|

시장보고서

상품코드

1628755

조톨유 유도체 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Crude Tall Oil Derivatives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

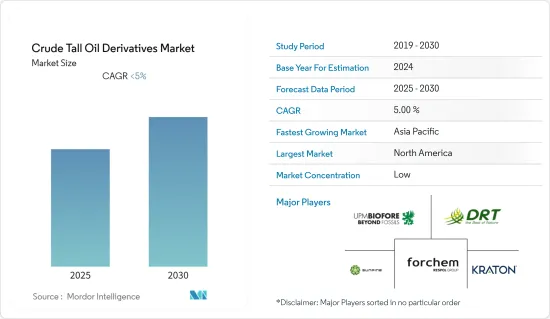

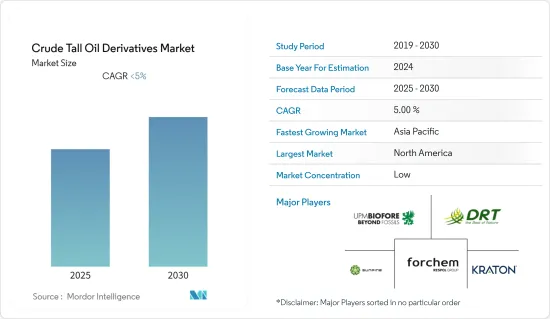

조톨유 유도체 시장은 예측 기간 동안 CAGR 5% 이하를 기록할 것으로 예상됩니다.

주요 하이라이트

- 2020년, 코로나19는 다양한 산업공급망 혼란으로 인해 산업 성장에 심각한 영향을 미쳤습니다. 그러나 팬데믹 이후 자동차 생산이 활성화되면서 전체 산업의 성장을 견인했습니다.

- 시장 성장을 가속하는 주요 요인은 최종 사용자 산업에서 바이오 화학제품에 대한 수요 증가와 자동차 산업에서 조잡한 톨루엔 유도체 사용 확대입니다. 반면, 조잡한 톨루엔 원료를 바이오디젤 용도로 더 많이 전환하는 것은 시장 성장을 저해하는 요인으로 작용할 것으로 예상됩니다.

- 아시아태평양 및 북미의 석유 및 가스 프로젝트 확대는 예측 기간 동안 새로운 성장 기회를 제공할 것으로 보입니다. 북미가 세계를 지배하고 있으며, 미국이 가장 많은 소비를 하고 있습니다.

조잡한 톨루엔유 유도체 시장 동향

TOFA 부문이 시장을 독점

- 전 세계적으로 유럽연합(EU)과 미국은 톨루엔 지방산의 주요 생산국이자 소비국입니다. 따라서 톨루엔 지방산의 순 국제 무역은 거의 없으며 수입 의존도는 제로입니다. EU에서 연간 2 킬로톤의 톨루엔 지방산이 윤활유로 생산되고 있으며, 톨루엔 지방산 생산의 대부분은 북유럽 국가들에서 이루어지고 있습니다.

- Kraton Corporation, Ingevity, Chemceed, Forchem Oyj, Spectrum Chemical Mfg Corp, Industrial Oleochemical Products, Parchem Fine &Specialty Chemicals가 TOFA 생산에 참여하는 주목할 만한 신규 진출기업입니다.

- 2017년 10월 미국 환경보호청(EPA)은 다음과 같은 상황에서 불활성 성분(용매/담체)으로 사용되는 경우 톨루엔 지방산 잔류물에 대한 허용 요건 면제 규정을 제정했다: 수확 후 재배 작물 및 생농산물에 적용되는 농약 제제, 동물에/동물에 적용되는 농약, 식품 접촉면의 항균제.

- Ingevity Corporation은 연방 식품, 의약품 및 화장품법(Federal Food, Drug, and Cosmetic Act: FFDCA)에 따라 EPA에 신청서를 제출하여 공차 요건에서 이러한 적용 제외를 요청했습니다. 이 규정에 따라, 이 면제 조건에 부합하는 톨루엔 지방산 잔류량에 대한 최대 허용치를 설정할 필요가 없어졌습니다. 이러한 새로운 예외조항은 지난 2년간 북미 시장 성장을 가속했습니다.

- 자동차 산업이 성장함에 따라 윤활유 수요도 증가할 것으로 예상됩니다. 유럽 연합, 미국, 아시아태평양을 포함한 다양한 지역의 자동차 생산 및 판매 급증은 윤활유 수요를 주도하고 있습니다.

- 2020년 1-3분기 유럽 연합에서 생산된 자동차는 거의 800만 대에 달하고, 2021년 같은 기간보다 5.8% 증가했습니다. 한편, 2022년 1-9월 유럽 연합에 등록된 상용차는 120만 대에 달하고, 전년 동기 대비 17.6% 감소했습니다.

- 북미 자동차 생산량은 2022년 1-9월에 11.8% 증가하여 약 800만 대를 기록했습니다. 또한 미국에서는 2020년 코로나19 사태 이후 2021년 자동차 생산량이 917만 대까지 증가했습니다. 또한 2022년 1월부터 9월까지 중국의 누적 등록대수는 8.2% 증가한 1,530만 대를 넘어섰습니다. 또한 중국의 자동차 생산량은 1월부터 9월까지 누적 생산량이 1,640만 대에 달하는 등 강한 회복세를 보였습니다.

- 따라서 이러한 요인들은 윤활유 내 전유 지방산의 소비를 증가시켜 전체 산업의 성장을 가속할 것으로 예상됩니다.

북미 시장을 장악하고 있는 미국

- 미국은 세계 최대 경제대국으로 2021년 경제 성장률이 연 5.7%로 1984년 이후 가장 강력한 경제대국이 될 조짐을 보이고 있습니다. 미국은 첨단 기술 연구 개발 및 혁신에 있어서는 매우 의존도가 높습니다. 그러나 지난 10년간 제조업은 멕시코, 캐나다, 중국, 인도 등 다른 국가로 이동했습니다.

- 이 점에서 현 정부는 국내 제조업을 활성화하고 고급 제품 생산기지로 만들기 위해 노력하고 있으며, 2021년 미국은 자동차 생산량이 2020년 대비 약 4% 증가하여 윤활유 생산 및 판매 경사로 이어졌습니다. 2021년 미국 정유소의 윤활유 순생산량은 하루 16만 8,000배럴로 전년 대비 약 10.5% 증가하여 최근 몇 년동안 미국의 높은 원유 소비량을 줄였습니다.

- 금속 가공유에 대한 수요를 크게 견인하는 것은 자동차 산업과 장비 제조 산업입니다. 미국은 건설 및 산업용 고급 기술 및 장비의 개발 및 생산으로 잘 알려져 있으며, 금속 가공 오일의 주요 소비국 중 하나입니다.

- 미국에서는 지난 수십년동안 석유 및 가스 산업이 강력한 성장을 이루며 산업 성장을 견인해 왔습니다. 2021년 미국의 석유 생산량은 약 7억 1,100만 톤으로 전년 대비 소폭 감소할 것으로 예상됩니다. 또한 미국의 원유 생산량은 2022년 1,170만 배럴/일, 2023년 1,240만 배럴/일로 2019년 기록한 사상 최고치를 넘어설 것으로 예상됩니다.

- 따라서, 이러한 모든 추세는 예측 기간 동안 바이오디젤, 금속 가공유, 유전 화학제품, 광산 화학제품, 페인트, 코팅제, 접착제 등 산업용 제품 생산에 사용되는 조잡한 톨루엔 유도체에 대한 수요와 소비를 증가시킬 것으로 예상됩니다.

조잡한 톨루엔유 유도체 산업 개요

조톨유 유도체 시장은 부분적으로 통합되어 있으며, 주요 5개 기업이 큰 점유율을 차지하고 있습니다. 조톨유 유도체 시장의 주요 기업으로는 Kraton corporation, Forchem Oyj, UPM, Les Derives Resiniques Et Terpeniques, SunPine AB 등이 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 성장 촉진요인

- 최종사용자 산업 바이오 화학제품 수요 증가

- 자동차 산업용도 증가

- 기타 촉진요인

- 성장 억제요인

- 조제 톨유 원료 바이오디젤 용도에의 이용 확대

- 기타 억제요인

- 산업 밸류체인 분석

- Porter의 Five Forces 분석

- 공급 기업의 교섭력

- 소비자의 교섭력

- 신규 진출업체의 위협

- 대체품의 위협

- 경쟁 정도

- 특허 분석

- 원료 분석

- 생산 분석

- 무역 분석

제5장 시장 세분화(시장 규모(수량))

- fraction

- 사용료 오일 피치(TOP)

- 톨유 로진(TOR)

- 증류 톨유(DTO)

- 톨유 지방산(TOFA)

- 최종사용자 산업

- 자동차

- 바이오디젤(연료)

- 윤활유

- 타이어 제조(고무)

- 특수화학제품 및 석유화학제품

- 플라스틱

- 금속 가공 유제

- 비누 및 세제

- 코팅

- 인쇄 잉크

- 종이 사이즈

- 접착제

- 석유 및 가스·광업

- 석유 시추

- 광업 부유

- 기타

- 스테로르

- 추잉껌

- 기타

- 자동차

- 지역

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 기타 북미

- 유럽

- 독일

- 프랑스

- 영국

- 스페인

- 핀란드

- 스웨덴

- 기타 유럽

- 기타

- 브라질

- 남아프리카공화국

- 기타 국가

- 아시아태평양

제6장 경쟁 구도

- 인수합병(M&A)/합작투자(JV)/협업/협정

- 시장 점유율(%)**/순위 분석

- 주요 기업의 전략

- 기업 개요

- Eastman Chemical Company

- Forchem Oyj

- Ingevity

- Kraton Corporation

- Les Derives Resiniques Et Terpeniques

- Mercer International Inc.

- Neste

- Ooo Torgoviy Dom Lesokhimik

- Pine Chemical Group Oy

- Segezha Group

- Sunpine AB

- UPM

제7장 시장 기회와 향후 동향

- 아시아태평양과 북미 석유 및 가스 프로젝트 확대

The Crude Tall Oil Derivatives Market is expected to register a CAGR of less than 5% during the forecast period.

Key Highlights

- In 2020, the pandemic severely impacted industry growth due to supply chain disruption across various industries. However, ramping automotive production post-pandemic propelled the overall industry growth.

- The major factors driving the market's growth are the increasing demand for bio-based chemicals in end-user industries and the rising application of crude tall oil derivatives in the automotive industry. On the flip side, directing crude tall oil feedstock more into biodiesel applications is expected to hinder the market's growth.

- The oil and gas project expansions in Asia-pacific and North America will likely offer new growth opportunities during the forecast period. North America dominates the world, with the largest consumption from the United States.

Crude Tall Oil Derivatives Market Trends

TOFA Segment to Dominate the Market

- Globally, the European Union (EU) and the United States are key producers and consumers of tall oil fatty acids. This implies little net international trade in tall oil fatty acids, resulting in zero import dependence. Tall oil fatty acids have a production volume for use as lubricants of 2-kilo metric tons/annum in the EU, and the majority of tall oil fatty acid production also takes place in Nordic countries.

- Kraton Corporation, Ingevity, Chemceed, Forchem Oyj, Spectrum Chemical Mfg Corp, Industrial Oleochemical Products, and Parchem Fine & Specialty Chemicals are the notable players involved in the production of TOFAs.

- In October 2017, the Environmental Protection Agency (EPA) enacted a regulation for exemptions from the requirement of a tolerance for residues of tall oil fatty acids when used as inert ingredients (solvent/carrier) in the following circumstances: in pesticide formulations applied to growing crops and raw agricultural commodities after harvest, in pesticides applied in/on animals, and in antimicrobial formulations for food contact surfaces.

- Ingevity Corporation submitted a petition to EPA under the Federal Food, Drug, and Cosmetic Act (FFDCA), requesting the establishment of these exemptions from the requirement of a tolerance. This regulation eliminates the need to establish maximum permissible levels for residues of tall oil fatty acids that are consistent with the conditions of these exemptions. These new exemptions have been encouraging market growth in North America for the past two years.

- With the growing automotive industry, the demand for lubricants is also expected to increase. The surging automotive production and sales in various regions, including the European Union, the United States, and the Asia-Pacific, drive the demand for lubricants.

- During the first three quarters of 2022, nearly 8 million cars were manufactured in the European Union, 5.8% more than during the same period in 2021. In contrast, 1.2 million commercial vehicles were registered in the European Union from January to September 2022, a year-on-year decline of 17.6%.

- North American output increased by 11.8% during the first nine months of 2022 - to nearly 8 million cars. Additionally, in the United States, automotive production increased to 9.17 million units in 2021 after the pandemic in 2020. Furthermore, in 2022, from January to September, cumulative volumes in China increased by 8.2% to more than 15.3 million cars registered. Additionally, Chinese car production rebounded strongly to reach 16.4 million units from January to September.

- Therefore, these factors are projected to boost the consumption of total oil fatty acid in lubricants, propelling the overall industry growth.

United States to Dominate the North America Market

- The United States is the world's largest and most powerful economy. In 2021, the economy increased by an annualized 5.7%. There were signs that the economy was the strongest since 1984. The country is highly relied on when it comes to R&D and innovation of advanced technologies. However, in the past decade, the country has shifted the manufacturing sector to other nations, such as Mexico, Canada, China, India, etc.

- In this regard, the present government has been making efforts to revitalize the manufacturing sector in the country and make the country a manufacturing hub of high-end products. In 2021, the United States recorded about a 4% increase in automotive production over 2020. This led to the country's inclining production and sales of lubricants. In 2021, the refinery's net production of lubricants stood at 168 thousand barrels per day, up by roughly 10.5 percent from the previous year in the country, reducing the consumption of crude tall in the country in recent years.

- The automotive and equipment manufacturing industries significantly drive the demand for metalworking fluid. The United States is well-known for advancing and producing high-end technologies and equipment for construction and industrial use, making the country one of the major consumers of metalworking fluids, further driving its production at a moderate rate in the domestic market.

- Strong growth in the oil and gas industry in the last few decades in the country has propelled the industry growth. Oil production in the United States amounted to some 711 million metric tons in 2021, a slight decrease compared to the previous year. Additionally, US crude oil production was 11.7 million b/d in 2022 and is forecasted to reach 12.4 million b/d in 2023, surpassing the record high set in 2019.

- Hence, all such trends in the country are anticipated to increase the demand and consumption of crude tall oil derivatives used in producing industrial products, such as biodiesel, metalworking fluids, oilfield chemicals, mining chemicals, paints, coatings, adhesives, etc., during the forecast period.

Crude Tall Oil Derivatives Industry Overview

The crude tall oil derivatives market is partially consolidated, with the top five players accounting for a significant share. Key players in the crude tall oil derivative market include Kraton corporation, Forchem Oyj, UPM, Les Derives Resiniques Et Terpeniques, and SunPine AB, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand For Bio-based Chemicals In End-user Industries

- 4.1.2 Rising Application in the Automotive Industry

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Directing Crude Tall Oil Feedstock More Into Biodiesel Application

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Patent Analysis

- 4.6 Raw Material Analysis

- 4.7 Production Analysis

- 4.8 Trade Analysis

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Fraction

- 5.1.1 Tall Oil Pitch (TOP)

- 5.1.2 Tall Oil Rosin (TOR)

- 5.1.3 Distilled Tall Oil (DTO)

- 5.1.4 Tall Oil Fatty Acid (TOFA)

- 5.2 End-user Industry

- 5.2.1 Automotive

- 5.2.1.1 Bio-diesel (fuel)

- 5.2.1.2 Lubricant

- 5.2.1.3 Tire Manufacturing (rubber)

- 5.2.2 Specialty Chemicals & Petrochemicals

- 5.2.2.1 Plastics

- 5.2.2.2 Metalworking Fluids

- 5.2.2.3 Soap & Detergents

- 5.2.2.4 Coatings

- 5.2.2.5 Printing inks

- 5.2.2.6 Paper Sizing

- 5.2.2.7 Adhesives

- 5.2.3 Oil & Gas and Mining

- 5.2.3.1 Oil Drilling

- 5.2.3.2 Mining flotation

- 5.2.4 Other End-user Industries

- 5.2.4.1 Sterols

- 5.2.4.2 Chewing gum

- 5.2.4.3 Other End Users

- 5.2.1 Automotive

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Rest of North America

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 France

- 5.3.3.3 United Kingdom

- 5.3.3.4 Spain

- 5.3.3.5 Finland

- 5.3.3.6 Sweden

- 5.3.3.7 Rest of Europe

- 5.3.4 Rest of the World

- 5.3.4.1 Brazil

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of the Countries

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Eastman Chemical Company

- 6.4.2 Forchem Oyj

- 6.4.3 Ingevity

- 6.4.4 Kraton Corporation

- 6.4.5 Les Derives Resiniques Et Terpeniques

- 6.4.6 Mercer International Inc.

- 6.4.7 Neste

- 6.4.8 Ooo Torgoviy Dom Lesokhimik

- 6.4.9 Pine Chemical Group Oy

- 6.4.10 Segezha Group

- 6.4.11 Sunpine AB

- 6.4.12 UPM

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Oil and Gas Project Expansions in Asia-pacific And North America

샘플 요청 목록