|

시장보고서

상품코드

1629812

음료용 뚜껑 및 마개 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Beverage Caps And Closures - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

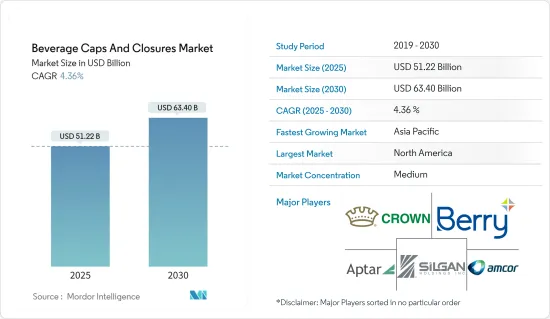

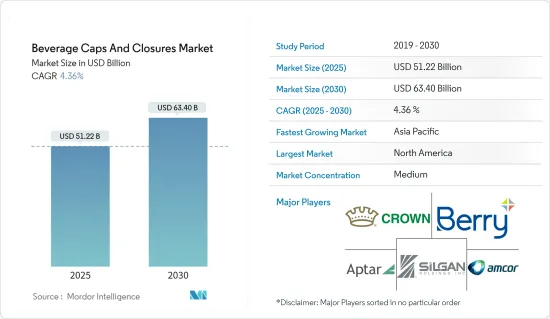

음료용 뚜껑 및 마개 시장 규모는 2025년 512억 2,000만 달러로 추정되며, 예측 기간(2025-2030년) 동안 4.36%의 CAGR로 2030년에는 634억 달러에 달할 것으로 예상됩니다.

주요 하이라이트

- 뚜껑 및 마개는 음료의 종류와 포장재에 관계없이 음료의 유출을 방지하고 제품의 신선도를 유지하는 데 매우 중요합니다. 이러한 부품은 유통기한을 연장하고 밀봉을 통해 미생물 오염으로부터 보호합니다. 미국에서 플라스틱 뚜껑 및 마개에 대한 수요는 편의성과 사용 편의성에 대한 소비자 선호가 주요 요인으로 작용하고 있습니다. 플라스틱 캡은 오염 물질과 미생물로부터 제품을 효과적으로 보호합니다. 또한, 플라스틱 뚜껑 및 마개는 금속 뚜껑 및 마개에 비해 비용 면에서 유리합니다.

- 뚜껑 및 마개에 대한 세계 수요는 사용 편의성과 지속가능한 포장 품질로 인해 증가하고 있으며, PET와 PP는 제조에 사용되는 주요 원료입니다. 이 부품은 음료 산업에서 알코올 및 무알콜 제품 모두에 널리 사용됩니다. 뚜껑 및 마개는 제품의 유통기한을 연장하고, 오염물질과 습기로부터 보호하고, 포장된 제품의 산소 농도를 조절하는 등 여러 가지 기능을 수행합니다. 수요가 지속적으로 증가함에 따라 예측 기간 동안 시장은 더욱 성장할 것으로 예상됩니다.

- 생수는 양적으로 가장 빠르게 성장하는 음료 카테고리 중 하나입니다. 생수에 대한 소비자 수요가 증가함에 따라 예측 기간 동안 개봉 방지 뚜껑 및 마개에 대한 수요가 증가할 것으로 예상됩니다. 소비자들 사이에서 건강과 웰빙에 대한 인식이 높아지면서 단 음료에서 더 건강한 대안으로 전환하고 있으며, 생수는 이러한 추세의 주요 수혜자입니다. 또한, 일부 지역에서는 수질에 대한 우려로 인해 생수에 대한 수요가 더욱 증가하고 있으며, 이에 따라 강력한 포장 솔루션이 필요합니다.

- 현대 소비자의 '이동 중' 라이프스타일은 가볍고 사용하기 편리한 포장 솔루션에 대한 수요를 증가시키고 있습니다. 맞춤형 뚜껑 및 마개 제조업체들은 보다 가볍고 효율적인 디자인으로 대응하고 있습니다. 다양한 종류의 음료에 대한 수요 증가로 인해 세계 시장의 성장이 더욱 가속화되고 있습니다. 이러한 추세는 재활용 가능한 재료와 E-Commerce의 요구를 충족시키는 디자인과 같은 포장 혁신으로 이어지고 있습니다. 커스텀 뚜껑 및 마개 시장은 소비자의 취향과 다양한 산업의 제품 요구 사항을 충족시키기 위해 계속 진화하고 있습니다.

