|

시장보고서

상품코드

1851590

은행용 사물인터넷(IoT) : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Internet Of Things In Banking - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

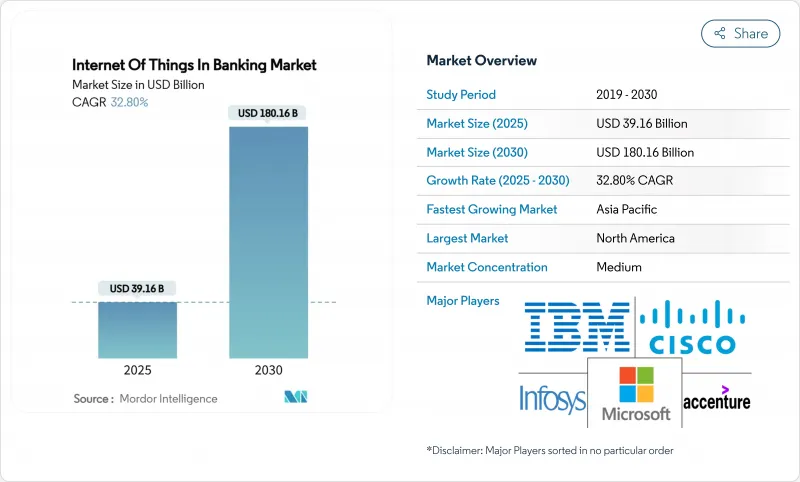

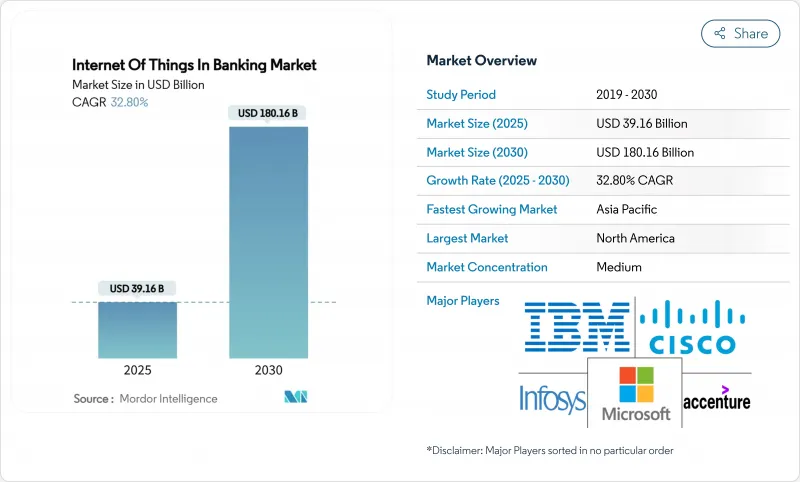

은행용 사물인터넷(IoT) 시장은 2025년에 391억 6,000만 달러, 2030년에는 1,806억 1,000만 달러에 이르고, CAGR 32.8%를 나타낼 것으로 예측됩니다.

이 성장 속도는 은행이 센서를 많이 사용하는 운영 모델, 실시간 데이터 흐름, 금융 서비스와 일상적인 장치 사용을 연결하는 임베디드 결제로 이동하고 있음을 반영합니다. 은행은 ATM과 지점, 모바일 단말기에 커넥티드 센서를 탑재해, 현금 업무의 효율화, 컨텍스트를 의식한 오퍼의 개시, 자동차나 스마트 가전으로부터의 결제의 자동화를 도모하고 있습니다. 2026년 4월 발효의 소비자 금융보호국(CFTB)의 오픈은행 규제를 필두로, 규제 강화의 움직임은 타사 개발자가 IoT 신호와 은행 데이터를 융합할 수 있도록 하는 API의 준비를 가속화하고 있습니다. 유럽에서는 PSD3 및 결제 서비스 규제 방안에 따라 강력한 인증 요건을 확대하고 IoT 대응 거래를 위한 안전한 레일을 구축하는 것이 병행하여 의무화되고 있습니다. 반도체를 둘러싼 공급망의 제약과 5G의 배포의 편차는 여전히 디바이스의 전개를 억제하고 있지만, 센서의 비용 저하와 엣지 컴퓨팅의 진보는 은행 시장에서 사물 인터넷의 지속적인 확대를 10년을 통해 시사하고 있습니다.

