|

시장보고서

상품코드

1550033

고전압 필름 커패시터 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2024-2029년)High Voltage Film Capacitor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

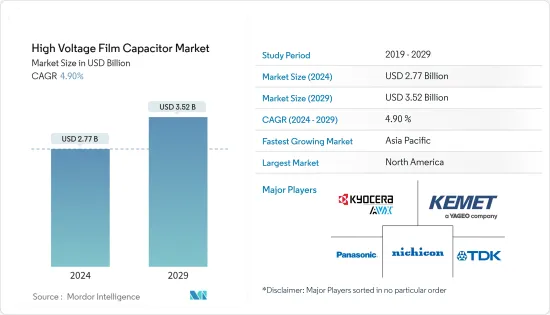

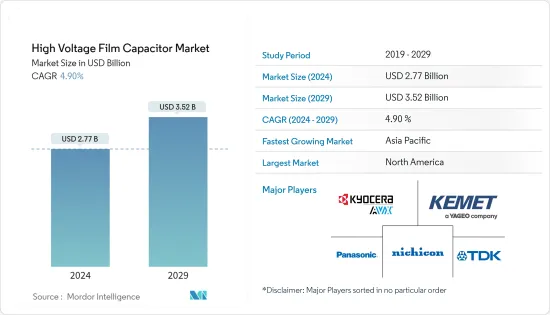

고전압 필름 커패시터 시장 규모는 2024년 27억 7,000만 달러로 추정 및 예측되며, 2029년에는 35억 2,000만 달러에 달할 것으로 예상되며, 예측 기간(2024-2029) 동안 4.90%의 CAGR로 성장할 것으로 예상됩니다.

고전압 필름 커패시터 시장은 효율적인 에너지 저장 및 변환 시스템을 필요로 하는 풍력 및 태양광발전과 같은 재생에너지의 채택이 증가함에 따라 성장세를 보이고 있습니다. 고전압 필름 커패시터는 안정성, 긴 수명 및 고전압 내성으로 인해 이러한 시스템에서 매우 중요합니다. 또한, 전기자동차, 송배전 수요 및 커패시터 기술의 지속적인 발전도 시장 성장을 촉진하는 요인 중 하나입니다.

주요 하이라이트

- 고전압 필름 커패시터는 고전압 수준에서 전기 에너지를 저장하고 방출하는 전기 부품입니다. 얇은 플라스틱 필름을 유전체 재료로 사용하고 금속 전극으로 끼워 넣은 구조로 되어 있습니다. 고전압 필름 커패시터는 절연 저항이 높고 안정성이 뛰어나며 고전압 응용 분야에서도 성능 저하가 적은 것으로 알려져 있습니다.

- 고전압 필름 커패시터는 고성능, 내구성 및 가혹한 조건에 대한 높은 내성으로 인해 광범위한 고전압 및 고전력 애플리케이션에 필수적인 커패시터로 선호되고 있습니다.

- 고전압 필름 커패시터는 부분적인 절연 파괴로부터 회복할 수 있는 자기 회복 특성으로 유명합니다. 금속 화 필름 커패시터에서 절연 파괴가 발생하면 절연 파괴 주변의 얇은 금속 층이 증발하여 고장을 격리하고 커패시터의 기능을 계속 유지합니다.

- 전력망의 현대화와 고전압 직류(HVDC) 송전 시스템의 확대로 인해 장거리 송전의 효율성과 신뢰성을 향상시키는 데 도움이 되는 이러한 커패시터에 대한 수요가 증가하고 있으며, 국제에너지기구(IEA)에 따르면 2012년부터 2040년까지 전 세계 전력 수요는 거의 80% 증가할 것으로 예상됩니다. 탄력성 향상을 위한 전력 인프라의 확장, 현대화, 디지털화, 분산화 및 세계경제포럼(WEF)과 같은 조직의 계획된 투자(향후 25년간 스마트 그리드에 7조 6,000억 달러 할당)로 인해 세계 시나리오의 다양한 시장 역학이 변화할 것으로 예상됩니다. 변화할 것으로 예상됩니다.