- 또한, 생활 패턴의 변화와 1인당 소비량 증가는 생수 시장 확대에 박차를 가하고 있습니다. 도시화, 바쁜 라이프스타일, 생수의 편리함이 그 인기에 기여하고 있습니다. 소비자들이 이동 중에도 수분을 보충하는 것을 선택함에 따라 제조업체들은 다양한 크기의 병과 혁신적인 마개 디자인을 제공하여 제품의 안전성과 사용 편의성을 보장하기 위해 대응하고 있습니다. 이러한 추세는 앞으로도 지속될 것으로 예상되며, 생수 포장용 변조 방지 뚜껑 및 마개 시장의 성장을 더욱 촉진할 것으로 보입니다.

- 플라스틱 포장의 기술 발전은 산업 내 제품 개발에서 큰 혁신을 가져왔습니다. 많은 기업들이 독특하고 비용 효율적인 제품을 생산하기 위해 연구 개발 활동에 많은 투자를 하고 있으며, 그 결과 시장의 혁신이 이루어지고 있습니다. 그러나 기후 변화에 대한 우려가 커지면서 포장용 플라스틱 사용에 대한 정부 규제가 강화되고 있습니다. 이러한 규제는 예측 기간 동안 음료용 뚜껑 및 마개 시장의 성장에 주요 제약요인으로 작용할 것으로 예상됩니다.

음료용 뚜껑 및 마개 시장 동향

생수 부문이 큰 시장 점유율을 차지

- 생수 시장은 미국과 같은 선진국 시장과 인도, 인도네시아와 같은 신흥국 시장에서 주요 음료 유형 중 가장 큰 폭의 성장을 기록할 것으로 예상됩니다. 이러한 성장의 원동력은 건강에 대한 인식 증가, 편의성, 일부 지역의 수돗물 수질에 대한 우려 등으로, 2023 회계연도에 Indian Railways Catering &Tourism Corporation Ltd. 생산할 계획입니다. (IRCTC)는 3억 5,700만 병 이상의 생수를 생산했으며, 이는 2022년의 1억 9,860만 병에서 거의 두 배로 증가한 수치입니다. 이는 인도 생수 시장의 급격한 성장세를 반영하는 것입니다.

- 생수 시장의 확대는 특히 생수 부문에서 플라스틱 뚜껑 및 마개에 대한 수요를 증가시키고 있습니다. 뚜껑 및 마개는 생수의 품질과 안전성을 유지하고 오염을 방지하며 신선도를 보장하는 데 중요한 역할을 합니다. 전 세계적으로 생수 소비가 지속적으로 증가함에 따라 플라스틱 뚜껑 및 마개 제조업체는 지속적인 성장 기회를 누릴 수 있을 것으로 보입니다. 이러한 추세는 변조 방지 기능 및 개선된 밀봉 기술 등 제품 안전과 소비자 신뢰도를 높이는 캡 디자인의 혁신으로 인해 더욱 가속화되고 있습니다.

- 음료 시장에서는 유리 용기에서 플라스틱 용기로의 전환이 진행되고 있으며, 이는 플라스틱 뚜껑 및 마개에 대한 수요를 증가시킬 것으로 예상됩니다. 이러한 전환은 가벼운 무게와 파손으로 인한 제품 손실을 줄일 수 있는 플라스틱의 장점에 의해 촉진되고 있습니다. 더 넓은 시장에서는 금속 캡이 특히 맥주 병에 선호되는 마개로 계속 우위를 차지할 것으로 보입니다. 와인 산업에서는 주로 일회용 와인 병의 인기가 높아지면서 금속 롤온 스크류 캡의 사용이 증가할 것으로 예상됩니다.

- 또한, 생수는 전 세계적으로 가장 빠르게 성장하고 있는 음료 카테고리 중 하나입니다. 생수에 대한 소비자 수요가 증가함에 따라 예측 기간 동안 개봉 방지 뚜껑 및 마개에 대한 수요가 증가할 것으로 예상됩니다. 생수 시장의 성장은 라이프스타일의 변화와 1인당 소비량 증가로 인해 촉진될 것입니다. 코카콜라, 다논, 네슬레, 펩시콜라, 농푸스프링(PepsiCo), 농푸스프링(Nongfu Spring)과 같은 국제적인 경쟁업체들의 존재감이 높아짐에 따라 생수 시장 내 경쟁업체들 간의 적대적 관계는 더욱 심화되고 있습니다.

