 아시아태평양

- 중국

- 일본

- 인도

- 동남아시아

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- GCC

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 기타 아프리카

- 중동

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Sony Semiconductor Solutions Corporation

- JBD(Jade Bird Display)

- Kopin Corporation

- Seiko Epson Corporation

- eMagin Corporation

- LG Electronics

- Himax Technologies Inc.

- BOE Technology Group Co. Ltd.

- Citizen Finedevice Co. Ltd.

- Microoled SA

- VueReal Inc.

- OLiGHTEK Opto-electronic Co. Ltd.

- Syndiant Inc.

- Raontech Co. Ltd.

- Dresden Microdisplay GmbH

- AU Optronics(AUO)

- Universal Display Corp.(UDC)

- eLux Inc.

- Mojo Vision Inc.

- OLEDWorks

제7장 시장 기회 및 장래 전망

AJY 26.01.30Microdisplay market size in 2026 is estimated at USD 2.90 billion, growing from 2025 value of USD 2.48 billion with 2031 projections showing USD 6.35 billion, growing at 16.98% CAGR over 2026-2031.

Multiple innovation cycles are converging at once: MicroLED mass-transfer yields are finally stabilizing, AR/VR ecosystems are entering a scale-up phase, and Level 3-plus driver-assistance systems are pushing transparent head-up displays from prototype to production. Manufacturing breakthroughs, notably laser-induced forward transfer (LIFT) that reaches 99.7% placement accuracy for 5 µm MicroLED chips, have removed a cost barrier that long limited wider adoption. Competitive dynamics are heating up as consumer-electronics giants join forces with specialist suppliers, compressing the time from lab demonstration to consumer launch. Sustained defense spending and automotive safety mandates add resilient end-market demand that cushions cyclical swings. Supply constraints in sapphire substrates and silicon backplanes remain the main operational risk, yet ongoing capacity additions suggest these headwinds will ease after 2026.

Global Microdisplay Market Trends and Insights

Exploding Demand for Ultra-Compact Displays in AR/VR Wearables across Asia

Rising disposable incomes and an entrenched consumer-electronics supply chain have turned East Asia into the launchpad for next-generation smart glasses. Shanghai-based JBD has shipped more than 1 million MicroLED engines since 2021 and continues to post 50% annual unit growth, validating volume potential in the region. China's SidTek moved a USD 826.3 million twelve-inch OLED-on-silicon line into pilot run during 2024, ensuring local capacity matches the surge in demand. Regional integration shrinks both logistics costs and design-cycle time, letting OEMs iterate optics, waveguides, and driver ICs faster than competitors elsewhere. As component prices slide on the back of this manufacturing density, the microdisplay market gains a broader consumer addressable base. The virtuous loop of scale, cost, and adoption positions the region to remain the growth engine of the global microdisplay market.

Automotive OEM Shift to Transparent MicroLED HUDs for Level-3+ ADAS

Automakers are racing to merge driver information with real-world scenes in the windshield. MicroLED technology delivers the luminance reserve-20 to 50 times the efficiency of legacy projector-based HUDs-needed to stay readable in direct sunlight while conserving electrical power. Demonstrations such as AUO's "Virtual Sky Canopy" cockpit, unveiled at CES 2025, prove that curved, bezel-less visual surfaces are ready for series production. Transparent HUDs also mitigate distraction, a factor in one quarter of traffic accidents, by projecting alerts at eye level. The safety argument dovetails with regulatory pushes for Level 3 autonomy, particularly in Europe, making MicroLED HUDs a future default rather than an option. As fleet roll-outs begin in premium cars from 2026 onward, the pull-through effect on the wider microdisplay market will be significant.

Yield Losses in RGB MicroLED Mass-Transfer Processes

Despite USD 12 billion sunk into development and USD 2.4 billion in acquisitions, mass-transfer yield remains the cost pivot of full-color MicroLED displays. Even sub-micron placement errors translate into visible dead pixels, forcing costly rework. Coherent's LIFT process is a vital step forward, yet scaling single-panel accuracy to the multiple million chips needed for a headset still challenges inline inspection and repair workflows. Fab expansions by Osram in Malaysia and Ennostar in Taiwan have both slipped to 2026-2027 completion windows as engineers chase yield plateaus. The next two years will therefore set the adoption tempo for consumer-grade MicroLED.

Other drivers and restraints analyzed in the detailed report include:

- Defense Modernization Programs Specifying Low-SWaP Visor Displays

- Rise of Metaverse-Ready Smart Glasses from Big-Tech Partnerships

- Limited Through-Wafer Heat Dissipation in High-Brightness OLED-on-Si

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Traditional LCoS, LCD, and DLP modules controlled 48.62% of the microdisplay market in 2025. However, MicroLED devices are set to clock a 20.85% CAGR to 2031 as transfer yields rise and power efficiency outpaces rivals. Q-Pixel demonstrated 6,800 PPI MicroLED arrays, eclipsing Apple Vision Pro's 3,380 PPI benchmark and proving room for further visual fidelity. The microdisplay market size for MicroLEDs is therefore positioned to climb rapidly once cost curves cross those of OLED-on-Si. Europe, through Aledia's USD 200 million GaN-on-silicon line, provides an alternative source that diversifies the supply base beyond Asia. Quantum-dot-on-silicon concepts, showcased by Applied Materials prototypes that exceed 90% DCI-P3, offer a hybrid path for brands prioritizing color uniformity over absolute brightness.

OLED-on-Si sits between legacy and emergent solutions, benefitting from mature evaporation know-how while tackling luminance ceilings. Foxconn's partnership with Porotech, intended to spin up a MicroLED wafer line by late 2025, signals how contract manufacturers aim to bridge OLED and MicroLED camps simultaneously. That dual-track strategy highlights the increasingly diversified technology toolkit available to brands looking to balance cost, brightness, and lifetime in the microdisplay market.

The Microdisplay Market Report is Segmented by Technology (Traditional (LCoS, LCD, DLP), OLED-On-Si, Microleds, and More), Resolution (Up To 1024 X 768, 1024 X 768 To 1920 X 1080, and Above 1920 X 1080), Application (Consumer and Automotive (Augmented Reality/Virtual Reality Headsets, and More), Defense, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific controlled 46.62% of revenue in 2025 and is on pace for a 17.42% CAGR through 2031, driven by aggressive fab construction in mainland China and robust substrate ecosystems in Taiwan. SidTek's twelve-inch OLED-on-Si ramp and JBD's cumulative million-plus MicroLED engine shipments exemplify regional volume leverage. The microdisplay market benefits from tight clustering of waveguide optics, driver IC, and finishing services, turning the region into a one-stop design-to-assembly hub. Government incentives, including city-level grants for display parks, further reduce capital payback times.

North America supplies critical system integration and dominates defense procurement. Kopin's U.S. Army contract validates domestic design know-how while actual wafer production often occurs offshore. Silicon Valley stakes in spatial-computing software ensure that use-case innovation remains anchored in the region. Canada and Mexico service the ecosystem through advanced optics polishing and final assembly, but scale remains modest relative to U.S. demand.

Europe's contribution centers on technology differentiation. Aledia's Grenoble line is Europe's flagship MicroLED project, promising 5,000 wafer starts per week when fully loaded. Fraunhofer IPMS pushes transparent OLED microdisplays for lightweight AR viewers, targeting industrial maintenance and surgical-assistance scenarios. Automotive tier-ones across Germany and Sweden also feed local demand for HUD modules that meet stringent safety standards. Although Europe cannot match Asia's volume, its R&D assets and premium automotive market keep it influential within the global microdisplay market.

- Sony Semiconductor Solutions Corporation

- JBD (Jade Bird Display)

- Kopin Corporation

- Seiko Epson Corporation

- eMagin Corporation

- LG Electronics

- Himax Technologies Inc.