세계의 은행용 사물인터넷(IoT) 시장 동향과 인사이트

옴니채널 고객 경험 추진

은행은 ATM, 모바일 앱, 웨어러블에 센서를 설치하여 물리적 환경과 디지털 환경을 원활하게 오가는 여행을 실현. NatWest는 5,500대의 ATM을 19인치 터치스크린과 라이브 텔레메트리로 업그레이드했으며 다운타임이 발생하기 전에 경고를 발행했습니다. 또한 고객이 시선과 제스처를 사용하여 자금을 이동할 수 있도록 Apple Vision Pro용 소매 은행 앱도 출시했습니다. 이러한 통합을 통해 금융기관은 지리적 위치 정보, 기기의 건강 상태, 구매 패턴을 혼합하여 필요를 예측할 수 있게 되었으며, 성숙한 롤아웃에서는 크로스셀의 정확도가 3분의 1로 향상되었습니다. 센서 분석을 통해 내점 전 지점 직원 배치, 대기행렬 경고, 고객 만족도를 2자리 올리는 동적 맞춤형 오퍼가 가능합니다. 이러한 이유로 은행용 사물인터넷(IoT) 시장은 사용자 정착률을 높이고 운영 비용을 줄이는 이점을 누리고 있습니다.

실시간 사기 감지 및 보안

분산 센서는 밀리초 단위로 의심스러운 패턴으로 플래그를 지정하는 비정상 엔진에 공급됩니다. 디바이스의 원격 측정과 트랜잭션 스트림을 결합한 연합 학습 모델은 개인 정보 보호를 위해 데이터를 로컬로 유지하면서 96.3%의 무단 감지 정확도를 달성합니다. 스마트 카메라와 환경 센서가 ATM과 현금 자동 예금을 모니터링하여 스키밍 장비와 변조 팁이되는 비정상적인 온도 상승을 감지합니다. 에지에서 적용되는 블록체인 해시는 분쟁 해결을 위한 불변의 로그를 생성하고, 디바이스의 AI는 한때 고객을 괴롭힌 오감지를 줄입니다. 조기 도입 기업에서는 도입 초년도에 20% 이상의 사기 피해 삭감이 보고되고 있습니다. 보안 긴급성은 지속적인 투자를 촉구하고 은행 시장에서 사물 인터넷을 사이버 범죄와 관련된 주저함으로부터 강화하고 있습니다.

데이터 프라이버시 및 사이버 보안에 대한 우려

EU의 사이버 탄력성 방법은 제조업체에 자동 보안 업데이트를 탑재한 장치의 출하를 의무화하고 있으며, 무선 패치 적용을 유지할 수 없는 벤더가 노출하고 있습니다. 은행은 캘리포니아의 소비자 프라이버시 법에서 인도의 디지털 개인 데이터 보호법에 이르기까지 다양한 규칙을 추적해야 하며 컴플라이언스의 오버헤드가 증가합니다. 세분화이 취약하다면, 단일 센서의 침해는 은행의 코어를 약화시킬 수 있습니다. Federated-learning의 테스트 운영은 원시 데이터를 내보내지 않고도 99.94%의 모델 정밀도를 보여주지만, 대부분의 금융기관은 디바이스 플릿의 보안 확보에 있어 여전히 스킬 갭에 직면하고 있습니다. 사이버 보험료의 상승은 프로젝트 비용을 증가시키고 은행용 사물인터넷(IoT) 시장에서 채용을 지연시킬 수 있습니다.

부문 분석

2024년 매출의 58%는 서비스였으며 전문 지식, 규제에 대한 인사이트, 24시간 체제 지원이 복잡한 롤아웃의 성과를 좌우하는 것으로 나타났습니다. 서비스 은행용 사물인터넷(IoT) 시장 규모는 레거시 코어 및 클라우드 패브릭에 센서를 통합하는 통합업체 수요를 반영하여 CAGR 33.37%를 나타낼 것으로 예측됩니다. 은행은 위험을 줄이기 때문에 위협 모델링, 컴플라이언스 매핑 및 장치 수명주기 거버넌스를 아웃소싱하는 경우가 많습니다. 솔루션은 하드웨어 키트, 소프트웨어 플랫폼, 연결성 번들 및 금융 기관이 On-Premise 데이터센터를 폐지할 수 있는 클라우드 네이티브 변화의 혜택을 누리고 있습니다. IBM-Wipro의 AI 지원 플랫폼과 같은 공동 오퍼는 애널리틱스와 사이버 하드닝을 번들로 제공하여 솔루션 제공업체 간의 경쟁을 강화하고 있습니다.

