|

시장보고서

상품코드

1628740

남미의 접착제 및 실란트 : 시장 점유율 분석, 산업 동향 및 성장 예측(2025-2030년)South America Adhesives And Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

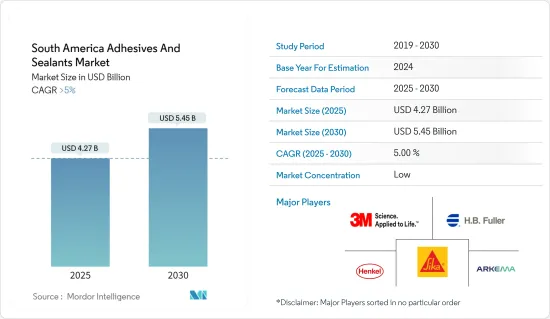

남미의 접착제 및 실란트 시장 규모는 2025년 42억 7,000만 달러에 이르고, 예측 기간(2025-2030년) 동안 5% 이상의 CAGR을 기록하여 2030년에는 54억 5,000만 달러에 달할 것으로 예상됩니다.

남미의 접착제 및 실란트 시장은 코로나19 팬데믹으로 인해 큰 영향을 받았으며, 이는 과제와 기회를 동시에 가져왔습니다. 초기에는 건설 및 제조업과 같은 산업에서 조업 중단과 혼란으로 인해 수요가 감소했습니다. 그러나 동시에 코로나19는 의료용품, 개인보호장비, 위생용품 제조에 있어 접착제 및 실란트의 필요성을 증가시켰습니다. 초기 침체에도 불구하고 시장은 회복되어 장기적인 성장을 보일 것으로 예상됩니다.

접착제 및 실란트 수요는 건설 산업 수요 증가와 의료 인프라 증가에 의해 크게 견인되고 있습니다.

그러나 접착제 및 실란트 관련 엄격한 VOC 배출 규제가 시장 성장에 걸림돌이 될 가능성이 높습니다.

바이오 접착제의 혁신과 개발, 복합재료 접착으로의 전환은 이 지역의 접착제 및 실란트 시장에 기회를 제공할 것으로 보입니다.

브라질은 건설, 항공우주, 자동차 등 최종 사용자 산업이 소비의 주요 원동력인 이 지역에서 가장 큰 접착제 및 실란트 시장입니다.

남미의 접착제 및 실란트 시장 동향

건축 및 건설 산업이 시장을 독점

- 접착제 및 실란트는 그 특성과 물리적 특성으로 인해 건축 및 건설 산업에서 널리 사용되고 있습니다. 이러한 특성에는 우수한 접착력과 탄성, 응집력, 높은 응집 강도, 유연성, 기판의 높은 탄성 계수, 열팽창에 대한 내성, 자외선, 부식, 염수, 비 및 기타 풍화 조건에 대한 내 환경성 등이 포함됩니다.

- 2022년 남미 지역에서는 건설 활동이 크게 증가할 것입니다. 그 이유는 팬데믹(세계적 대유행)의 해에 정부가 시행한 폐쇄 및 제한 조치의 영향에서 회복되기 때문입니다.

- 칠레건설회의소(CChC)에 따르면, 2023년 1-3월 건축자재 및 공급 가격 지수(IPMIC)가 전년 동기 대비 5.9% 상승했습니다.

- 브라질은 이 지역에서 가장 중요한 건설 및 부동산 시장입니다. 그러나 브라질의 경기 침체와 취약한 경제 상황은 이 지역의 건설 산업 성장을 저해할 것으로 예상됩니다.

- 브라질 정부는 항만, 도로, 철도, 송전선로, 위생 인프라 개발을 위한 인프라 컨세션 계획을 발표했습니다. 이 계획에 따라 정부는 민관협력(PPP) 모델을 통해 450억 BRL(미화 141억 달러)을 투자하는 것을 목표로 하고 있습니다. 또한, Minha Casa Minha Vida(MCMV), Plano Decenal de Expansao de Energia 2026, National Education Plan과 같은 정부 프로그램은 예측 기간 동안 산업 성장을 지원할 것으로 예상됩니다.

- 또한 2022년에는 브라질의 산업 건설이 크게 증가할 것입니다. 농업 비즈니스 체인 기업 BSBios는 브라질에 밀 에탄올 공장 건설을 계획하고 있습니다. 대형 투자 회사 인 Nordic Impact Corporation(NIC)은 브라질에 18 메가 와트 용량의 태양 광 발전소 6 개 건설에 투자하고 있습니다.

