|

시장보고서

상품코드

1624595

냉동식품 포장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Frozen Food Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

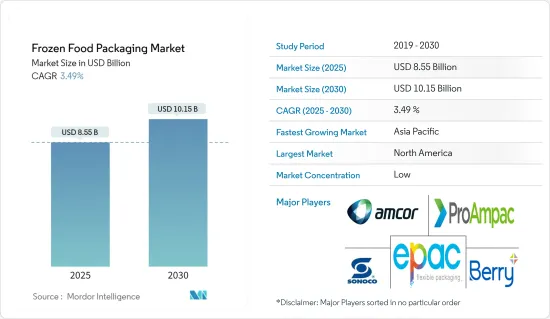

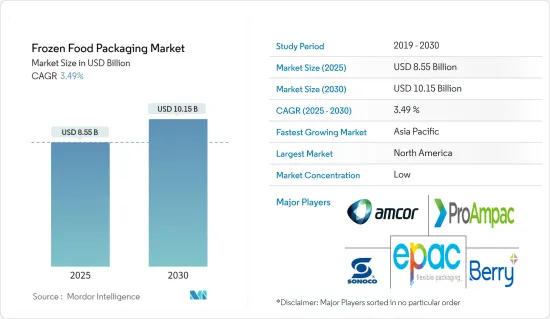

냉동식품 포장 시장 규모는 2025년 85억 5,000만 달러로 추정되며, 예측 기간(2025-2030년) 동안 3.49%의 연평균 복합 성장률(CAGR)로 2030년에는 101억 5,000만 달러에 달할 전망입니다.

냉동식품 포장은 가볍고 깨지지 않고 밀봉이 가능하며, 화석연료 사용량을 줄이고 온실 가스 배출과 물 사용량을 줄여 환경 친화적인 환경을 조성할 수 있습니다.

주요 하이라이트

- 시장 소비자는 소매점, 슈퍼마켓, 대형 마트를 선호합니다. 조직화 된 소매점은 전 세계적으로 큰 존재감을 보이고 있으며 시장의 상당 부분을 차지하고 있습니다. 조직화 된 소매 체인 증가는 냉동 식품 산업에서 식품 포장 솔루션의 요구와 직접적으로 관련이 있습니다.

- 육류, 가금류, 해산물과 같은 냉동 식품 포장은 다른 식품 용도 중 가장 빠른 성장세를 보였습니다. 전 세계의 많은 대형 식품 포장 회사들이 매우 창의적이고 장식적인 포장을 출시했습니다.

- 예를 들어, 2023년 8월, 섬유 기반 제품 제조업체인 Ahlstrom은 지속 가능한 포장 업체인 The Paper People과 협력하여 냉동 식품을 위한 지속 가능한 포장 솔루션을 발표했습니다. 양사가 공동 개발한 이 완전 섬유 기반 패키지는 주로 냉동 식품 포장에 사용되는 기존의 화석 자원에서 추출한 플라스틱과 필름을 대체할 수 있도록 설계되었습니다. 이 재활용 가능한 포장은 수직형 Form Fill Seal, 스탠드업 파우치, SOS 스타일 시스템 등 기존 포장 설비에서 사용할 수 있습니다.

- 또한 사빅은 2023년 5월 에스티코 패키징 솔루션즈(Estico Packaging Solutions) 및 노르웨이 브랜드 소유주인 콜드워터프론즈(Coldwater Prons)와 함께 냉동 새우를 위한 지속 가능한 새로운 포장용 파우치를 설계 및 제조했습니다. 이 파우치는 사빅 PP(폴리프로필렌) 크리스탈의 원형 인증 랜덤 폴리머 등급을 사용하고, 에스티코 패키징 솔루션즈가 제공하는 다층 필름으로 만들어졌으며, 해양 유래 플라스틱 함량이 약 60%에 달할 전망입니다.

- 그러나 정부의 포장 관련 법규가 시장 성장을 제한할 수 있습니다. 미국 식품의약국(FDA)은 식품에 첨가되는 물질의 안전성을 규제하고 있습니다. 전반적으로 냉동 식품 포장은 저온 및 고온에 대한 내성, 특정 기계적 강도, 식품에 함유된 산, 오일 및 기타 분해성 화학 물질에 대한 내성, 특정 위생 수준 및 유사성과 같은 본질적인 특성을 요구합니다.

냉동식품 포장 시장 동향

육류와 수산식품이 시장의 주요 점유율을 차지합니다.

- 냉동 육류 시장은 향후 몇 년동안 식습관의 변화로 인해 크게 성장할 것으로 예상되며, 코로나19 발생 이후 냉동 육류와 포장된 조리 식품에 대한 수요가 급증했습니다. 시간이 지남에 따라 육류 산업은 다양화되어 현재 많은 가공업체들이 냉동 육류 제품 및 조리된 식품을 제공합니다. 주목할 만한 점은 이 분야가 전 세계 거의 모든 지역으로 확대되고 있다는 점입니다.

- 소비자들은 더 높은 품질에 대해 프리미엄을 지불할 의향이 있습니다. 소비자들은 보존료를 최소화하거나 아예 사용하지 않는 냉동 육류 제품을 생산하는 브랜드를 선호하고 있습니다. 결과적으로 건강한 식단에 대한 소비자의 선호도가 높아짐에 따라 '유기농' 또는 무방부제 냉동 육류 및 생선 제품에 대한 수요가 증가하고 있습니다. 신선육에 비해 유통기한이 길다는 등의 장점에 이끌려 많은 사람들이 안심하고 냉동 육류 제품을 구매하고 있습니다.

- 뉴질랜드 통계청에 따르면 2023년 뉴질랜드의 냉동 닭고기 생산량은 6만 8,000톤 이상으로 전년도 약 6만 3,000톤에 비해 증가했습니다. 이러한 증가 추세는 앞으로도 계속될 것으로 예상되며, 냉동 식품 포장에 대한 수요를 더욱 증가시킬 것으로 보입니다.

- 노르웨이의 리스크 관리 및 보증 회사인 데트노르스케 베리타스(DNV)의 '수산물 예측'에 따르면, 전 세계 1인당 수산물 수요는 2050년까지 꾸준히 증가할 것이라고 합니다. 시장 확대에 따라 수산물 품질 유지가 가장 중요한 과제로 떠오르고 있습니다. 따라서 미생물의 번식을 억제하고, 냉동 데임을 방지하며, 급속냉동을 용이하게 하고, 물방울 손실을 최소화하여 유통기한을 연장할 수 있는 포장 솔루션이 필요합니다. 그 결과, 포장된 수산물 제품의 소비 증가는 냉동 수산물 포장에 대한 수요를 증가시키고 있습니다.

- 시장의 주요 기업들은 지속적으로 새로운 냉동 수산물 제품을 출시하고 있으며, 이를 통해 포장 공급업체의 기회를 확대하고 있습니다. 예를 들어, 2024년 5월 Scott &Jon's는 냉동 새우 요리 라인을 확장하고 전자 레인지로 조리할 수 있는 연어 덮밥을 새로 추가했습니다. 이 최신 제품들은 2023년 Scott &Jon's가 건강 지향적인 새우 덮밥 라인을 선보인 데 이어 나온 것입니다.

아시아태평양이 가장 빠른 성장세를 보이고 있습니다.

- 아시아태평양에서는 인구 증가가 식품 수요 증가를 주도하고 있습니다. 도시화와 식중독, 낭비, 부패에 대한 인식이 높아지면서 고품질 제품에 대한 수요가 증가하고 있습니다. 중국은 아시아태평양 냉동식품 포장 시장에서 큰 비중을 차지하고 있습니다. 중국의 방대한 인구와 도시화로 인해 냉동식품에 대한 수요가 증가하고 있습니다. 오늘날의 소비자들은 편리함과 품질을 모두 중요하게 여깁니다.

- 인도 냉동식품 분야는 빠르게 성장하고 있습니다. 각 브랜드의 냉동식품은 파티에서 가끔씩 제공되는 간식에서 모든 연령층이 즐기는 상비 식품으로 성공적으로 전환하고 있습니다. 특히 노동 인구 증가로 인해 조리된 식품(RTE)과 간편식에 대한 수요가 급증하고 있습니다. 이러한 추세는 바쁜 삶을 살면서 가족을 위해 빠르고 영양가 높은 식사를 원하는 현대의 부부들 사이에서 더욱 두드러지고 있습니다.

- 지역 전체에서 건강 및 피트니스 트렌드가 가속화되고 있는 가운데 냉동 식품 부문도 뒤처지지 않았습니다. 포장은 이 산업에서 매우 중요한 역할을 합니다. 식품 제조업체들은 생산부터 소비까지 제품이 안전하고 오염되지 않도록 하는 것을 최우선 과제로 삼고 있으며, 견고한 냉동식품 포장 솔루션이 이러한 과제를 효과적으로 해결하고 있습니다.

- 고품질과 간편한 조리법으로 인해 일본 소비자들은 냉동식품 포장을 선호하고 있습니다. 또한 일본의 다국적 식품 및 생명공학 기업인 아지노모도는 일본의 가정용 냉동식품 소비가 전년도 486억 엔(3억 3,000만 달러)에서 2023년 603억 엔(4억 1,000만 달러)으로 증가할 것이라고 보고했습니다. 이러한 급격한 증가는 이 지역의 냉동 식품 포장 옵션 시장을 촉진할 것으로 보입니다.

- 또한 중국, 일본, 인도 및 기타 아시아 국가의 냉동 식품 포장 시장 규모는 냉동 육류 및 조리 된 육류 제품에 대한 수요 증가로 인해 확대되고 있습니다. 중국 국가통계국에 따르면 최근 몇 년동안 냉동 식품 포장이 30% 가까이 증가했다고 합니다.

냉동식품 포장산업 개요

냉동식품 포장 시장은 세분화되어 있으며, Sonoco Products Company.ProAmpac LLC, Cascades Inc. 등 여러 주요 업체로 구성되어 있습니다. ProAmpac LLC, Cascades Inc. 등 시장 점유율 측면에서 현재 시장을 독점하고 있는 주요 업체는 소수에 불과합니다. 그러나 독창적이고 장식적인 포장 패턴을 가진 중견 및 중소기업은 신규 계약 체결 및 새로운 시장 개발을 통해 시장에서의 존재감을 높이고 있습니다.

기타 혜택 :

기타 혜택- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 업계의 매력 - Porter의 Five Forces 분석

- 신규 진출업체의 위협

- 구매자/소비자의 교섭력

- 공급 기업의 교섭력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 산업 밸류체인 분석

제5장 시장 역학

- 시장 성장 촉진요인

- 시장 성장 억제요인

제6장 시장 세분화

- 식품 유형별

- 과일 및 채소

- 고기 및 해산물

- 냉동 디저트 및 아이스크림

- 제과

- 포장 유형별

- 백

- 박스

- 튜브 및 컵

- 트레이

- 래퍼

- 파우치

- 기타 포장

- 지역별

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 아시아

- 중국

- 일본

- 인도

- 한국

- 호주 및 뉴질랜드

- 라틴아메리카

- 중동 및 아프리카

- 북미

제7장 경쟁 구도

- 기업 개요

- ProAmpac LLC

- Sonoco Products Company

- Amcor PLC

- Berry Plastics Group Inc.

- ePac Holdings, LLC

- Cascades Inc.

- Duropack Limited

- Smurfit Westrock plc

- Mondi Group

- American Packaging Corporation

- ThinkInk Packaging

제8장 투자 분석

제9장 시장 기회와 향후 동향

LSH 25.01.15The Frozen Food Packaging Market size is estimated at USD 8.55 billion in 2025, and is expected to reach USD 10.15 billion by 2030, at a CAGR of 3.49% during the forecast period (2025-2030).

Frozen food packaging delivers lightweight, unbreakable, and resealable features, lowers fossil fuel usage, and can reduce greenhouse gas emissions and water usage to create an eco-friendly environment.

Key Highlights

- The market's consumers prefer retail stores, supermarkets, and hypermarkets. Organized retail stores are a substantial part of the market with a significant global presence. The increase in the organized retail chain is translating directly into the need for food packaging solutions in the frozen food industry.

- Packaging for frozen foods like meat, poultry, and seafood witnessed the fastest growth among other food applications. Many large food packaging companies across the globe are launching hugely creative and decorative packaging.

- For instance, in August 2023, fiber-based products manufacturer Ahlstrom teamed up with sustainable packaging provider The Paper People to launch a sustainable packaging solution for frozen food. Co-developed by the two companies, this fully fiber-based packaging is mainly designed to substitute traditional fossil-based plastic and films for frozen food packaging. The recyclable packaging can be utilized on existing packaging equipment, including vertical form-fill-seal, stand-up pouches, and SOS-style systems.

- Also, in May 2023, Sabic joined forces with Estiko Packaging Solutions and brand owner Coldwater Prawns of Norway to design and execute a sustainable new packaging pouch for frozen prawns. The pouch is made from a multilayer film offered by Estiko Packaging Solutions utilizing a circular-certified random polymer grade of Sabic PP (polypropylene) Qrystal with an ocean-bound plastic content of around 60%.

- However, the government packaging laws and regulations could limit the market growth. In the United States, the Food and Drug Administration (FDA) regulates the safety of substances added to food. Overall, frozen food packaging should have the following essential characteristics: Resistance to low and high temperatures, a particular mechanical strength, resistance to acid, oil, and other degrading chemicals in the food product, and a specific level of hygiene and similar.

Frozen Food Packaging Market Trends

Meat and Sea Food to Account for a Major Share in the Market

- The frozen meat market is poised for substantial growth in the coming years, primarily driven by shifting food preferences. Following the COVID-19 outbreak, demand surged for frozen meats and packaged, ready-to-eat foods. Over time, the meat industry has diversified, with numerous processing firms now offering frozen meat products and ready-to-eat items. Notably, this sector is witnessing expansion in nearly every region worldwide.

- Consumers are increasingly willing to pay a premium for higher quality. They consistently prefer brands that prioritize producing frozen meat items with minimal or no preservatives. As a result, the growing consumer preference for healthy eating is set to boost the demand for frozen meat and fish products marketed as "organic" and preservative-free.Many individuals now purchase frozen meat products with confidence, drawn by advantages like extended shelf life compared to fresh meat.

- Statistics New Zealand reported that New Zealand produced just over 68 thousand metric tons of frozen chicken meat in 2023, up from approximately 63 thousand metric tons the year before. This upward trend is anticipated to continue, further driving the demand for frozen food packaging.

- According to the "Seafood Forecast" by Det Norske Veritas (DNV), a Norwegian risk management and assurance firm, global per capita seafood demand is set to rise steadily until 2050. As markets expand, maintaining seafood quality becomes paramount. This necessitates packaging solutions that extend shelf life by curbing microbial growth, preventing freezer burn, facilitating rapid freezing, and minimizing drip loss. Consequently, the rising consumption of packaged seafood products is driving up the demand for frozen seafood packaging.

- Major players in the market are consistently launching new frozen seafood products, thereby expanding opportunities for packaging vendors. For example, in May 2024, Scott & Jon's expanded its frozen shrimp entree line to include new microwavable salmon bowls. These latest offerings come on the heels of Scott & Jon's 2023 debut of its health-focused shrimp bowl line.

Asia-Pacific to Witness the Fastest Growth

- In the Asia-Pacific region, a growing population is driving an increasing demand for food products. Urbanization and heightened awareness of foodborne illnesses, wastage, and spoilage are fueling demand for higher-quality offerings. China holds a significant share of the Asia-Pacific frozen food packaging market. The country's vast population and urbanization have spurred a rising appetite for frozen food items. Today's consumers prioritize both convenience and quality.

- India's frozen food segment is witnessing rapid expansion. Brands have successfully transitioned their offerings from being occasional party snacks to regular meal items enjoyed by all age groups. The surge in demand for ready-to-eat (RTE) and convenience foods is particularly pronounced among the growing working population. This trend is even more evident among modern couples, both of whom lead busy lives and seek quick, nutritious meals for their families.

- As the health and fitness trend gains momentum across the region, the frozen foods sector is not left behind. Packaging plays a pivotal role in this industry. Food manufacturers prioritize ensuring their products remain safe and contamination-free from production to consumption, a challenge effectively addressed by robust frozen food packaging solutions.

- Due to its high quality and popular easy-to-cook trends, frozen food packaging is preferred by Japanese consumers. Moreover, Ajinomoto, a Japanese multinational food and biotechnology corporation, reported that the consumption of home-use frozen meals in Japan rose to JPY 60.3 billion (USD 0.41 billion) in 2023, up from JPY 48.6 billion (USD 0.33 billion) the previous year. This surge is poised to boost the market for frozen food packaging options in the region.

- Additionally, the size of China, Japan, India and other Asian countries frozen food packaging market is expanding due to the rise in demand for frozen meat and ready-to-eat meal products. The National Bureau of Statistics of China states that the industry saw an increase in frozen food packaging of almost 30% in the last few years.

Frozen Food Packaging Industry Overview

The frozen food packaging market is fragmented and consists of several major players, such as Sonoco Products Company. ProAmpac LLC, Cascades Inc., and more. In terms of market share, few of the major players currently dominate the market. However, with creative and decorative packaging patterns, mid-size to smaller companies are increasing their market presence by securing new contracts and tapping new markets.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Frozen Food Demand in Emerging Countries

- 5.1.2 Rising Number of Organized Retail Stores

- 5.2 Market Restraint

- 5.2.1 Government Regulations and Interventions

6 MARKET SEGMENTATION

- 6.1 By Type of Food

- 6.1.1 Fruits and Vegetables

- 6.1.2 Meat and Sea Food

- 6.1.3 Frozen Desserts and Ice Creams

- 6.1.4 Baked Foods

- 6.2 By Type of Packaging

- 6.2.1 Bags

- 6.2.2 Boxes

- 6.2.3 Tubs and Cups

- 6.2.4 Trays

- 6.2.5 Wrappers

- 6.2.6 Pouches

- 6.2.7 Other Types of Packaging

- 6.3 Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 Germany

- 6.3.2.3 France

- 6.3.2.4 Italy

- 6.3.2.5 Spain

- 6.3.3 Asia

- 6.3.3.1 China

- 6.3.3.2 Japan

- 6.3.3.3 India

- 6.3.3.4 South Korea

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 ProAmpac LLC

- 7.1.2 Sonoco Products Company

- 7.1.3 Amcor PLC

- 7.1.4 Berry Plastics Group Inc.

- 7.1.5 ePac Holdings, LLC

- 7.1.6 Cascades Inc.

- 7.1.7 Duropack Limited

- 7.1.8 Smurfit Westrock plc

- 7.1.9 Mondi Group

- 7.1.10 American Packaging Corporation

- 7.1.11 ThinkInk Packaging