2세대의 도입에서는 종량 과금의 매니지드 서비스가 선호되고, 중소 은행은 설비 투자가 큰 자사 구축보다 턴키 번들을 채용하게 되어 있습니다. 벤더는 엣지 컴퓨팅 노드에 개방형 은행 API용 사전 인증 커넥터를 패키징하여 가치 실현 시간을 단축합니다. 하드웨어 이자율은 여전히 얇기 때문에 공급업체는 장치 모니터링 및 예측 유지 보수를 중심으로 연금 모델로 축 발을 옮깁니다. 클라우드 벤더가 금융 등급 에지 스택을 출시함에 따라 은행용 사물인터넷(IoT) 시장은 서비스 중심의 경제성에 더욱 기울어지고 있습니다.

보안 용도는 2024년 매출의 36.2%를 차지했고, CAGR은 34.73%를 나타냈습니다. 보안 은행용 사물인터넷(IoT) 시장 규모는 2025년에 141억 7,000만 달러에 이르고, 2030년에는 710억 달러 이상에 달할 것으로 예상됩니다. 스마트 ATM은 온도 이상, 충격 이벤트, 변조 패턴을 감지하고 디스펜서를 자동으로 잠글 수 있습니다. 디바이스 레벨 암호화 및 트러스트 칩 루트는 현재 프리미엄 터미널에 기본적으로 탑재되어 컴플라이언스 감사에 소요되는 시간을 단축하고 있습니다.

모니터링, 데이터 관리 및 고객 경험의 각 모듈은 인프라를 공유하지만 분석 능력은 다양합니다. 은행은 원격 측정을 활용하여 지점의 에너지 사용을 최적화하고 전력 비용을 전년 대비 최대 12% 절감하고 있습니다. 고객 경험 엔진은 풋 트래픽 센서와 CRM의 이력을 연결하여 지점 내에서 개인화된 인사를 실시합니다. 동일한 센서 그리드에서 여러 용도를 호스팅하는 통합 플랫폼은 전반적인 TCO를 줄이고 은행 시장에서 사물 인터넷 전체의 매력을 넓힐 수 있도록 도와줍니다.

세계의 은행용 사물인터넷(IoT) 시장 보고서는 구성 요소별(솔루션 및 서비스), 용도별(보안, 모니터링, 기타), 조직 규모별(대기업 및 중소기업), 최종 사용자별(소매 은행, 기업 은행, 투자 은행 등), 지역별로 분류됩니다.

지역 분석

북미가 2024년 매출액의 38.5%를 차지해 선두를 유지, 견조한 사이버법제와 핀테크와 은행의 조기 제휴가 뒷받침했습니다. 센서 대응 지점에서는 생산성이 30-40% 향상되고, 양자 평가판 알고리즘은 기존의 옵티마이저보다 1,000배 고속으로 동작합니다. 캐나다에서는 커넥티드 커뮤니티 ATM에 의한 캐시 서클 인클루전이 진행되고, 멕시코에서는 거래 수수료를 삭감하는 IoT 기반의 송금 키오스크가 활용되고 있습니다. 은행용 사물인터넷(IoT) 시장에서는 연방정부가 5G의 미정비지역으로의 확대를 지원하고 대륙간의 지연격차가 평평해지고 있습니다.

아시아태평양은 성장 엔진이며 CAGR 33.86%로 약진하고 있습니다. 중국의 AIBank는 IoT 데이터를 수집하고 대출을 개인화하는 마이크로 서비스 코어로 1억 명 이상의 고객에게 서비스를 제공합니다. 인도에서는 엣지 미니 데이터센터를 전개하고, 광섬유가 드문 농촌에 모바일 은행을 확대하고 있습니다. 동남아시아의 슈퍼 앱은 라이드 헤일링, 푸드 딜리버리, 인스턴트 크레딧을 융합해, IoT 센서가 드라이버의 퍼포먼스를 추적해 다이내믹한 보험 가격 설정을 실현합니다. 현지 규제 당국이 샌드박스 승인을 급격히 진행하고 은행용 사물인터넷(IoT) 시장이 스마트폰의 보급률 상승을 확실히 파악합니다.