- 위의 모든 요인들은 예측 기간 동안 브라질의 접착제 및 실란트 수요를 증가시킬 것으로 예상됩니다.

브라질, 남미 지역에서 수요를 독식합니다.

- 브라질은 남미에서 접착제 소비량이 가장 많은 국가입니다. 포장, 자동차, 건설 및 기타 부문이 접착제에 크게 의존하고 있습니다.

- 브라질의 성장은 주로 주택 및 상업용 건축 부문의 급속한 성장과 경제 성장에 힘입어 성장하고 있습니다.

- 브라질 정부에 따르면 브라질의 관광 도시 상태를 업그레이드하고 이 산업의 잠재력을 극대화하여 더 많은 관광객을 유치하고 더 편안한 숙박을 제공하기 위해 2022년까지 762개의 인프라 프로젝트에 8억 6,600만 달러가 투자될 것이라고 밝혔습니다.

- 브라질의 제지 및 펄프 부문은 브라질에서 가장 성공적인 농산물 수출국 중 하나이며, 이러한 유형의 제품을 생산하는 국가 중 상위권에 속합니다. 종이팩에는 판지, 이중접기, 화이트 크래프트, 재활용, 복합재 등 다양한 재료가 사용되며, SIG는 2022년 5월 브라질 최대 우유 제조업체 중 하나인 Frimesa와 함께 Combistyle 카톤 포장을 도입했습니다. 이 카톤 팩은 브라질 소파울루에서 열린 미주 최대 F&B 박람회인 APAS Show 2022에서 전시되었습니다.

- 브라질은 남미에서 가장 큰 골판지 시장 중 하나입니다. 브라질 지역 통계 연구소의 추정에 따르면 브라질의 시트 및 골판지 포장 생산량은 2018년28 억 9,000만 달러에서 2023년에는 31 억 8,000만 달러로 증가할 것으로 예상됩니다.

- 브라질의 전자상거래 시장은 2021년 상반기에 31% 성장했으며, 2020년에는 이미 40% 성장했습니다. 경쟁이 치열한 오늘날의 FMCG 시장에서 기업이 경쟁사와 차별화하고 시장에서 브랜드 이미지를 유지하기 위해서는 매력적인 포장을 사용하고 포장에 혁신을 가져 오는 것이 불가피합니다.

- 자동차 산업은 국내에서 접착제 및 실란트를 널리 사용하는 또 다른 주요 부문으로, OICA에 따르면 2022년 승용차와 상용차를 포함한 총 자동차 생산량은 2,360 만대로 2021년대비 5% 증가했으며, 2021년총 자동차 생산량은 약 224 만대로 추정됩니다. 추정되고 있습니다.

- 이 나라는 이 지역에서 성숙한 의약품 시장입니다. 이 나라 시장은 국내 대형 벤더 덕분에 의약품 포장 제품을 중심으로 다양한 제품 혁신을 확인했습니다.

- 또한 브라질 병원연맹, 브라질 국민보건연맹, 브라질 보건부에 따르면 브라질의 병원 수는 2022년 7,191개에 달할 것으로 예상됩니다. 이러한 병원의 성장은 의약품 포장에 대한 수요 증가에 대응하기 위해 전국적으로 의약품 포장 공급업체에 대한 기회를 증가시킬 것으로 보입니다.

- 위의 모든 요인은 모두 중국의 접착제 및 실란트 수요에 큰 영향을 미치고 있습니다.

남미의 접착제 및 실란트 산업 개요

남미의 접착제 및 실란트 시장은 그 특성상 세분화되어 있습니다. 주요 기업으로는 Henkel AG &Co.KGaA, 3M, H.B. Fuller Company, Arkema, Sika AG 등이 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 성과

- 조사 전제

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 성장 촉진요인

- 브라질 건설 산업에서의 수요 증가

- 포장 산업용도 확대

- 기타 촉진요인

- 성장 억제요인

- VOC 배출에 관한 엄격한 환경 규제

- 기타 억제요인

- 산업 밸류체인 분석

- Porter의 Five Forces 분석

- 공급 기업의 교섭력

- 바이어의 교섭력

- 신규 진출업체의 위협

- 대체품의 위협

- 경쟁 정도

제5장 시장 세분화(금액 기준 시장 규모)

- 접착제 수지

- 폴리우레탄

- 에폭시

- 아크릴

- 실리콘

- 시아노아크릴레이트

- VAE·EVA

- 기타 수지(폴리에스테르, 고무 등)

- 접착 기술

- 용제계

- 반응성

- 핫멜트

- UV 경화형 접착제

- 실란트 수지

- 실리콘

- 폴리우레탄

- 아크릴

- 에폭시 수지

- 기타 수지(역청, 폴리 설파이드 UV 경화형 등)

- 최종사용자 산업

- 항공우주

- 자동차

- 건축 및 건설

- 신발·피혁

- 의료

- 포장

- 목공·창호

- 기타 최종사용자 산업(일렉트로닉스, 소비자/DIY 등)

- 지역

- 아르헨티나

- 브라질

- 콜롬비아

- 기타 남미

제6장 경쟁 구도

- 인수합병(M&A)/합작투자(JV)/협업/협정

- 시장 점유율(%)**/순위 분석

- 주요 기업의 전략

- 기업 개요

- 3M

- Arkema Group

- Ashland

- Avery Dennison Corporation

- Beardow Adams

- Dow

- DuPont

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Hexion

- Huntsman International LLC

- ITW Performance Polymers(Illinois Tool Works Inc.)

- Jowat AG

- Mapei Inc.

- Tesa SE(A Beiersdorf Company)

- Pidilite Industries Ltd

- RPM International Inc.

- Sika AG

- Wacker Chemie AG

제7장 시장 기회와 향후 동향

- 바이오 접착제 혁신과 개발

- 복합재료 접착에의 시프트

The South America Adhesives And Sealants Market size is estimated at USD 4.27 billion in 2025, and is expected to reach USD 5.45 billion by 2030, at a CAGR of greater than 5% during the forecast period (2025-2030).

The South American adhesives and sealants market was significantly affected by the COVID-19 pandemic, bringing both challenges and opportunities. Lockdowns and disruptions in industries like construction and manufacturing initially reduced demand. However, the pandemic simultaneously increased the need for adhesives and sealants in manufacturing medical supplies, personal protective equipment, and hygiene products. Despite the initial setbacks, the market is anticipated to recover and exhibit long-term growth.

The demand for adhesives and sealants is extensively driven by the growing demand from the construction industry and increasing healthcare infrastructure.

However, the market growth is likely to be hindered by the stringent VOC emissions regulations related to adhesives and sealants.

The innovation and development of bio-based adhesives and shifting focus toward adhesive bonding for composite materials are likely to offer opportunities for the adhesives and sealants market in the region.

Brazil stands to be the largest market for adhesives and sealants in the region, where the end-user industries, such as construction, aerospace, and automotive, majorly drive consumption.

South America Adhesives and Sealants Market Trends

The Building and Construction Industry to Dominate the Market

- Adhesives and sealants have been extensively used in the building and construction industry owing to their characteristics and physical properties. These properties include good adhesion and elasticity, cohesion, high cohesive strength, flexibility, the high elastic modulus of the substrate, resistance from thermal expansion, and environmental resistance from UV light, corrosion, salt water, rain, and other weathering conditions.

- In 2022, the South American region will see a tremendous increase in construction activities. The reason for this is the rebounding from the impact of lockdowns and restrictions imposed by the government during the pandemic year.

- According to the Chilean Chamber of Construction (CChC), the Construction Materials and Supplies Price Index (IPMIC) rose by 5.9% YoY in the first three months of 2023.

- Brazil is the primary and most significant construction and real estate market in the region. However, the country's recession and weak economic conditions are expected to hamper the growth of the region's construction industry.

- In Brazil, the government launched an infrastructure concessions program with an aim to develop the country's port, road, railway, power transmission lines, and sanitation infrastructure. Under this plan, the government aims to invest BRL 45.0 billion (USD 14.1 billion) through the public-private partnership (PPP) model. Furthermore, government programs such as Minha Casa Minha Vida (MCMV), Plano Decenal de Expansao de Energia 2026, and the National Education Plan are expected to support industry growth over the forecast period.

- Furthermore, in 2022, there will be a tremendous rise in industrial construction in Brazil. BSBios, an agribusiness chain company, is planning to construct a wheat ethanol plant in Brazil. Nordic Impact Cooperation (NIC), a major investment company, has invested in the construction of six solar PV plants with a capacity of 18MW in Brazil.

- All of the above thin Brazil factors are likely to increase the demand for adhesives and sealants in the region during the forecast period.

Brazil to Dominate the Demand in South American Region

- Brazil is the country with the highest consumption of adhesives in South America. Packaging, automotive, construction, and other sectors rely heavily on adhesives.

- Brazil's growth is fueled mainly by rapid expansion in the residential and commercial building sectors and the country's expanding economy.

- According to the Brazilian government, USD 866 million was invested in 762 infrastructure projects in 2022 to upgrade the state of Brazilian tourist cities and maximize the potential of the industry, drawing more tourists and providing them with a more comfortable stay.

- Brazil's paper and pulp sector is one of the country's most successful agricultural exports, ranking high on the list of nations that generate this kind of product. Cartons can be made from various materials such as paperboard, duplex, white kraft, recycled materials, or composite. Combistyle carton packaging was introduced in May 2022 by SIG, along with Frimesa, one of the largest milk producers in Brazil. These carton packs were showcased at APAS Show 2022, the biggest F&B trade show in the Americas, held in So Paulo, Brazil.

- Brazil is one of South America's largest markets for corrugated cardboard. According to estimates from the Brazilian Institute of Geography and Statistics, Brazil's production of sheets and corrugated cardboard packaging is expected to rise from USD 2.89 billion in 2018 to USD 3.18 billion in 2023.

- The Brazil e-commerce market grew by 31% in the first half of 2021, and in 2020, it had already grown by 40%. In today's competitive FMCG market, it has become inevitable for companies to use attractive packaging and bring innovation to their packaging to stand out from their competitors and maintain their brand image in the market.

- The automotive industry is another primary sector that uses adhesives and sealants extensively in the country. According to OICA, the total production of automotive, including passenger cars and commercial vehicles, in 2022 was 2.36 million units, registering a 5% growth in production compared to 2021. In 2021, the total automotive production was estimated to be around 2.24 million units.

- The country is a mature pharmaceutical market in the region. The market in the country witnessed various product innovations, especially pharmaceutical packaging products, owing to significant vendors across the country.

- Furthermore, according to the Brazilian Federation of Hospitals, National Health Confederation (Brazil), and Ministry of Health (Brazil), the number of hospitals in Brazil reached 7,191 in 2022. Such growth in hospitals would increase the opportunities for pharmaceutical packaging vendors nationwide to serve the growing need for prescribed pharmaceuticals.

- All the factors above have a significant impact on the demand for adhesives and sealants in the country.

South America Adhesives and Sealants Industry Overview

The South American adhesives and sealants market is fragmented in nature. The major players (not in any particular order) include Henkel AG & Co. KGaA, 3M, H.B. Fuller Company., Arkema and Sika AG.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Report

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Rising Demand from the Construction Industry in Brazil

- 4.1.2 Growing Usage in the Packaging Industry

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Stringent Environmental Regulations Regarding VOC Emissions

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Adhesives Resin

- 5.1.1 Polyurethane

- 5.1.2 Epoxy

- 5.1.3 Acrylic

- 5.1.4 Silicone

- 5.1.5 Cyanoacrylate

- 5.1.6 VAE/EVA

- 5.1.7 Other Resins (Polyester, Rubber, etc.)

- 5.2 Adhesives Technology

- 5.2.1 Solvent-borne

- 5.2.2 Reactive

- 5.2.3 Hot Melt

- 5.2.4 UV-Cured Adhesives

- 5.3 Sealant Resin

- 5.3.1 Silicone

- 5.3.2 Polyurethane

- 5.3.3 Acrylic

- 5.3.4 Epoxy

- 5.3.5 Other Resins (Bituminous, Polysulfide UV-Curable, etc.)

- 5.4 End-user Industry

- 5.4.1 Aerospace

- 5.4.2 Automotive

- 5.4.3 Building and Construction

- 5.4.4 Footwear and Leather

- 5.4.5 Healthcare

- 5.4.6 Packaging

- 5.4.7 Woodworking and Joinery

- 5.4.8 Other End-user Industries (Electronics, Consumer/DIY, etc.)

- 5.5 Geography

- 5.5.1 Argentina

- 5.5.2 Brazil

- 5.5.3 Colombia

- 5.5.4 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Arkema Group

- 6.4.3 Ashland

- 6.4.4 Avery Dennison Corporation

- 6.4.5 Beardow Adams

- 6.4.6 Dow

- 6.4.7 DuPont

- 6.4.8 H.B. Fuller Company

- 6.4.9 Henkel AG & Co. KGaA

- 6.4.10 Hexion

- 6.4.11 Huntsman International LLC

- 6.4.12 ITW Performance Polymers (Illinois Tool Works Inc.)

- 6.4.13 Jowat AG

- 6.4.14 Mapei Inc.

- 6.4.15 Tesa SE (A Beiersdorf Company)

- 6.4.16 Pidilite Industries Ltd

- 6.4.17 RPM International Inc.

- 6.4.18 Sika AG

- 6.4.19 Wacker Chemie AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Innovation and Development of Bio-based Adhesives

- 7.2 Shifting Focus Toward Adhesive Bonding for Composite Materials