- 플라스틱 포장의 기술 발전은 음료 산업의 제품 개발에 혁신을 가져왔습니다. 많은 기업들이 독특하고 비용 효율적인 제품을 개발하기 위해 연구 개발 활동에 많은 투자를 하고 있으며, 이 부문의 기술 혁신이 눈에 띄게 증가하고 있습니다.

- Amcor 및 Ball과 같은 다른 많은 대기업들도 비슷한 전략을 취하여 새롭고 혁신적인 최종 제품을 제공하고 있습니다. 산업의 혁신과 함께 제품에 대한 수요가 증가함에 따라 전 세계 음료 산업에서 뚜껑 및 마개의 성장을 주도하고 있습니다.

아시아태평양, 큰 성장세를 기록

- 아시아태평양 뚜껑 및 마개 시장은 중국이 주도하고 있으며 인도와 일본이 근소한 차이로 뒤를 잇고 있습니다. 몇 가지 중요한 요인이 이러한 선도적 지위를 뒷받침하고 있습니다. 첫째, 음료 산업에서 생수 및 포장 음료에 대한 수요가 증가함에 따라 시장이 크게 성장하고 있습니다. 둘째, 뚜껑 및 마개 제조에 고성능 소재를 사용함으로써 제품의 품질과 기능이 향상되고 있습니다. 셋째, 이 시장은 다양한 재료 구성의 혜택을 누리고 있으며, 이는 다양한 포장 솔루션의 다양성을 가능하게 합니다.

- 중국의 경제 성장은 시장 상황 형성에 중요한 역할을 하고 있습니다. 중국 경제가 빠르게 성장함에 따라 중산층 가정의 가처분 소득이 크게 증가했습니다. 이러한 구매력 증가로 인해 음료수를 중심으로 한 포장 제품 소비가 증가하여 뚜껑 및 마개에 대한 수요를 주도하고 있습니다. 이러한 추세는 앞으로도 지속될 것으로 예상되며, 아시아 지역의 시장 리더로서 중국의 입지를 더욱 공고히 할 것으로 보입니다.

- 아시아태평양의 뚜껑 및 마개 시장은 주로 음료 소비 증가와 인구 증가로 인해 확대되고 있습니다. 이 지역의 음료 산업은 가처분 소득의 증가로 인해 지난 10년간 엄청난 성장을 이루었습니다. 이러한 추세는 소비자의 선호도 변화, 특히 에너지 및 영양 음료에 대한 수요 증가에 영향을 받아 예측 기간 동안 계속될 것으로 예상됩니다.

- 이 지역의 플라스틱 뚜껑 및 마개 시장은 급속한 도시화, 인구 증가 및 알코올 수요 증가에 의해 주도되고 있습니다. 또한이 지역의 플라스틱 재활용 및 지속가능성을 중시하는 산업이 증가함에 따라 뚜껑 및 마개에 재활용 가능한 플라스틱 소재의 채택이 증가할 것으로 예상되며, 2023 회계 연도에 인도의 다양한 증류주 중 위스키가 2억 5, 000 만 케이스를 초과하여 가장 많은 양을 차지할 것으로 예상됩니다. 000만 케이스를 넘어설 것입니다. 반면 브랜디는 약 8,200만 케이스가 될 것으로 예상됩니다. 전체 증류주 시장 규모는 4억 케이스에 육박하고 있습니다. 이러한 추세는 다양한 주류에 대한 뚜껑 및 마개에 대한 수요를 창출하고 있습니다.

- Berrycup의 최근 조사에 따르면 중국의 중산층은 특히 캡이나 마개와 같은 플라스틱 부품이 필요한 포장 산업에서 더욱 정교한 제품을 요구하고 있습니다. 그 결과, 중국의 플라스틱 산업은 기술과 환경 친화적인 개념에 초점을 맞춘 종합적인 변화의 시기를 맞이하고 있습니다. 시장의 추세는 매력적인 색상과 인쇄로 향하고 있습니다. 제품의 색상, 모양, 질감, 그래픽 및 인쇄는 브랜드 식별을 전달하고 매장에서 경쟁사와 차별화하기 위해 기업은 눈길을 끄는 포장재 생산에 점점 더 많은 관심을 기울이고 있습니다.

