|

시장보고서

상품코드

1549891

산업 자동화 - 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2024-2029년)Industrial Automation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

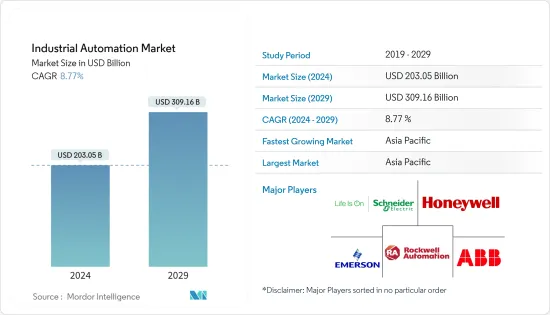

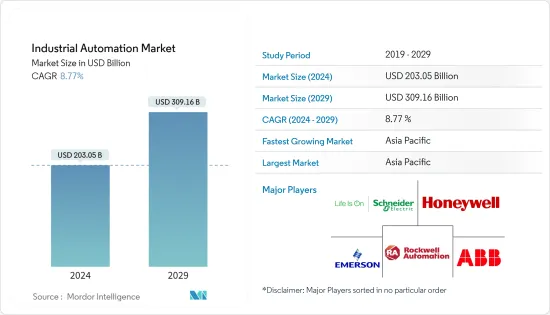

세계 산업 자동화 시장 규모는 2024년 2,030억 5,000만 달러로 추정되며, 2029년에는 3,091억 6,000만 달러에 달할 것으로 예상되며, 예측 기간(2024-2029년) 동안 CAGR 8.77%로 성장할 것으로 예상됩니다.

주요 하이라이트

- 산업 자동화는 개발도상국의 수출 경쟁력을 높일 수 있습니다. 제조 공정을 자동화함으로써 이들 국가는 더 빠르고, 효과적이고, 저렴하게 상품을 생산할 수 있어 세계 시장에서 경쟁력을 높일 수 있습니다. 그 결과 수출 수준이 향상되고 외화 수입이 개선되고 신흥국 경제가 개선될 수 있기 때문에 신흥 경제국의 산업 자동화 시장이 활성화될 수 있습니다.

- 산업 자동화는 개발도상국의 중소기업에 큰 영향을 미칩니다. 자동화는 이러한 기업의 경쟁력을 높이고 지속가능한 성장을 달성 할 수 있습니다. 중소기업이 생산성을 높이고 운영을 간소화하며 대규모 고객 및 공급망의 요구를 충족시킬 수 있습니다. 예를 들어, 산업 자동화는 자원을 최적화하고 생산 시간을 단축하여 인력을 전략적 업무에 투입할 수 있습니다. 국제로봇연맹(IFR)에 따르면, 제조업에서 여러 공정을 자동화하면 생산성이 최대 30%까지 향상될 수 있다고 합니다.

- 국제통화기금(IMF)에 따르면, 신흥시장 및 신흥경제국의 성장률은 2023년 4.3%, 2024년과 2025년 4.2%로 예상됩니다. 인도와 같은 많은 신흥국에서는 인도 정부의 스크랩 정책, 자동차 미션 플랜 2026, 생산 연동형 인센티브 제도와 같은 몇 가지 이니셔티브가 인도를 이륜차 및 사륜차 시장의 중요한 플레이어로 만들 것으로 예상됩니다. 이러한 정책에는 자동화 기술을 채택하고 시장 조사에 유리한 환경을 조성하는 것이 포함됩니다.

- 자동화 설비는 스마트 제조를 위한 고가의 설비 투자를 요구한다(자동화 시스템 설치, 설계 및 제작에 수백만 달러가 소요될 수 있습니다). 로봇 시스템, 컨베이어 벨트, 센서, 제어 시스템 등 장비 구매 비용이 상당합니다. 공장 자동화 장비는 또한 기존 생산 시스템에 대한 사용자 정의 및 통합이 필요합니다. 이 프로세스에는 특정 제조 요구 사항을 충족하기 위한 장비 설계, 엔지니어링 및 프로그래밍이 포함됩니다. 이는 조사 대상 시장의 성장에 큰 걸림돌이 될 수 있습니다.

- 산업 자동화 솔루션의 공급망과 생산에 직접적으로 영향을 미치는 것 외에도, 팬데믹의 후유증은 조사 대상 시장의 성장에 영향을 미치고 있습니다. 예를 들어, 북미를 포함한 여러 지역에 닥쳐오고 있는 경기 침체의 위협은 소비자와 기업이 불확실한 경제 상황으로 인해 자동차 등 고가 제품이나 확장 프로젝트에 대한 지출을 늘리지 못하게함으로써 시장 성장에 부정적인 영향을 미칠 수 있습니다.

산업 자동화 시장 동향

석유 및 가스 산업은 괄목할 만한 성장 전망

- 석유 및 가스 산업은 산업 자동화 솔루션 도입에 있어 압도적인 비중을 차지하고 있습니다. 그러나 이 산업에서 산업 자동화의 성장 전망은 다른 개발도상국 산업에 비해 제한적이기 때문에 이 산업의 성장률은 둔화될 것으로 예상됩니다.

- 석유 및 가스 자동화(유전 자동화라고도 함)는 세계 시장에서 에너지 생산자의 경쟁력을 강화하기 위해 디지털 기술을 활용하는 일련의 프로세스입니다. 산업 내 특정 부문은 자동화를 더욱 촉진하는 반면, 주요 분야에는 시추, 생산 작업, 물류, 안전, 소매업 등이 포함됩니다. 석유 및 가스 자동화는 주로 IoT 기반 센서, 예측 시스템, AI 기반 전문가 시스템에 의존하여 생산성을 높이고 노동력 부족으로 인한 기술 격차를 해소할 수 있습니다.

- 석유 및 가스 산업의 위험한 환경은 자동화를 통해 점점 더 개선되고 있습니다. 로봇과 자동화 시스템이 시추, 검사, 유지보수 등의 작업을 처리하여 인간이 위험에 노출될 기회를 크게 줄였습니다.

- 산업계는 비상 정지 시스템과 같은 자동화 기능을 통해 안전을 강화하고 어려운 상황에 신속하게 대응할 수 있도록 보장하고 있습니다. 센서와 자동화 도구를 도입함으로써 기업은 규제 준수를 보장하고 환경에 미치는 영향을 억제할 수 있습니다.

- 석유 및 가스 산업은 세계 경제의 중요한 구성요소입니다. IEA에 따르면 2024년 세계 액체 연료 생산량은 OPEC의 자발적 감산이 비 OPEC 공급 증가로 인해 OPEC의 자발적 감산이 OPEC 이외의 공급 증가로 인해 2023년의 180 만 b/d 증가에서 둔화되어 80 만 b/d 이상 증가할 것이라고 IEA는 예측했습니다. OPEC의 원유 생산량은 전년 대비 90만 b/d 감소할 것으로 예상되지만, 비OPEC 생산량은 미국, 가이아나, 브라질, 캐나다가 주도하여 180만 b/d 증가할 것으로 예상됩니다. 석유 생산량이 크게 증가하고 디지털화가 진행됨에 따라 석유 및 가스 기업들은 디지털 기술과 자동화에 대한 의존도를 높이고 있습니다.

아시아태평양이 가장 빠른 성장세를 기록할 것으로 예상

- 아시아태평양에는 중국, 일본, 한국, 대만 등 세계 최대의 제조업 경제권이 있습니다. 자동차, 전자, 항공우주, 의료기기 등의 제조업이 지속적으로 확대되면서 산업 자동화에 대한 수요가 크게 증가하고 있습니다.

- 인도와 같은 신흥국의 제조업 확대와 자립을 위한 노력은 시장 성장을 더욱 촉진하고 있습니다. 인도에서는 제조업이 고성장 분야 중 하나로 부상하고 있습니다. IBEF에 따르면, 인도는 2030년까지 1조 달러 상당의 상품을 수출할 수 있는 잠재력을 가지고 있으며, 세계 제조 허브로서 인도를 세계 지도에 올려놓는 '메이크 인 인디아' 프로그램을 통해 인도 경제를 세계적으로 인정받고 있습니다.

- 인도 정부는 2025년까지 5조 달러 규모의 경제 규모를 목표로 하고 있으며, 그 중 제조업은 1조 달러의 가치를 지닙니다. 이 목표를 달성하기 위해서는 Make in India, Skill India, Digital India와 같은 플래그십 프로그램의 통합이 필수적이며, 이를 통해 이 지역의 시장 성장을 촉진할 수 있습니다.

- 전기자동차 보급을 앞당기기 위해 배터리 제조 공장 건설 계획이 진행 중인 것도 시장 성장에 힘을 보태고 있습니다. 예를 들어, 리차지 인더스트리즈(Recharge Industries)는 2023년 8월, 연간 30만 대의 전기자동차에 배터리를 공급할 수 있는 30기가와트시 규모의 공장 건설 계획을 발표했으며, 2024년 5월경 착공해 2025년 생산에 들어갈 예정입니다.

- 이 지역은 대만 반도체 제조회사(Taiwan Semiconductor Manufacturing Company)와 같은 기업의 존재로 인해 가장 큰 반도체 및 전자제품 제조업체가 되었습니다. 대만은 전 세계 반도체의 60% 이상, 최첨단 반도체의 90% 이상을 생산하고 있습니다. 대부분의 반도체는 TSMC가 생산하고 있습니다.

산업 자동화 산업 개요

산업 자동화 시장은 중소기업과 세계 기업이 존재하기 때문에 매우 세분화되어 있습니다. 이 시장의 주요 기업으로는 슈나이더 일렉트릭 SE, 로크웰 오토메이션, 하니웰 인터내셔널, 에머슨 일렉트릭, ABB 리미티드 등이 있습니다. 시장의 주요 기업들은 제품 라인업을 강화하고 지속가능한 경쟁 우위를 확보하기 위해 인수 및 파트너십과 같은 전략을 채택하고 있습니다.

- 2024년 6월 - 로크웰 오토메이션은 보다 안전하고 스마트한 산업용 AI 모바일 로봇 개발을 촉진하기 위해 엔비디아와의 제휴를 발표했습니다. 이번 제휴는 자율 이동 로봇(AMR)의 AI 활용을 촉진하고 성능과 효율성을 향상시킬 것으로 기대됩니다.

- 2024년 2월 - 슈나이더일렉트릭은 기술 선도 기업인 인텔 및 레드햇과 협력하여 새로운 소프트웨어 프레임워크인 분산 제어 노드(DCN)를 발표했습니다. 슈나이더일렉트릭의 에코스트럭처 오토메이션 엑스퍼트(EcoStruxure Automation Expert)를 기반으로 구축된 이 혁신적인 프레임워크는 산업 기업들이 소프트웨어 정의 플러그 앤 플레이 모델로 전환할 수 있도록 지원합니다. 이러한 전환은 업무 효율성과 품질을 향상시키고 프로세스를 간소화하여 궁극적으로 비용을 절감할 수 있도록 돕습니다.

기타 혜택

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 소개

- 조사 가정과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 기술 동향/진보

- 업계의 매력 - Porter's Five Forces 분석

- 공급 기업의 교섭력

- 구매자의 교섭력

- 신규 참여업체의 위협

- 대체품의 위협

- 경쟁 정도

- 업계 밸류체인 분석

- 시장 거시적 동향 분석

제5장 시장 역학

- 시장 성장 촉진요인

- 신흥 경제 국가의 산업 활동 성장

- 에너지 효율과 비용 절감에 대한 관심 상승

- 시장 억제요인

- 높은 설치 및 재구축 비용

제6장 시장 세분화

- 솔루션별

- 산업용 제어 시스템

- 분산형 제어 시스템(DCS)

- 감시제어·데이터 수집(SCADA)

- 프로그래머블 로직 컨트롤러(PLC)

- 휴먼 머신 인터페이스(HMI)

- 기타 제어 시스템

- 필드 기기

- 센서와 트랜스미터

- 밸브와 액추에이터

- 모터 및 드라이브

- 로봇

- 기타 필드 기기

- 소프트웨어

- 제품 수명주기 관리(PLM)

- 전사적 자원 관리(ERP)

- 제조 실행 시스템(MES)

- 기타 소프트웨어

- 산업용 제어 시스템

- 최종 이용 산업별

- 석유 및 가스

- 제약

- 자동차·운송

- 식품 및 음료

- 전력·유틸리티

- 화학·석유화학

- 기타 최종 이용 산업

- 지역별

- 북미

- 유럽

- 아시아

- 호주·뉴질랜드

- 라틴아메리카

- 중동 및 아프리카

제7장 경쟁 상황

- 기업 개요

- Schneider Electric SE

- Rockwell Automation Inc.

- Honeywell International Inc.

- Emerson Electric Co.

- ABB Limited

- Mitsubishi Electric Corporation

- Siemens AG

- Omron Corporation

- Yokogawa Electric Corporation

- Yaskawa Electric Corporation

- Kuka Aktiengesellschaft

- Fanuc Corporation

- Regal Rexnord Corporation

- Nidec Corporation

- Basler AG

제8장 투자 분석

제9장 시장 전망

ksm 24.09.26The Industrial Automation Market size is estimated at USD 203.05 billion in 2024, and is expected to reach USD 309.16 billion by 2029, growing at a CAGR of 8.77% during the forecast period (2024-2029).

Key Highlights

- Industrial automation may potentially and considerably increase export competitiveness in developing nations. By automating their manufacturing processes, these nations can create items more quickly, effectively, and affordably, which boosts their ability to compete in the global market. This may result in higher levels of exports, better foreign currency revenues, and an improvement in the emerging economy, hence driving the market for industrial automation in developing countries.

- Industrial automation significantly impacts small and medium-sized firms (SMEs) in developing nations. Automation may boost these companies' competitiveness and achieve sustained growth. It enables SMEs to improve productivity, streamline operations, and satisfy the needs of larger customers and supply chains. For instance, Industrial automation optimizes resources and reduces production times, freeing personnel for strategic tasks. According to the International Federation of Robotics (IFR), productivity increases by up to 30% in manufacturing with automation in multiple processes.

- According to the International Monetary Fund (IMF), growth rates for emerging markets and developing economies are projected to be 4.2% in 2024 and 2025 compared to 4.3% in 2023. In many developing countries such as India, several initiatives by the Government of India, like the scrappage policy, Automotive Mission Plan 2026, and production-linked incentive scheme in the Indian market, are expected to make India a significant player in the two-wheeler and four-wheeler market. Such policies include adopting automation technologies and fostering a favorable environment for the market studied.

- Automation equipment mandates high capital investment to fund smart manufacturing (an automated system may cost millions of dollars to install, design, and fabricate). The cost of purchasing the equipment, including robotic systems, conveyor belts, sensors, and control systems, can be substantial. The factory automation equipment also necessitates the customization and integration into existing production systems. This process involves designing, engineering, and programming the equipment to meet specific manufacturing requirements. This poses a significant hindrance to the growth of the market studied.

- Apart from the direct impact evident in the supply chains and production of industrial automation solutions, the aftereffects of the pandemic are also impacting the growth of the studied market. For instance, the ongoing threat of recession looming over various regions, including North America, may negatively influence the studied market's growth as the economic uncertainty will prevent consumers and businesses from spending more on high-value products such as automobiles and expansion projects, which may impact the growth of the market studied.

Industrial Automation Market Trends

Oil and Gas Industry to Witness Significant Growth

- The oil and gas industry has been a dominating segment in adopting industrial automation solutions. However, the growth prospects for industrial automation in this industry are limited compared to other developing industries, and therefore, the growth rate is expected to slow in this industry.

- Oil and gas automation, also known as oilfield automation, is a set of processes, many leveraging digital technologies, aimed at enhancing the competitiveness of energy producers in global markets. While certain sectors within the industry are more primed for automation, key areas include drilling, production operations, logistics, safety, and retail operations. Oil and gas automation predominantly relies on IoT-based sensors, predictive systems, and AI-driven expert systems to boost productivity and bridge skill gaps arising from labor shortages.

- The oil and gas industry's hazardous environments are increasingly being navigated through automation. Robots and automated systems handle tasks like drilling, inspection, and maintenance, significantly reducing human exposure to risks.

- The industry is bolstering safety with automated features like emergency shutdown systems, guaranteeing swift responses to difficult situations. By deploying sensors and automated tools, companies are ensuring compliance with regulations and curbing their environmental footprint.

- The oil and gas industry is a vital component of the global economy. As per IEA, global production of liquid fuels will increase by more than 0.8 million b/d in 2024, slowing from the 1.8 million b/d increase in 2023, as OPEC+ voluntary production cuts are offset by supply growth outside of OPEC+. Although OPEC+ crude oil production in 2024 decreases by 0.9 million b/d compared with last year, forecast production outside of OPEC+ increased by 1.8 million b/d, led by the United States, Guyana, Brazil, and Canada. With significant surge in oil production and surging digitization, oil and gas companies have increasingly relied on digital technology and automation.

Asia-Pacific is Expected to Register the Fastest Growth

- Asia-Pacific is home to some of the world's largest manufacturing economies, including China, Japan, South Korea, and Taiwan. The ongoing expansion of manufacturing industries in automotive, electronics, aerospace, and medical devices creates a significant demand for industrial automation.

- Initiatives by emerging countries like India to expand their manufacturing footprint and become self-reliant further propel the market growth. Manufacturing emerged as one of the high-growth sectors in India. The 'Make in India' program places India on the global map as a manufacturing hub and globally recognizes the Indian economy. According to IBEF, India can export goods worth USD 1 trillion by 2030 and is on the road to becoming a significant global manufacturing hub.

- The government of India aims for a USD 5 trillion economy by 2025, of which manufacturing would be worth USD 1 trillion. The convergence of flagship programs, such as Make in India with Skill India and Digital India, would be vital to achieving this goal, thereby driving the region's market growth.

- The ongoing initiatives to build a battery manufacturing plant for faster adoption of electric vehicles are further driving the market growth. For instance, in August 2023, Recharge Industries announced its plans to build a factory with an annual capacity of 30 gigawatt-hours to supply batteries for roughly 300,000 EVs. Construction is expected to begin around May 2024, with production slated to start in 2025.

- The region is the biggest semiconductor and electronics product manufacturer due to the presence of companies like Taiwan Semiconductor Manufacturing Company. Taiwan produces over 60% of the world's semiconductors and over 90% of the most advanced ones. Most of the semiconductors are manufactured by TSMC.

Industrial Automation Industry Overview

The industrial automation market is highly fragmented due to the presence of small and medium-sized enterprises and global players. Some of the major players in the market are Schneider Electric SE, Rockwell Automation Inc., Honeywell International Inc., Emerson Electric Co., and ABB Limited. Key players in the market are adopting strategies such as acquisitions and partnerships to enhance their product offerings and gain sustainable competitive advantage.

- June 2024 - Rockwell Automation announced a partnership with NVIDIA to expedite the development of safer and smarter industrial AI mobile robots. The collaboration is anticipated to drive the use of AI in autonomous mobile robots (AMRs), improving their performance and efficiency.

- February 2024 - Schneider Electric, in partnership with tech giants Intel and Red Hat, unveiled a new software framework, the Distributed Control Node (DCN). Building upon Schneider Electric's EcoStruxure Automation Expert, this innovative framework empowers industrial firms to transition to a software-defined, plug-and-play model. This shift boosts operational efficiency and quality and streamlines processes, ultimately leading to cost savings.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Technological Trends/Advancements

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Degree of Competition

- 4.4 Industry Value Chain Analysis

- 4.5 Analysis of the Macro Trends on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growth of Industrial Activities in Developing Economies

- 5.1.2 Growing Emphasis on Energy Efficiency and Cost Reduction

- 5.2 Market Restrains

- 5.2.1 High Cost of Installation and Re-building

6 MARKET SEGMENTATION

- 6.1 By Solution

- 6.1.1 Industrial Control Systems

- 6.1.1.1 Distributed Control System (DCS)

- 6.1.1.2 Supervisory Control and Data Acquisition (SCADA)

- 6.1.1.3 Programmable Logic Controller (PLC)

- 6.1.1.4 Human-machine Interface (HMI)

- 6.1.1.5 Other Control Systems

- 6.1.2 Field Devices

- 6.1.2.1 Sensors and Transmitters

- 6.1.2.2 Valves and Actuators

- 6.1.2.3 Motors and Drives

- 6.1.2.4 Robotics

- 6.1.2.5 Other Field Devices

- 6.1.3 Software

- 6.1.3.1 Product Lifecycle Management (PLM)

- 6.1.3.2 Enterprise Resource and Planning (ERP)

- 6.1.3.3 Manufacturing Execution System (MES)

- 6.1.3.4 Other Software

- 6.1.1 Industrial Control Systems

- 6.2 By End-user Industry

- 6.2.1 Oil and Gas

- 6.2.2 Pharmaceuticals

- 6.2.3 Automotive and Transportation

- 6.2.4 Food and Beverage

- 6.2.5 Power and Utilities

- 6.2.6 Chemical and Petrochemical

- 6.2.7 Other End-user Industries

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Schneider Electric SE

- 7.1.2 Rockwell Automation Inc.

- 7.1.3 Honeywell International Inc.

- 7.1.4 Emerson Electric Co.

- 7.1.5 ABB Limited

- 7.1.6 Mitsubishi Electric Corporation

- 7.1.7 Siemens AG

- 7.1.8 Omron Corporation

- 7.1.9 Yokogawa Electric Corporation

- 7.1.10 Yaskawa Electric Corporation

- 7.1.11 Kuka Aktiengesellschaft

- 7.1.12 Fanuc Corporation

- 7.1.13 Regal Rexnord Corporation

- 7.1.14 Nidec Corporation

- 7.1.15 Basler AG