- BOE Technology Group Co. Ltd.

- Citizen Finedevice Co. Ltd.

- Microoled SA

- VueReal Inc.

- OLiGHTEK Opto-electronic Co. Ltd.

- Syndiant Inc.

- Raontech Co. Ltd.

- Dresden Microdisplay GmbH

- AU Optronics (AUO)

- Universal Display Corp. (UDC)

- eLux Inc.

- Mojo Vision Inc.

- OLEDWorks

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Exploding Demand for Ultra-Compact Displays in AR/VR Wearables across Asia

- 4.2.2 Automotive OEM Shift to Transparent Micro-LED HUDs for Level-3+ ADAS

- 4.2.3 Defense Modernization Programs Specifying Low-SWaP Visor Displays (United States and NATO)

- 4.2.4 Rise of Metaverse-Ready Smart Glasses from Big-Tech Partnerships

- 4.2.5 Mini-Fab Outsourcing Enabling Cost-Effective OLED-on-Si for Consumer Cameras

- 4.2.6 Cinematic Drones and Micro-Projectors Driving High-Nits LCoS Adoption

- 4.3 Market Restraints

- 4.3.1 Yield Losses in RGB Micro-LED Mass-Transfer Processes

- 4.3.2 Limited Through-Wafer Heat Dissipation in High-Brightness OLED-on-Si

- 4.3.3 Supply-Chain Bottlenecks for High-Purity Sapphire and Silicon Backplanes

- 4.3.4 IP Litigation Risk among United States and Chinese Panel Makers

- 4.4 Industry Ecosystem Analysis

- 4.5 Technology Snapshot

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Type of Technology

- 5.1.1 Traditional (LCoS, LCD, DLP)

- 5.1.2 OLED-on-Si

- 5.1.3 MicroLEDs

- 5.1.4 Quantum-Dot-on-Si

- 5.2 By Resolution

- 5.2.1 Up to 1024 x 768

- 5.2.2 1024 x 768 to 1920 x 1080

- 5.2.3 Above 1920 x 1080

- 5.3 By Application

- 5.3.1 Consumer and Automotive

- 5.3.1.1 Augmented Reality/Virtual Reality Headsets

- 5.3.1.2 Automotive HUDs

- 5.3.1.3 Traditional Applications (Projection/Camera, Others)

- 5.3.2 Defense

- 5.3.3 Others

- 5.3.1 Consumer and Automotive

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Nordics

- 5.4.2.5 Rest of Europe

- 5.4.3 South America

- 5.4.3.1 Brazil

- 5.4.3.2 Rest of South America

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 South-East Asia

- 5.4.4.5 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 Gulf Cooperation Council Countries

- 5.4.5.1.2 Turkey

- 5.4.5.1.3 Rest of Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Rest of Africa

- 5.4.5.1 Middle East

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Sony Semiconductor Solutions Corporation

- 6.4.2 JBD (Jade Bird Display)

- 6.4.3 Kopin Corporation

- 6.4.4 Seiko Epson Corporation

- 6.4.5 eMagin Corporation

- 6.4.6 LG Electronics

- 6.4.7 Himax Technologies Inc.

- 6.4.8 BOE Technology Group Co. Ltd.

- 6.4.9 Citizen Finedevice Co. Ltd.

- 6.4.10 Microoled SA

- 6.4.11 VueReal Inc.

- 6.4.12 OLiGHTEK Opto-electronic Co. Ltd.

- 6.4.13 Syndiant Inc.

- 6.4.14 Raontech Co. Ltd.

- 6.4.15 Dresden Microdisplay GmbH

- 6.4.16 AU Optronics (AUO)

- 6.4.17 Universal Display Corp. (UDC)

- 6.4.18 eLux Inc.

- 6.4.19 Mojo Vision Inc.

- 6.4.20 OLEDWorks

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment