|

시장보고서

상품코드

1550203

캡 라이너 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2024-2029년)Cap Liners - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

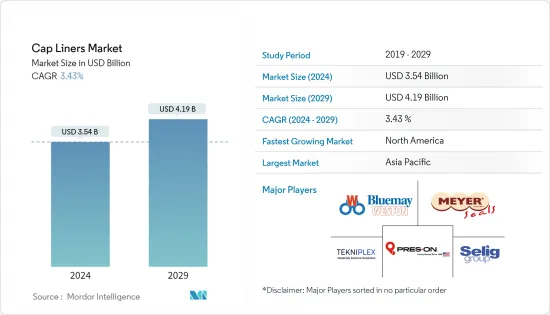

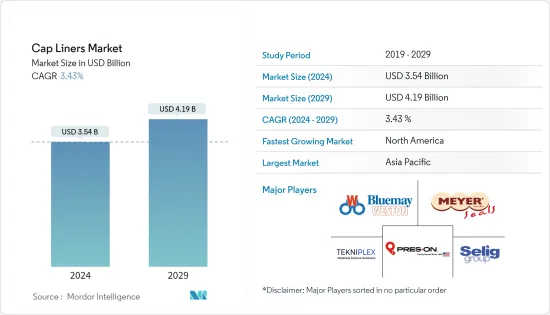

캡 라이너 시장 규모는 2024년 35억 4,000만 달러로 추정되며, 2029년에는 41억 9,000만 달러에 달할 것으로 예상되며, 예측 기간(2024-2029년) 동안 3.43%의 CAGR로 성장할 것으로 예상됩니다.

포장 산업에서 캡 라이너에 대한 수요는 업계가 경계를 넓혀감에 따라 급증할 것으로 예상됩니다. 캡 라이너는 식품, 음료 및 의약품과 같은 여러 최종사용자 산업에서 그 어느 때보다 중요성이 커지고 있습니다.

캡 라이너의 변조 방지 능력은 그 수요를 새로운 차원으로 끌어올리고 있습니다. 필수, 감압, 열 유도 등 다양한 종류의 캡 라이너가 포장 산업에 혁명을 일으키고 있습니다.

기업들은 이산화탄소 배출량을 줄이기 위해 지속가능한 재료에 점점 더 많은 관심을 기울이고 있습니다. 통기성 유도 캡 라이너를 채택하여 높은 고도에서 병이 무너지는 문제를 해결하는 것은 제품 제조업체에게 특히 유망합니다. 포장 제품의 밀폐성, 브랜드 파워 및 선반 진열 능력을 향상시키기 위해 이러한 라이너에 대한 의존도가 점점 더 높아지고 있습니다.

Integrated Liner Technologies에 따르면 일반적인 캡 라이너 유형에는 실리콘, 부틸 고무, PTFE, 폴리에틸렌, 호일 등이 있습니다. 각각은 최종사용자 산업의 다양한 요구에 맞는 뚜렷한 이점을 제공하며, 선택 과정은 내용물의 화학적 특성, 온도 민감성 및 외부 취약성과 같은 요인에 따라 달라집니다. 이러한 고려 사항은 내화학성, 유연성, 완충성 및 규제 준수를 보장하는 것을 목표로 하며, 이는 모두 품질 및 안전 표준을 유지하는 데 매우 중요합니다.

또한, 식품 안전과 지속가능성에 대한 소비자의 인식이 높아지면서 혁신적인 캡 라이너 소재와 디자인이 채택되고 있습니다. 또한 제약회사들은 내용물과의 호환성 및 보관 중 샘플을 보호하는 데 중요한 씰의 무결성을 유지하는 능력에 따라 캡 라이너를 선택하고 있습니다.

또한 캡과 라이너의 접촉 불량으로 인한 밀봉 불량, 누출, 유출 등의 문제에 직면 할 수 있으며, IH 캡 라이너의 과도한 가열은 포장 품질을 손상시켜 시장의 도전이 되고 있습니다. 그러나 플라스틱이나 폴리에스테르 라이너를 사용하는 것은 환경 친화적인 기업에게는 실망스럽고 캡 라이너의 광범위한 채택을 방해하고 있습니다.