음료용 뚜껑 및 마개 산업 개요

음료용 뚜껑 및 마개 시장은 세분화되어 있으며, 각 업체들은 경쟁력 있는 가격과 최첨단 제품을 제공함으로써 고객을 확보하기 위해 노력하고 있습니다. Global Closure Systems 등이 시장을 선도하고 있습니다. 이들은 R&D 투자, 신규 시장 진출, 세계 입지, 생산 기지 및 시설, 생산능력, 제품 출시 등으로 인해 시장 경쟁이 치열합니다.

- 2024년 6월, BERICAP은 아프리카, 남미, 동남아시아에 새로운 생산 시설을 설립하여 국제적인 발자취를 넓혔습니다. 이 회사는 케냐 나이로비와 베트남 호치민시에 새로운 공장을 설립하고 페루 리마와 남아프리카공화국 더반에 설립 된 생산 단위를 인수했습니다. 이러한 전략적 이전을 통해 벨리컵은 25개국에 30개의 생산 거점을 확보하게 되었으며, 고객들은 현지에 기반을 둔 프로젝트 지원, 물류 및 서비스 혜택을 누릴 수 있게 되었습니다.

- 2024년 3월, 와인 및 증류주용 마개 및 캡슐 분야의 세계 리더인 Amcor Capsules는 1964년 프랑스 샤론 쉬르 손에서 출시된 STELVIN 알루미늄 스크류 캡 시리즈 출시 60주년을 맞이했습니다. STELVIN 캡은 와인 산업에서 매우 중요한 진화의 선구자 역할을 했습니다.

기타 혜택

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 소개

- 조사 상정과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 산업 공급망 분석

- 산업의 매력 - Porter's Five Forces 분석

- 공급 기업의 교섭력

- 소비자의 협상력

- 신규 참여업체의 위협

- 대체품의 위협

- 경쟁 기업 간의 경쟁 관계

제5장 시장 역학

- 시장 성장 촉진요인

- 신흥 경제 국가의 음료 소비 증가

- 기술의 진보와 혁신적 포장 솔루션

- 시장 성장 억제요인

- 플라스틱 뚜껑 및 마개 사용에 관한 엄격한 규제

제6장 시장 세분화

- 재료별

- 금속

- 플라스틱

- 기타 재료(고무, 코르크)

- 용도별

- 맥주

- 와인

- 생수

- 탄산음료

- 유제품

- 조미료·소스

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 아시아태평양

- 중국

- 일본

- 인도

- 호주·뉴질랜드

- 라틴아메리카

- 브라질

- 멕시코

- 콜롬비아

- 중동 및 아프리카

- 아랍에미리트

- 사우디아라비아

- 남아프리카공화국

- 북미

제7장 경쟁 구도

- 기업 개요

- Crown Holdings Inc.

- Berry Global Inc.

- Aptar Group Inc.

- Global Closure Systems

- Silgan Holdings Inc.

- Bericap GmbH & Co. KG

- Guala Closures Group

- Ball Corporation

- Amcor Group

- Pact Group

- Albea Group

- Tetra Laval International

제8장 투자 분석

제9장 시장 기회와 향후 동향

ksm 25.01.23The Beverage Caps And Closures Market size is estimated at USD 51.22 billion in 2025, and is expected to reach USD 63.40 billion by 2030, at a CAGR of 4.36% during the forecast period (2025-2030).

Key Highlights

- Caps and closures are crucial in preventing beverage spillage and maintaining product freshness, regardless of the beverage type or packaging material. These components extend shelf life and protect against microbial contamination through tight seals. In the United States, the demand for plastic caps and closures is primarily driven by consumer preferences for convenience and ease of use. Plastic caps effectively shield products from contaminants and microorganisms. Additionally, plastic caps and closures offer a cost advantage over their metal counterparts.

- The global demand for caps and closures is increasing due to their ease of use and sustainable packaging qualities. PET and PP are the primary raw materials used in their manufacture. These components are extensively utilized in the beverage industry for both alcoholic and non-alcoholic products. Caps and closures serve multiple functions: they extend product shelf life, protect against contaminants and moisture, and regulate oxygen levels in packaged goods. As demand continues to rise, the market is expected to experience further growth during the forecast period.

- Bottled water is one of the fastest-growing beverage categories in terms of volume. This increasing consumer demand for bottled water is expected to drive the need for tamper-proof caps and closures during the forecast period. The growing awareness of health and wellness among consumers has shifted from sugary drinks to healthier alternatives, with bottled water being a primary beneficiary of this trend. Additionally, concerns about water quality in some regions have further boosted the demand for bottled water, necessitating robust packaging solutions.

- The modern consumer's "on-the-go" lifestyle has driven demand for lightweight, user-friendly packaging solutions. Custom caps and closures manufacturers are responding with lighter and more efficient designs. The global market growth is further propelled by increasing demand for various beverage types. These trends have led to packaging innovations, including recyclable materials and designs catering to e-commerce needs. The custom caps and closures market continues evolving, meeting consumer preferences and product requirements across diverse industries.

- Moreover, changes in lifestyle patterns and increased per capita consumption fuel the expansion of the bottled water market. Urbanization, busy lifestyles, and the convenience of bottled water have contributed to its popularity. As consumers increasingly opt for on-the-go hydration, manufacturers are responding by offering a variety of bottle sizes and innovative closure designs that ensure product safety and ease of use. This trend will likely continue, driving further growth in the tamper-proof caps and closures market for bottled water packaging.

- Technological advancements in plastic packaging have led to significant innovations in product development within the industry. Many companies invest heavily in research and development activities to create unique and cost-effective products, resulting in increased market innovations. However, the growing concern over climate change has led to stringent government regulations on plastic usage for packaging. These regulations are expected to be the primary constraint on the growth of the beverage caps and closures market during the forecast period.

Beverage Caps And Closures Market Trends

Bottled Water Segment Holds a Significant Market Share

- The bottled water market is expected to register the most substantial gains among major beverage types in developed markets like the United States and developing areas such as India and Indonesia. This growth is driven by increasing health consciousness, convenience, and concerns about tap water quality in some regions. In the financial year 2023, Indian Railways Catering & Tourism Corporation Ltd. (IRCTC) produced over 357 million units of bottled water, nearly doubling their production from 198.60 million units in 2022. This significant increase reflects the rapidly expanding bottled water market in India.

- The growing market for bottled water is creating increased demand for plastic caps and closures, particularly within the expanding bottled water segment. Caps and closures play a crucial role in maintaining the quality and safety of bottled water, preventing contamination, and ensuring freshness. As bottled water consumption continues to rise globally, manufacturers of plastic caps and closures are likely to see sustained growth opportunities. This trend is further supported by innovations in cap design, such as tamper-evident features and improved sealing technologies, which enhance product safety and consumer confidence.

- The ongoing transition from glass to plastic containers is expected to boost demand for plastic caps and closures in the beverage market. This shift is driven by plastic's advantages, including its lightweight nature and ability to reduce product loss through breakage. In the broader market, metal caps will continue to dominate, particularly as the preferred closure for beer bottles. The wine industry is likely to see an increase in metal roll-on screw cap usage, primarily due to the growing popularity of single-serve wine bottles.

- Moreover, bottled water is one of the beverage categories with the fastest growth in terms of volume globally. There would be a rise in the consumer demand for bottled water, raising the need for tamper-evident caps and closures in the forecast period. The bottled water market's growth is fueled by changes in lifestyle and per capita consumption. The competitive rivalry in the market for bottled water is intensified by the increasing presence of international competitors like Coca-Cola, Danone, Nestle, PepsiCo, and Nongfu Spring.

- Technology advancements in plastic packaging have resulted in innovations in product development in the beverage industry. Many companies are investing significantly in R&D activities to develop unique and cost-effective products, and innovation in this space is increasing significantly.

- Many other major companies, such as Amcor and Ball Corp., follow similar strategies and offer new and innovative final products. With innovations in the industry, the demand for products is also growing, thus driving the growth of caps and closures in the beverages industry around the globe.

Asia-Pacific to Register Major Growth

- The Asia-Pacific caps and closures market is dominated by China, with India and Japan following closely behind. Several key factors drive this leadership position. First, the beverage industry's increasing demand for bottled water and packaged drinks has significantly boosted the market. Second, adopting high-performance materials in cap and closure manufacturing has enhanced product quality and functionality. Third, the market benefits from a wide range of material compositions, allowing for versatility in packaging solutions.

- China's economic growth has played a crucial role in shaping the market landscape. As the country's economy continues to expand rapidly, middle-class families are experiencing a substantial increase in their disposable incomes. This rise in purchasing power has led to higher consumption of packaged goods, particularly beverages, driving the demand for caps and closures. The trend is expected to continue, further solidifying China's position as the market leader in the Asia region.

- The Asia-Pacific caps and closures market is experiencing expansion, primarily driven by increasing beverage consumption and population growth. The region's beverage industry has grown enormously over the past decade, attributed to rising disposable incomes. This trend is expected to continue throughout the forecast period, influenced by evolving consumer preferences, particularly the growing demand for energy and nutritional drinks.

- The plastic caps and closures market in this region has been driven by rapid urbanization, population growth, and increasing alcohol demand. Additionally, the region's adoption of recyclable plastic materials for caps and closures is expected to rise as industries increasingly emphasize plastic recycling and sustainability. In the financial year 2023, whiskey had the highest sales volume among various spirits in India, exceeding 250 million cases. Brandy, in contrast, had a sales volume of approximately 82 million cases. The country's overall spirits market sales approached 400 million cases. This growing trend creates demand for caps and closures for various alcoholic beverages.

- A recent survey by Bericap indicates that China's expanding middle class is demanding more sophisticated products, particularly in the packaging industry, which requires plastic components like caps and closures. Consequently, China's plastic industry is undergoing a comprehensive transformation, focusing on technology and environmentally friendly concepts. The market is experiencing a trend toward attractive colors and printing. Companies are increasingly emphasizing the production of eye-catching packages, as the color, shape, texture, graphics, and printing of products communicate brand identity and differentiate them from competitors on store shelves.

Beverage Caps And Closures Industry Overview

The beverage caps and closures market is fragmented, with firms varying for customers by offering competitive prices and cutting-edge products. Crown Holdings Inc., Berry Global Inc., Aptar Group Inc., Evergreen Packaging Inc., and Global Closure Systems are a few of the market's biggest companies. Due to R&D investments, new market efforts, global presence, production sites and facilities, production capabilities, and product launches, the market is competitive.

- June 2024: BERICAP broadened its international footprint by setting up new production facilities in Africa, South America, and Southeast Asia. The company launched new plants in Nairobi, Kenya, and Ho Chi Minh City, Vietnam, and also acquired established production units in Lima, Peru, and Durban, South Africa. These strategic moves brought BERICAP's total to 30 production sites in 25 countries, ensuring customers benefit from localized project support, logistics, and services.

- March 2024: Amcor Capsules, a worldwide leader in crafting closures and capsules for wine and spirits, marked the 60th anniversary of its STELVIN aluminum screw cap range. Launched in 1964 in Chalon-sur-Saone, France, the STELVIN cap heralded a pivotal evolution in the wine industry.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHT

- 4.1 Market Overview

- 4.2 Industry Supply Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Beverage Consumption in Developing Economies

- 5.1.2 Technological Advancements and Innovative Packaging Solutions

- 5.2 Market Restraints

- 5.2.1 Stringent Regulations on the Usage of Plastic caps and closures

6 MARKET SEGMENTATION

- 6.1 By Material

- 6.1.1 Metal

- 6.1.2 Plastic

- 6.1.3 Other Materials (Rubber, Cork)

- 6.2 By Application

- 6.2.1 Beer

- 6.2.2 Wine

- 6.2.3 Bottled water

- 6.2.4 Carbonated soft drinks

- 6.2.5 Dairy products

- 6.2.6 Condiments and sauces

- 6.2.7 Other Applications

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 Germany

- 6.3.2.2 United Kingdom

- 6.3.2.3 France

- 6.3.3 Asia-Pacific

- 6.3.3.1 China

- 6.3.3.2 Japan

- 6.3.3.3 India

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.5.1 Brazil

- 6.3.5.2 Mexico

- 6.3.5.3 Colombia

- 6.3.6 Middle East and Africa

- 6.3.6.1 United Arab Emirates

- 6.3.6.2 Saudi Arabia

- 6.3.6.3 South Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Crown Holdings Inc.

- 7.1.2 Berry Global Inc.

- 7.1.3 Aptar Group Inc.

- 7.1.4 Global Closure Systems

- 7.1.5 Silgan Holdings Inc.

- 7.1.6 Bericap GmbH & Co. KG

- 7.1.7 Guala Closures Group

- 7.1.8 Ball Corporation

- 7.1.9 Amcor Group

- 7.1.10 Pact Group

- 7.1.11 Albea Group

- 7.1.12 Tetra Laval International