유럽에서는 프라이버시와 ESG의 진전이 예측됩니다. PSD3와 PSR은 인증과 API의 조화를 의무화하고 장치의 안전한 온보딩을 촉진합니다. 각 기관은 에너지 모니터링 센서를 통합하여 탄소 발자국을 측정하고 그물 제로 로드맵에 대한 헌신과 일치시킵니다. 장치 제조업체는 절전 칩을 통합하여 IoT의 전력 소비에 대한 모니터링을 지원합니다. 라틴아메리카와 중동 및 아프리카의 신흥 지역에서는 결제의 근대화 프로그램과 모바일 머니 제도가 비약적인 전개를 가능하게 하는 토양이 되고 있습니다. 예를 들어, 브라질의 PIX와 나이지리아의 eNaira 레일에서는 IoT 엔드포인트가 실시간 결제를 시작할 수 있어 은행용 사물인터넷(IoT) 시장의 수익원이 다양해지고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 옴니채널 고객체험 추진

- 실시간 부정 감지 및 보안

- 규제상의 오픈은행의무

- 센서에 의한 지점/ATM 비용 최적화

- IoT를 활용한 임베디드 결제(자동차나 가전제품)

- 엣지 애널리틱스 주도의 초퍼스널라이즈드 마이크로 렌딩

- 시장 성장 억제요인

- 데이터 프라이버시와 사이버 보안에 대한 우려

- 디바이스/플랫폼의 상호 운용성의 갭

- 지방의 5G 지연 병목

- IoT 에너지 소비에 관한 ESG 조사

- 밸류체인 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 주요 이용 사례와 사례 연구

- 대출 인수를 위한 원재료 재고 추적

- 유연한 대출 조건을 위한 팜 아웃풋 분석

- IoT를 활용한 사이버 공격 방지 시스템

- 소매 은행 정세

- Beacon 대응 ATM 사전 발표(JPM 체스)

- 신체의 불편한 고객을 위한 지점내 내비게이션(버클레이즈)

- Beacon에 의한 미이용 점포의 재생(미국 은행과 시티)

제5장 시장 규모와 성장 예측

- 구성 요소별

- 솔루션

- 서비스

- 용도별

- 보안

- 모니터링

- 데이터 관리

- 고객 경험 관리

- 기타 용도

- 조직 규모별

- 대기업

- 중소기업

- 최종 사용자별

- 소매 은행

- 기업 은행

- 투자 은행

- 비은행 금융회사

- 보험

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ASEAN

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- IBM Corporation

- Microsoft Corporation

- Cisco Systems Inc.

- Oracle Corporation

- Accenture plc

- Temenos AG

- Infosys Limited

- Software AG

- Vodafone Group plc

- Tibbo Systems

- SAP SE

- Capgemini SE

- Intel Corporation

- Amazon Web Services

- FIS Global

- NCR Atleos

- Thales Group

- Diebold Nixdorf

- HPE(Aruba)

- Huawei Technologies

제7장 시장 기회와 향후 전망

KTH 25.11.13The Internet of Things in Banking market stands at USD 39.16 billion in 2025 and is forecast to reach USD 180.61 billion by 2030, advancing at a 32.8% CAGR.

The growth pace mirrors banks' shift toward sensor-rich operating models, real-time data flows, and embedded payments that link financial services to daily device usage. Institutions are layering connected sensors on ATMs, branches, and mobile endpoints to streamline cash operations, trigger context-aware offers, and automate payments initiated from vehicles and smart appliances. Regulatory push, notably the Consumer Financial Protection Bureau's open-banking rule effective April 2026, is accelerating API readiness that lets third-party developers fuse IoT signals with banking data. Parallel mandates in Europe under PSD3 and the proposed Payment Services Regulation expand strong-authentication requirements and create secure rails for IoT-enabled transactions. Banks that orchestrate these capabilities report 30-40% efficiency gains and 20-30% uplifts in product-recommendation hit rates when omnichannel IoT programs mature.Supply-chain constraints around semiconductors and uneven 5G rollout still temper device deployments, yet falling sensor costs and edge-compute advances point to sustained expansion of the Internet of Things in the Banking market through the decade.

Global Internet Of Things In Banking Market Trends and Insights

Omnichannel Customer-Experience Push

Banks wire sensors into ATMs, mobile apps, and wearables to create journeys that pivot seamlessly across physical and digital environments. NatWest upgraded 5,500 ATMs with 19-inch touchscreens and live telemetry that flags downtime before it occurs. The bank also released a retail-banking app for Apple Vision Pro so clients can move funds using gaze and gesture. Such integrations let institutions blend geolocation, device health, and purchase patterns to anticipate needs, lifting cross-sell accuracy by one-third on mature rollouts. Sensor analytics enable pre-visit branch staffing, queue alerts, and dynamic personalized offers that raise customer satisfaction scores by double digits. The Internet of Things in Banking market, therefore, benefits from higher user stickiness and reduced operating costs.

Real-Time Fraud Detection and Security

Distributed sensors feed anomaly engines that flag suspicious patterns in milliseconds. A federated-learning model combining device telemetry with transaction streams now achieves 96.3% fraud-detection accuracy while keeping data local for privacy. Smart cameras and environmental sensors guard ATMs and cash machines, detecting skimming devices or abnormal temperature spikes that hint at tampering. Blockchain hashes applied at the edge create immutable logs for dispute resolution, and on-device AI reduces false positives that once annoyed customers. Early adopters report fraud-loss reductions of more than 20% in the first implementation year. Security urgency propels continual investment, fortifying the Internet of Things in the Banking market against cybercrime-related hesitancy.

Data-Privacy and Cybersecurity Concerns

The EU Cyber Resilience Act obliges manufacturers to ship devices with automatic security updates, exposing vendors that cannot maintain over-the-air patching. Banks must track diverging rules from California's Consumer Privacy Act to India's Digital Personal Data Protection law, adding compliance overhead. Breaches at a single sensor can undermine banking cores if segmentation is weak. Federated-learning pilots show 99.94% model accuracy without exporting raw data, but most lenders still face skills gaps in securing device fleets. Rising insurance premiums for cyber coverage inflate project costs and can slow adoption within the Internet of Things in Banking market.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Open-Banking Mandates

- IoT-Enabled Embedded Payments (Cars and Appliances)

- Device / Platform Interoperability Gaps

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services hold 58% of 2024 revenue, underscoring that domain expertise, regulatory insight, and 24-hour support tilt outcomes in complex rollouts. The Internet of Things in Banking market size for services is projected to expand at 33.37% CAGR, reflecting demand for integrators who stitch sensors into legacy cores and cloud fabrics. Banks often outsource threat modeling, compliance mapping, and device-life-cycle governance to reduce risk. Solutions cover hardware kits, software platforms, and connectivity bundles, and they benefit from cloud-native shifts that let lenders retire on-premises data centers. Joint offers, such as IBM-Wipro's AI-enabled platform, bundle analytics and cyber hardening, amplifying competition among solution providers.

Second-generation deployments favor pay-as-you-grow managed services, pushing smaller banks to embrace turnkey bundles rather than capex-heavy in-house builds. Vendors are packaging edge-compute nodes with pre-certified connectors for open-banking APIs, trimming time to value. Hardware margins remain thin, so suppliers pivot to annuity models around device monitoring and predictive maintenance. As cloud vendors release financial-grade edge stacks, the Internet of Things in Banking market further tilts toward service-centric economics.

Security applications captured 36.2% of 2024 revenue and expand at 34.73% CAGR, riding regulatory imperatives and growing attack vectors. The Internet of Things in Banking market size for security reached USD 14.17 billion in 2025 and is forecast to exceed USD 71 billion by 2030. Smart ATMs detect temperature anomalies, shock events, or tampering patterns and can lock dispensers automatically. Device-level encryption and root-of-trust chips now ship by default in premium terminals, reducing compliance audit time.

Monitoring, data management, and customer experience modules share infrastructure but vary in analytics heft. Banks leverage telemetry to optimize branch energy use, cutting power costs by up to 12% year over year. Customer-experience engines marry foot-traffic sensors with CRM histories to trigger in-branch personalized greetings. Integrated platforms that host multiple applications on the same sensor grid help reduce overall TCO, broadening appeal across the Internet of Things in the Banking market.

The Global Internet of Things in Banking Market Report is Segmented by Component (Solutions and Services), Application (Security, Monitoring, and More), Organization Size (Large Enterprises and Small and Medium Enterprises), End User (Retail Banking, Corporate Banking, Investment Banking, and More), and Geography.