- 또한, 전 세계 전력회사들이 인공지능 및 디지털 트윈과 같은 기술을 채택하고 있으며, 이는 정부의 지원과 이니셔티브의 증가와 함께 스마트 그리드 프로젝트에 대한 투자를 더욱 끌어들이고 있습니다. 예를 들어, 미국 에너지부는 2024년 1월 전력망 현대화, 송전선로 지중화, 노후화된 인프라를 갱신하기 위한 기술 개발에 3,400만 달러의 보조금을 지원한다고 발표했습니다. 이 프로그램은 극한의 날씨로 인한 혼란을 최소화하고, 비용을 절감하며, 재생에너지의 채택을 가속화함으로써 전력망 인프라를 현대화하고 강화하는 솔루션을 촉진하는 것을 목표로 합니다.

- 공급망 혼란, 에너지 가격, 제재, 무역 제한, 인플레이션 상승과 같은 거시경제적 요인에 더해 러시아-우크라이나 전쟁은 고전압 필름 커패시터 시장에 어려운 환경을 조성하고 있습니다. 혼란과 비용 상승이 큰 도전이 되고 있지만, 재생에너지와 전기자동차의 추진이 지속적으로 수요를 견인하고 있어 부정적인 요인을 어느 정도 상쇄하고 있습니다.

고전압 필름 커패시터 시장 동향

자동차 부문, 큰 폭의 성장률 기록할 전망

- 고전압 필름 커패시터는 자동차 산업, 특히 전기자동차, 하이브리드 전기자동차 및 첨단 내연 기관 자동차에서 중요한 역할을 합니다. 이 커패시터는 자동차의 전기 에너지 흐름과 변환을 관리하는 전력 전자 시스템에 필수적입니다.

- EV 및 HEV에서 배터리 관리 시스템은 고전압 필름 커패시터를 사용하여 전압을 안정화하여 배터리의 충전 및 방전 주기를 관리합니다. 이를 통해 배터리 팩의 최적의 성능과 수명을 보장합니다.

- 또한 ABS 및 ADAS를 채택하려는 노력이 증가하면서 이 부문의 성장을 더욱 촉진하고 있습니다. 자동차에 ADAS 기능이 탑재되고 고도화될수록 전력 수요는 증가합니다. 고전압 필름 커패시터는 이러한 전력 수요를 관리하고 ADAS 기능을 구현하는 센서와 프로세서에 안정적이고 신뢰할 수 있는 전력을 공급합니다.

- 인도 정부는 다양한 규제와 정책을 통해 ADAS 도입을 적극적으로 추진하고 있습니다. 세계적인 추세를 반영하여 신차에 특정 ADAS 기능을 의무화하려는 움직임이 예상됩니다. 이러한 규제 강화로 인해 이러한 기술의 보급이 가속화될 가능성이 높습니다.

- 또한, Automotive Industry Standard 145는 인도에서 판매되는 모든 자동차에 에어백, SBR, ABS, SWS 장착을 의무화하고 있습니다. 최근 도입된 AIS 197: BNCAP(Bharat New Car Assessment Program)은 보다 엄격한 충돌 테스트 기준을 규정하고 있으며, ADAS가 필수 요건이 될 수 있는 토대를 마련함으로써 패시브 및 액티브 세이프티 도입을 촉진할 것으로 기대됩니다.

아시아태평양은 큰 폭의 시장 성장이 예상

- 산업 확장, 재생에너지 프로젝트, 교통의 전기화, 가전제품의 성장, 스마트 그리드 개발, 기술 발전, 정부 지원 정책, 에너지 수요 증가는 아시아태평양의 고전압 필름 커패시터의 성장을 촉진하고 있습니다.

- 중국은 지난 몇 년 동안 세계 최대 자동차 시장 중 하나이며, 자동차 기술 강국이 되고 있습니다. 중국은 기술 발전에 개방적이기 때문에 향후 몇 년 동안 자동차 산업에 큰 영향을 미칠 수 있습니다. 또한, 인더스트리 4.0의 도래와 함께 "메이드 인 차이나 2025"와 같은 계획으로 중국은 자동화 및 산업 분야에서 대규모 성장을 이룰 것으로 예상됩니다.

- 또한 올해 1월에는 중국의 BYD가 테슬라를 제치고 세계 최대 순수 전기자동차 제조업체로 부상했습니다. 이러한 급격한 증가는 판매되는 자동차의 40%가 전기자동차인 중국의 전기자동차 수요 증가에 힘입은 것입니다. 이러한 전기자동차로의 전환과 아시아태평양의 전기 대중교통 시스템 개발이 고전압 필름 커패시터 수요를 견인하고 있습니다.

- 인도에서는 가전 및 통신 산업도 괄목할만한 성장세를 보이고 있습니다. ICEA에 따르면 인도는 2025년까지 노트북과 태블릿PC 제조 분야에서 1,000억 달러의 가치를 달성할 수 있을 것으로 예상되며, 인도 가전 및 통신 산업은 고전압 필름 커패시터 시장 개척에 유리한 시장 시나리오를 창출할 것으로 예상됩니다. 또한 IBEF에 따르면 인도의 가전 및 가전제품 산업은 2배 이상 증가한 211억 8,000만 달러 규모에 달할 것으로 예상됩니다.

- 또한 인도의 통신 타워 산업은 지난 7년간 65%의 큰 폭의 성장을 이루었으며, 2021-2022년 6억 6,800만 달러, 2022-2023년 6억 9,400만 달러의 통신 부문 직접투자가 이루어졌습니다.

고전압 필름 커패시터 산업 개요

고전압 필름 커패시터 시장은 경쟁이 치열하고 다양한 규모의 업체들이 존재하고 있습니다. 각 기업이 현재의 경기 둔화를 상쇄하기 위해 전략적 투자를 계속하고 있기 때문에 시장은 많은 제휴, 합병 및 인수 합병을 겪을 것으로 예상됩니다. 시장에 진출한 주요 기업으로는 TDK Corporation, KYOCERA AVX, Kemet Corporation, Vishay Intertechnology 등이 있습니다.

- 2024년 4월 교세라 AVX는 두 가지 새로운 스냅인 알루미늄 전해 커패시터 시리즈인 SNA 시리즈와 SNL 시리즈를 출시하여 고신뢰성, 고내압, 고CV 성능, 긴 수명을 실현했습니다. 또한 두 시리즈 모두 무연 및 RoHS 지침을 준수하며, -25℃-105℃의 온도 범위에서 사용할 수 있어 주파수 컨버터, 태양광 인버터, 전력 인버터, 축전 시스템, 전원 공급 장치 등 상업용 및 산업용 애플리케이션에 사용하기에 적합합니다.

- 2024년 4월 KEMET Corporation은 R41P를 출시할 것이라고 발표했는데, R41P는 Y2/X1 필름 커패시터로 소형 사이즈(R41T보다 40% 더 작음)로 공간 요구 사항과 비용이 우선시되는 응용 분야에서 특히 우수합니다. 따라서 THB 값이 낮고 고온에서의 사용 수명이 짧습니다. 이 커패시터 시리즈는 안전 등급 Y2/X1이 요구되는 '라인-투-그라운드' 및 '오버-더-라인' 애플리케이션에서 전자기 간섭(EMI) 억제 필터에 적합합니다.

기타 혜택:

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 소개

- 조사 상정과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 업계의 매력 - Porter's Five Forces 분석

- 신규 참여업체의 위협

- 구매자/소비자의 협상력

- 공급 기업의 교섭력

- 대체품의 위협

- 경쟁 기업 간의 경쟁 강도

- 산업 밸류체인 분석

- COVID-19의 부작용과 기타 거시경제 요인이 시장에 미치는 영향

제5장 시장 역학

- 시장 성장 촉진요인

- 전기자동차 수요 증가

- 스마트 그리드 수요 증가

- 에너지 효율적 기술에 대한 수요 증가

- 시장 성장 억제요인

- 원재료 입수가 어려움

- 높은 생산 비용

제6장 권선 유형과 적층 유형 분석

제7장 시장 세분화

- 최종 이용 산업별

- 자동차

- 항공우주 및 방위

- 석유 및 가스

- 드라이브와 인버터(비자동차)

- 기타 최종 이용 산업

- 지역별

- 북미

- 유럽

- 아시아태평양

- 호주·뉴질랜드

- 라틴아메리카

- 중동 및 아프리카

제8장 경쟁 상황

- 기업 개요

- TDK Corporation

- KYOCERA AVX Components Corporation

- Nichicon Corporation

- Kemet Corporation

- Panasonic Industry Co. Ltd

- Vishay Intertechnology nc.

- WIMA GmbH & Co. KG

제9장 시장 전망

ksm 24.09.13The High Voltage Film Capacitor Market size is estimated at USD 2.77 billion in 2024, and is expected to reach USD 3.52 billion by 2029, growing at a CAGR of 4.90% during the forecast period (2024-2029).

The market for high-voltage film capacitors is witnessing growth due to the increasing adoption of renewable energy sources, such as wind and solar power, which require efficient energy storage and conversion systems. High-voltage film capacitors are crucial in these systems for their stability, long lifespan, and high voltage tolerance. Additionally, the demand for electric vehicles, power transmission and distribution, and the continuous improvements in capacitor technology are some of the factors that are driving market growth.

Key Highlights

- High-voltage film capacitors are electrical components that store and release electrical energy at high voltage levels. They are constructed using thin plastic films as the dielectric material sandwiched between metal electrodes. These capacitors are known for their high insulation resistance, stability, and ability to handle high-voltage applications without significant performance degradation.

- High-voltage film capacitors are favored for their high performance, durability, and ability to withstand harsh conditions, making them indispensable in a wide range of high-voltage and high-power applications.

- High-voltage film capacitors are known for their self-healing properties, which allow them to recover from partial dielectric breakdown. In metalized film capacitors, when a dielectric breakdown occurs, the thin metal layer around the breakdown evaporates, isolating the fault and allowing the capacitor to continue functioning.

- The increasing modernization of power grids and the expansion of high-voltage direct current (HVDC) transmission systems are driving the demand for these capacitors, as they help improve the efficiency and reliability of power transmission over long distances. According to the IEA (International Energy Agency), the world electricity demand is anticipated to increase by nearly 80% between 2012 and 2040. Expansion, modernization, digitization, and decentralization of the electricity infrastructure for improved resiliency and a planned investment from organizations such as the World Economic Forum (USD 7.6 trillion allocated for smart grids for the next 25 years) are expected to change various market dynamics in the global scenario.

- Further, utilities worldwide are increasingly adopting technologies like artificial intelligence and digital twinning, coupled with increased government support and initiatives, which are further attracting investments in smart grid projects. For instance, in January 2024, the US Department of Energy announced the development of technologies aimed at modernizing the electric grid, undergrounding power lines, and replacing aging infrastructure with USD 34 million in grants. The program is aimed at advancing solutions to modernize and boost the country's power grid infrastructure by minimizing extreme weather-related disruptions, lowering costs, and accelerating the adoption of renewable energy.

- The impact of macroeconomic factors such as supply chain disruptions, energy prices, sanctions, trade restrictions, and rising inflation, along with the Russia-Ukraine War, has created a challenging environment for the high-voltage film capacitor market. While disruptions and cost increases pose significant challenges, the ongoing push for renewable energy and electric vehicles continues to drive demand, providing some counterbalance to the negative factors.

High Voltage Film Capacitor Market Trends

Automotive Segment is Expected to Witness a Significant Growth Rate

- High-voltage film capacitors play a crucial role in the automotive industry, particularly in electric vehicles, hybrid electric vehicles, and advanced internal combustion engine vehicles. These capacitors are integral in power electronics systems that manage vehicles' flow and conversion of electrical energy.

- In EVs and HEVs, battery management systems use high-voltage film capacitors to stabilize voltage and manage the battery's charging and discharging cycles. This ensures the battery pack's optimal performance and longevity.

- Further, the increasing initiatives for adopting ABS and ADAS are further boosting the segment's growth. As vehicles become more advanced with ADAS features, the power requirements increase. High-voltage film capacitors help manage these power needs, providing stable and reliable power to sensors and processors that enable ADAS functionalities.

- The Indian government has been actively promoting the adoption of ADAS through various regulations and policies. Initiatives to mandate certain ADAS features in new cars are anticipated, mirroring global trends. This regulatory push is likely to accelerate the widespread adoption of these technologies.

- Further, Automotive Industry Standard 145 requires every vehicle sold in India to have airbags, SBR, ABS, and SWS. The recently introduced AIS 197: BNCAP (Bharat New Car Assessment Program), with its stricter crash testing norms, is expected to catalyze the uptake of passive and active safety, laying the groundwork for ADAS becoming a mandatory requirement.

Asia-Pacific is Expected to Witness Significant Market Growth

- Industrial expansion, renewable energy projects, transportation electrification, consumer electronics growth, smart grid development, technological advancements, supportive government policies, and increasing energy demand propel the growth of high-voltage film capacitors in Asia-Pacific.

- China has been one of the world's largest automotive markets for the past years and is becoming a powerhouse for automotive technology. The country may considerably impact the automotive industry in the coming years as it is open to technological progress. Moreover, with the arrival of Industry 4.0, China is expected to see massive growth in the automation and industry sector, owing to schemes like "Made in China 2025."

- Further, in January of this year, China's BYD outpaced Tesla in becoming the world's largest producer of pure-electric vehicles. The surge is fuelled by rising EV demand in China, where 40% of vehicles sold are electric. This shift toward electric vehicles and the development of electric public transportation systems in Asia-Pacific are driving the demand for high-voltage film capacitors.

- The consumer electronics and telecommunication industries in India are also witnessing significant growth. These industries are expected to create a favorable market scenario for the development of the country's high-voltage film capacitor market. According to ICEA, India can achieve a value of USD 100 billion in the manufacturing of laptops and tablets by 2025. Furthermore, according to IBEF, the Indian appliances and consumer electronics industry is expected to more than double to reach USD 21.18 billion.

- Further, the Indian telecom tower industry has grown significantly by 65% over the past seven years. FDI in the telecommunication sector during 2022-2023 was USD 694 million compared to USD 668 million during 2021-2022.

High Voltage Film Capacitor Industry Overview

The high-voltage film capacitor market is highly competitive, with several vendors of different sizes. As organizations continue to invest strategically in offsetting the present slowdowns, the market is anticipated to encounter a number of partnerships, mergers, and acquisitions. The key companies operating in the market include TDK Corporation, KYOCERA AVX, Kemet Corporation, and Vishay Intertechnology.

- April 2024: Kyocera AVX released two new snap-in aluminum electrolytic capacitors series. The SNA and SNL Series deliver high reliability, high voltage, and high CV performance over long lifetimes. In addition, both series are lead-free compatible and RoHS compliant, rated for temperatures extending from -25°C to +105°C, and ideal for use in commercial and industrial applications, including frequency converters, solar inverters, power inverters, energy storage systems, and power supplies.

- April 2024: KEMET Corporation announced launching the R41P, a Y2/X1 film capacitor whose smaller size (40% smaller than the R41T) is particularly impressive in applications where space requirements and costs are prioritized. Accordingly, the component has a lower THB value and a shorter service life at high temperatures. This capacitor series is suitable for use in filters for suppressing electromagnetic interference (EMI) in "line-to-ground" and "across-the-line" applications that require safety classification Y2/X1.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Demand for Electric Vehicles

- 5.1.2 Rising Demand for Smart Grids

- 5.1.3 Increasing Demand for Energy Efficient Technologies

- 5.2 Market Restraints

- 5.2.1 Limited Availability of Raw Materials

- 5.2.2 High Production Cost

6 ANALYSIS OF WOUND TYPE AND LAMINATE TYPE

7 MARKET SEGMENTATION

- 7.1 By End-user Industry

- 7.1.1 Automotive

- 7.1.2 Aerospace and Defense

- 7.1.3 Oil and Gas

- 7.1.4 Drives and Inverters (Non-automotive)

- 7.1.5 Other End-user Industries

- 7.2 By Geography

- 7.2.1 North America

- 7.2.2 Europe

- 7.2.3 Asia-Pacific

- 7.2.4 Australia and New Zealand

- 7.2.5 Latin America

- 7.2.6 Middle East and Africa

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 TDK Corporation

- 8.1.2 KYOCERA AVX Components Corporation

- 8.1.3 Nichicon Corporation

- 8.1.4 Kemet Corporation

- 8.1.5 Panasonic Industry Co. Ltd

- 8.1.6 Vishay Intertechnology nc.

- 8.1.7 WIMA GmbH & Co. KG