캡 라이너 시장 동향

제약 업계의 캡 라이너 사용 증가

- 의약품 생산 및 포장에는 엄격한 규제가 있으며 포장 파트너는 업계의 요구 사항에 대해 잘 알고 있어야합니다. 제약 회사의 포장 담당자는 일반 의약품(OTC) 정제, 정제 및 액체의 안전을 보장하기 위해 유도 캡 실러에 의존하고 있습니다.

- 설계상, 유도 밀봉은 승인된 변조 방지 솔루션을 제공합니다. 용기 입술에 라이너 잔여물을 남기고 소비자가 개봉했음을 알 수 있도록 합니다. 인덕션 씰은 변조 방지뿐만 아니라 누출을 방지하고 제품의 신선도를 유지하여 제약 업무에도 도움이 됩니다. 인덕션 캡의 밀폐 밀봉은 산소와 습기가 용기의 내용물을 손상시키는 것을 방지합니다.

- Integrated Liner Technologies에 따르면 제약 회사는 실험용 저장 용기의 캡 라이너를 매우 신중하게 선택한다고 합니다. 이 라이너는 실리콘, 부틸 고무, PTFE, 폴리에틸렌, 호일 등 내용물과의 호환성 및 시료 오염을 방지하는 데 중요한 밀봉 무결성을 유지하는 능력에 따라 선택됩니다. 각 라이너 유형은 의약품의 필요에 따라 뚜렷한 이점을 제공합니다.

- 또한 캡 라이너의 선택 과정은 내용물의 화학적 특성, 온도 민감성 및 외부 요소에 대한 취약성에 따라 달라집니다. 내화학성, 유연성, 쿠션, 밀폐성을 우선시함으로써 기업은 제품이 엄격한 규제 기준을 충족하고 업계 최고의 품질 및 안전 벤치마크를 유지하도록 보장합니다.

- 제약 산업도 질병 증가로 인해 성장하고 있습니다. 아스트라제네카에 따르면 2023년부터 2027년까지 라틴아메리카의 의약품 시장 성장 전망은 22%로, 라틴아메리카가 세계 1위를 차지하고 유럽이 10.6%의 성장률을 기록할 것으로 예상됩니다. 그러나 제약 산업의 상승은 다양한 의약품과 약품의 포장 요구 사항이 증가함에 따라 캡 라이너 시장을 더욱 촉진할 것으로 보입니다.

북미가 가장 큰 성장 지역이 될 것으로 예상

- 플라스틱 뚜껑 및 마개는 많은 산업 분야에서 매우 중요하며 비용 효율적인 밀봉 솔루션을 제공하며, PP, HDPE, LDPE 등 다양한 플라스틱을 위한 열 유도 캡 및 라이너는 누출을 방지할 뿐만 아니라 무단 개봉 방지 기능을 강화합니다. 이러한 이중 기능성은 예측 기간 동안 시장 성장을 촉진할 것입니다.

- 포장된 음료 및 의약품에 대한 수요가 크게 증가하고 있습니다. 그 결과, 조사 대상 시장도 예측 기간 동안 수요 증가를 기록할 것으로 예상됩니다. 소비자의 건강 지향성이 점점 더 높아지면서 건강 음료에 대한 수요도 증가하고 있습니다. 이로 인해 생수는 개인에게 더 친숙해졌으며, 이는 지역 캡 라이너 시장의 성장을 촉진하고 있습니다.

- 이 지역에서는 생수를 포함한 무알콜 음료가 대량으로 소비되고 있습니다. 미국은 광범위한 소비자 기반을 자랑하며 세계 생수 시장을 독점하고 있으며, FDA는 용기에 밀봉된 생수는 사람이 마실 목적으로만 사용할 수 있으며 추가 성분을 포함해서는 안 된다고 규정하고 있습니다. Beverage Marketing Corporation과 국제 생수 협회가 2023년 3월에 발표한 보고서에 따르면 생수는 2022년 미국에서 가장 인기 있는 음료로 전체 음료 소비량의 약 25%를 차지할 것으로 예상했습니다.

- 또한 Monster Beverage Corporation에 따르면 2023년 미국의 무알콜 음료 판매액 성장률에서 에너지 음료 부문이 8.3%로 1위를 차지했고, 탄산음료가 3.6%로 그 뒤를 이었습니다. 따라서 음료 성장률의 증가는 지역 전체의 캡 라이너 시장을 강화할 것으로 예상됩니다.

캡 라이너 산업 개요

캡 라이너 시장은 세분화되어 있으며, Tekni-Plex Inc., Meyer Seals GmbH, Bluemay Weston Limited, Press-On Corporation, Selig UK Limited, B&B Cap Liners LLC와 같은 다양한 다양한 기업들이 이 업계에서 사업을 전개하고 있습니다. 기업들은 인수, 제휴, 합병 및 기타 전략을 통해 사업 확장에 주력하고 있습니다.

- 2024년 1월 TekniPlex는 재활용 가능한 종이 기반 유도 열 밀봉 라이너의 새로운 시리즈 인 ProTecSeals 재활용 가능한 IHS 라이너는 목재 펄프로 만든 재활용 가능한 종이로 만들어졌습니다. 기존 IHS 라이너와 동일한 기준으로 수분 및 산소 차단, 누출 방지, 오염 방지 및 유통기한 연장을 제공합니다.

- 2023년 6월, Selig UK Limited는 컨테이너 씰링 및 벤트 기술을 통합한 새로운 웹사이트를 개설하고 사업을 확장한다고 발표했습니다. 새로운 웹사이트는 기존 여러 웹사이트의 컨텐츠를 통합하여 셀리그의 다양한 솔루션과 제품을 소개하고 있습니다. 이 웹사이트는 회사의 세계 입지와 고객 기반을 반영하기 위해 영어, 중국어, 프랑스어, 독일어, 스페인어 등 5개 국어로 제공됩니다.

기타 혜택

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 소개

- 조사 상정과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 업계의 매력 - Porter's Five Forces 분석

- 공급 기업의 교섭력

- 구매자의 교섭력

- 신규 참여업체의 위협

- 대체품의 위협

- 경쟁 기업 간의 경쟁 관계

- 산업 밸류체인 분석

제5장 시장 역학

- 시장 성장 촉진요인

- 제품 안전하고 확실한 취급, 보관, 수송

- 제약 업계로부터의 수요 증가

- 시장 성장 억제요인

- 부적절한 라이너는 유통기한을 줄이거나 제품 누출을 유발하는 가능성이 있다

제6장 시장 세분화

- 재료 유형별

- 고무

- 금속

- 플라스틱

- 종이

- 용도별

- 보틀

- 자·용기

- 제품 유형별

- 열전도 캡 라이너

- 원피스

- 투피스

- 하프문 라이너

- 기타 열전도 캡 라이너

- 감압 라이너

- 기타 제품 유형

- 열전도 캡 라이너

- 최종 이용 산업별

- 식품

- 음료

- 퍼스널케어 및 화장품

- 화학·비료

- 오일, 윤활유, 그리스

- 홈케어

- 기타 최종 이용 산업

- 지역별

- 북미

- 미국

- 캐나다

- 유럽

- 프랑스

- 독일

- 스페인

- 영국

- 터키

- 아시아태평양

- 중국

- 인도

- 일본

- 태국

- 호주·뉴질랜드

- 라틴아메리카

- 브라질

- 멕시코

- 중동 및 아프리카

- 아랍에미리트

- 사우디아라비아

- 이집트

- 남아프리카공화국

- 북미

제7장 경쟁 상황

- 기업 개요

- Meyer Seals GmbH

- Tekni-Plex Inc.

- Bluemay Weston Limited

- Press-On Corporation

- B&B Cap Liners LLC

- Low's Cap Seal Sdn Bhd

- Tien Lik Cap Seal Sdn Bhd

- Captel International Pvt. Ltd

- The Cary Company

- Selig UK Limited

- M.F.I. Capliners

제8장 주요 기업 개요 히트맵 분석

제9장 기업 분류 분석 - 신흥 기업과 기존 기업

제10장 투자 분석

제11장 시장 향후 전망

ksm 24.09.13The Cap Liners Market size is estimated at USD 3.54 billion in 2024, and is expected to reach USD 4.19 billion by 2029, growing at a CAGR of 3.43% during the forecast period (2024-2029).

The demand for cap liners in the packaging industry is poised to surge as the industry pushes its boundaries. Cap liners are gaining unprecedented importance in multiple end-user industries, such as food, beverage, and pharmaceuticals, driven by the growing reliance of the affluent population.

Cap liners' ability to establish tamper evidence propels their demand to new heights. A wide array of cap liners, including essential, pressure-sensitive, and heat induction, is revolutionizing the packaging industry.

Businesses are increasingly turning to sustainable materials to shrink their carbon footprints. Adopting vented induction cap liners to tackle the high-altitude bottle collapsing issue is particularly promising for product manufacturers. Industries increasingly rely on these liners to enhance the sealing, branding, and shelf appeal of their packaged product.

According to Integrated Liner Technologies, the prevalent cap liner types include silicone, butyl rubber, PTFE, polyethylene, and foil. Each offers distinct advantages tailored to different end-user industry needs, with the selection process hinging on factors like content chemistry, temperature sensitivity, and external vulnerability. These considerations aim to ensure chemical resistance, flexibility, cushioning, and regulatory compliance, all pivotal for upholding quality and safety standards.

Moreover, heightened consumer awareness of food safety and sustainability is driving the adoption of innovative cap liner materials and designs. Also, pharmaceutical companies select cap liners based on their compatibility with the contents and ability to maintain seal integrity, which is crucial for safeguarding samples in storage.

The market might also face challenges, such as poor cap-liner contact, leading to inadequate sealing, leaks, and spills. Excessive heating of induction cap liners compromises packaging quality and challenges the market. However, using plastic or polyester liners is a letdown for eco-conscious businesses, hindering the wider adoption of cap liners.

Cap Liners Market Trends

Increased Use of Cap Liners in the Pharmaceutical Industry

- Pharmaceutical production and packaging are subject to stringent regulations, necessitating packaging partners to be well-versed in the industry's demands. Pharmaceutical packagers rely on induction cap sealers to secure over-the-counter (OTC) prescription pills, tablets, and liquids.

- By design, induction seals offer an approved tamper-evident solution. They leave a liner residue on the container lip, signaling to consumers of any prior opening. Beyond tamper-evidence, induction seals also aid pharmaceutical operations by ensuring leak prevention and preserving product freshness. The airtight seal on the induction cap prevents oxygen and moisture from compromising the container's contents.

- According to Integrated Liner Technologies, pharmaceutical companies meticulously select cap liners for their lab storage containers. These liners, including silicone, butyl rubber, PTFE, polyethylene, and foil, are chosen based on their compatibility with the contents and ability to maintain seal integrity, which is crucial for preventing sample contamination. Each liner type offers distinct advantages tailored to the pharmaceutical product's needs.

- Additionally, the selection process of cap liners depends on content chemistry, temperature sensitivity, and vulnerability to external elements. By prioritizing chemical resistance, flexibility, cushioning, and hermetic sealing, companies ensure their products meet stringent regulatory standards, upholding the industry's highest quality and safety benchmarks.

- The pharmaceutical industry is also growing owing to the rise in diseases. According to AstraZeneca, the projected pharmaceutical market growth between 2023 and 2027 in Latin America is expected to be 22%, with Latin America taking the top position globally, followed by Europe recording a 10.6% growth. However, a rise in the pharmaceutical industry would further boost the cap liners market, with growing packaging requirements for various medicines and drugs.

North America is Expected to be the Largest-growing Regional Market

- Plastic caps and closures are pivotal in many industries, offering a cost-effective sealing solution. Heat induction cap liners, compatible with a range of plastics like PP, HDPE, and LDPE, not only prevent leaks but also enhance tamper-proof features. This dual functionality is set to drive market growth over the forecast period.

- The demand for packaged beverages and pharmaceutical drugs has been increasing enormously. As a result, the market studied is also expected to register increased demand during the forecast period. Consumers are becoming increasingly health-conscious, and the demand for healthy beverages is rising. This has made bottled water more accessible to individuals, aiding the regional cap liner market's growth.

- The region witnesses vast consumption of non-alcoholic beverages, including bottled water. The United States dominates the global market for bottled water, boasting an extensive consumer base. The FDA specifies that bottled water, sealed in its container, is solely intended for human consumption and must not contain any additional ingredients. According to a report published by the Beverage Marketing Corporation and the International Bottled Water Association in March 2023, bottled water was the most popular drink in the United States in 2022, accounting for about 25% of all beverage consumption.

- Further, according to Monster Beverage Corporation, in terms of sales value growth of non-alcoholic beverages in the United States in 2023, the energy drinks segment took the top position with 8.3%, followed by carbonated soft drinks with 3.6% in the same year. Therefore, rising beverage growth is expected to bolster the cap liners market across the region.

Cap Liners Industry Overview

The cap liners market is fragmented, with various players, such as Tekni-Plex Inc., Meyer Seals GmbH, Bluemay Weston Limited, Press-On Corporation, Selig UK Limited, and B&B Cap Liners LLC, operating in the industry. The players are focused on expanding their business through acquisitions, collaborations, mergers, and other strategies.

- January 2024: TekniPlex launched a new series of recyclable, paper-based induction heat seal liners designed to seal dry pharma, nutrition, and food products in bottles and jars with protective properties identical to conventional solutions. The ProTecSeals Recyclable IHS Liners are made of recyclable paper from tree pulp. They offer moisture and oxygen barrier properties, resist leaks, prevent contamination, and prolong shelf life to the same standard as traditional IHS liners.

- June 2023: Selig UK Limited announced that it was expanding its business by launching a new website that consolidates its container sealing and venting technologies. The new site integrates content from several legacy websites and exhibits Selig's diverse solutions and products. To reflect the company's global presence and customer base, the website was made available in five languages: English, Mandarin, French, German, and Spanish.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces' Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Safe and Secure Handling, Storage, and Transport of Products

- 5.1.2 Increased Demand from the Pharmaceutical Industry

- 5.2 Market Restraints

- 5.2.1 Improper Liners May Shorten Shelf Life or Cause Leakage of Products

6 MARKET SEGMENTATION

- 6.1 By Material Type

- 6.1.1 Rubber

- 6.1.2 Metal

- 6.1.3 Plastic

- 6.1.4 Paper

- 6.2 By Application

- 6.2.1 Bottles

- 6.2.2 Jars & Containers

- 6.3 By Product Type

- 6.3.1 Heat-induction Cap Liners

- 6.3.1.1 One-piece

- 6.3.1.2 Two-piece

- 6.3.1.3 Halfmoon Liner

- 6.3.1.4 Other Heat-induction Cap Liners

- 6.3.2 Pressure Sensitive Liners

- 6.3.3 Other Product Types

- 6.3.1 Heat-induction Cap Liners

- 6.4 By End-user Industry

- 6.4.1 Food

- 6.4.2 Beverage

- 6.4.3 Personal Care & Cosmetics

- 6.4.4 Chemicals & Fertilizers

- 6.4.5 Oil, Lubricants, and Grease

- 6.4.6 Home Care

- 6.4.7 Other End-user Industries

- 6.5 By Geography

- 6.5.1 North America

- 6.5.1.1 United States

- 6.5.1.2 Canada

- 6.5.2 Europe

- 6.5.2.1 France

- 6.5.2.2 Germany

- 6.5.2.3 Spain

- 6.5.2.4 United Kingdom

- 6.5.2.5 Turkey

- 6.5.3 Asia-Pacific

- 6.5.3.1 China

- 6.5.3.2 India

- 6.5.3.3 Japan

- 6.5.3.4 Thailand

- 6.5.3.5 Australia and New Zealand

- 6.5.4 Latin America

- 6.5.4.1 Brazil

- 6.5.4.2 Mexico

- 6.5.5 Middle East and Africa

- 6.5.5.1 United Arab Emirates

- 6.5.5.2 Saudi Arabia

- 6.5.5.3 Egypt

- 6.5.5.4 South Africa

- 6.5.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Meyer Seals GmbH

- 7.1.2 Tekni-Plex Inc.

- 7.1.3 Bluemay Weston Limited

- 7.1.4 Press-On Corporation

- 7.1.5 B&B Cap Liners LLC

- 7.1.6 Low's Cap Seal Sdn Bhd

- 7.1.7 Tien Lik Cap Seal Sdn Bhd

- 7.1.8 Captel International Pvt. Ltd

- 7.1.9 The Cary Company

- 7.1.10 Selig UK Limited

- 7.1.11 M.F.I. Capliners