Geography Analysis

North America retains leadership with 38.5% of 2024 revenue, buoyed by solid cyber legislation and early fintech-bank partnerships. Sensor-enabled branches post 30-40% productivity uplifts, and quantum-trial algorithms run 1,000 times faster than legacy optimizers. Canada advances cash-circle inclusion through connected community ATMs, while Mexico leverages IoT-based remittance kiosks that cut transaction fees. The Internet of Things in Banking market sees federal support for 5G expansion into underserved zones, flattening latency disparities across the continent.

Asia-Pacific is the growth engine, charging ahead at 33.86% CAGR. China's AIBank serves more than 100 million customers on microservices cores that ingest IoT data to personalize lending. India deploys edge mini-data centers to extend mobile banking into rural districts where fiber remains sparse. Southeast Asian super-apps fuse ride-hailing, food delivery, and instant credit, with IoT sensors tracking driver performance for dynamic insurance pricing. Regional regulators fast-track sandbox approvals, ensuring the Internet of Things in Banking market captures rising smartphone penetration.

Europe predicates progress on privacy and ESG. PSD3 and the pending PSR impose mandatory authentication and harmonized APIs, fostering secure device onboarding. Institutions integrate energy-monitoring sensors to gauge carbon footprints, aligning with commitments to net-zero roadmaps. Device makers embed power-thrifty chips, addressing scrutiny over IoT electricity draw. In emerging regions of Latin America and the Middle East and Africa, payments modernization programs and mobile-money regimes create fertile ground for leapfrogging deployments. For instance, Brazil's PIX and Nigeria's eNaira rails allow IoT endpoints to initiate real-time payments, diversifying revenue sources within the Internet of Things in Banking market.

- IBM Corporation

- Microsoft Corporation

- Cisco Systems Inc.

- Oracle Corporation

- Accenture plc

- Temenos AG

- Infosys Limited

- Software AG

- Vodafone Group plc

- Tibbo Systems

- SAP SE

- Capgemini SE

- Intel Corporation

- Amazon Web Services

- FIS Global

- NCR Atleos

- Thales Group

- Diebold Nixdorf

- HPE (Aruba)

- Huawei Technologies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Omnichannel customer-experience push

- 4.2.2 Real-time fraud detection and security

- 4.2.3 Regulatory open-banking mandates

- 4.2.4 Branch/ATM cost-optimization via sensors

- 4.2.5 IoT-enabled embedded payments (cars and appliances)

- 4.2.6 Edge-analytics-driven hyper-personalized microlending

- 4.3 Market Restraints

- 4.3.1 Data-privacy and cybersecurity concerns

- 4.3.2 Device / platform interoperability gaps

- 4.3.3 Rural 5G latency bottlenecks

- 4.3.4 ESG scrutiny on IoT energy consumption

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Key Use-cases and Case Studies

- 4.8.1 Tracking raw-material inventory for loan underwriting

- 4.8.2 Farm-output analytics for flexible lending terms

- 4.8.3 IoT-driven cyber-attack prevention systems

- 4.9 Retail Banking Landscape

- 4.9.1 Beacon-enabled ATM pre-announce (JPM Chase)

- 4.9.2 In-branch navigation for disabled customers (Barclays)

- 4.9.3 Beacon revival of under-used branches (US Bank and Citi)

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.2 Services

- 5.2 By Application

- 5.2.1 Security

- 5.2.2 Monitoring

- 5.2.3 Data Management

- 5.2.4 Customer Experience Management

- 5.2.5 Other Applications

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By End User

- 5.4.1 Retail Banking

- 5.4.2 Corporate Banking

- 5.4.3 Investment Banking

- 5.4.4 Non-Banking Financial Companies

- 5.4.5 Insurance

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Russia

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 ASEAN

- 5.5.4.6 Rest of Asia Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 IBM Corporation

- 6.4.2 Microsoft Corporation

- 6.4.3 Cisco Systems Inc.

- 6.4.4 Oracle Corporation

- 6.4.5 Accenture plc

- 6.4.6 Temenos AG

- 6.4.7 Infosys Limited

- 6.4.8 Software AG

- 6.4.9 Vodafone Group plc

- 6.4.10 Tibbo Systems

- 6.4.11 SAP SE

- 6.4.12 Capgemini SE

- 6.4.13 Intel Corporation

- 6.4.14 Amazon Web Services

- 6.4.15 FIS Global

- 6.4.16 NCR Atleos

- 6.4.17 Thales Group

- 6.4.18 Diebold Nixdorf

- 6.4.19 HPE (Aruba)

- 6.4.20 Huawei Technologies

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment